Investors should consider local-currency EM debt to counter lack of yield in government bonds For investors trying to find yield in government bond markets, especially in developed markets, life isn’t getting any easier.

It has been 10 years since the end of the financial crisis and into the global economic recovery, and there is still more than $12 trillion worth of government debt trading at negative yields, including in the Eurozone, Switzerland and Japan.

The Emerging Markets Debt team at Eaton Vance, a leading global investment manager, notes: “Even in the U.S., 5-year Treasury yields are negative when deflated by inflation expectations. The situation is not likely to change any time soon. Around the globe, many central banks, including the U.S. Federal Reserve and the European Central Bank, are contemplating looser monetary policy in light of weaker global growth and low inflation.

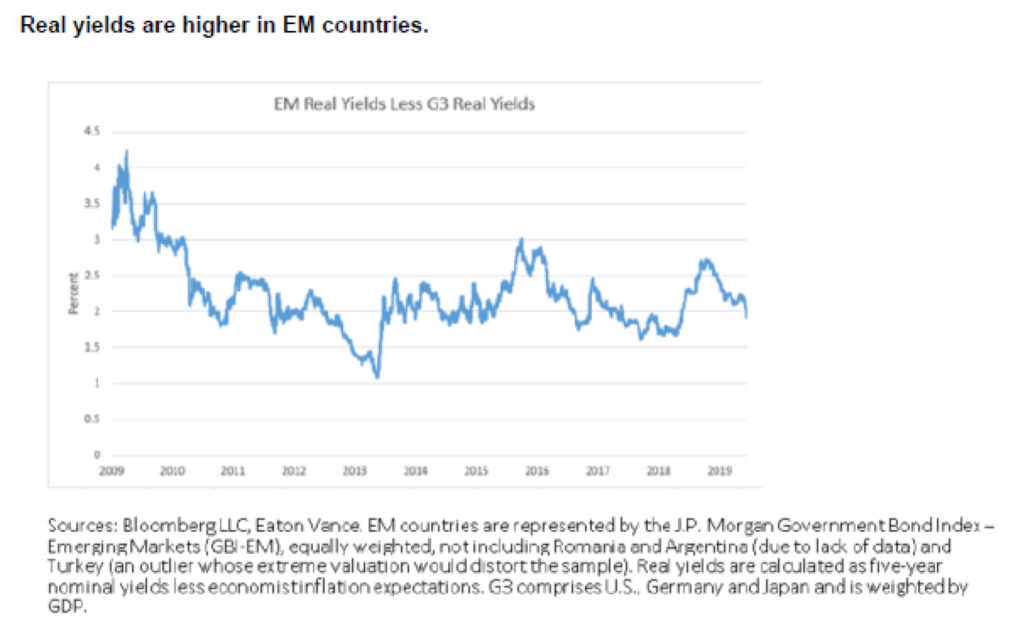

‘Against this backdrop, emerging-markets (EM) local-currency debt offers opportunity, even after the recent rally in yields. The chart below shows that the real yield spread of EM local-currency government bonds over G3 (U.S., Germany, Japan) bonds, as of June 12, was 193 bps. Local currency EM debt carries currency risk but minimal credit risk compared to hard-currency EM debt.”

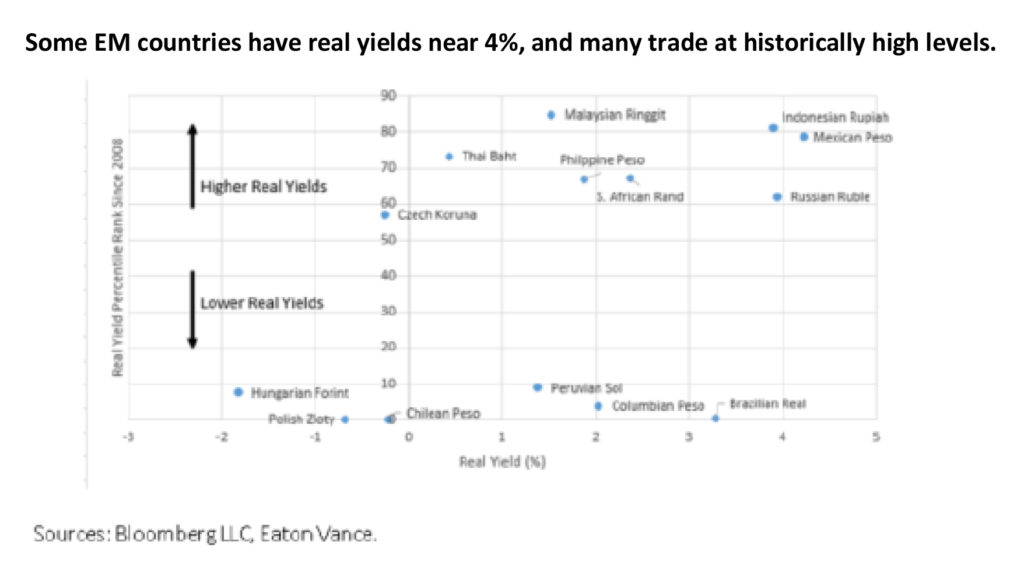

Within the EM debt sector, there is a wide dispersion in yields. For example, real yields in Malaysia, Indonesia and Mexico are in the 80th percentile relative to their levels over the past 10 years, meaning that they are higher than they have been 80% of the time over that period. Other EM countries, like Poland, Hungary and Chile, have real yields near the lows over the past 10 years.

“Investors looking for yield in government bonds who want to minimize credit risk should consider local-currency EM debt. Investors must carefully weigh ever-present political and currency risk in the asset class. But with due diligence, EM debt can offer relief from the negative rate blues in global government bond markets,” says Eaton Vance.