Investment markets and key developments

Global shares rose again over the last week, helped by ongoing confidence that major central banks are on track to cut rates this year and strong US earnings results. The Australian share market rose around 1.7% helped by the positive global lead and a less hawkish than feared RBA with the gains being led by utility, energy, property and IT shares. Bond yields fell in the US and Australia but were flat to up in Europe and Japan. Oil and metal prices rose but the iron ore price fell back a bit. The $A was little changed with the $US up slightly.

Shares have had a nice rebound from their falls in April, but the ride is likely to remain more volatile and constrained than we saw in the first three months of the year, as valuations remain stretched, sentiment didn’t fall to bearish extremes, uncertainty remains regarding the outlook for interest rate cuts and geopolitical risks around the Israel/Iran conflict and US election are high. However, we continue to see further gains in shares this year though as disinflation resumes, central banks ultimately cut interest rates and recession is avoided or proves mild.

Are Chinese shares in a new bull market? At their February low Chinese shares had fallen 45% from their 2021 high on the back of worries about the Chinese property market and economy and this left them very undervalued trading on a PE of around 10 times and under loved. Since then, they have rebounded 15%, with a recent pause giving way to a new recovery high. At this stage it’s too early to tell if it’s just a bounce or the start of a new bull market. But there are some positives supporting the case for more upside. While Chinese policy stimulus has been light on, the economy has been better than feared defying forecasts of a property driven collapse. And the strength in copper prices and the pickup in iron ore since its April low are providing some positive confirmation of possibly better conditions in China. If it does have further to go its positive for the $A, which has so far been a laggard but is looking a bit stronger lately, and for resources shares.

RBA held at 4.35%, retained a formal neutral bias in “not ruling anything in or out” but with more hawkish language suggesting its more cautious on inflation. The bad news is that the RBA still considers the jobs market as too tight, inflation is falling more slowly than expected, it revised up its inflation forecasts for this year and it actually considered hiking again. In the event, the RBA decided to leave rates on hold on the grounds that rates are restrictive enough, higher rates have impacted households more than in other countries because of a high share of variable rate mortgages and it still sees inflation falling back to the high end of the target range by end next year and to the mid-point by mid-2026. In other words, it sees the hot March quarter CPI and near-term pressures from higher fuel prices as temporary and not warranting a further tightening and has chosen to simply go down a similar path to the Fed in effectively ratifying “high for longer rates” rather than seeing a need for “higher rates”. However, its language is more hawkish than after its March meeting suggesting a low tolerance for anything that leads it to forecast that it will take “markedly longer” to get inflation back to target. The Governor’s use of the word “markedly” suggests the hurdle to hike again is high, but it’s likely that near term risks are still skewed up for rates. Key things to watch apart from inflation are whether the Budget adds extra net stimulus to the economy for the next year, the impact of the 1 July tax cuts on consumer spending and the size of the rise in minimum and award wages in the upcoming Fair Work Commission decision.

Meanwhile, the Bank of England left rates at 4.25%, but was dovish and looks to be preparing for a June rate cut with: two votes for a cut; inflation forecasts revised down; Governor Bailey indicating the BoE will likely need to cut…over coming quarters”; and the Bank noting that it will “consider forthcoming data” and how it informed its assessment that inflation risks are receding. The money market is pricing in a 78% probability of a cut in June.

And the Swedish Riksbank became the second developed country central bank (after the Swiss) to cut rates. The Riksbank’s cut its key policy rate by 0.25% to 3.75% citing inflation nearing its target and weak economic activity. It also flagged two rate cuts in the second half if inflation continues to fall. So, despite slippage at the Fed, the global trend in rates is still down.

Major global economic events and implications

It was a relatively quiet week for US data releases. However, the latest Fed survey of bank loan officers showed a further tightening in lending standards (except for prime mortgages), but at a slowing rate. Meanwhile unemployment claims rose but remain low.

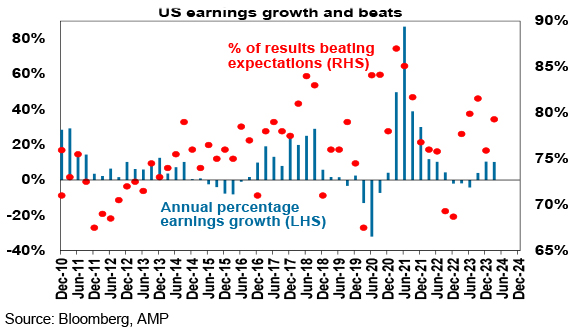

US March quarter earnings were strong. 92% of S&P 500 companies have reported with 79% beating, against a norm of 76% and earnings growth expectations now at 10.2%yoy, up from 4.1% 4 weeks ago. Tech earnings are up 38%yoy with growth cooling whereas ex-tech earnings are up 1%yoy with growth accelerating.

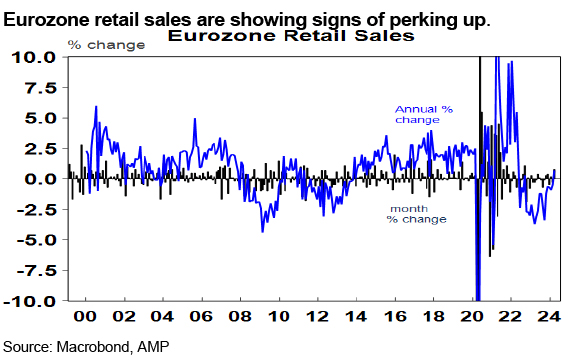

Eurozone retail sales are showing signs of perking up.

Chinese exports and imports both rose more than expected in April, partly helped by a soft base a year ago.

Australian economic events and implications

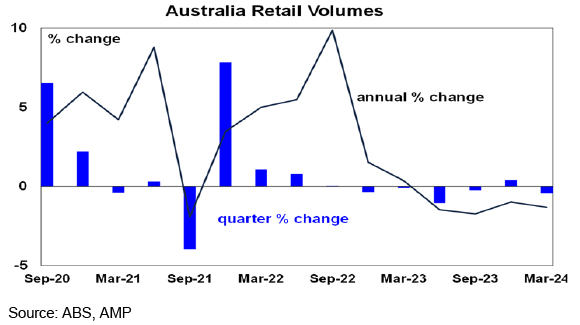

The weakness in Australian consumer spending was highlighted yet again with real consumer spending down 0.4%qoq in the March quarter. This was worse than expected with real retail sales now down five of the last six quarters consistent with flat to down March quarter consumer spending. What’s more real per person spending was down 1%qoq or 3.6%yoy and has fallen for seven consecutive quarters. Real retail sales in key discretionary areas like household goods, clothing and department stores are all down on a year ago. Cost of living pressures are clearly continuing to hit along with high interest rates in working to cool demand.

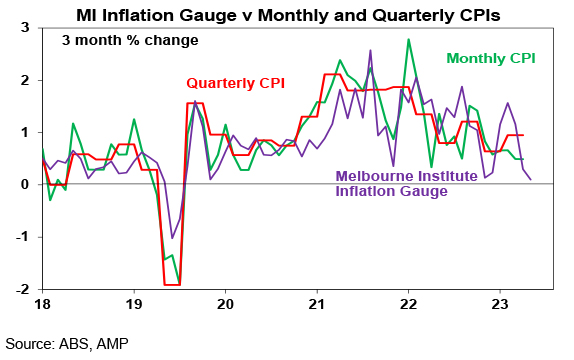

The Melbourne Institute’s Inflation Gauge points to a renewed slowing in CPI inflation in April. According to the Gauge inflation was 0.1%mom slowing to 3.7%yoy with its trimmed mean slowing to 3.2%yoy. But the cooling pace of monthly inflation in the Gauge and in its trimmed mean point a slowing in inflation in April.

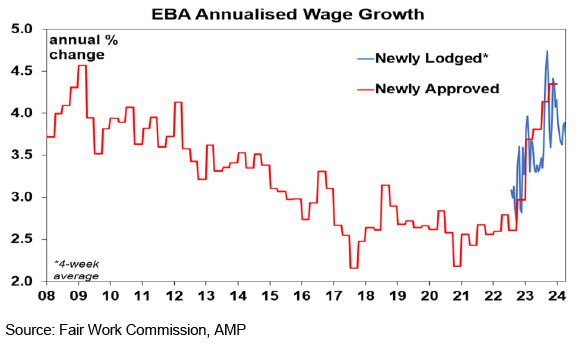

Newly lodged enterprise bargaining wage agreements continue to suggest the pace of wage rises under EBAs have peaked.

What to watch over the next week?

In the US the focus will be back on inflation with the April CPI (Wednesday) expected to show a slight slowing to 0.3%mom or 3.4%yoy from 3.5%yoy and core inflation slowing to 0.3%mom or 3.6%yoy from 3.8%yoy. Producer price inflation data will also be released Tuesday. In other data expect a slowing in April retail sales growth (Wednesday) and in industrial production (Thursday) but stronger housing starts (also Thursday). Small business optimism for April (Tuesday) is likely to have remained soft and May manufacturing conditions for the New York and Philadelphia regions are likely to weaken a bit.

Japanese March quarter GDP growth is expected to slip back into negative with a 0.4%qoq fall after a 0.1%qoq gain in the December quarter with weak consumer spending, investment and trade.

Chinese economic activity data for April (Friday) is expected to show a modest improvement with slightly stronger growth in industrial production, retail sales and investment.

The 2024-25 Australian Budget (Tuesday) looks like it’s going to be mainly about whether it makes the RBA’s job in fighting inflation easier or harder in the near term and getting “Future Made in Australia” (FMIA) protectionism underway over the medium term. Key features are likely to be:

- Minimal cost of living measures for low to middle income workers, including an extension off energy bill relief.

- A renewed talking up of the benefits to low and middle income households from the rejigged Stage 3 tax cuts (worth $1929pa for those on $90,000pa and $2429pa for those on $110,000pa).

- A combination of subsidies, tax breaks, cheap loans & relaxed foreign investment rules to boost investment in government chosen industries in a return to post war protectionism and picking winners as part of the “Future Made in Australia” policy.

- Specific measures to include $91m to train home builders (although there is something like this every year and the planned 22,000 new workers is only a modest 1.7% boost to the total construction sector workforce) and a change to the indexation of student debt which reduces the value of debt by an average $1200 but without any near-term budget impact as it won’t involve a handout to students.

- Some further savings in areas like consultant fees, tougher compliance and efficiencies.

- Net immigration of 450,000 this financial year up from a MYEFO forecast of 375,000, falling to 250,000 in 2024-25.

- A budget surplus of around +$13bn this financial year (MYEFO forecast a deficit of -$1bn) thanks to higher than forecast commodity prices and personal tax collections, but a return to a deficit of around -$15bn in 2024-25 (MYEFO forecast a deficit of -$19bn). March budget data shows a financial year to date deficit of just $2bn which is $4bn better than projected in MYEFO. As its tracking better than the 2022-23 budget profile another $22bn plus surplus is possible this financial year. However, with the Government admitting that new spending in the Budget will exceed $25bn in revenue upgrades over four years, deficits are likely to worsen for 2025-26 (MYEFO was -$35bn) and 2026-27 (MYEFO was -$19.5bn) and thereafter.

- The 2023-24 GDP growth forecast may be revised down to 1.5% from 1.75% with the growth forecast for 2024-25 being revised down to 2% from 2.25%. Inflation forecasts are likely to remain at 3.75% for this financial year (which is similar to the RBA’s 3.8%) but be revised up to 3% for next financial year from 2.75%.

The key is that with inflation proving sticky the Budget needs to take more out of the economy for the next financial year than it puts back in so as to make the RBA’s job easier. Any near term spending associated cost of living relief, “Future Made in Australia” subsidies or other measures should be more than offset by savings elsewhere. From 2025-26 inflation should be less of a constraint. But extra spending as already flagged by the Government will add to the upward drift in government spending as a share of the economy. In the December mid-year review Federal spending as a share of GDP was already projected to average 26.2% over the long term which is well above the pre-pandemic average of 24.8%. Ever bigger government and now a return to the failed industry policies of the past, ie to pick winners and protectionism under FMIA, are not the answer to Australia’s poor productivity performance. In fact, they risk making it worse.

On the data front in Australia, expect March quarter wages growth (Wednesday) to remain at 0.9%qoq or 4.2%yoy and April jobs data (Thursday) to show employment up 25,000 after a 6600 fall and unemployment to rise to 3.9%. Note that the jobs report has been erratic lately partly reflecting changed seasonal patterns so its dangerous to read too much into monthly movements. The NAB April business survey will be released Monday. RBA Chief Economist Sarah Hunter will deliver a speech on Thursday which is likely to be consistent with recent RBA commentary but will be watched for any reaction to the Budget.

Outlook for investment markets

Easing inflation pressures, central banks moving to cut rates and prospects for stronger growth in 2025 should make for good investment returns this year. However, with a high risk of recession, delays to rate cuts and significant geopolitical risks, the remainder of the year is likely to be rougher and more constrained than the first three months were.

We expect the ASX 200 to return 9% this year and rise to around 7900. A recession is probably the main threat.

Bonds are likely to provide returns around running yield or a bit more, as inflation slows, and central banks cut rates.

Unlisted commercial property returns are likely to be negative again due to the lagged impact of high bond yields & working from home.

Australian home prices are likely to see more constrained gains in the year ahead as the supply shortfall remains, but still high interest rates constrain demand and unemployment rises. The delay in rate cuts and talk of rate hikes risks renewed falls in property prices as its likely to cause buyers to hold back and distressed listings to rise.

Cash and bank deposits are expected to provide returns of over 4%, reflecting the back up in interest rates.

A rising trend in the $A is likely taking it to $US0.70 over the next 12 months, due to a fall in the overvalued $US, but in the near term the risks for the $A are on the downside as the Fed delays rate cuts and given the still high risk of an escalating conflict in the Middle East.

By Shane Oliver