Key Points:

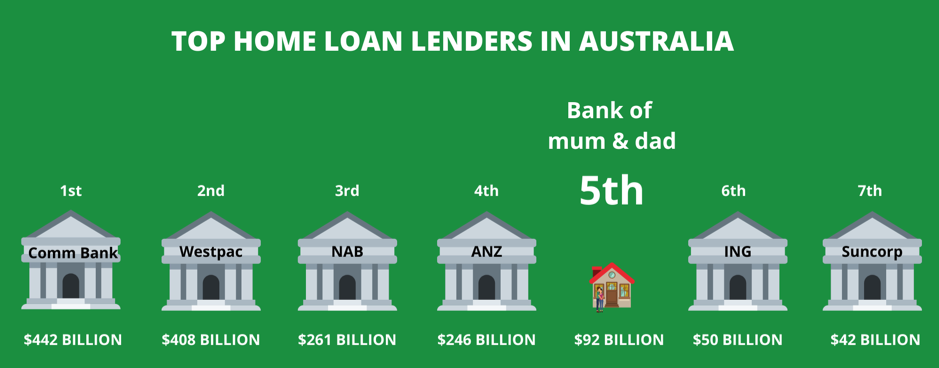

- Bank of Mum and Dad is Australia’s fifth biggest lender, after the Big 4 Banks

- $92.3 billion lent to children to help them onto the property ladder, with 59% of parents not expecting repayment

- Nearly half of parents cutting expenses or delaying retirement in a bid to get their children on the property ladder, one in four facing financial hardship

- Of parents expecting repayment, nearly 20% reported their child is yet to make a repayment

New nationally representative research from comparison site Mozo.com.au has found that the Bank of Mum and Dad is on the rise, after quizzing Australian parents across the country about their financial contributions towards their children. The study found the total amount lent by the Bank of Mum and Dad is up 41% from when parents were last surveyed two years ago.

With 1.2 million parents across the country providing financial assistance totalling $92 billion to help their children step onto the property ladder, the Bank of Mum and Dad is the nation’s fifth largest mortgage lender, sitting behind the big four banks – ANZ, Commonwealth Bank, NAB and Westpac.

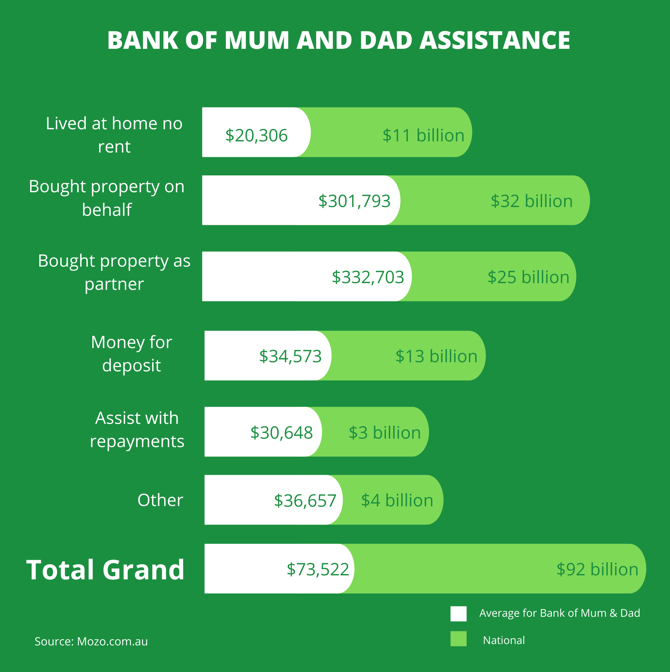

The portion of parents helping their children to buy a home has remained steady between 2017 to 2019, sitting at 29%, however due to an expanding population, the number of parents contributing jumped from 1.02 million in 2017 to 1.2 million in 2019. On average, families lent $73,522 to their children, up $9316 from 2017. This vastly increased the total sum the Bank of Mum and Dad has lent, taking it from $65.3 billion in 2017 to $92.3 billion.

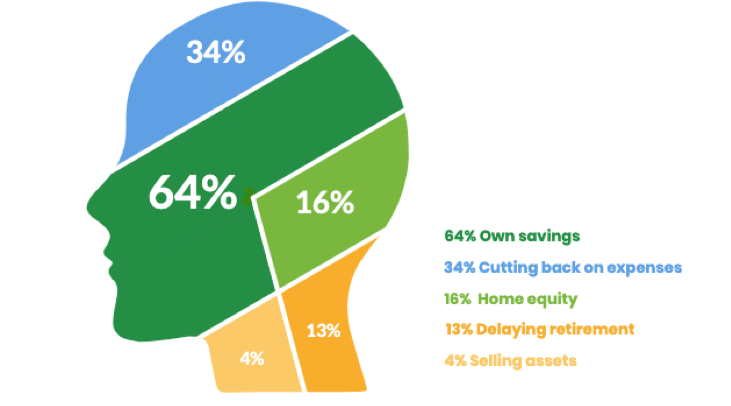

Showing just how far parents will go to help their children onto the property ladder, Mozo’s research reveals that 64% of parents dipped into their own savings for the funds, 16% pulled money from their home equity and 13% delayed retirement .

“The property market in Australia is incredibly challenging for younger generations to break into with property prices surging by 395% in the last twenty five years. For this reason the Bank of Mum and Dad has become an essential player in our nation’s housing market. Loan contributions have grown by 41% in the last two years alone highlighting that the Bank of Mum and Dad will not be closing shop anytime soon,” says Kirsty Lamont, Mozo Director.

“It could be argued that such a dominance in family assistance is feeding into a greater inequality in this country with many first home buyer hopefuls without financial aid remaining locked out as property prices rise faster than they can feasibly save a deposit. Income to property ratios have changed dramatically in the past twenty five years. At present, the cost of buying a property is 7.2 times the annual income of a typical household, whereas 25 years ago it was 1.6 times the annual household income.”

Letting adult children live at home rent free remains the most popular way to assist children with 43% of parents using this as a means of assistance. Providing money for a deposit was the other dominant form of assistance with 32% of parents offering this as a way for their children to get on the property ladder. Other forms of assistance included acting as a guarantor (14%), assisting with repayments (10%), purchasing a property on behalf of children (9%) or buying a property as a partner (6%).

Bank of Mum and dad extends beyond buying a home

Mozo’s research also found that Australian parents are providing financial assistance to their children beyond property endeavours, including contributing towards a vehicle (46%), helping with education costs (39%), paying ongoing bills (33%) and paying for household items like couches and beds (27%) to help their children get on their feet.

One in four parents facing hardship to get their children on the ladder

Nearly half of parents reported cutting back on expenses or delaying retirement in a bid to get their children on the property ladder. While the majority of parents did not expect any form of repayment from their children, one in four reported they were at risk of financial hardship and stress in the face of their contribution. 26% of parents who acted as guarantors reported that their child defaulted on the loan, resulting in the bank calling them and one in five parents who expected repayment from their contribution reported that their child had missed repayments.

“Many parents are feeling the pressure to help their children purchase their first property and for some, this is causing a real strain, especially when they find themselves working for far longer than they’d envisioned or repayment deals are reneged on or. With one in four parents providing assistance are at risk of financial hardship, the path to property ownership is less than rosy for many families,” says Lamont.

“For younger generations hoping to own their own home, it can certainly feel like a dealbreaker whether or not Mum and Dad are available to chip in. While the property market can feel like a large fence to scale, there are ways for first home buyers to save for a deposit independently. From making a concentrated effort to blast debt to looking at first home owner grants in your state and considering re-intvestment, there are ways to make your first home purchase a possibility.”