Reece Birtles

As we approach the end of Australian company reporting season, the results have demonstrated resilience of company performance in the face of fears about inflation, rate rises and recession notes Martin Currie, an active equities investment manager, part of Franklin Templeton.

Reece Birtles, chief investment officer Martin Currie, says there are already some clear trends emerging.

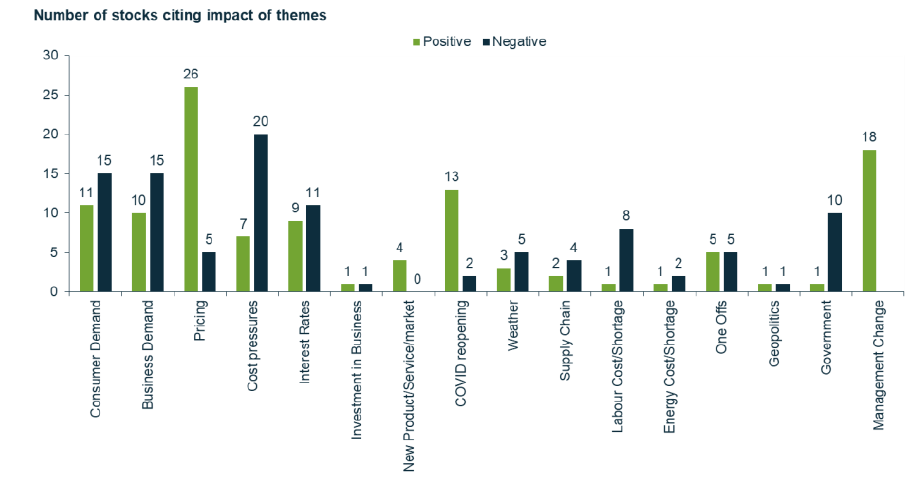

“The dominant themes influencing company beats and misses have been pricing power, cost pressures, leverage to interest rates, COVID reopening and resilient but softening consumer and business demand. Broad market earnings growth expectations have been trimmed to zero for the year ahead emphasising the importance of focusing on resilience of earnings in a slowing economy and wide valuation dispersions across stocks,” says Birtles.

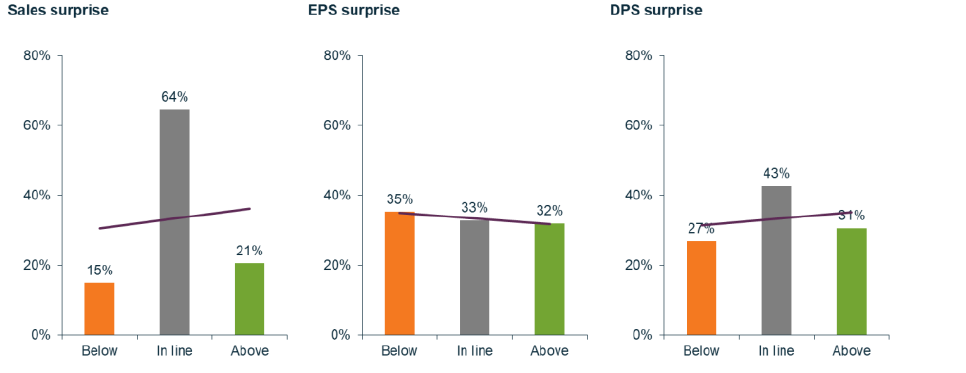

“There has been an overwhelming number of sales / revenue results in line with consensus expectations with an even balance of earnings / dividend surprises and disappointments.”

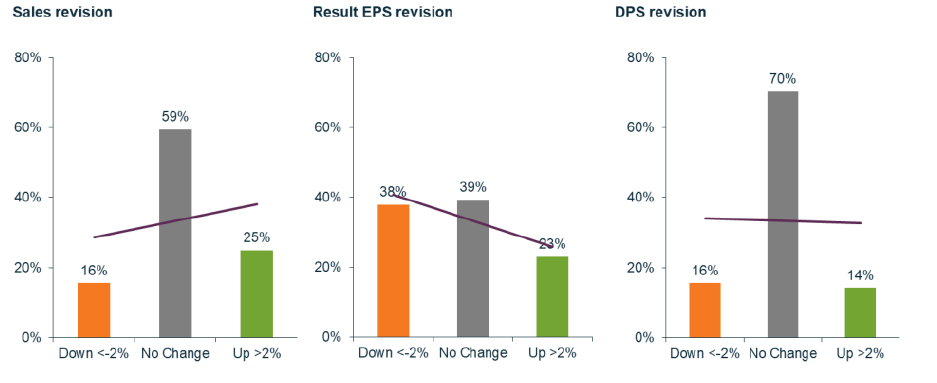

“Similarly with respect to guidance revisions, a generally benign outlook for sales / revenue offset by worsening costs indicative of the inflationary environment has led to a marginally negative skew for EPS guidance feeding through to strong resilience in dividend expectations.”

Birtles adds: “In fact, the key theme of results overall is the lack of volatility across the board, despite how it may feel. We have been looking for material evidence of the interest rate induced recession; however, the numbers simply don’t show that yet, notwithstanding management commentary pointing to some clouds on the horizon.

“The top issues cited by companies, in both results and guidance outlooks, are pricing strength and consumer / business demand. Management change and the benefits of post-COVID reopening have been frequently cited as positives while cost pressures, the impact of increasing interest rates and ongoing labour shortages are consistent negatives.

“There has been surprisingly little mention of supply-chain pressures and the energy crisis although there have been pockets of concern over the potential impact of government intervention.

“The cracks are more evident when looking across sectors with weaker first halves especially visible in Energy and Utilities feeding through to decreased market confidence in the second half outlook for earnings in these sectors. Lower quality stocks have also borne the brunt of negative earnings revisions, although an increasing number of mid-strength quality companies have generated negative EPS outlooks indicating a tougher profit cycle for some on the horizon.

“From a total market perspective, consensus EPS over the next twelve months is expected to hold steady, reflecting robust sales and revenue expectations but offset by increasing cost pressures. This points to an environment where stock selection will continue to dictate the total return outcome for portfolios more so than has been the case over the last decade,” says Birtles.