The COVID-19 crisis and sharp fall in economic activity has led to deteriorating corporate fundamentals for many high-yield issuers, which we think warrants close watching, says Jeffrey D. Mueller, Co-Director of High Yield Bonds and Portfolio Manager at Eaton Vance.

He notes: “We’ve seen a contraction across earnings, revenue growth and interest coverage, along with an increase in leverage. The key takeaway here is that fundamentals have weakened and that has contributed to a rise in defaults and a tremendous surge in “fallen angels” – debt downgraded from investment-grade to high-yield ratings.”

Mueller says: “Fed support has kept the market in check. Softer fundamentals have contributed to a big pickup in defaults, which began to increase sharply in March and continued to climb in Q2 and thus far in Q3.

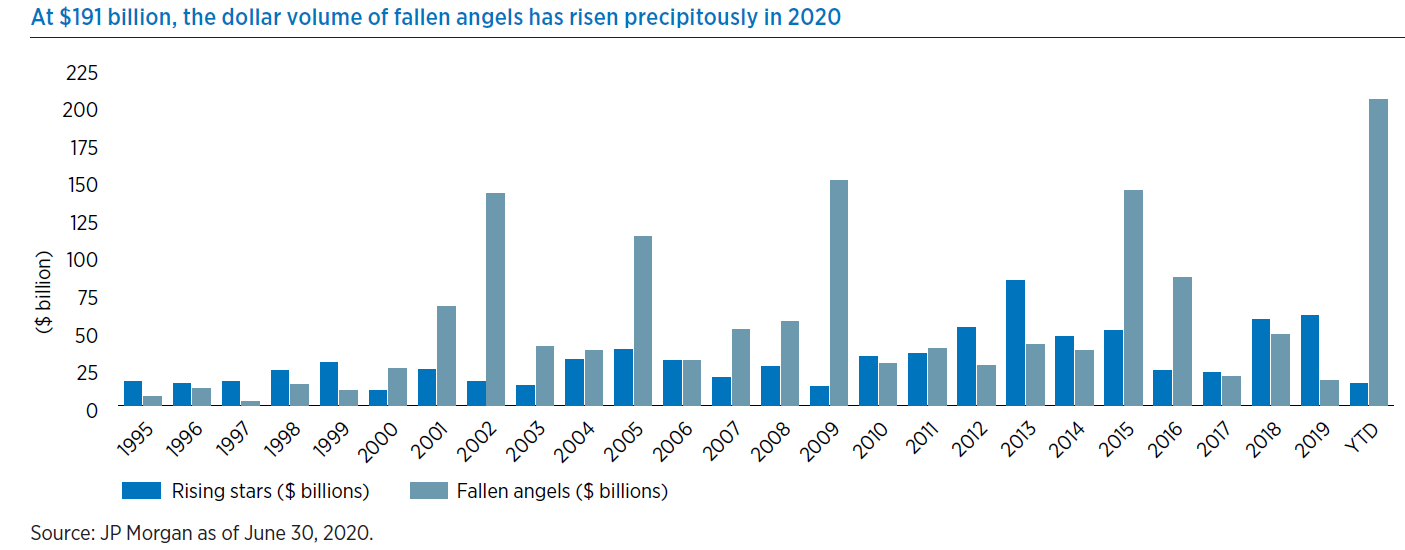

“We’re seeing distress across most sectors, though it is most pronounced in energy. Through the end of Q2, $191 billion of previously investment-grade-rated debt was downgraded to high yield.1 That is a hugely meaningful number, and we think it will continue to climb. However, credit facilities launched by the Federal Reserve (the Fed) will help mitigate this situation. In effect, what the Fed has done is help ensure that fallen angels do not overwhelm the high-yield market. We think what prompted the Fed’s actions here was the downgrade of Ford, given the size of the company and how large an employer it is. Notably, as a whole, fallen angels performed extremely well during the second quarter.

“Yet, at the end of June, the default rate for the overall high-yield market was at a 10-year high, at 6.2%. Energy constituted 46% of the last 12-month volume of bond defaults. As of June 30, energy was 63% of all high-yield bonds trading below $0.50, and 48% of all bonds trading below $0.70. We expect a continuation of this default trend, and we’ve keeping a close eye on a number of credits in this sector.

“At the end of 2019, energy represented 12.5% of the high-yield market. Now, it’s 13%, but this includes 4% from fallen angels that entered the index this year. If we exclude fallen angels, the legacy energy index is almost 30% smaller relative to year-end 2019, and this is due to the depreciation of bond prices and defaulted companies that have exited the index.

“Unfortunately, we think the outlook is clear as mud. The fundamentals are pretty bleak, with high US unemployment, at around 80 million people. It’s getting better sequentially, but obviously, from a historical perspective, unemployment is quite high.

“As we’ve discussed, defaults have accelerated, particularly in the energy sector, and recovery is slow. However, countering all this is the Fed and US government, which have passed $3.7 trillion in stimulus for a variety of different programs, and they’re not done should the need arise. Meanwhile, the European Central Bank (ECB) has issued $2 trillion in stimulus, and these global central banks have done this over the course of only a few short months. That’s lit a fire under the US high-yield market and caused a rapid move toward recovery, including spurring some robust flows into the asset class.

“While central bank and fiscal stimulus represent a significant silver lining, we also think it’s important not to ignore the risks inherent in the high-yield market and global economies as we face the ongoing challenges of the coronavirus, compounded by difficult geopolitics,” says Mueller.

————