For most Australians, the majority of their wealth is tied up in their family home.

Australia is facing a major retirement funding challenge. Our longevity has been well documented and even during a pandemic, Australia was the only developed nation to experience increased life expectancy[1], a feat attributed to lockdowns, a reduction in other diseases and decreased road fatalities.

While longer lives are good news for most, it’s becoming increasingly clear that many people don’t have enough superannuation to fund a comfortable retirement. This is particularly prevalent among Australia’s baby boomers, waves of whom are reaching retirement. Over the coming years, 5.5 million people born between 1946 and 1964 will retire. For many of those, compulsory super started too late into their working lives to provide meaningful retirement savings. As these baby boomers approach retirement, inadequate funding looms as a major socio- economic problem that must be addressed.

The case for home equity

For most Australians, the majority of their wealth is tied up in their family home. Around 80 percent of retirees own their home; given the 22 percent surge in Australian property prices in 2021[2], the value of untapped home equity owned by Australian retirees is well over one trillion dollars. This appreciation also means the value of home equity is now worth 3-4 times superannuation savings.

However, this wealth is locked away and has been largely inaccessible to fund retirement needs. Given that most retirees wish to stay in their own home as they age, this untapped savings is a valuable resource that could be utilised to provide improved retirement funding and cover important costs such as age-appropriate in-home care and home renovations to allow retirees to live safely and comfortably at home.

The potential of home equity to fund retirement has not gone unnoticed by the federal government. In the Retirement Income Review (2020), home equity was cited as a key part of the third pillar of retirement funding, sitting alongside superannuation and the Age Pension.

More recently, the federal government announced that its Centrelink Pension Loans Scheme reverse mortgage will be relaunched as the Home Equity Access Scheme – a welcome move in meeting the challenge of funding an ageing population and one that underscores the importance placed on home equity retirement funding by the government.

Importantly, facilitating access to home equity to fund long-term retirement needs represents an opportunity to meet a major unmet community need and provide a sustainable fiscal stimulus to enhance economic growth.

Ways to access home equity

After almost two years living with the threat of COVID, in and out of lockdown, older Australians understand more than ever the value of the family home as a safe haven and the preferred place to live during retirement.

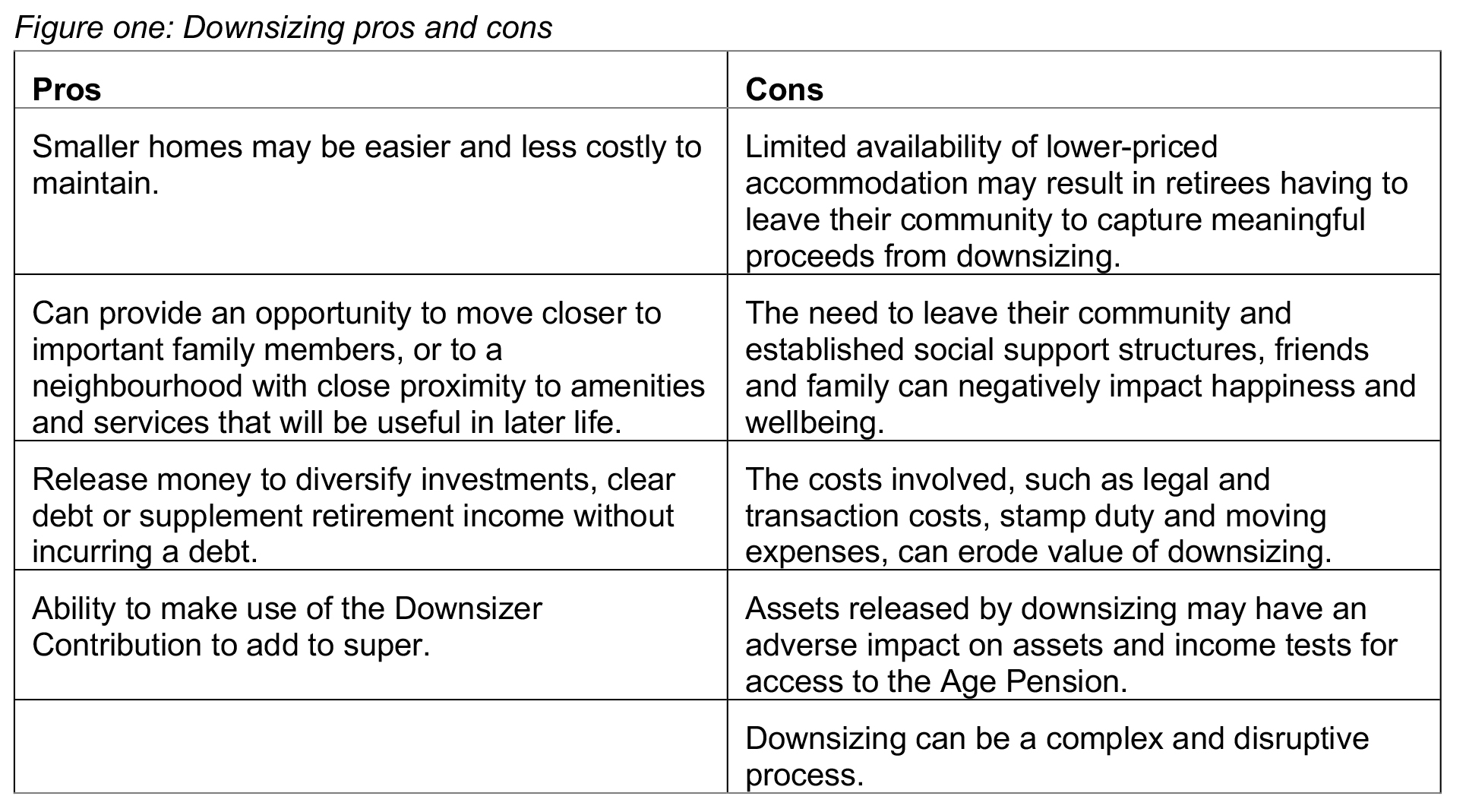

Downsizing

Selling the family home, moving to a lower-priced property and using the difference to fund retirement is often suggested as a way to access to home equity. To encourage retirees to downsize and increase the available ‘stock’ of family homes, the federal government introduced its ‘Downsizer Contribution’.

Australians aged 65 plus can sell their principal residence (which needs to have been owned for at least 10 years) and use the proceeds to make a non-concessional contribution of up to $300,000 to their super account. In the case of a couple, both parties can make a downsizer contribution.

There’s a range of eligibility criteria and rules that apply.[3]

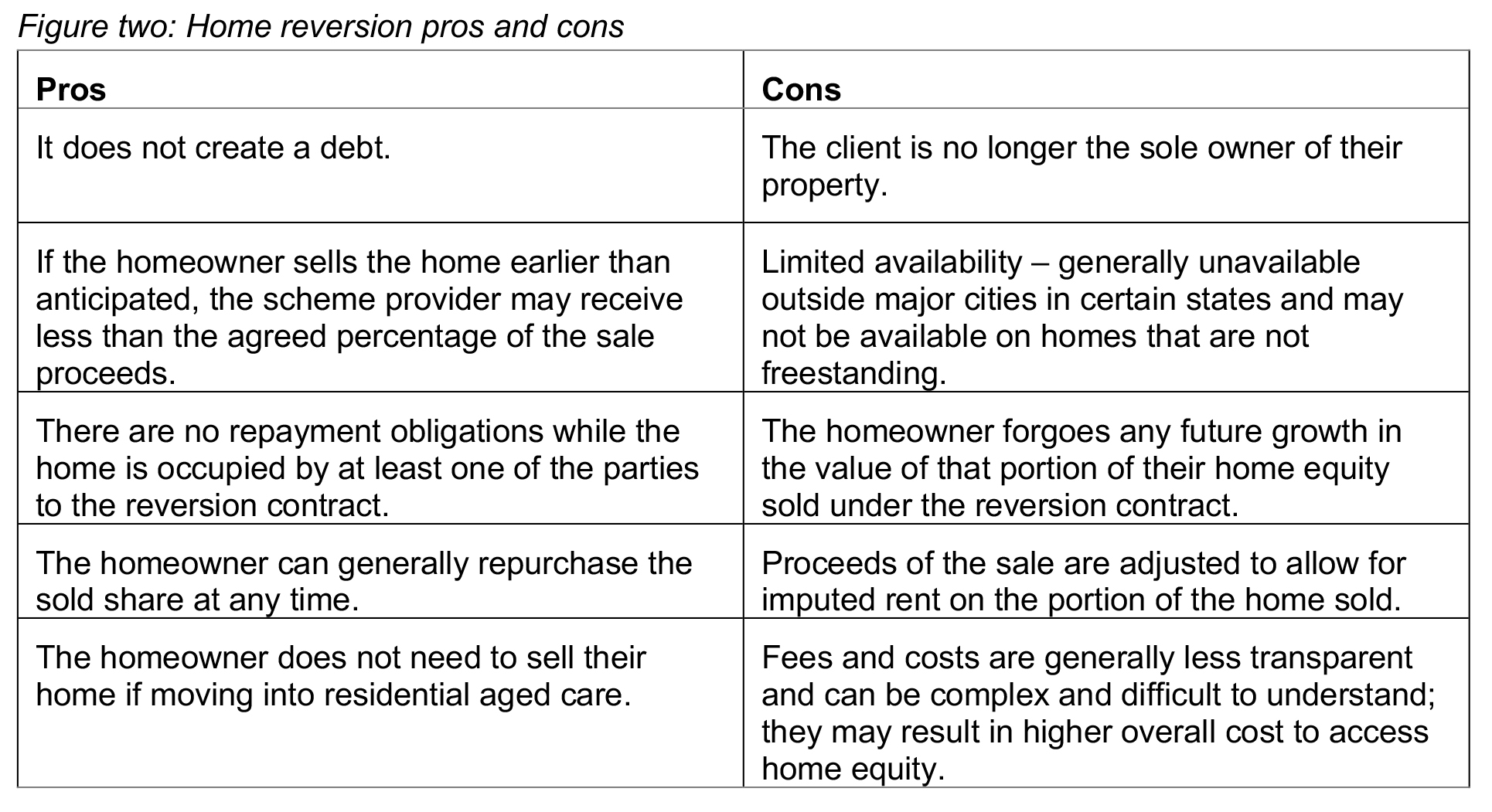

Home reversion schemes

Often marketed as a ‘debt free’ way to access home equity, a home reversion scheme is a contract for the partial sale of the home.

Instead of borrowing against the value of their home, the homeowner agrees to sell a share of the future sale proceeds of their home. This portion of home equity is sold at a discount to its current value in return for a lump sum payment. The discount applied is age based and decreases with age.

When the home is sold, the home reversion scheme provider receives the value of the proportion of equity it purchased, at the price of the day of sale.

A client using a home reversion scheme will receive an amount of money based on several factors:

- the assessed value of the property

- the proportion of the home being sold

- the age and number of people living in the home.

Centrelink Home Equity Access Scheme

Formerly known as the Pension Loans Scheme, this program provides support to Australian homeowners of Age Pension age in the form of a fortnightly income stream. It is a reverse mortgage administered by the Department of Human Services and distributed by Centrelink, although is regulated differently to commercial reverse mortgages and is not subject to responsible lending guidelines.

The Centrelink Home Equity Access Scheme allows retirees to borrow up to 150% – or 1.5 times – the maximum Age Pension. The maximum income available currently corresponds to a maximum $36,121.80 per annum for singles and a maximum of $54,451.80 for couples.

From 1 July 2022, lump sum borrowing will be accommodated, but only within the same borrowing parameters.

Reverse Mortgage

A reverse mortgage is the primary mechanism used by retired Australians to access their home equity; it’s achieved via a loan facility that doesn’t require repayment until the property is vacated. While the reverse mortgages of the early 2000s left a lot to be desired, regulatory change, consumer protections and responsible lending requirements have resulted in a product that puts consumer interests front and centre.

As with a standard home loan, a reverse mortgage is secured by registering a first mortgage over a homeowner’s property. The primary difference between a standard home loan and reverse mortgage is that regular repayments are not required.

As a result, the monthly interest compounds over time and increases the balance of the loan, unless the borrower chooses to make monthly interest payments.

Importantly, the borrower remains the owner of their home and reaps the full benefit of the home’s capital growth.

The regulatory environment for reverse mortgages

The National Consumer Credit Protection Act (2012) provided the foundation for access to home equity in Australia by stipulating clear consumer protections and market parameters at both the beginning and end of all loans. These protections include:

- Prospective loan-to value ratios (LVR): At 60 years, borrowers can obtain 15% of their home value, increasing 1% for every year of age—i.e. 25% LVR at age 65. LVRs above this are presumed to be unsuitable for the borrower.

- No negative equity guarantee: Borrowers cannot owe more than 100% of the market value of their home when it is sold. Lenders cannot claim against the borrower or estate any amount in excess of the value of the home. This protection is being introduced by the government for its Centrelink Home Equity Access Scheme this year.

- Guaranteed occupancy: Borrowers cannot be evicted or foreclosed based on longevity, property prices or the value of the loan, in other words, borrowers can stay in their home for as long as they choose.

- Responsible lending: Credit providers must enquire about the possible future requirements and objectives of the customer including the ability to live in the home without hardship, future aged care needs and future bequests.

- Consumer disclosures: Credit providers must give borrowers projections of future home equity concordant with the ASIC MoneySmart calculator, an information statement, occupancy protection information and provide annual statement and servicing.

- Enforcement and discharge: Loan default provisions are limited in circumstances of serious contractual breach and must be notified via direct personal communication.

A 2018 ASIC review found these protections to be robust. The Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, held around the same time, did not receive submissions with respect to reverse mortgage products.

The overall conclusion from a review of reverse mortgage policy and legislation is that the foundations of responsible, long-term access to home equity to fund retirement are in place to meet the needs of Australian retirees alongside their superannuation, pension entitlements and other investments.

Myth Busting

Despite a robust regulatory environment, the shadows cast by products of the past have led to some misconceptions about today’s products.

Myth one: My client could lose their home

Homeowners can remain living in their home as long as they wish; they continue to own the home and retain the title. Because regular repayments are not required, there’s no default risk and the homeowner cannot be forcibly removed. Borrowers need to meet simple obligations, such as remain living in the home, maintain it and pay the council rates and home insurance.

Myth two: My client could end up owing more than the home is worth

That’s not possible. The “no negative equity guarantee” (NNEG) clause in the National Consumer Credit Protection Act means the borrower is protected by law and cannot owe more than their home is worth, regardless of what happens to the property value.

Myth three: The kids are being disinherited

Retirees are living longer, which means bequests are delayed past the time when their children face their biggest financial needs. Using home equity, retirees can help their kids and grandkids when they need it most. Choosing the timing of a bequest rather than waiting until death is a desirable option for the whole family.

Myth four: A reverse mortgage is a ‘last resort’

Home equity can be used to enhance your clients’ lifestyle and wellbeing in retirement, without needing to sell their home. Products are increasingly sophisticated, providing flexibility and choice, capital and income, to improve retirement funding.

Myth Five: There’ll be nothing left to cover aged care costs

The amount able to be borrowed is dependent on the LVR, which is conservative on a reverse mortgage. Accordingly, if in later years a client needs to fund a move into aged care, there should be sufficient equity to cover the accommodation deposit or daily fee as required.

Myth six: It’s better to access home equity by downsizing

While it suits some people, many retirees are reluctant to downsize. As well as the financial costs, moving from the home and community can result in social and emotional costs. Selling up may also impact Age Pension entitlements.

Myth seven: I already have a mortgage so I can’t get a reverse mortgage

In many cases, a reverse mortgage can be used to refinance a mortgage. Because a traditional bank mortgage has to be repaid each month, it impacts your client’s retirement cashflow. It also carries default risk if your client is unable to meet those repayments. By refinancing with a reverse mortgage, your client can free up their retirement income and don’t run the risk of the bank foreclosing.

Myth eight: I can’t help my clients access a reverse mortgage

Reverse mortgages are a type of credit product and regulated by the National Consumer Credit Protection Act (NCCP). To provide clients advice on specific reverse mortgages (or any credit product), an adviser needs to be a Credit Representative under an Australian Credit License (ACL). As such, many advisers choose to refer their clients to a Credit Provider to offer the specific implementation of the reverse mortgage. This allows advisers to continue to help their clients without additional license or compliance requirements.

Benefits of responsible access

The psychology of baby boomers, their homes and retirement is complex. Just as there is no “average” baby boomer, there is wide heterogeneity in attitudes, retirement needs and experience in using debt to both invest and consume.

By restructuring responsible access to home equity, retirees receive multiple benefits:

- Access to savings: where the majority of lifetime savings are in the home, these are now available to improve retirement funding.

- Improved retirement funding: where the Age Pension and superannuation are inadequate, home equity can improve retirement funding.

- More reliable retirement income: for some retirees, income may be volatile relative to the performance of superannuation. Home equity can smooth income and capital supply.

- Meet large capital needs: retirees can utilise reverse mortgages to meet large capital needs, enabling them to retain their income producing assets.

- Sequencing risk management: responsible, long-term access to home equity adds a second, independent, largely uncorrelated source of income should super assets decline periodically.

Increasing longevity suggests it’s an optimal time to include home equity as a part of retirement planning. By drawing on multiple sources of income, Australian retirees can achieve funding adequacy throughout the full course of 25+ years of retirement. However, to achieve this, retirees must be able to responsibly and cost-effectively access home equity savings to generate retirement income.

———