Fixed income investments have long held a central role in a diversified portfolio. Whether government or corporate bonds, or shorter-dated bank bills, fixed income is an important source of income and diversification for investors.

Direct investment has traditionally been the domain of professional investors; however, recent Fintech developments have brought direct investment in fixed income within reach of retail investors. In this article, OpenMarkets examines the asset class and discusses one of the newest listed fixed income investments, XTBs.

What is fixed income?

A central tenet of modern portfolio theory is diversification, both within and across asset classes, and fixed income investments are traditionally included in a diversified portfolio; investors and advisers like the capital stability and predictability of returns that fixed income can deliver.

A fixed income investment is a loan made by an investor to a government or corporate borrower in exchange for a fixed rate of interest for a fixed amount of time…hence such investments are called fixed income or fixed interest securities.

There are a number of terms you may hear when fixed income is being discussed:

- Issuer: The entity that sells fixed income securities to raise money for its operations. Issuers are responsible for making interest or coupon payments, and to pay the ‘loan’ amount in full when the security matures.

- Coupon: The interest rate of a fixed income security upon issue.

- Maturity: The time period at which a fixed income security will be repaid in full by the issuer.

- Par value: the face value of a fixed income security. Par value determines the maturity value and coupon payments of the security.

- Pull to par: The movement of a fixed income security’s price toward its par value as it approaches its maturity date.

- Duration: A measure of the sensitivity of the price of a fixed-income security to a change in interest rates; generally, the longer the duration, the more sensitive the security is to rising interest rates.

It’s important to note that not all interest rates on fixed income investments are fixed. Some have a floating rate and can fluctuate, comparable to a variable home loan. And as with any investment, some fixed income assets pay higher returns than others, but they generally come with a higher risk of loss. As with any investment, greater risk should equate to higher returns.

How does fixed income work?

At the maturity date, the issuer promises to return the principal amount of each fixed income security to the investor. Fixed income has a natural buyer in the issuer, who is required to pay back the loan (bond) at par value – i.e. the maturity value of a bond – when it reaches its stated maturity date. This gives bonds a greater predictability of returns.

Another benefit of having this natural buyer is that bonds that have sold off (i.e. dropped in value) will naturally ‘pull to par’ or pull back to their par value as the maturity date approaches.

Example: If an investor was to buy a 10 year fixed income security at issue for $100, receive an interest rate (or coupon) of 5%, and hold it to maturity, it would look like this:

If that investor was to sell the bond before the maturity date, they may get more or less than they paid when the bond was issued. This is because the price of a fixed income security has an inverse relationship to interest rates; bond prices and interest rates tend to move in opposite directions.

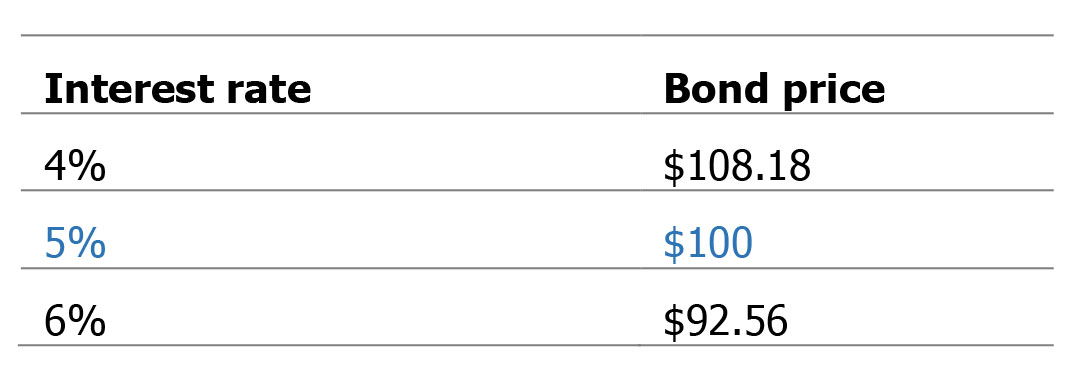

When interest rates rise, bond prices fall; when interest rates fall, bond prices rise. Using the $100 bond example again, a change in interest rates results in the following changes to bond prices:

Direct versus indirect investment

While there are many differences between fixed income securities and equities, there are two significant factors that set them apart:

- Fixed income securities do not require a buyer to determine value, as with equities. A company’s shares are priced according to what investors are willing to way. Fixed income securities have a set price to be paid at maturity.

- Related to this is the fact that fixed interest is a ‘closed-end’ investment – it has a maturity date, unlike shares, which are perpetual.

Therefore, holding equities in an open-end managed fund or exchange traded fund (ETF) makes sense as both the vehicle and the investments therein are likewise perennial, until a corporate event brings about change.

By holding fixed income in a fund, investors automatically lose the bonds’ most fundamental economic feature; the repayment of capital on the maturity date, and the predictability of income and capital return that goes with that.

Holding direct corporate and government bonds converts the uncertain into the certain, providing information on the exact return an investor will receive on the day you implement their investment strategy. This assumes no default, which is not zero risk; it is a lower risk for investment grade bonds in Australia, but may increase for corporate bonds for corporates outside the ASX200.

As the fintech revolution continues a-pace, the door has opened for retail investors to get direct access to exchange traded government and corporate bonds; government bonds are on the ASX using CDIs, and senior corporate bonds are on the ASX using XTBs.

Why corporate bonds?

Corporate bonds share many characteristics with other forms of fixed income…the main differentiator being that they are issued by companies rather than governments or statutory bodies. As a result, corporate bonds can have widely disparate risk profiles, largely linked to financial stability of the business that issues them.

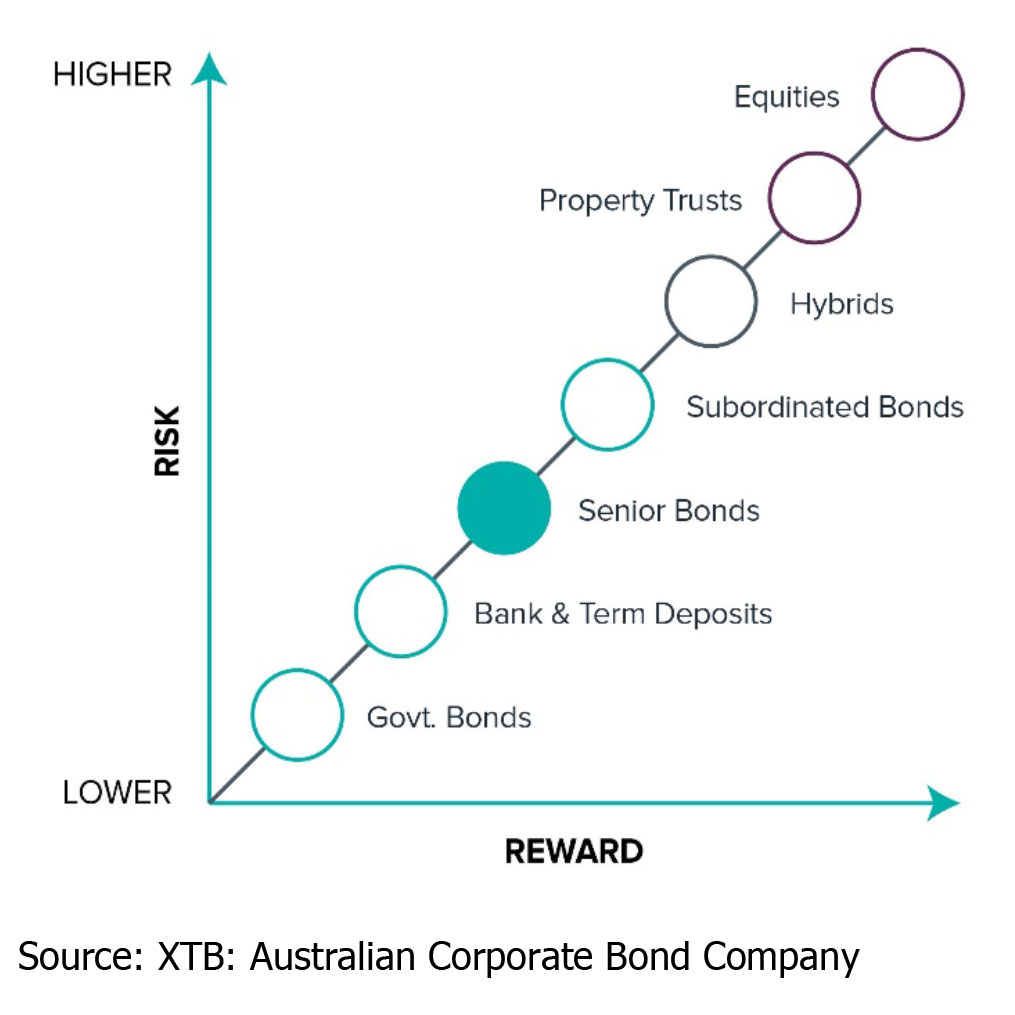

Australian companies can raise money via equity (issuing shares) or debt. This can take two forms – borrowing from the bank or issuing bonds. As illustrated, senior (or corporate) bonds are considered lower risk than equities, and in the unfortunate event of a corporate collapse, holders of bonds are paid out before shareholders.

Example: Qantas downturn ~ equity versus debt market reactions

A complete disconnect can exist between debt and equity when it comes to news that detrimentally, or positively impacts a company’s general business. In late April 2016, Qantas announced a downturn in its domestic capacity. This sent Qantas shares tumbling by 11% on the day, a significant move for a company of that size.

Credit spreads for Qantas bonds (the yield gap between them and government bonds) widened by just 5 basis points. Excluding the accrued interest earned that day, this would have translated into a 0.21% loss for the bond holders. In other words, there was minimal impact.

The question the bond market asks about such disclosures is – ‘will this have a meaningful impact on the issuer’s ability to meet its senior debt obligations?’ The answer was obviously ‘no’ from the lack of any significant reaction.

If it doesn’t significantly impact a firm’s ability to meet its debt obligations, then bond holders know they’re getting paid, otherwise the company is in default.

Senior bonds are really just securitised loans to the corporate, which is why they have relatively low volatility and lack of reaction to a great deal of corporate disclosure.

XTBs

Issued by the Australian Corporate Bond Company (ACBC), XTBs (Exchange Traded Bond units) provide individual investors with access to the returns of individual corporate bonds; they’re securities traded on the ASX that bring together the predictable income from corporate bonds with the transparency and liquidity of the ASX market.

Usually the domain of institutional investors, financial advisers can now pick and choose which corporate bonds they’d like to include in clients’ portfolios in the same way they select shares; buying XTBs on the ASX is just like buying shares or exchange traded funds.

XTBs provide investors with the income and capital repayment of specific ASX100 corporate bonds, including Telstra, Woolworths and BHP. The performance of each XTB closely follows its individual bond counterpart in the wholesale market. Each XTB has the same maturity date and coupon payment frequency as its corporate bond – for example, a 3-year corporate bond with a coupon of 5% translates to a 3-year XTB with a coupon of 5%.

Once an investment decision has been made, the order for an XTB is executed in the same way as for other ASX-traded securities; transactions are settled through CHESS and each XTB is listed on the investor’s CHESS account.

XTB trading recently passed the $100 million milestone. The prevailing low interest rate environment world-wide, coupled with the continued GFC hangover, is driving the need for higher-yielding, lower volatility products. XTBs over corporate bonds are a relatively stable and predictable income-generating security.

With financial institutions struggling to offer three percent on the average term deposit, XTBs outstrip cash accounts; and without the price volatility of other income generating investments such as shares and hybrids. As with all fixed income, a change in interest rate will impact the price of XTBs, as illustrated in the following table.

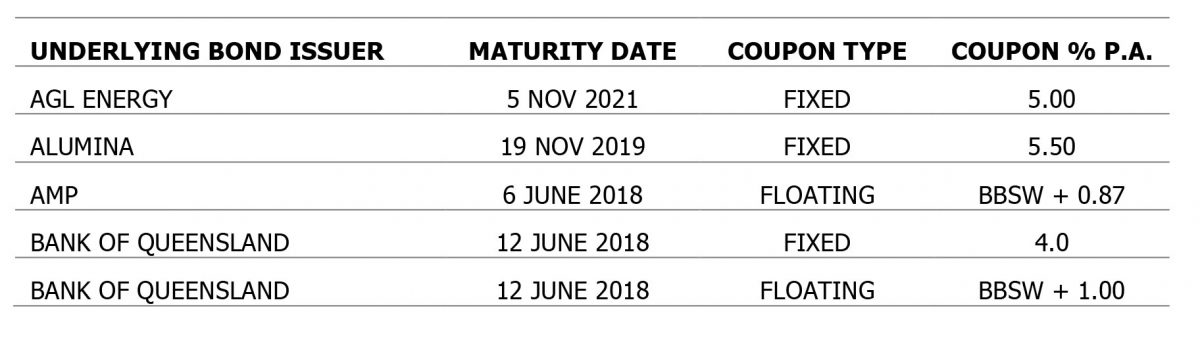

ACBC currently offers 49 XTBs, including two ‘green’ XTBs over corporate bonds committed to using the funds for purposes that meet the requirements of the Climate Bonds International Standards and Certification Scheme. The XTBs comprise 10 floating-rate and 39 fixed-rate, across a broad range of familiar ASX-listed companies, including:

The yield and price of each XTB will reflect the yield and price of the underlying bond, after fees and expenses. For fixed-rate XTBs, the fees are 0.4% of the face value of the bond for the life of the bond, and 0.2% for floating-rate XTBs.

As little as $100 can be invested in each XTB you select (broker dependent). Financial advisers recommending XTBs can create a portfolio or use one of four XTB model portfolios that have been created to meet different investment objectives. Alternatively, the XTB website offers an interactive cash flow tool that enables you to build a bespoke XTB model portfolio and map its cash flows. That way, you can be sure to meet your clients’ income needs.

XTBs are yet another great example of a business using technology to make investment more accessible, at a reasonable price, to all investors.

———