Mind the gap…

Mind the (implementation) gap

In a financial advice context, the gap between client intentions and action is nothing new.

In a macro sense, we see this gap play out before people even get through the door of an adviser’s office. ASIC research [1] from 2019, for example, found that 20% of those intending to seek financial advice in the coming year never acted on that intention. Another study[2] posited that the unfolding multi-trillion-dollar intergenerational wealth transfer could come unstuck because of inertia. (80% of respondents intended to transfer their wealth but less than half had actually put a plan in place to do so.)

Even more perplexing are those clients who actually meet an adviser and pay for their advice, but then fail to implement it. Whilst there are undoubtedly advisers who boast a 100% success rate on this front, a survey[3] of advisers from the US – which found that more than half of clients receiving a financial plan implemented less than 20% of the recommendations 6 months after receiving the plan – is likely to be instructive.

So, what could cause such a gap? Surely, if someone goes to the trouble of seeking out – and paying for – financial advice, they should be prepared to act on that advice?

There are a few ways we could look at this conundrum.

A Canadian study[4] from 2019, ‘Why Do People Fail to Act on Financial Plans?’, identified seven possible reasons for the implementation gap in financial advice:

The same study proposes a variety of techniques to mitigate these barriers to action, including:

- breaking down advice and goals into smaller, easier to manage pieces (an incremental approach)

- the regular and highly visual reporting of progress; and

- simplification of documentation and language used

But are people seeking advice actually ready to change?

As valuable as the Rotman/BEAR research is, its starting assumption is that people seeking advice are actually ready to make the behavioural changes inherent in the advice. This may not actually be the case, which is a why a different perspective may be more helpful.

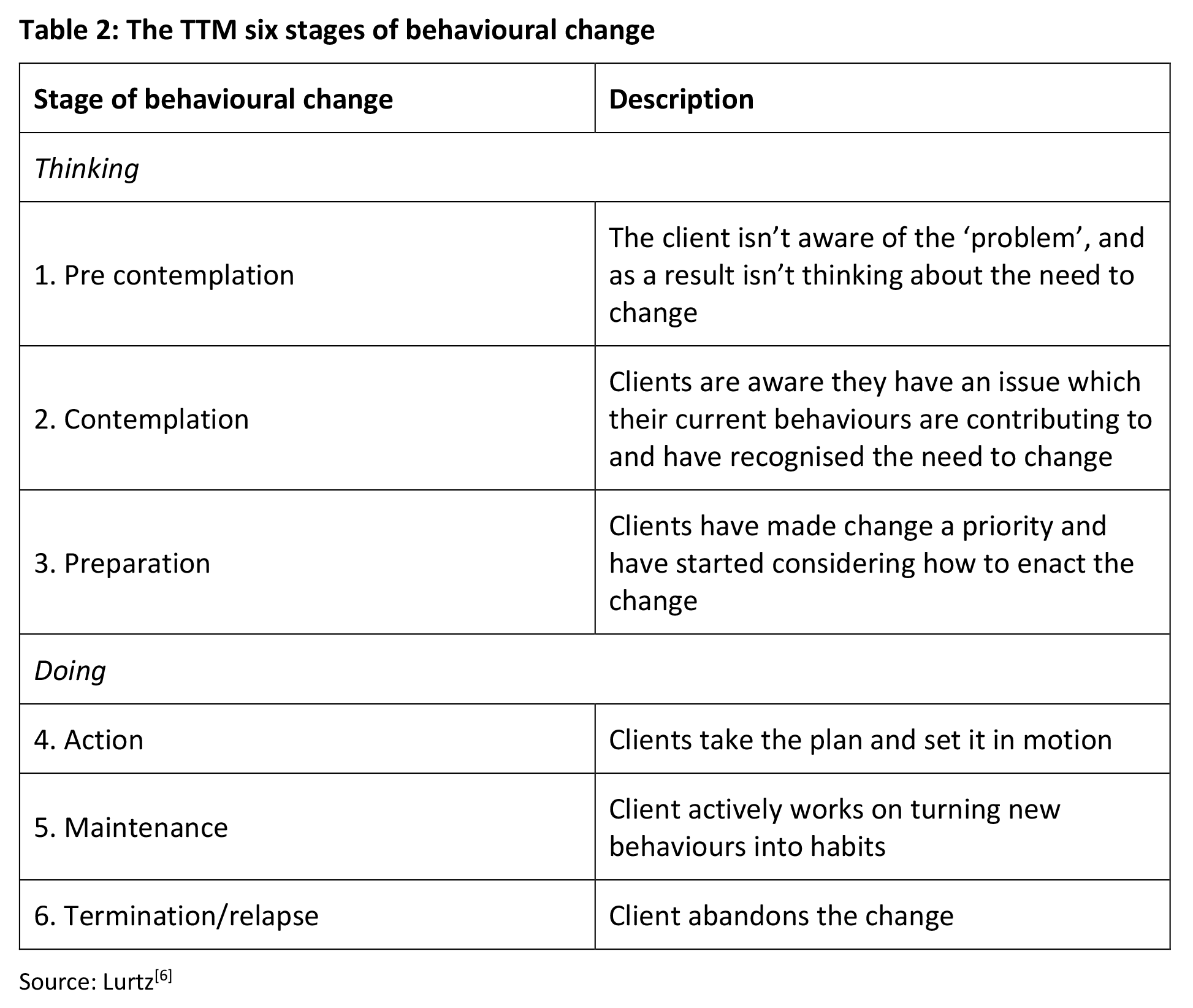

The 6 stage Process of Change[5], developed in the 1990s by researchers James Prochaska, John Norcross, and Carlo DiClemente, identified 6 steps to behavioural change.

These steps involve 3 ‘thinking’ stages and 3 ‘doing’ stages, as shown in Table 2 below:

One of the most immediate – and important – take outs from this model, called the Transtheoretical Model (TTM) of Change, is that the assumption that people seeking advice are ready to act on it, is in fact false. In many cases, the client may have not even have recognised there was a problem needing change! (An example of how this can happen is when a client comes to see you at the insistence of their spouse.)

According to Prochaska et al, around 80% of clients sit in the first three – thinking – stages[7], a finding highly consistent with the alarmingly low implementation rates referred to in Figure 1 above.

To move clients through the stages, we need to identify the stage they are in

According to experts, clients can be stuck in the ‘thinking’ stages for as long as a year. Indeed, they can spend 6 months or more purely in the Pre-Contemplation stage! And for advice businesses, that means closing the intention/action gap is likely to be a strategic priority.

But in order to help clients move between all the different stages – which needs to be in sequence if the change is going to be sustainable – advisers first need to understand what stage the client is actually in.

Sometimes this is easy to identify. In our example mentioned above, the client has only agreed to seek out advice at the insistence of their spouse. In such circumstances, it is not unusual for the client to be in denial, believing they have no need to see an adviser. You will probably be able to spot this client’s verbal and body language a mile away.

But in other cases, it will be less obvious.

One technique is to pose a series of open-ended questions, such as those proposed[8] by Karen Miller Kovach, Chief Scientific Officer for Weight Watchers (there are many parallels in the ways we make changes relating to physical health, and financial health).

These questions include:

- What would you like to have happen? Has the client (themselves) even recognised the need for change? If the client answers in the negative, they are definitely in the Pre-Contemplation stage. If they have at least recognised the change, they are further along the change journey.

- What needs to happen? If the client has recognised the need for change but doesn’t know where to begin (either because they don’t understand the steps, or aren’t motivated to find out), they are likely in the Contemplation stage.

- Can you? If the client responds to this question with a plan of action (for example, ‘to increase my retirement savings’, ‘put a will in place’) then they may have stopped Contemplating and started Preparing. If, on the other hand, the client says ‘no’, or ‘I’m not sure’, they are probably still in the Contemplation stage. The adviser may need to help the client determine if the issue is related to the advice itself, or a personal issue that is holding them back.

- Will you? If the client answers ‘yes’, this is a good sign they are in the last ‘thinking’ stage and ready to take action. They have acknowledged the need for change, understand what they need to do, feel capable of doing it and are now emotionally ready. A client who says ‘I’ll try’ may need some extra monitoring or support to start the first step. This stage is about getting their commitment.

Scaled questions are an alternative to this approach. Applying a scale of 1 to 10 – where 1 is ‘no need to change anything’ and 10 is ‘ready to make changes now’ – can help advisers zero in on what stage the client may be at.

Techniques to move advice clients through the stages

Integral to the TTM model is the idea that people need different types of support at different stages of change. In all there are 10 steps, in two categories: ‘experiential steps’, which are generally limited to the ‘non action’ change stages, and ‘behavioural’ steps.

Experiential steps

- Consciousness-Raising: as the client may not even recognise the need for change, the goal in this step is to build awareness through information, education, and feedback about their current behaviour and/or their potential new behaviour. Advisers could discuss concepts such as risk and diversification, and the behavioural biases that may be holding the client back.

- Dramatic Relief: there needs to be an emotional commitment to change. Individuals may feel fear or anxiety because of their current behaviour or feel inspiration and hope when they hear about how people are able to achieve outcomes as a result of advice. Advisers should help them visualise the positive and tap into the resulting motivation.

- Self-Re-evaluation: here the adviser helps individuals clarify values and realise that creating new healthy money habits is an important part of who they are and aspire to be. This is about reinforcing the way these behaviours are connected to deep seated life goals.

- Environmental Re-evaluation: help the client understand the impact of their current money behaviours on others (their spouse, their children), and how making positive change will benefit those people.

- Social Liberation: clients in all stages can benefit from this step, which is where individuals realise that society is supportive of their new ‘healthier’ behaviour. An adviser might talk about the greater community of other clients who have made the same change – testimonials can work well here. It’s like there’s an exciting new world that your client can enter, just by making some changes.

Behavioural steps

- Self-Liberation: this is where clients make choices and commitments. Here advisers can help clients set goals and gain commitment to those goals.

- Counterconditioning: the substitution of new healthy ways of thinking and acting for the old, sub-optimal, behaviours and attitudes. An advice example is when a client implements a new savings plan.

- Stimulus Control: this involves observing and managing the environment to remove reminders about ‘unhealthy’ behaviour and replacing them with positive cues. People can get addicted to success and so in this step, regular client communication showing progress to goals, in a way that reinforces how the progress couldn’t have been made with the old behaviours, can be effective.

- Helping Relationships: individuals undertaking change can benefit from finding others who support their new behaviours. Indeed, extensive research[9] shows that having a human mentor (not a computer!) significantly increases the chances of behavioural changes being sustained. The adviser needs to make sure they aren’t the only source of this support, instead enlisting friends, family members, or maybe even other members of their client community.

- Reinforcement Management: clients need feedback when making changes, including positive reinforcement when progress is good, and encouraging reflection if progress stalls.

Many of the above steps will come into play in more than one stage, as can be seen in Figure 3 below.

When talking about change, Karen Miller Kovachs also noted,[11] “The willingness to make a change is directly connected to a person’s feelings about whether change is worthwhile (its

importance) and whether it is achievable (confidence that it can happen).”

What she is alluding to are two more concepts that are absolutely fundamental to the TTM model of change, decision balance, and self-efficacy.

Decision balance can be thought of as a decisional balance sheet, comparing the pros and cons, or gains and losses, of a given change. Indeed, the balance sheet analogy can become literal, where advisers provide clients a worksheet to list out items in the pro and con columns. It is important to note, however, that simply having more ‘pros’ than ‘cons’ isn’t likely to be sufficient in encouraging change. As Michael Kitces observes[12], loss aversion theory – where we experience losses far more deeply than a gain of the same magnitude – means the ratio may need to be two or three to one!

Self-efficacy is about the individual’s confidence in their ability to make the change. A concept first developed by psychologist Albert Bandura[13], it relates to the ability to maintain positive behavioural change, especially in circumstances that may trigger relapse. Although his studies were focused on people dealing with addiction issues, the concept is absolutely relevant to financial advice.

An Australian study[14] by Griffith University examined the importance of self-efficacy in changing retirement savings behaviours, and the practical steps advisers could take to help the client build that confidence.

They suggested that ‘providing aspirational images of what is possible without either firstly or simultaneously providing a means for a person to gain confidence about their abilities in this area may be ineffective in motivating a person to take action’.

The study also noted that ‘providing an environment and background that engenders a positive attitude towards saving for retirement with the assistance of a professional financial services planner, is also crucial for a person to do something in this area’.

The authors of the study concluded that there are four ways in which self-efficacy can be built: personal experience, observing others, verbal persuasion, and a heightened emotional situation. In this context, they suggested that providing a ‘free’ first consultation may assist in further encouraging individuals to utilise the services of an adviser, and that case studies and testimonials were a valuable way of allowing potential clients to observe the positive impact of financial advice.

Finally, a word about physical environment

Reactance theory explains our inherently human tendency to not do as we are told, and as alluded to in the Griffith University study above, the environment in which clients and advisers engage can make a big difference on the way clients behave.

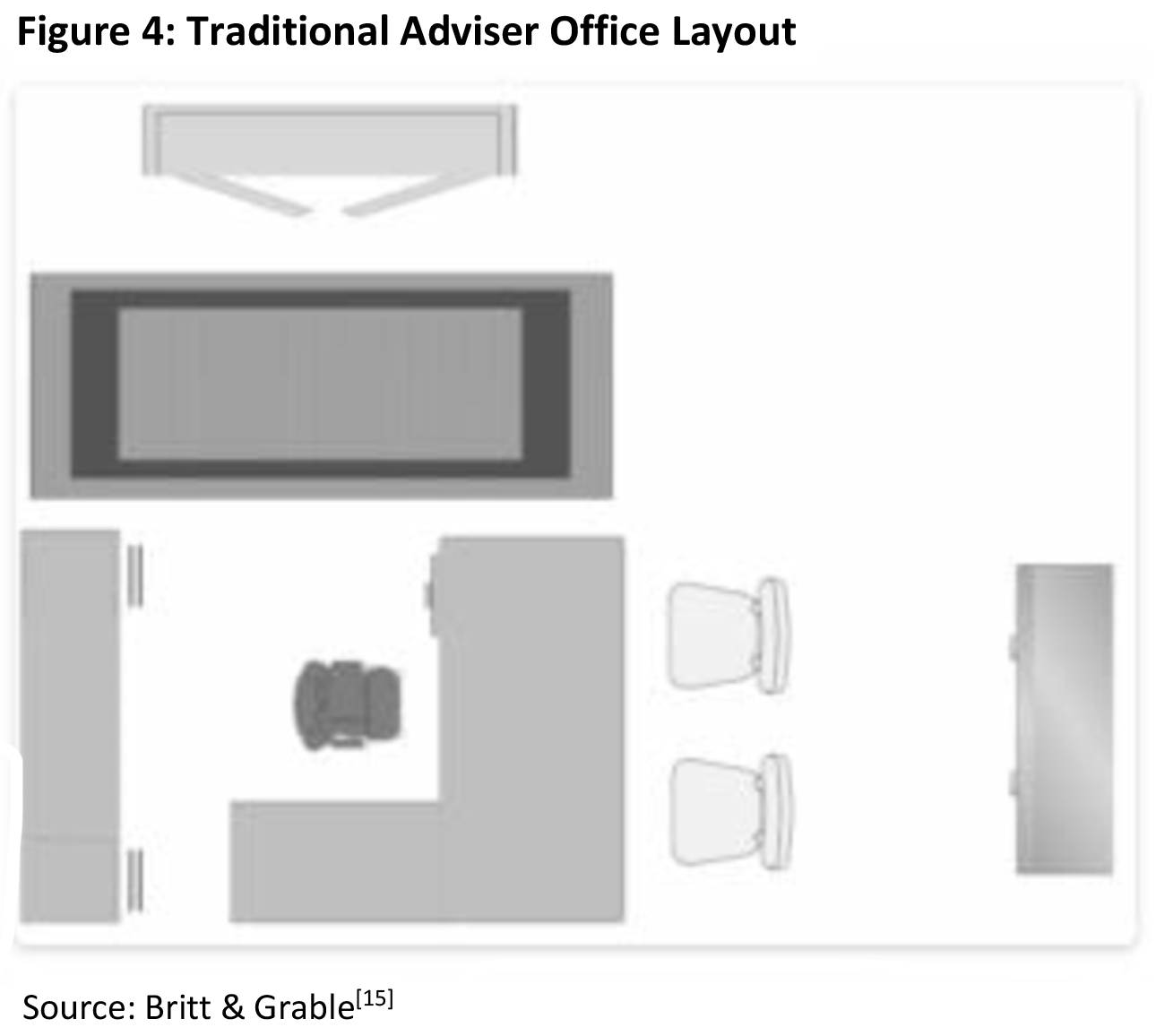

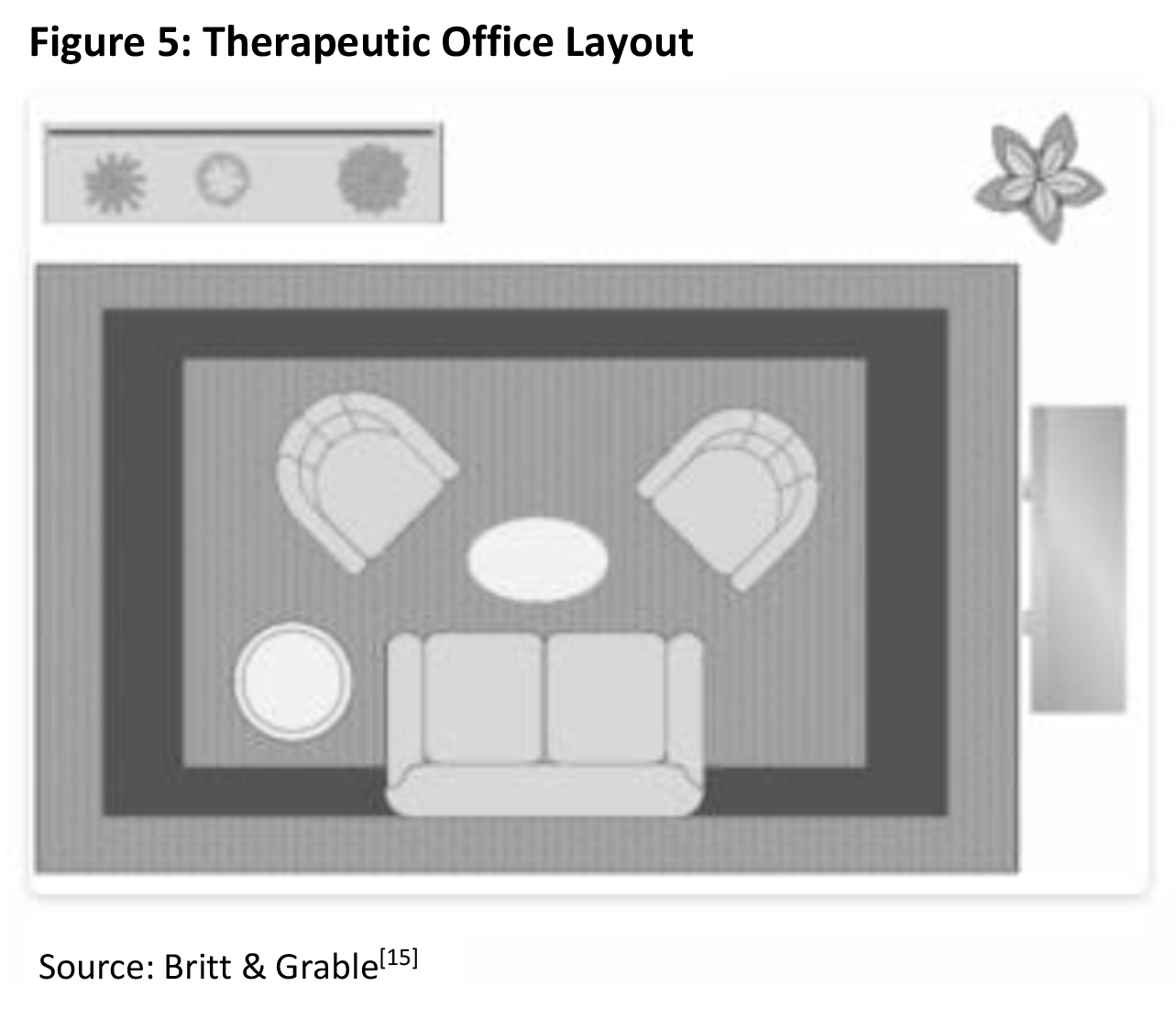

Specific work[15] on this topic, by Sonya Britt and John Grable, showed that the physiological response of clients engaging with a financial adviser – and their subsequent willingness to change behaviours and attitudes – was significantly influenced by the physical environment where the client and adviser met. Specific issues addressed in their work included colour (advisers should avoid red and other colours that increase heart rate) and office layout.

Whilst the typical layout for an office may have resembled Figure 4 below (with the adviser behind a desk and the clients on the other side), Britt and Grable found that a therapeutic office setup – as seen in Figure 5 – encouraged a more open dialogue, reducing client stress and enabling the adviser to gather more information (in turn allowing their advice to be more tailored).

The desk can be seen as a barrier to open dialogue, and the adviser is perceived as being more accessible and friendly when the ‘barrier’ is eliminated. Britt and Grable also noted that ‘clients do not find the use or lack of a desk to impact adviser credibility’.

Conclusion

Financial advice recommendations are, in essence, recommendations to make changes to money behaviours and habits. The mere act of seeking advice does not in itself guarantee an individual is in the right frame of mind to make those changes, and indeed they may not even be aware that change is needed. The ‘implementation gap’ that exists between intent and action is problematic for advisers because it both undermines the effectiveness and perceived value of their advice, and challenges the economic viability of advice practices. It is thus crucial that advisers understand the stages of change clients go through, how to recognise what stage they are in, and the practical steps they can take to help clients progress through each stage. These steps include the way advisers engage and communicate with their clients, and even the physical office environment in which that engagement takes place.

———-