Investment markets and key developments over the past week

Share markets plunged over the last week on the back of a rapid escalation of new coronavirus (Covid-19) cases outside China – notably in Korea, Italy and Iran – and concern that (whether its labelled a pandemic or not) it will disrupt economic activity more deeply and for longer than had been expected a week or so ago. US shares fell 11.5% for the week, Eurozone shares fell 12.4% and Japanese shares lost 10%. Chinese shares fell smaller 5.1%, possibly because the number of new cases in China has slowed and the Chinese share market already saw a 12% plunge into early February. Australian shares followed the global lead and saw a 9.8% fall with IT, energy, retailers and materials seeing the steepest falls.

From their recent highs US shares have fallen 12.8%, Eurozone shares have fallen 15.8%, Japanese shares have fallen 12.2% and Australian shares have lost 10.1%.

The retreat to safety and expectations for more monetary easing saw bond yields fall to new record lows in the US and Australia. Commodity prices also fell as did the Australian dollar although this was limited by a fall in the US dollar. At one point the $A fell to $US0.6434, but managed to end the week at $US0.65.The plunge in the $A by making Australia more competitive internationally will act as a shock absorber for the blow to exports from the coronavirus outbreak.

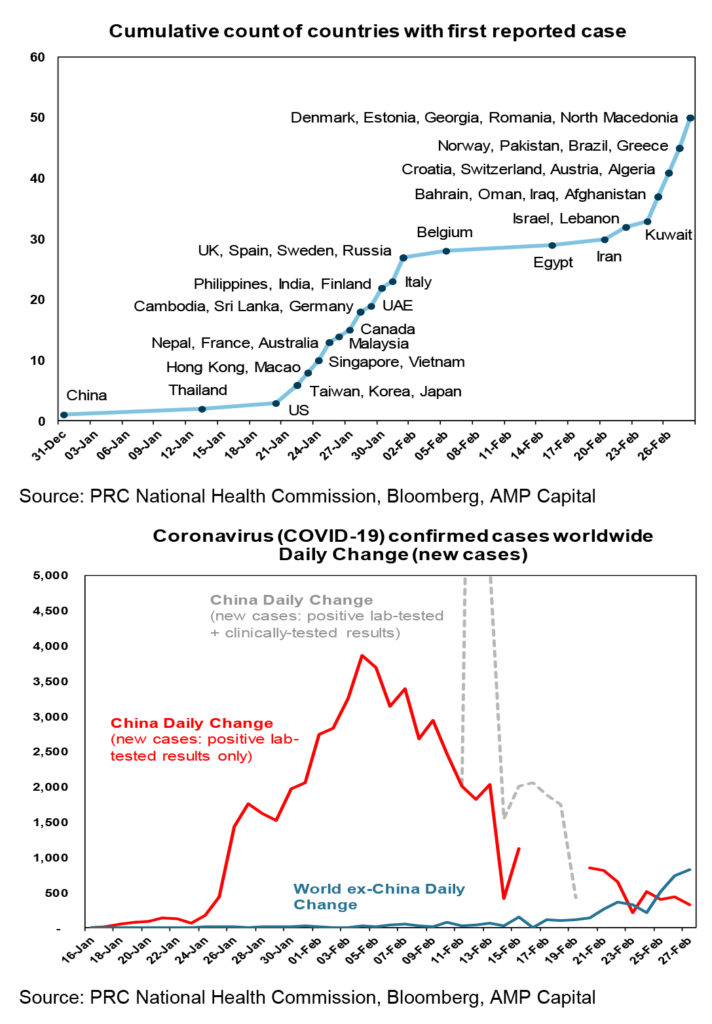

The news on coronavirus got worse over the last week as it has spread globally – with cases now reported in more than 50 countries (see first chart). The daily number of new cases outside China (second chart) now exceeds the daily number of new cases in China raising the threat of a more broad-based disruption to global economic activity well beyond China. Although new cases may have slowed in Japan and Singapore they continued to surge in Italy, Korea and Iran.

It seems to be only a matter of time before the World Health Organisation labels it a pandemic. However, amidst all the gloom there are some positive snippets to allow for:

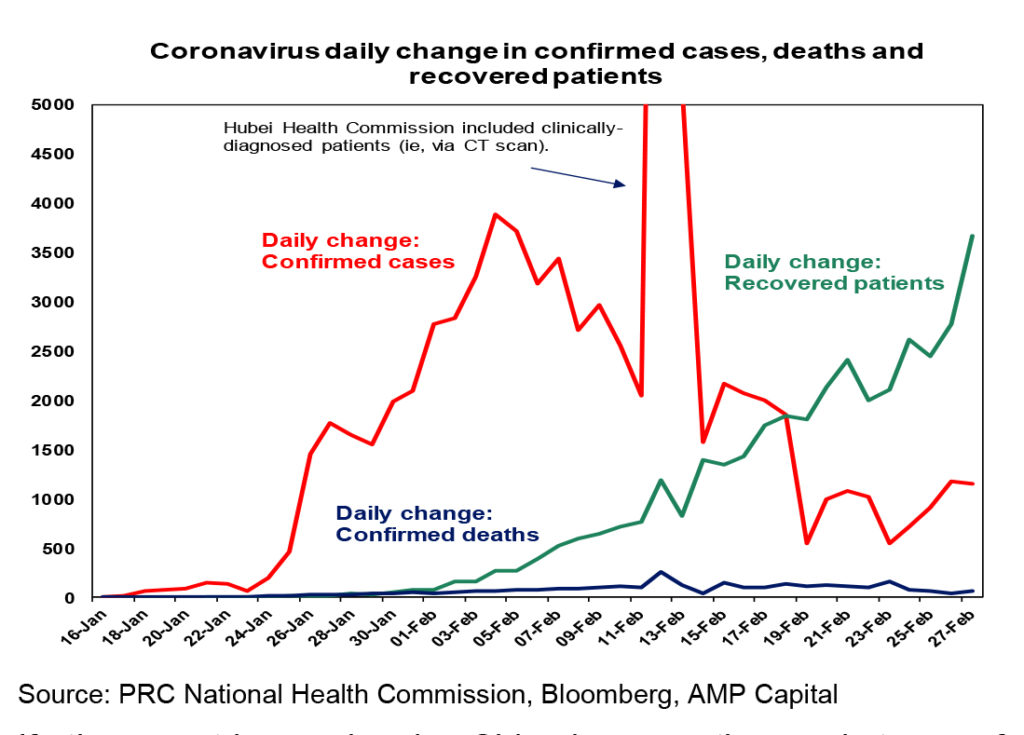

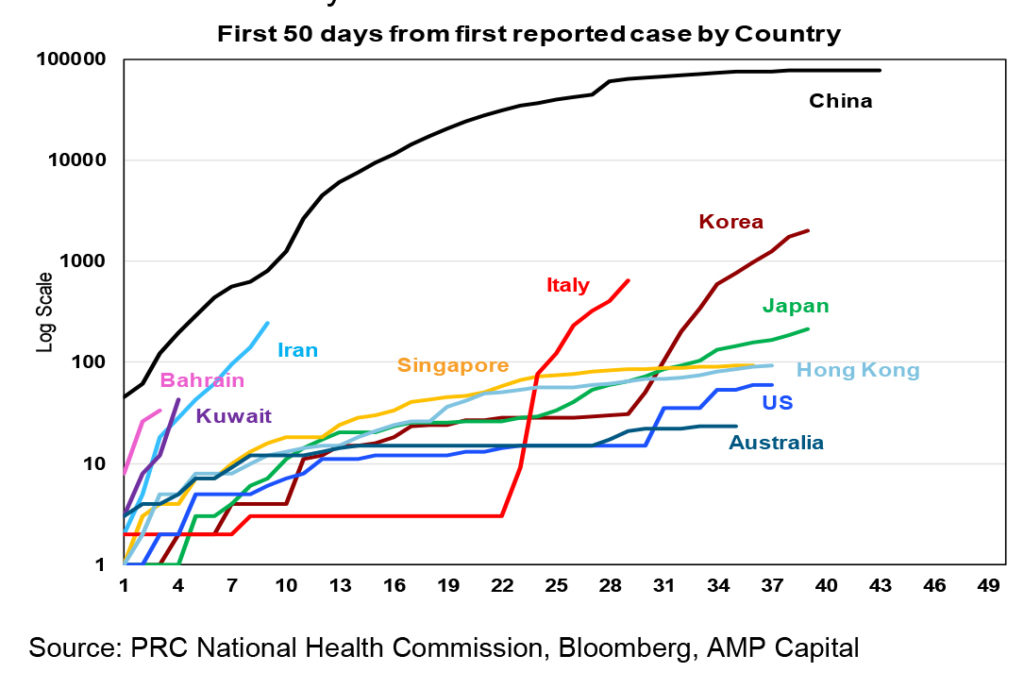

First, assuming its reliable, the reported data for China offers some hope as it has seen a sharp decline in new cases from the start of February, deaths have also fallen and there are now more recoveries than new cases (see the next chart).

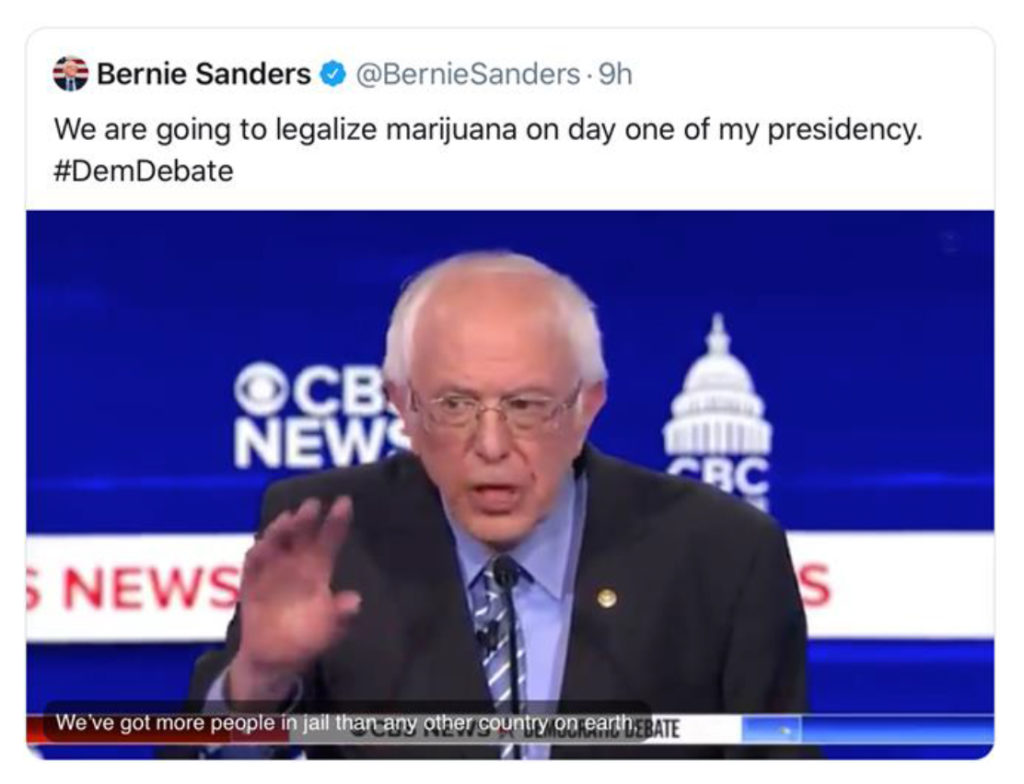

If other countries are lagging China by a month or so in terms of a sharp rise in the number of cases (see the next chart) then this holds out the hope that they should be able to bring it under control like China appears to be doing. Developed countries may not have the ability to implement China’s hard-line containment measures to the same degree but they are better resourced medically and were forewarned.

Second there is much talk that the true number infected is being underestimated. This is probable because many may not get sick enough to show up for medical help. If so, the true death rate may actually turn out to be a lot lower. This is what occurred with swine flu in 2009 which is ultimately estimated to have infected 0.7 to 1.4bn people globally but with a death rate of 0.02 to 0.04%. Consequently, swine flu did not derail the global economy at the time.

But with no sign yet of a peak in the number of new cases outside China, and a high risk of more cases popping up in the US and Australia, uncertainty remains high including in relation to the hit to global growth. So, share markets could still fall further in the short term. But here are several points are worth noting.

- First, share markets were already at risk of a correction given the strong gains from their last greater than 5% fall into August last year and coronavirus has clearly provided a trigger and explains its severity.

- Second, from a purely technical point of view it’s premature to conclude we have hit bottom yet – but markets are very oversold, the US share market managed to bounce off technical support from August lows on Friday, the VIX (or fear) index has spiked to levels last seen at the time of the last major fall in share markets into December 2018 (when US shares fell 20% and Australian shares fell 14%) and put/call ratios have spiked higher. So, we may be getting close to the capitulation by investors often seen at market bottoms.

- Second, the experience of the Chinese share market is instructive. It fell 12% to its early February low and before turning up again as the number of new cases in China peaked, all of which sounds like what happened around SARS.

- Third, share markets are now very cheap again given the 10% or so plunge in prices and the plunge in bond yields. Valuations are no guide to short term timing but when they are attractive they tell you there is rising potential for a rebound.

- Finally, policy stimulus is ramping up beyond China with fiscal easing in HK and Singapore, talk of more in Europe and the Fed signalling another rate cut. Fed Chair Powell has signalled that “the coronavirus poses evolving risks” which the Fed is “closely monitoring” and “will use our tools and act as appropriate.” So, a 0.5% rate cut is looking likely at the Fed’s mid-March meeting. Even Australia looks to be heading in the direction of fiscal stimulus, albeit very slowly, and we now see the RBA cutting this Tuesday (see the “What to watch over the next week” section below). Policy stimulus won’t stop the spread of the virus but it will help supercharge the eventual recovery in global growth and share markets.

The bottom line is that share markets face significant uncertainty in the short term and remain at high risk of more downside given the unknowns around Covid-19. But we continue to see it as part of a correction in a broader bull market. Key to watch for a bottoming and the eventual rebound are signs of a peak in new cases outside China, even stronger indicators of extreme negative investor sentiment (as that’s when markets normally bottom) and more policy stimulus.

Democratic presidential nominee and socialist Bernie Sanders’ continued success in US primaries – which lately has seen him on a similar trajectory that Trump was in 2016 is leading to increasing talk that he will win the Democrat nomination and potentially the presidency – which (at least initially) might not go down well with investment markets given his policies favouring increased taxes, public spending and regulation. Even if he falls short of a majority of delegates to the Democratic National Convention, if he gets a plurality of 40% or more it may be hard for the DNC not to give him the nomination. Our view – based on history – remains that if the economy stays strong Trump will be re-elected and, in any case, key mid-west states won’t go for a socialist. A big risk for investment markets now is if coronavirus knocks the US into recession turning down support for Trump. Super Tuesday in the week ahead where 14 states will hold primaries awarding more than a third of delegates to the DNC. Anyway, even if he does get the nomination and wins the presidency this tweet from Bernie Sanders has me relaxed in anticipation – he clearly has worked out the most important priority in the US and after doing that nothing will get done!

Major global economic events and implications

US economic data was good, although its arguably dated given the escalating concerns around the Covid-19 “pandemic”. Consumer confidence remains strong, underlying durable goods orders saw a decent rise, personal income and spending were solid in January, jobless claims remain low and new and pending home sales surged in January and house prices rose in December. The renewed plunge in US bond yields and mortgage rates will likely further boost housing demand (beyond any virus disruption). Meanwhile, core private final consumption deflator inflation was weaker than expected at 1.6% in January leaving plenty of scope for the Fed to ease as Fed Chair Powell is now signalling. Expect a 50 basis point cut at the mid-March meeting.

Eurozone confidence indicators for February rose slightly consistent with the reading from the preliminary February business conditions PMIs. Of course, that’s yet to reflect the recent escalation in Covid-19 fears.

Japanese industrial production continued to recover in January from the impact of the sales tax hike in October, but labour market data was softer than expected.

Chinese business conditions PMIs collapsed in February with the composite falling a whopping 24.1 points to 28.9. This is consistent with the roughly 50% lockdown in the economy seen this month as evident in daily tracking indictors for traffic congestion, coal consumption, etc. These are only gradually heading higher and remain well below normal levels.

Australian economic events and implications

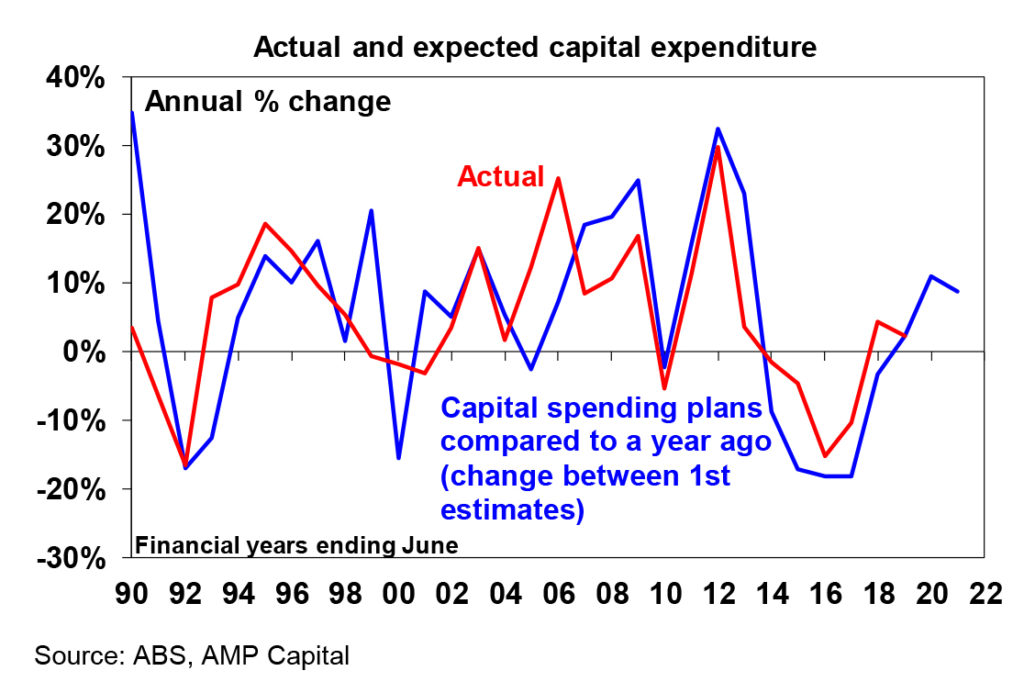

The Australian economy looks to have been soft in the December quarter even before the intensification of the bushfires and coronavirus hit in the current quarter. Construction data showed another sharp fall in housing investment and non-residential construction in the December quarter with the latter resulting in another sharp fall in business investment. While business investment plans for 2020-21 are up 8.8% on plans made a year ago its narrowly based on a big lift in mining investment with non-mining investment set to remain weak. It’s also noted that while the approach of comparing investment plans on a year ago gives a good guide to the direction of the business investment cycle it looks to have been too optimistic for this financial year with investment tracking around 2% growth compared to an 11% rise in investment plans a year ago.

Meanwhile, credit growth remained weak in January at 2.5% year on year, but it did edge up a bit from a near ten year low of 2.4% helped by a pick-up in business lending, and monthly growth in housing credit is holding above its lows but remains weak as the rapid rate of debt paydowns continues to offset growth in new loans.

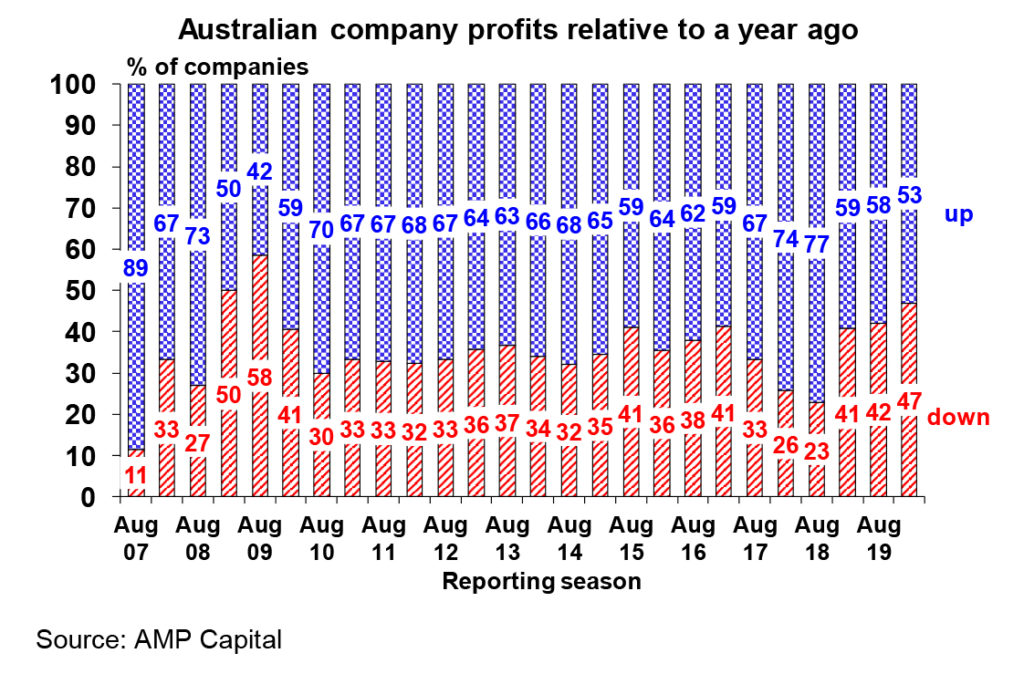

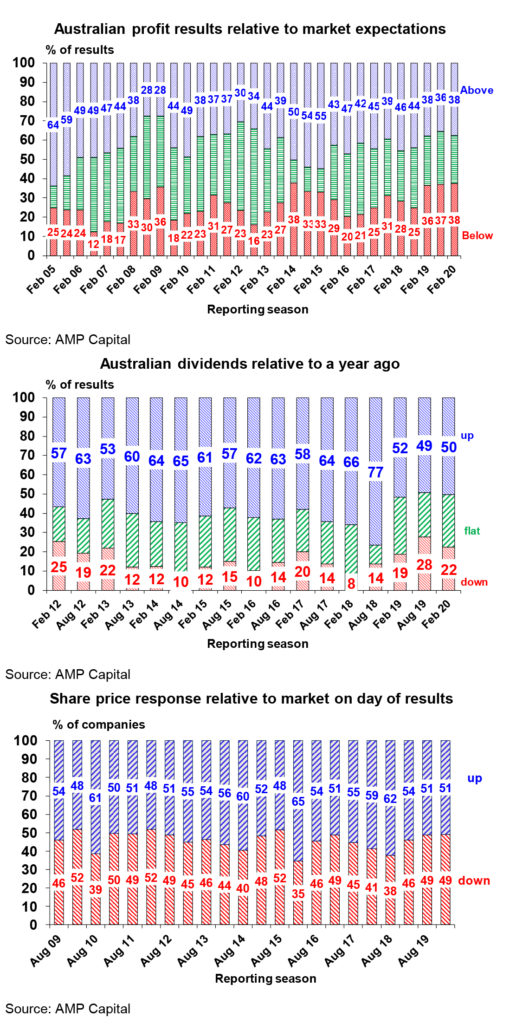

The December half profit reporting season is now wrapped up and while better than feared it was a bit mixed and the share market reaction in the last week was overwhelmed by global coronavirus concerns. The good news was that more companies saw profits rise than fall, dividends are strong, guidance was generally good and consensus expectations remain for modest profit growth this year. Against this though only 53% of companies saw profits rise which is the lowest since 2009 (see the first chart), the proportion of companies surprising on the upside was only 38% which is lower than the norm of 44% (second chart) and only 50% of companies raised dividends which is below the long-term norm of 62% (third chart). And several companies issued profit downgrades related to the impact of coronavirus. Reflecting the mixed results overall, the proportion of companies seeing their shares outperform the market versus underperform on the day they reported came in at 51% to 49% which was the same as in the August reporting season (fourth chart). Consensus earnings growth expectations for 2019-20 fell from 3% to 2.3% due mainly to weaker than expected resources profit growth. Earnings growth is strongest in tech, telcos, general industrials and REITS and weakest amongst utilities, media and insurers.

What to watch over the next week?

The global spread of Covid-19 will no doubt continue to dominate in the week ahead as investors attempt to assess how long it will take to be contained outside China and how bad the hit to economic activity will be.

In the US, expect the February manufacturing conditions ISM (Monday) to fall slightly as the coronavirus outbreak impacts supply chains, demand and sentiment but payroll employment (Friday) to remain strong. Payrolls are expected to have risen by 190,000 and unemployment is expected to have fallen back to 3.5% but wages growth is likely to have slipped to 3% year on year. Meanwhile, expect a rebound in construction (Monday), a sharp fall in the non-manufacturing conditions ISM (Wednesday) reflecting the impact of coronavirus and a slight fall in the trade deficit (Friday).

Eurozone unemployment is expected to have remained at 7.4% in January and core inflation is likely to have remained weak at around 1.1% year on year in February with both due Tuesday. Final business conditions PMIs for February will be watched for downwards revisions due to coronavirus.

Chinese Caixin business conditions PMIs for February are likely to show sharp falls due to the disruption from the coronavirus outbreak.

In Australia, the RBA should be cutting interest rates again on Tuesday in the face of the threat to the economic outlook from coronavirus. And with the Fed now signalling an imminent rate cut, its now likely that the RBA will cut in the week ahead. The reasons the RBA should be cutting now are simple.

- The run of economic data since the last RBA meeting has mostly been soft with falls in retail sales, construction and business investment, weak confidence readings, continuing poor wages growth and a rise in unemployment and underemployment which in total were already high.

- December quarter GDP is likely to show a renewed slowing in quarterly GDP growth.

- The bushfires and the coronavirus will likely take the economy backwards this quarter with significant uncertainty around the duration of the hit from coronavirus.

- We were already a long way from the RBA’s full employment and inflation objectives and developments over the last month have likely taken us further away from them.

- Ideally significant fiscal stimulus is required, but while the Government has further relaxed its focus on the budget surplus in the face of coronavirus the PM is so far only talking about “targeted, modest and scalable” assistance to impacted sectors but for now appears to be ruling out “broader, larger, fiscal stimulus-type responses [as this] is not the advice we’re receiving from Treasury.” This leaves all the pressure on the RBA in the short term.

- If the RBA doesn’t ease and then the Fed cuts in two weeks’ time as now looks likely then the Australian dollar will likely rise which the RBA will want to avoid.

Against the background of already weak economic growth and the threat of further weakness to come, the benefits of another interest rate cut – which also include keeping the $A down – likely outweigh the costs and so the RBA should be easing again. I get the feeling that the RBA would probably prefer to wait a bit longer – to better assess Covid-19’s impact to and see if there is a more “material” rise in unemployment. But things are moving fast around the threat from coronavirus with very sharp falls in share markets warning that the threat to the growth outlook is very serious. And other central banks, notably the Fed, are getting close to easing again which runs the risk that if the RBA does not ease and the Fed does then the $A will rise which would put more pressure on the Australian economy. The bottom line is that the RBA should be easing on Tuesday and with the Fed now signalling a rate cut in two weeks’ time we have raised the probability of a rate cut on Tuesday from close to 50/50 to now 70%.

On the data front in Australia, the focus is likely to be on December quarter GDP growth which we expect to show a rise of 0.3% quarter on quarter or 1.9% year on year. This reflects decent growth in public spending and contributions to growth from stock building and exports offset by improved but still constrained consumer spending and falls in housing and business investment. The slide in quarterly growth back to 0.3% from a recent high of 0.6% in the June quarter will further call into question the RBA’s assessment that the economy has passed through a “gentle turning point”. In terms of other data expect to see another 0.9% rise in CoreLogic home prices for January (Monday), a 4% gain in building approvals (Tuesday), a fall in the trade deficit for January to $3.5bn (Thursday) and flattish retail sales for January (Friday).

Outlook for investment markets

Improving global growth and still easy monetary conditions should drive reasonable investment returns through 2020 as a while – providing the coronavirus is contained in the next month or so. But returns are likely to be more modest than the double-digit gains of 2019 as the starting point of higher valuations for shares and geopolitical risks are likely to constrain gains and create some volatility:

- Shares are at risk of a further short-term correction with uncertainty around the coronavirus remaining high both in terms of the outbreak’s duration and its economic impact even if it’s soon contained.

- But for the year as a whole global shares are expected to see total returns around 9.5% helped by better growth and easy monetary policy.

- Cyclical, non-US and emerging market shares are likely to outperform, particularly if the US dollar declines and trade threat recedes as we expect.

- Australian shares are likely to do okay this year but with total returns also constrained to around 9% given sub-par economic & profit growth.

- Low starting point yields and a slight rise in yields through the year are likely to result in low returns from bonds.

- Unlisted commercial property and infrastructure are likely to continue benefitting from the search for yield but the decline in retail property values will still weigh on property returns.

- National capital city house prices are expected to see continued strong gains in the months ahead on the back of pent up demand, rate cuts and the fear of missing out. However, poor affordability, the weak economy and still tight lending standards are expected to see the pace of gains slow leaving property prices up 10% for the year as a whole. The coronavirus outbreak could be a bit of a short-term dampener though, particularly in terms of keeping Chinese buyers away.

- Cash & bank deposits are likely to provide very poor returns, with the RBA expected to cut the cash rate to 0.25%.

- The $A has now reached our expected level of $US0.65. If the coronavirus outbreak is contained with only a hit to March quarter global GDP followed by a rebound, then the $A is likely to drift up towards $US0.70 by year end. A more drawn out hit to global growth through the June quarter from Covid-19 would likely see the $A pushed to $US0.60 or even below. Given the uncertainty around the virus the short-term risks for the $A are on the downside.

By Shane Oliver