Investment markets and key developments over the past week

Shares pulled back a bit over the last week not helped by some disappointing earnings results from US tech stocks and surprise inaction by the Bank of Japan. Shares had become overbought so were due a bit of a pause or pull back. This wrapped up a mostly positive month for shares with good gains in Europe, Australia and the US, but falls in Japanese and Chinese shares. Bond yields were mixed over the last week: up in the Eurozone, but down in the US and Australia. The oil price continued to recover as the $US fell, but the $A got hit by heightened RBA rate cut expectations following lower than expected March quarter inflation.

The big surprise over the last week was the decision by the Bank of Japan to not undertake more monetary easing despite soft economic data, inflation well below target, strength in the Yen and the earthquakes. Maybe the BoJ is waiting to assess a fiscal response from the Japanese Government and get the May 26-27 G7 summit to be held in Japan out of the way. Our assessment is that more BoJ easing is just a matter of time. Failure to do more soon though risks unwinding all the progress on inflation expectations seen under Abenomics, particularly with the Yen breaking to ever higher levels.

By contrast the Fed’s April meeting delivered no surprises, with the Fed remaining gradual. A June rate hike is unlikely as US data probably won’t have improved enough by then and markets may be nervous given the Brexit vote on June 23. The US money market’s assessment of just a 26% probability of a July hike appears a bit low though – I would think it’s around 50%. The key message from the Fed is that it will not do anything that upsets the outlook for global and US growth.

Australian inflation (or deflation) has set the RBA up for a rate cut on Tuesday, or at least it should have. While it would be wrong to conclude that Australia is on the brink of sustained deflation – as falls in petrol and fruit prices won’t be repeated – the big surprise in the March quarter inflation data was that price weakness was broad based with underlying inflation running at its lowest annual rate on record. Both headline and underlying inflation are now running well below the RBA’s 2-3% inflation target. The risk is that thanks to a combination of deflationary pressures globally, soft demand domestically and very weak wages growth, inflation could remain well below target for an extended period. This is a risk the RBA cannot ignore and is best to address early before inflation expectations fall too far and under target inflation becomes entrenched. As a result, we think that the RBA should, and most likely will, cut the official cash rate by 0.25% taking it to 1.75% when it meets on Tuesday. But it’s not just low inflation that justifies a rate cut. Other reasons include the risk of a soft spot in growth later in the year as housing slows, the still too strong $A and to offset upwards pressure on bank mortgage rates from higher bank funding costs. Will the banks pass a cut on in full? Probably not – “funding cost” arguments may see only 0.15% or so of a 0.25% cut passed on.

Major global economic events and implications

Here we go again – another weak start to the year for the US economy with March quarter GDP up just 0.5% annualised with weakness in capex, inventories and trade. This was pretty much as expected and needs to be seen in perspective given that weak March quarter growth has been the norm over the last 20 or so years with average growth of 1% annualised ahead of a rebound to average 3% growth in the June quarter. So far the evidence is mixed though as to whether growth in the current quarter is rebounding. In the past week we have seen weak readings for new home sales, durable goods orders and consumer confidence but solid readings for the services conditions PMI, pending home sales and the goods trade deficit and continued very low readings for jobless claims. At present though, it’s all consistent with the Fed remaining very gradual.

US Q1 earnings have seen some mixed high profile results for tech stocks but have generally been better than expected. 58% of S&P500 stocks have now reported with 77% beating on earnings and 57% beating on sales.

Eurozone bank lending ticked up and economic sentiment rose both of which are consistent with ongoing modest growth.

Japanese data was messy with strong labour market readings (although this may be due partly to a declining labour force) and a rebound in industrial production but a dip in inflation back into negative territory, a fall in core inflation to just 0.7% year on year, poor household spending and a fall in small business confidence. The impact from the Kumamoto earthquakes won’t be helping and so further monetary easing is still needed.

Australian economic events and implications

Apart from the much lower than expected March quarter inflation data, export and import prices both fell more than expected pushing the terms of trade down yet again, producer price inflation remained low and credit growth remained moderate. In fact annual growth in credit to property investors is now less than that to owner occupiers.

What to watch over the next week?

In the US, the big focus will be on the ISM manufacturing conditions index Monday and labour market data Friday. Regional surveys point to a fall back in the April ISM manufacturing index to around 51, leaving it still well above the low of 48 seen in December but April jobs growth is likely to remain solid with a 200,000 gain in payrolls, unemployment remaining at 5% and wages growth edging up slightly.

In China, a further slight increase is expected in the official manufacturing conditions PMI (Sunday) for April and the Caixin manufacturing PMI (Tuesday).

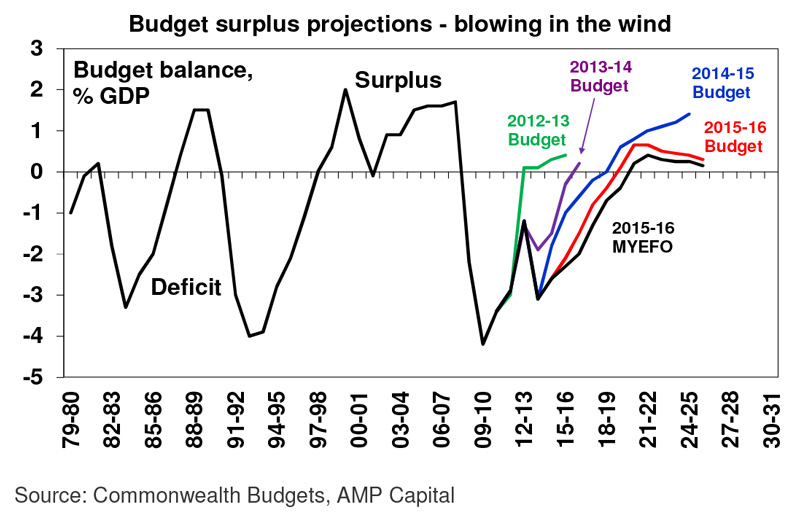

In Australia, after the RBA Board meeting (see above), the focus will shift to the 2016-17 Federal Budget on Tuesday night. This budget is more significant than usual for two reasons. First, it will likely be the Government’s main economic statement ahead of a likely July 2 election and as such the Government will want to include some sweeteners. Second, because it comes after several years that have seen the return to surplus pushed out further and further, the ratings agencies are losing patience with the threat of a downgrade to our sovereign AAA rating if they are not happy. And the ratings agencies have a point. We are now looking at a 12-13 year run of budget deficits which swamps the 7 years seen in the 1990s and the 5 years in the 1980s. And this despite not even having had a recession. Rather we have done this thanks largely to a “dumb country” combination of politicians ramping up spending commitments on a whole range of things without facing up to how they will be paid for.

These two considerations point in opposite directions. And so it will be a difficult balancing act for the Government.

Fortunately some improvement in the jobs outlook and the iron ore price should offset lower wages growth to allow this Budget to be the first in several years to more or less hold the line on the last set of budget projections, which in this case are the MYEFO projections from late last year. As such, we expect the 2016-17 deficit projection to come in around $34bn (2% of GDP) and that for 2017-18 to be around $23bn. The return to surplus could be pushed out to 2021-22 though. The Government is likely to forecast 2016-17 GFP growth of 2.75%.

Key measures are likely to include: raising the $80,000 income tax threshold slightly; removal of the deficit levy on schedule next year; a crackdown on tax avoidance by multinationals to fund cutting the corporate tax rate; reduced superannuation concessions for high income earners; a hike in tobacco excise; and more funding/inducements for infrastructure spending likely involving some form of partnership with private sector partners that want to take advantage of the Governments low borrowing costs. Overall, the Government is expected to aim for a cap on revenue as a share of GDP and to limit spending growth in contrast to the Labor opposition which is more likely to focus on growing tax revenue (via reduced access to negative gearing, the capital gains tax discount and superannuation) to fund increased spending.

Should the Government worry about maintaining its AAA rating? Yes. Its loss may not ultimately have much impact on government borrowing rates. And if a downgrade knocks the $A down that would be good. So no worries here. Rather the real concern would be that the loss of the rating would signal an undoing of all the work in the 1980s and 1990s by political leaders on both sides of politics to set public finances onto a sustainable path.

On the data front in Australia, expect the CoreLogic RP data home price index to show continued modest growth in home prices in April and the AIG manufacturing conditions PMI and NAB business conditions index to fall back slightly from the high levels seen in March (all Monday), building approvals (Tuesday) too fall slightly, a 0.3% gain in March retail sales and a fall in the March trade deficit to a still big $2.9bn (both Thursday). The RBA will release is quarterly Statement on Friday which will be watched for downwards revisions to inflation forecasts.

Outlook for markets

Expect short term share market volatility to remain high as we head into May (“sell in May and go away, come back on St Leger’s Day”), global growth remains fragile and the Fed eventually starts to soften markets up for another rate hike. However, beyond near term volatility, we still see shares trending higher this year helped by a combination of relatively attractive valuations, further global monetary easing and continuing moderate global economic growth.

Very low bond yields point to a soft medium term return potential from them, but it’s hard to get too bearish in a world of fragile growth, spare capacity and low inflation.

Commercial property and infrastructure are likely to continue benefitting from the ongoing search by investors for yield.

Capital city residential property price gains are expected to slow to around 3% this year, as the heat comes out of Sydney and Melbourne. Prices are likely to continue to fall in Perth and Darwin, but price growth is likely to pick up in Brisbane.

Cash and bank deposits are likely to provide poor returns.

The ongoing delay in Fed tightening poses further short term upside risks for the $A, particularly if the RBA does not ease rates soon. However, any further short term strength in the $A is unlikely to go too far and the broad trend is likely to remain down as the interest rate differential in favour of Australia narrows as the RBA resumes cutting the cash rate and the Fed eventually resumes hiking, commodity prices remain in a secular downswing and the $A undertakes it’s usual undershoot of fair value.

By Shane Oliver, AMP Capital