2025-26 saw lots of noise but strong returns (again) – can it continue?

Shane Oliver

Key points

- While we saw a long list of worries over the last year, 2025-26 saw another financial year of strong returns.

- Risks around Iran and oil, various other geopolitical issues, sticky inflation and possible further rate hikes and AI related bubble worries could drive another correction in shares.

- In Australia, the main risks relate to sticky inflation, RBA rate hikes and the property downturn.

- However, with recession looking unlikely, profits likely to keep rising and the Fed and RBA likely to be cutting rates in 2027, investment returns are likely to be reasonable over the year ahead but maybe a bit slower than those of the last four years.

- The key for investors including super fund members is to maintain a long-term strategy and turn down the noise.

Introduction

The last financial year has seen investment markets climb another wall of worry, with strong returns for diversified investors. But can it continue?

Key themes – lots of noise but rising profits

The key themes over the last financial year have been:

- US trade conflicts – while US tariffs remained an issue with various flare ups the general picture was an easing of tensions as the US backed down from its extreme “Liberation Day” threats, countries including China signed “deals” and the US Supreme Court ruled against US reciprocal tariffs, albeit they’re being replaced with others.

- Geopolitical tensions – notably with the US intervening in Venezuela, threatening to take Greenland, attacking NATO allies & attacking Iran.

- An oil supply shock – the Iran War and Iran’s effective closure of the Strait of Hormuz disrupting 20% of global oil and gas supplies saw the world oil price initially spike to around $US120/barrel but it was gradually reversed as the world relied on reserves and in anticipation of an interim peace deal which has been agreed but remains shaky. This saw oil prices fall back to near pre-War levels around $US70.

- Worries about rising public debt – several major developed countries, including the US are running budget deficits above 5% of GDP. Concerns on this front were earlier enhanced by the Trump Administration’s attacks on the Fed although pressure from markets, Congress and the Supreme Court forced Trump to back down.

- Better than feared economic growth – despite another round of recession fears on the back of the oil shock, global growth has remained around 3% and the Australian economy has kept growing.

- Ongoing China worries, but it seems okay – despite an ongoing property slump the Chinese economy has continued to grow at a reasonable pace by boosting exports outside the US.

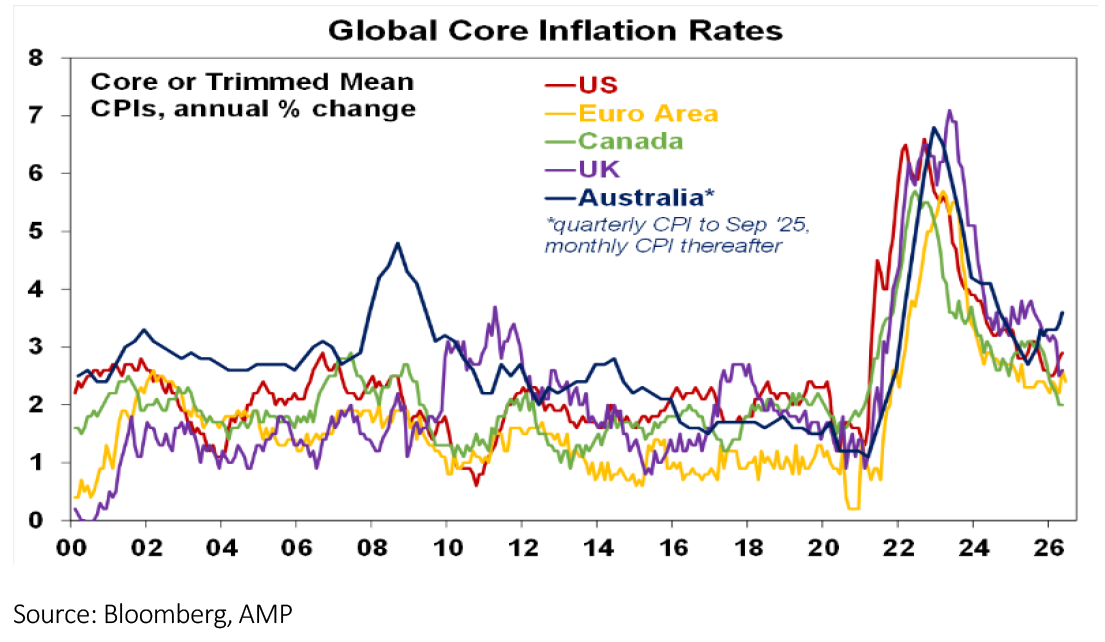

- Sticky inflation & more cautious central banks – while central banks including the RBA had been cutting interest rates in 2025, they turned more cautious in the last six months as inflation proved sticky and the oil shock added to inflation fears. The RBA led the change with three rate hikes starting before the War as underlying inflation rose relative to other countries. And market expectations for the Fed swung from cuts to hikes. This saw the $US rise in the last few months.

- AI enthusiasm – AI has continued to boost, mainly US, tech stocks with optimism about its productivity enhancing benefits.

- Surging profits – and partly related to this, profits rose strongly providing an offset to geopolitical, oil and interest rate concerns.

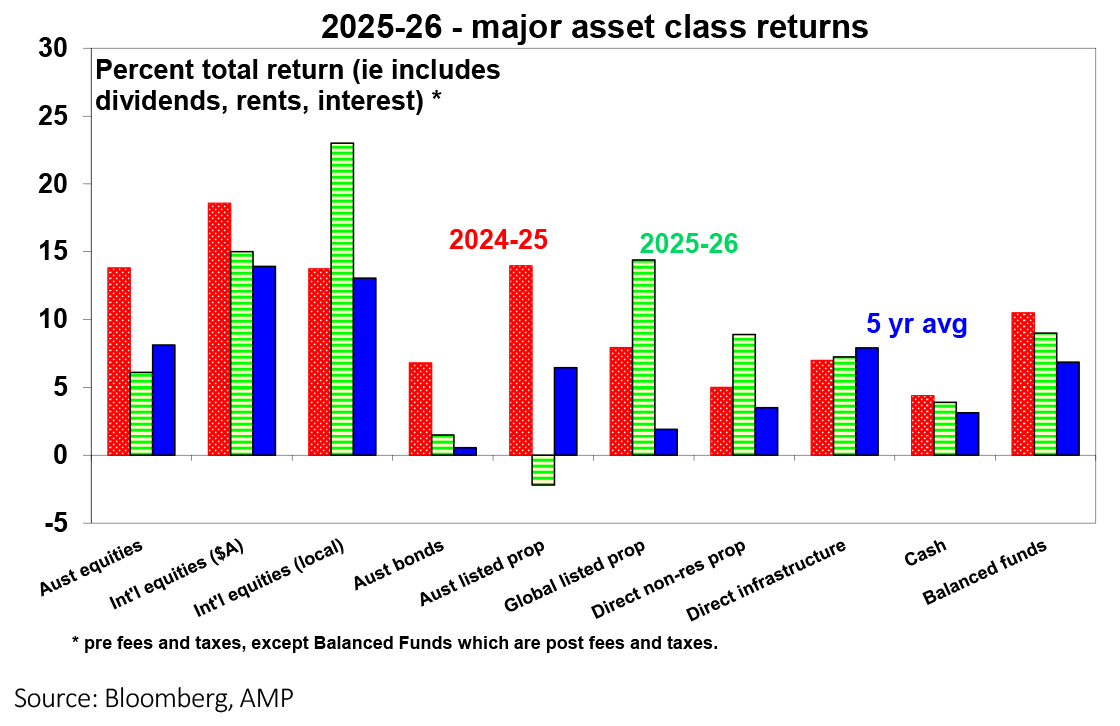

Another financial year of strong returns

The result has been another financial year of strong investment returns.

- Global shares returned 23% in local currency terms over 2025-26 helped by strong profits, but with a rise in the $A cutting this to 15% in $A terms. Japanese, Asian and Chinese shares outperformed.

- Australian shares underperformed with a 6.1% return, not helped by RBA rate hikes, stock specific issues and Budget tax hikes on investors.

- Global listed property returned 14.4%, but Australian REITs lost 2.2%.

- Unlisted commercial property returns remained strong after their 2022-24 slump helped by better leasing and rental growth.

- Bond returns were poor on inflation & central bank rate hike worries.

- Cash returned 3.9%, down from 2024 as rates fell in 2025.

- Gold surged into January on worries about debt and “US dollar debasement” but struggled along with Bitcoin over the last six months not helped by a stronger $US and US rate hike talk.

- Australian home prices rose 7.3%, but fell in the last quarter as rate hikes, investor tax hikes and poor confidence hit. Perth, Darwin and Brisbane boomed but prices in Melbourne fell and Sydney was flat.

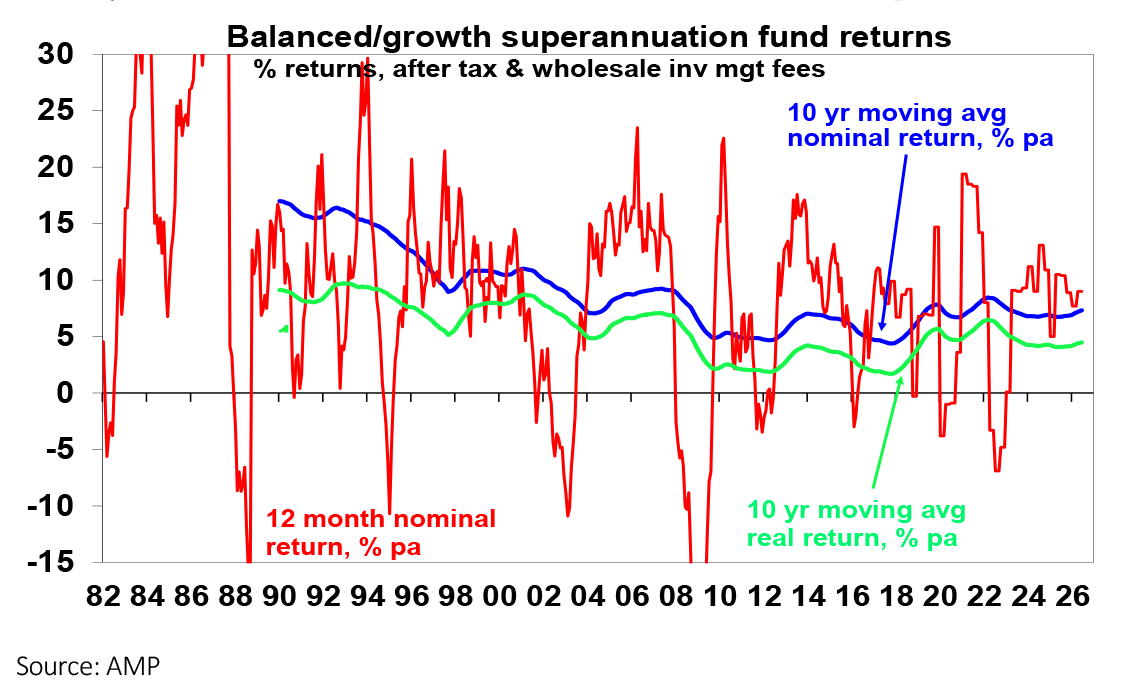

- Combined this drove a 9% or so return in average balanced growth super funds, down from 10.5% in 2024-25 but still strong.

This makes four financial years in a row of strong (9 to 10%) average super fund returns, after the inflation blowout of 2022 depressed returns. History warns a setback is likely sooner or later so it’s best to focus on longer-term returns which have been 7.3% pa over the last decade or 4.5% pa after inflation. And that’s after fees & taxes, which is pretty good.

Some lessons from 2025-26

The past financial year provided several lessons for investors. First, Trump still faces constraints from markets, consumers and GOP politicians and so backed down (“TACOed”) on his Iran threats as his popularity collapsed, opting for a deal team that seems to have left Iran the winner. Second, markets have learned after numerous experiences that TACO is the norm and so now assume it will happen eventually. Third, the world seems to have become even less vulnerable to oil supply shocks (although a run down in reserves played a big role here). Fourth, unless real economic activity and profits fall investment markets will ultimately look through a geopolitical shock. Finally, the last financial year was another reminder of just how hard it is to time markets. Shares plunged into March, only to bottom out and then for global shares to quickly make new record highs.

Key risks to look out for

There are several risks for investment markets in the year ahead:

- Trump’s luck may run out – the Administration’s decision-making process looks long on bravado & group think but lacks consideration of the risks (e.g. that China could retaliate on trade with rare earth bans or that Iran would block the Strait). So far, he’s been able to manage it by just backing down but it will come at a cost to American credibility. Eg, the Iran peace deal looks fragile with little really gained so it could flare up again threatening a more serious hit to oil supplies.

- Trump will be less constrained after the midterm elections – with a window next year before the presidential election in 2028 Trump might decide to ramp up foreign adventures including another go at Iran, and maybe Greenland and Cuba. This is particularly so if he loses the House and the Senate in November. Alternatively, he could join the Democrats in a agreeing to a billionaires’ tax or AI restrictions.

- With its war in Ukraine not going well, Russia could decide to escalate – e.g. with an attack on Poland to test NATO.

- Risks remain around the Chinese economy and tensions with the US – although these look contained for now.

- Public debt worries could flare up again – this is particularly the case in the US where the budget deficit remains around 6.5% of GDP and could put upwards pressure on bond yields. A renewed tilt by Trump to undermine the Fed’s independence could accentuate this.

- There is an ongoing risk that the AI boom is morphing into a bubble – the main concerns are centred around the sustainability of related profits. We think it has further to go, but surging IPOs and debt to fund data centre capex are warning signs.

- Inflation is a bit sticky – and it may get another boost from the AI boom with Apple and Microsoft already announcing price rises due to rising memory costs. This could see more rate hikes.

- In Australia the combination of RBA rate hikes and falling home prices on the back of the Budget tax hikes could threaten recession. We continue to anticipate a further increase in interest rates from the RBA reflecting underlying inflation running well above target with the next hike likely in August. But next year we expect the RBA to start cutting which should help stabilise growth and property prices, which we expect will see around a 7% top to bottom fall.

- Shares are overvalued – this is all coming at a time when US and Australia share valuations are stretched offering little risk premium over bonds. But this has been the case for two years now!

These risks could easily trigger a new bout of volatility – potentially in the seasonally weak months of August and September and the period ahead of the US midterms has historically seen bouts of weakness. However, similar things could have been said in the last two years, and both financial years saw solid returns. In the absence of recession, solid profit growth and the Fed and RBA likely to cut rates next year should result in okay overall returns over the next 12 months. So, while we may see renewed volatility, super returns overall should be reasonable this financial year albeit after four years of returns around 9-10% some slowing is to be expected to around 6-7%. For the ASX 200, we expect it to rise to around 9200 over the next 12 months.

Nine key things for investors to always keep in mind

- Make the most of compound interest to grow wealth. Saving in growth assets can grow wealth significantly over long periods.

- Don’t get thrown off by the cycle. Falls in asset markets can throw investors off a well-considered strategy, destroying potential wealth.

- Invest for the long-term. Given the difficulty in timing market moves, it’s best to get a long-term plan that suits circumstances and stick to it.

- Diversify. Don’t put all your eggs in one basket.

- Turn down the noise. The key is to avoid the click bait, turn down the noise and stick to a long-term strategy.

- Buy low, sell high. The cheaper you buy an asset, the higher its prospective return will likely be and vice versa.

- Avoid the crowd at extremes. Don’t get sucked into euphoria or doom and gloom around an asset.

- There is no free lunch! If an investment looks dodgy, hard to understand or has to be justified by odd valuations, then stay away.

- Seek advice. Investing can get complicated.

By Dr Shane Oliver, Head of Investment Strategy and Chief Economist, AMP