Sander Bus

The US economy is growing above its potential. Job openings are now exceeding the number of unemployed workers. In this environment it is no surprise that the Fed is continuing to hike. Tighter dollar liquidity is putting pressure on non-US issuers that rely on dollar funding. At the same time the ECB is still reluctant to tighten monetary policy more aggressively.

Divergence between global bond markets has increased in the last three months with US spreads tightening further, while Europe and especially emerging markets have underperformed. We do not believe that the negative correlation between the US and international credit markets can continue indefinitely and would argue that US spreads should widen. We reaffirm our belief – made in our last outlook for Q3 – that the tightest spreads in this cycle are now behind us. And although there is no reason to expect a full- blown crash anytime soon, spreads are likely to widen gradually.

Market technicals are still weak. The fact that the Fed is on a hiking path and the ECB’s quantitative easing is drawing to a close are not helping fixed income as an asset class. The huge supply of US Treasuries could crowd out other financial assets and US investment grade (IG) is right in the line of fire. It makes you wonder who will be the marginal buyer of credit and fixed income in general in such an environment. US insurance companies and pension funds could be potential candidates as they may have an incentive to increase fixed income allocations now that coverage ratios have improved. However, overall we would still conclude that technicals are negative for our asset class.

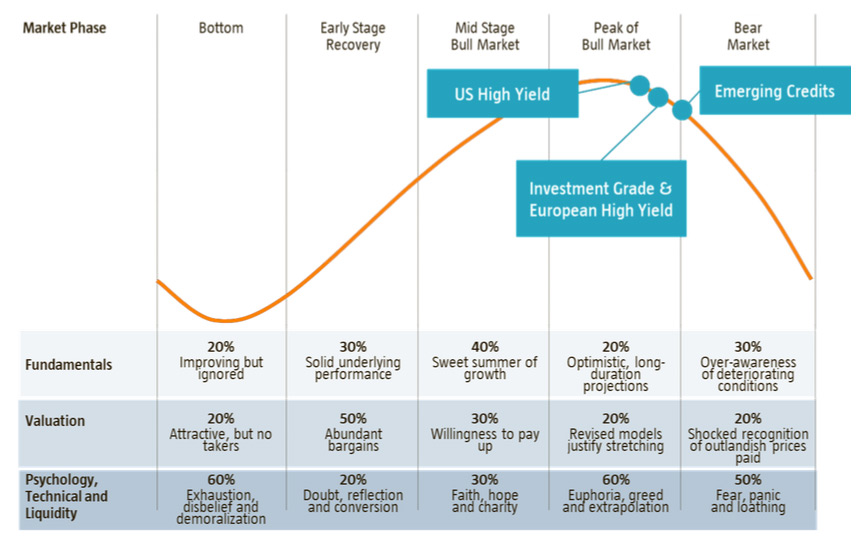

As always, our outlook is divided into three sections: fundamentals, valuations and technicals. But first, here’s where we think the main credit markets are in the cycle.

Figure 1 | The Market Cycle: mapping our view on market segments

Source: Robeco, Morgan Stanley, September 2018

Where are we in the credit cycle?

We continue to see indications that the cycle is maturing and still feel that spreads probably reached their tightest levels last January. Of course, It is notoriously difficult to predict the exact point at which the cycle will turn and the depth of the ensuing bear market, but since we believe spreads will grind wider we have placed the dots in the bear market phase. This does not mean that there are not still opportunities, however. In this sort of environment, we can expect pockets of the market to occasionally reprice quite aggressively and if such situations result in buying opportunities we will not hesitate to take advantage of these. US high yield has held up well compared to other bond segments, but we think that here too spreads will eventually follow those in other parts of the market and start to widen.

Fundamentals: Economic slack is a thing of the past

In this chapter we look at economic fundamentals, such as economic growth, inflation expectations, debt levels and dollar liquidity.

We are living in interesting times. A number of long-term trends seem to have reached an inflection point. Ten years on from the Global Financial Crisis, there is no longer any slack in the economy. Labor markets have recovered and monetary stimulus is being reversed. Another long-term trend also seems to be coming to an end. Globalization. This has helped to keep inflation low and economic growth high. It was good for corporate profits and financial markets but blue-collar workers suffered. With Trump at the helm this is changing. He is determined to bring the supply chain ‘home’ by increasing trade barriers. The long-term effects will probably be higher inflation (through higher wages) and lower global growth. The short-term effects of lower tax rates, deregulation and a pick-up in capex have propelled risky assets but we do not believe this will be a positive development for markets in the longer term.

US: steaming ahead – but how long can it go it alone?

The US economy is growing well above potential, which heightens the risk of inflation. But as yet figures have remained rather muted, with core CPI ex-shelter still at just 1.3%. However, wages are now definitely moving higher so it will just be a matter of time until this is reflected in the overall figures. And we should not overlook the extent to which inflation is a lagging variable: it could be with us before we are fully aware of its presence.

US investment grade leverage has increased rapidly. In the past, leverage has always peaked in a recession when EBITDA levels have dipped. So in the current environment, it is striking that leverage is now already above previous peaks, while EBITDA continues to grow at a healthy pace.

M&A related debt issuance is one of the main culprits for the heightened leverage. Rating agencies have been quite relaxed about accepting leverage that is ‘temporarily’ at an elevated level. The risk is that this will trigger downgrades if companies do not deliver on their promises to reduce leverage should we move into a more adverse economic environment.

Earnings growth is solid but headwinds will increase going forward, with margins likely to shrink as wage pressure creeps in and input costs rise. But as EBITDA margins are at a high level, we do not see a corporate crisis as one of the major risks.

The US consumer is in a strong position as reflected by consumer sentiment indices. Strong labor markets and wage growth support the consumer. Income growth in the US stands at 5% due to wage growth of around 3% in addition to the increase in the number of jobs.

Europe: political risk overshadows economic fundamentals

Political risk in Europe is still elevated. The political situation in Italy is still reason for concern and could have a significant destabilizing effect, especially on other peripheral markets. The ECB wants to avoid a flare up of a sovereign debt crisis at any price.

Business sentiment in Europe is still positive but industrial production growth has come down. Despite the strong labor market data, consumer spending has continued to slow, but should be supported by wage growth, which is now starting to gain momentum. Core Inflation has so far remained range bound and although it could trend higher on the back of higher wages, the ECB is not under huge pressure to hike interest rates too quickly or aggressively.

At company level, profits are still solid so from a credit perspective there is not too much to worry about in terms of corporate health although it seems unlikely growth will accelerate. European corporates have also been much more conservative in using leverage than their US counterparts, which should make them more resilient in the event of a market turn down.

Emerging Markets: dollar squeeze and China slowdown

Emerging markets are clearly suffering from a reduction in dollar liquidity, with countries that depend on foreign funding (Turkey, Argentina) really feeling the pain. Several have been forced to hike rates in order to stem weakness in their own currencies. The collateral damage if this trend continues is severe economic slowdown.

We cannot talk about emerging markets without spending some time on China. One indicator which highlights the weaker growth in the Chinese economy is the demand for industrial metals. These indices have been declining since the second quarter. They reflect the lower demand for metals in China, which is accompanying a sharp decline in infrastructure spending.

The policy options still open to the Chinese authorities to stem the weakness are also limited. Monetary loosening is no real solution as this would weaken the currency too much at a time when the Fed is hiking. A weak renminbi is referred to as the ‘nuclear option’ as it could spark a widespread currency crisis across Asia. Stimulating credit growth is not an attractive alternative either as China is trying to clamp down on excessive leverage, especially via shadow banking, in the corporate and local government space. The one remaining option could be fiscal stimulus in the form of tax reform. All in all, it will be quite tough for China to avoid a prolonged period of slower growth.

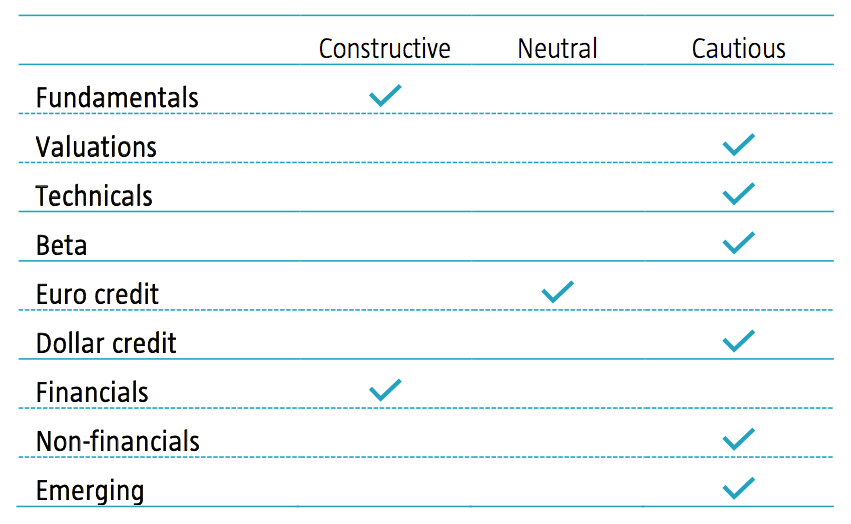

Valuation: Better value to be found in European credit

In this section we look at valuations – which market segments look rich and which offer room for spread tightening?

Spreads in Europe have widened slightly further in the last three months but are still not cheap in historical terms. US credit has continued to outperform and can now be classified as outright expensive. We have also seen wider spreads in emerging markets although this weakness has mainly been in a selective group of high yield countries.

While we conclude that the market as a whole is still not cheap, it is interesting to look at ratios and make some comparisons. If we divide US IG spreads by European IG spreads we see that the ratio has dropped from 1.7 to 1.0 since the start of the year and a very similar shift has occurred in high yield spreads. On a cross-currency-hedged basis we can conclude that European credit is now cheap relative to US dollar credit. In the case of high yield, it is also important to realize that it’s not just a case of a better spread in Europe; the quality of debt is much better too. The average credit rating in the European high yield market is BB, whereas the US market is dominated by single Bs. So we maintain our overweight in Europe, even though the position has not played out so far this year.

Risk on in US High Yield

Since the start of the year CCC have outperformed significantly in the US high yield market. This is clear evidence of the risk on sentiment in the US. CCC also outperformed as this category is perceived to be less sensitive to interest rate increases than higher rated credits. However, at current valuation levels, CCC credit spreads are not offering sufficient compensation for an average default scenario in the next five years and so we avoid this category as much as we can.

Nor are we convinced that the worst is behind us for emerging markets. Spreads are still not wide enough across the board, but we are prepared to selectively take positions in bonds that have undergone significant repricing. For example, we have recently picked up a few high-quality Turkish and Chinese credits that got dragged down by the broader Turkish market turmoil.

For a long time now, we have had a preference for investment grade financials. This is still the case as we still find relatively attractive investment opportunities in this segment. Within financials we will move some exposure to more senior parts of the capital structure as there are some attractively priced senior preferred and senior non-preferred new issues.

Technicals: ongoing headwinds for credit

In this chapter we discuss technical factors, such as global reduction in US dollar supply, increased Treasury issuance and increasing hedging costs.

Although corporate profitability is still strong we believe that the dominant factor for credit will be weaker market technicals. A reduction in central bank liquidity is still the key driver for markets and Fed policy does not only result in higher rates, it also leads to lower dollar excess reserves. The impact of this is mainly felt by oversees US dollar borrowers. It is therefore not surprising that the first cracks have started to appear in the offshore dollar market for some high-risk dollar borrowers (i.e. Turkey and Argentina).

A second technical that has the potential to hurt credit markets is the huge supply of US Treasuries being used to finance the country’s fiscal deficits. Buyers will be found for these issues – they will be priced to ensure that this is the case and other fixed income categories could be crowded out as a result. A somewhat mitigating factor is the relatively mild supply of corporate debt.

Higher short-term dollar rates are also continuing to have an impact on hedging costs. Cross- currency-rate differentials determine the costs of hedging and these have clearly expanded. The logical effect will be a lower demand for US fixed income, at least until repricing causes these to revert to more acceptable levels.

In previous outlooks we have extensively discussed the end of quantitative easing in Europe. This event is well flagged but still important for the market. The ECB’s CSPP and PSPP programs are now in their final stages. In the foreseeable future, the biggest net buyer of European credit will limit it’s purchasing to just reinvesting coupons and redemptions. European IG spreads have already widened significantly from their tightest levels in early 2018 in anticipation of this.

Ballooning BBB universe

Another market technical we discussed is the massive growth of the BBB universe in both Europe and in the US. Since 2010, This segment of the market has more than tripled in Europe and more than doubled in the US. In itself, this is not a major issue. But if the tide turns in the market and rating agencies are forced to take action, the relatively small high yield market could be inundated with a wave of ‘fallen angels’ as companies lose their IG status. Given the still solid outlook for corporate profitability, this is not a theme that should upset markets in the short run, but in a weaker market environment it could make matters worse.

As a final point we would like to discuss interest rate coverage. According to this metric, credit quality still looks sound although coverage levels have slipped somewhat due to higher debt levels. Rising EBITDA is a mainstay for interest-rate coverage ratios as are the declining average coupon levels. However, we have now reached a point where new issues no longer print at a lower coupon and, although this is a gradual process, we should realize that the tailwind offered by refinancing into lower coupons is behind us. For companies that use leveraged loans as a main funding source (an increasing number of companies are loan-only financed) the coverage ratio will decline much more rapidly in an environment of rising Libor rates. This adds an additional vulnerability to the loan market, which is already rife with aggressive financing structures and over leveraged businesses.

Our conclusion is unchanged from our previous quarterly outlook. Technicals continue to look vulnerable.

Conclusion & positioning: caution in world of shrinking liquidity

How will we be positioning our credit portfolios in the coming quarter?

Cautious positioning despite improved valuations

Valuations have become slightly better in Europe and emerging markets, but not enough to justify a more aggressive positioning. Caution is warranted in a world of shrinking liquidity. In the new era of tighter monetary policy, we are probably going to see more instances of aggressive de-risking in pockets of the market. This can offer opportunities in situations where repricing has caused markets or individual issues to overshoot. We will be on the look out for these opportunities as they arise and will be proactive in taking advantage of them. At the same time, we will also make sure that our portfolios are defensively positioned. We expect most of these opportunities to arise in the emerging markets space.

Euro credit is cheaper in relative terms

Hedging costs for US assets are high and this makes Euro denominated assets look cheap on a relative basis. Our preference for Europe extends to both the investment grade and high yield segments.

Quality financials look attractive

In Europe, we see still see value in financials, although we are very selective in terms of the quality of the issuers in which we invest. Within this space we are increasingly seeing value outside the most junior parts of the capital structure, so we have move some investments into senior preferred and senior non-preferred debt.

Conclusion

All in all, these are quite challenging times for credit markets. Tighter global monetary policy, diverging growth patterns in the major economic regions, shrinking dollar liquidity and increasing competition from US Treasuries could crowd out credit. However, in general, fundamentals remain solid, especially for corporates, so there is no cause for undue panic and a scenario of gradually rising spreads offers opportunities for us to find value in those pockets of the market that reprice to more attractive levels.

Guests

We would like to thank the guests who contributed to this new quarterly outlook with their valuable presentations and discussions. The views of Torsten Slok (Deutsche Bank), Shobhit Gupta (Barclays), Guy Stear (Societe Generale) and Rikkert Scholten (Robeco) have been taken into account in establishing our credit views.

By Sander Bus, Co-head Credit team, and Victor Verberk, Co-head Credit team