Victor Verberk

Key highlights:

- Global debt is near cyclical highs

- Despite weaker than expected data, markets rallied – a typical bear market rally

- The bar to cutting rates is low, with central banks desperate to avoid a recession

- Corporate margins are under pressure, an earnings recession in the making.

- The Q1 2019 rally looks increasingly like a dead cat bounce

Despite the weaker than expected macro data, risk assets have performed very well since the start of the year. So why have markets bounced so vigorously? A dovish Fed shift, expectations for a China trade deal and the backdrop of an oversold market late last year all help explain.

We see the current rally as typical of bear markets. Nearly all bear markets have occasional rallies, and they are often sharp and painful, just like episodes of spread widening. Sentiment in credit bear markets swings much more wildly in both directions.

In times such as these, when thorough issuer selection pays off, the market will increasingly distinguish between winners and losers. We construct our portfolios cautiously.

We are also conscious of the fact that it is expensive to be underweight. But rather than succumbing to the temptation to be long for the carry, we prefer to get prepared so we can return quickly after markets have repriced.

Companies enjoyed multiple years of expanding margins. Profits as a share of GDP rose to record levels. But those days are over. With wages rising faster than inflation, corporate margins are under pressure. Even consensus equity analyst estimates expect an earnings recession. Central banks are prepared to take aggressive steps in order to raise inflation and have become more responsive to developments in financial markets. But, aside from the moral hazard that this creates even larger asset bubbles in the future, the growth in floating rate markets, such as leveraged loans, means cutting rates may create its own unintended consequences. In our view, this is a dead cat bounce. The downside of this policy, is that it can lead to bubbles and create bigger problems down the road.

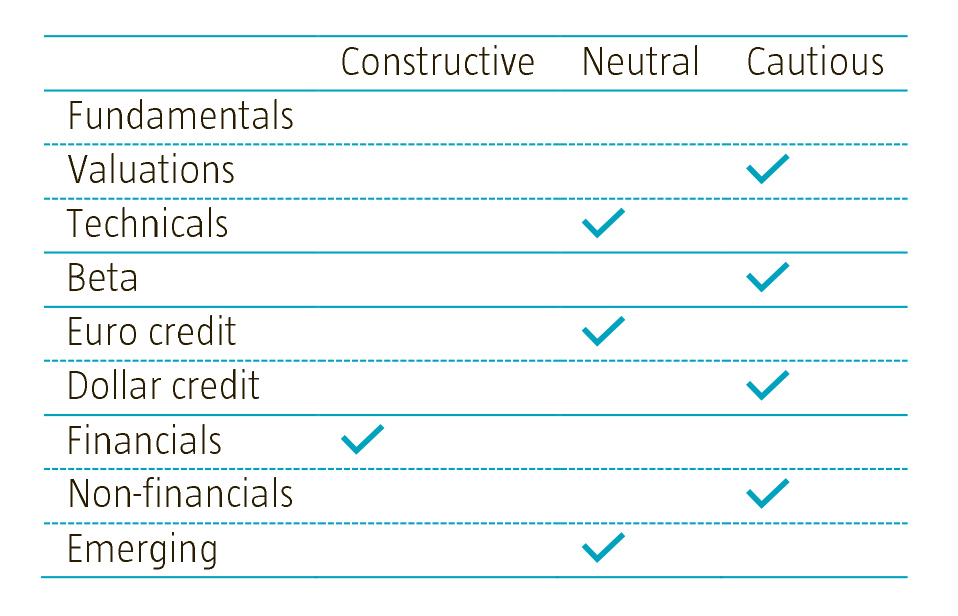

Fundamentals: earnings recession around the corner

In this part we look at economic fundamentals, such as economic growth, inflation expectations, debt levels and dollar weakness.

The key question for investors and policymakers is whether we are in a soft patch or at the beginning of an extended period of weak economic data. Central banks seem worried, as demonstrated by their reaction to the weak data. It has become clear that the Fed rate hike in December was a policy error which they have sought to correct with dovish speeches, forward guidance and the announcement of a gradual end to quantitative tightening. The ECB lowered its growth forecast and implemented a TLTRO and China has stepped on the gas as well with fiscal and monetary stimulus. It is clear that policymakers are very eager to prevent a recession. Whether or not they actually can, is questionable.

US

Leverage for US investment grade companies, measured as debt/EBITDA is now well above previous peak levels. High leverage is worrisome when profitability is still very sound, because leverage will go even higher once the economy slows and profits start to drop. In 2018, companies benefited from lower taxes but they did not pro-actively deleverage in the good times. On the contrary, in many cases they did the opposite, as evidenced by the amount of debt-funded mergers and acquisitions and share buy-backs. This is a typical end- cycle phenomenon: debt rises during the boom years, then earnings fall once growth slows, causing leverage to shoot higher.

At this stage in the cycle, the biggest risks are weakening earnings and, eventually, downgrades (investment grade) and defaults (high yield). We think this is now playing out as evidenced by the many profit warnings that have been issued. Equity analyst consensus estimates are now forecasting a 3.7% year-over-year earnings decline for Q1, with several sectors seeing double digit declines (energy, materials and tech). That is what is referred to as an earnings recession. Margins are under pressure as wage increases can neither be offset by higher selling prices nor by gains in productivity.

But will an earnings recession also mean an economic recession? That is a very hard question to answer and an answer might not even be required in order to predict market developments. An increase in perceived recession risk is enough to make credit markets widen. We see some red flags that point to an increased risk of recession. For example, there is a huge negative gap in consumer confidence between current conditions and expectations. Historically, gaps of this size have always been followed by recessions. We see similar patterns in Germany in the Ifo survey. And the NY Fed themselves model a 1 in 4 and rising probability of recession within the next twelve months given the flatness of the front and intermediate parts of the Treasury yield curve.

So the Fed is very eager to raise inflation and, if they can, to gently steepen the yield curve. We believe that the bar for cutting rates is very low. When further macro weakness becomes evident, which is likely, the Fed will probably cut rates. That could temporarily help sentiment and maybe even extend the cycle, but it most likely will not prevent the earnings recession from happening.

Europe

Europe is much more dependent on global trade than the US. This helps to explain the disappointing economic data from Germany, centered on weak export orders. Year to date, European data has continued to deteriorate, but the recent monetary and fiscal stimulus in China should help to improve things somewhat going forward. It is worth noting that European companies have been comparably more disciplined when it comes to debt-funded mergers and acquisitions and, in particular, share buy-backs. So even though European corporations are more exposed to a global slowdown, their balance sheets are generally less vulnerable than their US counterparts. Political risk is as always an issue in Europe. The Brexit process, May elections and Italian sovereign questions all remain outstanding, even if markets are fairly relaxed on this front currently. The rise of non-centrist politics is still a theme that should not be overlooked. It is a long term challenge to the status quo which could reverse the economic benefits of global trade and globalization.

Emerging markets

In emerging markets, both private and public sector debt ratios have continued to move up at an alarming pace. Excessive debt is a ticking macroprudential time bomb for a number of economies. Emerging market dollar-denominated debt as a share of both GDP and exports is now as high as it was in the late 1990s. Waves of stimulus have caused total debt in China to soar to a staggering 270% of GDP. Since most of the new credit has been used to finance fixed-asset investment, China has ended up with a severe overcapacity problem. Still, another round of stimulus is currently being implemented and will probably help prevent growth in China from dropping below the lower boundary. Chinese authorities are being more careful this time around as they are conscious of the negative consequences of excessive debt, so measures are focused on partly unwinding some of the tightening policies that were implemented last year and reducing VAT.

Valuation: back to tight levels

In this section we look at valuations – which market segments look rich and which offer room for spread tightening?

Markets have been very volatile since our last quarterly outlook in December. They crashed towards the end of the year and recovered in the first few weeks of the new year almost as quickly as they had come down. At the time of writing, global high yield had a total return of 6.5% year to date, which is more than what most market participants, including us, would have expected for the entire year. We see that spreads for almost all credit categories have again moved to well below long-term averages. US investment grade and high yield spreads are the most expensive at 75% and 71% of the long-term average. We feel that this is expensive given the current point in the cycle. Euro investment grade is the exception with a spread that is currently still close to the long-term average, which we would call a fair valuation.

Within high yield we see a striking disparity between high quality and low quality. CCC rated bonds strongly underperformed during the crash in December.

Interestingly, they continued to underperform on a beta-adjusted basis during the rebound in the first quarter. This is another indication that this is a bear market rally, rather than a genuine recovery. The underperformance of CCCs can be explained by underlying pressure on corporate profitability which for these weak credits immediately challenges the viability of the business model. And it’s not just CCCs: 30yr BBBs have not kept up in beta terms with BBBs across the curve and second lien loans are underperforming too. So we can see at least three signs within the structure of credit markets that 2019’s price action looks like a bear market rally.

For global portfolios we see some tactical value in Asia, as spreads are still wide versus developed markets and this market will benefit the most from the Chinese stimulus program. But longer term, we remain cautious about emerging markets, as many of them are facing unsustainably high debt levels. In developed markets, we continue to favor European markets, since these are more appropriately valued and tend to have better fundamentals in the form of lower leverage. In addition, Europe will benefit more from Chinese stimulus in the short run.

Technicals: selling the rally

In this part we discuss technical factors, such as increasing US dollar hedging costs, investors pulling out of the US and the shift from bank funding to capital market funding.

A dovish central bank usually means risk on. This time was no different, as we have witnessed in the first quarter of 2019. Sentiment had shifted too far in the negative direction at the end of 2018 and investor positioning was very defensive. So it is not surprising that the markets rallied once central banks reversed course. The big question is, is this a bear market rally or not? We believe it is.

As we wrote last time, the credit bear market started in early 2018. Nearly all bear markets have periodic (usually multi-month) rallies, and they are often sharp and painful, just like episodes of spread widening. This is a credit bear market, in our view, where sentiment swings much more sharply in both directions. And as a result, you have to fight the urge to chase the market when everything starts to feel much better, as it does today, unless the fundamental story has truly changed. Also, don’t forget that in an average cycle, the bulk of spread widening actually happens after the hiking cycle is over, because that is when growth weakens the most. So a pause in the hiking cycle is not usually the best time to be adding risk. In fact, of the last seven big bear market rallies we can find, the Fed cut rates in five of them. As for the other two, in 2002, the Fed had already cut by over 400bps and in 2014, rates were still at the lows so the Fed weren’t able to cut.

Fed and ECB easing has pushed rates down and that undoubtedly starts the process of making credit look attractive in relative terms. It is expensive to be underweight credit. This applies even more to Europe where the alternative has a negative yield and where the government curve is still steeper than in the US. It is tempting to pursue the carry trade, but this is not the right time in the cycle to do that. It is akin to collecting pennies in front of a steamroller. At the same time, it is important to understand this technical, as it will mean that investors will probably quickly return after a sell-off.

Apart from central banks there are two other factors that are worth considering. BBB issuance and the state of the leveraged loan market. BBB issuance has ballooned since the financial crisis as investment grade companies have engaged in debt-funded share buybacks and mergers and acquisitions. In many cases, rating agencies have so far been very forgiving and have maintained investment grade ratings on the promise of deleveraging. With the outlook for corporate profitability looking more clouded, it is likely that we will see a large number of fallen angels dropping into the high yield market. That will create opportunities, as these companies have enough levers to pull to ensure their survival, but it is better to avoid this segment now and be very selective in what you buy. This is where having a strong analyst team really helps, where active management can really make a difference.

The leverage loan market is where we see the biggest bubble in today’s credit markets. The US leveraged loan market has ballooned to USD 1.13 trillion, of which more than half has been pooled in collateralized loan obligations, or CLOs. That is not a problem, as long as profitability remains favorable, but today’s lax lending standards will contribute to painful losses in leveraged loans in the next recession. These products have often been sold on the premise of a secure asset class with a floating rate that protects against rising rates. Since central banks have reversed course and money market rates are no longer going up, flows into the loan market have turned significantly negative. So paradoxically, a looser monetary policy stance has actually started to tighten the availability of credit through the leveraged loan market.

Through what transmission channels could weakness in the loan market filter through to bond markets? First, the two markets’ issuers partly overlap. So if loans widen, bonds are likely to follow suit. Secondly, multi-asset credit funds that invest in both categories might have to sell the more liquid bonds if they face outflows since loans are hard to sell. Finally, increased supply in the bond market as companies struggle to refinance maturities in the loan market could also be a means by which bond markets are affected.

Positioning

How will we position our credit portfolios in the coming quarter?

If anything, our conviction is strengthening that spreads will trend wider over the medium term. The fundamental challenges that have built up over the course of a nearly decade-long bull market will gradually rise to the surface, and the credit cycle is starting to turn. After the huge sell-off in December, we added risk early this year. Investment grade portfolios saw their betas climb well above 1 and for high yield we moved the beta to 1. But then in early March, we faded the rally and reduced betas again, taking profits.

We now feel comfortable with a beta of 1 for investment grade and below 1 for high yield. We have a clear preference for Europe over the US for all global portfolios. Our portfolios are defensively constructed. Within investment grade, we still like European financials in core Europe. We expect the underperformance of lower quality, high beta names to continue. This is not the time to reach for yield.

Liquidity in credit markets is still challenging. This means there is a need for a contrarian investment style: sell when things look good and buy when markets get ugly. December was a good example of that. And early March another. We will only know in Q2 if the cat is dead, but for now, it looks decidedly ill.

Guests

We would like to thank the guests who contributed to this new quarterly outlook . The views of Winifred Cisar (Wells Fargo), Michael Anderson (Citigroup), Robert McAdie (BNP Paribas) and Rikkert Scholten (Robeco) have been taken into account in forming our credit views.

By , credit strategist.

———-