Understanding the importance of ethical principles as they apply to estate planning.

Estate planning sits at the intersection of finance, law and family. For advisers, it brings unique ethical challenges: how to respect the wishes of a client while also acknowledging the influence of family dynamics and upholding professional duty? This article, proudly sponsored by GSFM, explores these ethical challenges and how the principles that underpin ethical conduct intersect with estate planning.

Estate decisions are rarely black and white; they often involve difficult trade-offs between fairness and equality, confidentiality and transparency, and emotional versus rational choices. Navigating these dilemmas requires not only technical knowledge but also empathy and a strong ethical compass.

The importance of sound estate planning has become more apparent with the significant transfer of intergenerational wealth over the coming years. The most recent numbers suggest $5.4 trillion will transfer from older to younger generations over the next 20 years[1].

The role of the adviser in estate planning

Financial advisers are central to the estate planning process. While you will likely need to work with other professionals, such as accountants and estate lawyers, the adviser’s role is critical to help clients protect assets, minimise tax exposure and ensure each client’s wealth is distributed according to their wishes.

While technical expertise in areas such as trusts, superannuation and tax planning is essential, the adviser’s role extends beyond numbers and structures. Estate planning is as much about people as it is about money, and advisers are often called upon to act as confidants and mediators. This is why the trust relationship between adviser and client is so important.

One of the most valuable contributions an adviser makes in the estate planning process is to provide an impartial perspective. Estate planning discussions often involve deeply personal issues: changing family dynamics, second marriages and blended families, and sometimes, conflicting views about fairness versus equality. In these situations, advisers are often the only objective voice in the room, their role to help clients navigate competing priorities while remaining focused on long-term goals. By approaching these conversations with empathy and professionalism, advisers can defuse tension and help clients make thoughtful, values-aligned choices.

At the core of the adviser’s role lies fiduciary responsibility: the duty to always act in the client’s best interests, a concept that underpins the Financial Planners and Advisers Code of Ethics. Yet what constitutes “best interests” is not always clear-cut.

A client may wish to leave unequal inheritances to children based on differing financial needs, exclude a family member altogether, or allocate a significant portion of their estate to charitable causes. While these decisions may spark disagreement within the family, the adviser’s duty is to honour the client’s instructions and ensure that all decisions are clearly documented, legally sound and tax efficient.

Advisers may also play a preventative role and help clients to anticipate and mitigate potential disputes. For example, advisers might recommend:

- one or more family meetings to explain estate intentions

- the use of testamentary trusts to manage complex distributions

- the client records their reasoning for the distribution of assets in a letter of wishes.

By proactively addressing sources of conflict, advisers can help reduce the risk of costly litigation and preserve both wealth and family harmony.

Ultimately, the adviser’s role in estate planning is multifaceted: part financial strategist, part empathetic listener, part risk manager. By combining technical expertise with ethical judgment and interpersonal skills, advisers help clients transfer assets efficiently and leave behind a legacy that reflects their values and intentions.

Common ethical dilemmas in estate planning

Conflicts of interest

A common dilemma arises when one or more family members push for outcomes that differ from the client’s wishes. For example, a child may lobby for a larger share of the estate, or siblings may pressure an ageing parent to change their will. Advisers can find themselves in a challenging situation, particularly multiple members of the same family are clients.

The ethical principle here is clear: the adviser’s duty lies with the client who engaged them, not with interested relatives.

Capacity and vulnerability

Australia is experiencing an increase in both longevity and dementia. In 2025, there are 443,000 Australians living with dementia, a figure expected to increase significantly in coming years[2]. Therefore, it’s important to understand that as clients age, their cognitive capacity may decline. Unfortunately, this can open the door to undue influence from relatives or caregivers. An adviser may suspect that a client is being pressured into decisions that do not reflect their true wishes, but proving this can be difficult.

In such cases, advisers face a dilemma: respect the client’s autonomy or intervene to protect them from potential exploitation? The ethical principle here is clear: the adviser’s duty lies with the client and acting in their best interests. It also good practice to document all decisions – and the rationale for each – to quickly deal with issues that arise from family members or other interested parties.

Fairness versus equity

One of the most emotionally charged dilemmas is whether assets should be divided equally or fairly among beneficiaries. Equality suggests each child receives the same amount, but fairness may account for differences. Examples include a child who provided years of care to a parent, one who already received significant financial support during their life or one who is disabled and requires ongoing care.

Advisers may often find themselves guiding clients through the difference between fairness and equality. The ethical challenge lies in supporting the client’s values while recognising the potential for resentment among heirs. Advisers must help clients make decisions they can defend, ideally with clear reasoning documented in writing.

Professional duty and ethical standards

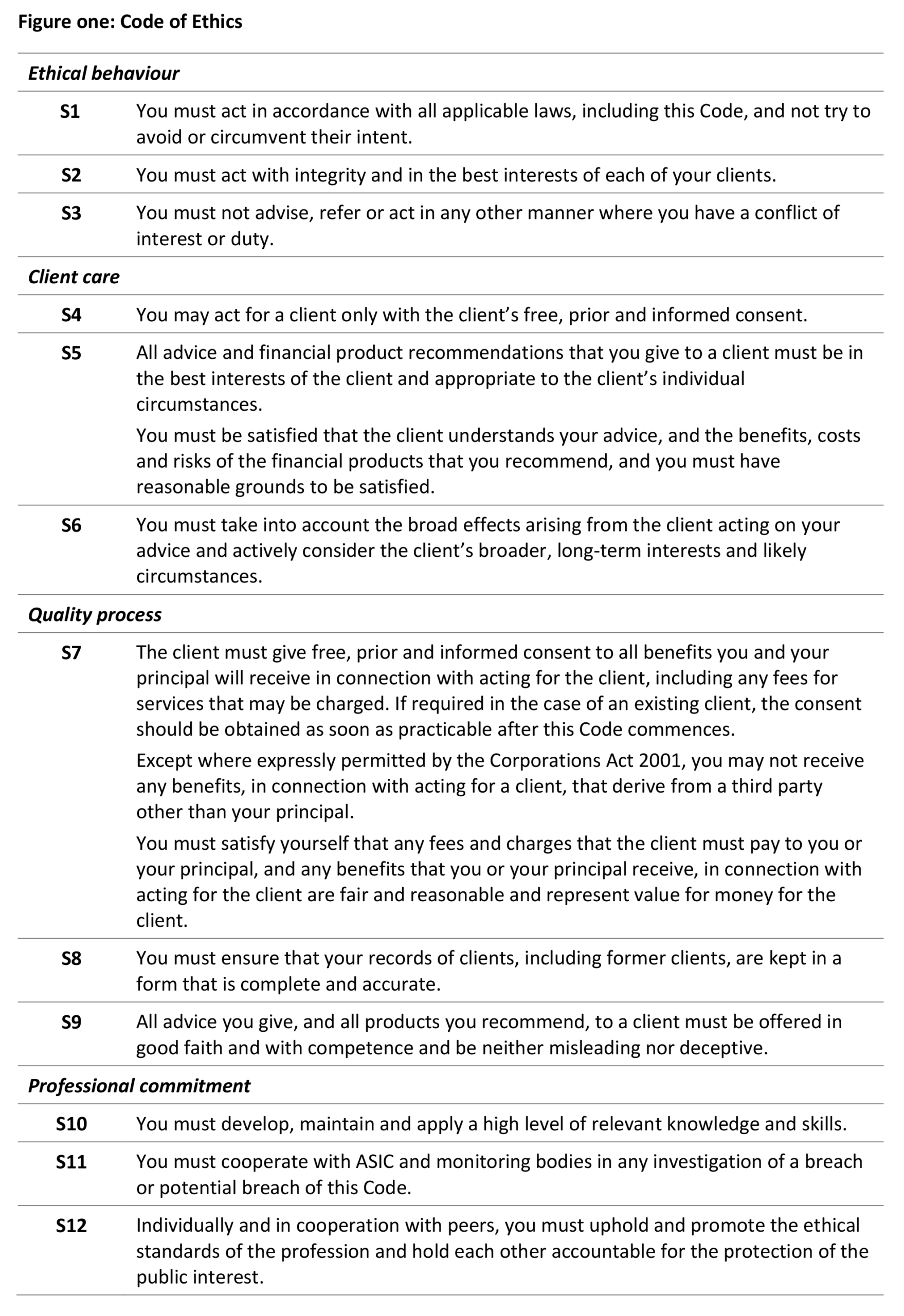

The Code of Ethics provides the foundation for ethical and compliant advice. By adhering to these standards that make up the Code of Ethics (figure one), advisers can provide guidance that is not only technically sound but also ethically defensible.

For the client, the Code of Ethics ensures advice is trustworthy, confidential and truly in their best interests. For the adviser, it provides clarity, protection from disputes and the confidence to navigate complex family dynamics without losing impartiality.

By grounding estate planning advice in professional duty and regulatory standards, advisers safeguard both the financial outcomes of the estate plan and the integrity of the process itself.

Acting in the client’s best interests

At the heart of estate planning is the fiduciary obligation to act in the client’s best interests. Yet, “best interests” is not always clear-cut. For example, a client may choose to:

- Disinherit one child due to estrangement

- Gift unequal amounts to children, perhaps favouring a carer

- Leave substantial assets to charity, against family wishes

These decisions may conflict with what others perceive as fair, but advisers must respect client autonomy while ensuring decisions are lawful, transparent and properly documented. Standards 2 and 5 reinforce this by requiring advisers to act with integrity and provide advice that is not only legally compliant but also demonstrably in the client’s best interests.

Integrity: avoiding conflicts of interest

Integrity underpins all ethical decision-making. In estate planning, conflicts often arise subtly. For example, an adviser might be working with multiple family members, each with competing interests.

Standard 2 requires advisers to act with integrity, while standard 3 explicitly prohibits conflicts of interest, real or perceived. Advisers must therefore be transparent about their role, disclose any potential conflicts, and, where necessary, decline to act if impartiality cannot be maintained. In practice, this may mean referring some family members to independent advisers to avoid perceptions of bias.

Competence: multidisciplinary knowledge

Estate planning touches on multiple domains – tax, superannuation, trusts, property law, the list goes on. No single adviser can be expert in all these areas, and the Code of Ethics recognises this. Standard 9 requires advisers to ensure their advice is appropriate and informed by the necessary expertise and standard 10 requires that advisers develop, maintain and apply a high level of relevant knowledge and skills.

Competence, one of the values that underpins the Code of Ethics has two dimensions:

- Staying current – estate planning legislation changes frequently, examples being superannuation reforms or updates to taxation of trusts. Advisers must engage in ongoing professional development to ensure recommendations are accurate.

- Knowing when to collaborate – complex estates often require input from specialist lawyers and accountants. Ethical advisers do not stretch beyond their remit; instead, they coordinate with other professionals to deliver positive outcomes for clients.

Accountability: record-keeping and transparency

When disputes arise, detailed records are an adviser’s strongest defence. Estate planning decisions are often contested, especially where distributions are unequal or complex family structures exist. Standard 8 and ASIC’s compliance requirements highlight the importance of keeping thorough and contemporaneous records.

Best practice includes:

- Documenting the reasoning behind each recommendation.

- Recording client instructions and conversations around sensitive matters.

- Retaining evidence of collaboration with legal or tax professionals.

These records provide transparency for the client and protection for the adviser. Should a decision be challenged in court, written documentation demonstrates that the advice process was both ethical and compliant, and aligned with professional duty.

However, even with clear frameworks, it’s likely that advisers will face grey areas. For example:

- Family members who are also clients lobby the adviser to influence the older client’s decision making.

- A client appears to be making decisions based on temporary emotions rather than long-term goals.

- Beneficiaries are treated unequally.

Where there are grey areas, the Code of Ethics can provide an ethical compass. It requires advisers to prioritise honesty, fairness and the client’s informed consent. By applying these principles, advisers can navigate uncertainty with confidence that their decisions are ethically sound.

Strategies for ethical estate planning

While ethical dilemmas in estate planning cannot always be avoided, advisers can adopt proactive strategies to navigate them effectively and reduce the likelihood of conflict. These strategies not only protect the adviser’s professional integrity but also help clients achieve outcomes that align with their intentions and values.

- Encourage open communication – where possible, help clients explain their decisions to family members in advance. This can prevent surprises and reduce disputes.

- Document thoroughly – keep detailed notes of client conversations, especially around sensitive decisions. Written evidence provides protection if decisions are later contested.

- Involve other professionals – ethical estate planning often requires a multidisciplinary approach. Estate lawyers, tax specialists, and sometimes medical professionals can provide objective input and helps ensure decisions are in the client’s best interests.

- Promote clarity in estate documents – ambiguity can lead to disputes. Advisers can encourage clients to include explanatory notes, such as a letter of wishes, alongside formal documents like wills or trusts. While not legally binding, these notes provide context and reduce misunderstandings, helping beneficiaries accept decisions even when they may not agree with them.

- Stay impartial – Even when family members are vocal, advisers must maintain neutrality and avoid giving the impression of siding with one party.

- Review regularly – estate planning is not a “set and forget” exercise. Life events – such as marriage, divorce, births, deaths, or the sale of a business – can quickly make an existing plan outdated or inappropriate. Advisers should encourage regular reviews to ensure the estate plan continues to reflect both the client’s circumstances and their intentions.

Case studies

The following case studies are mostly based on real events; however, the names of people and organisations have been changed, and some details altered. The case studies have been drawn from ASIC and the Australian Financial Complaints Authority (AFCA). For each, potential breaches of the Code of Ethics are identified.

Case study one: The guardian

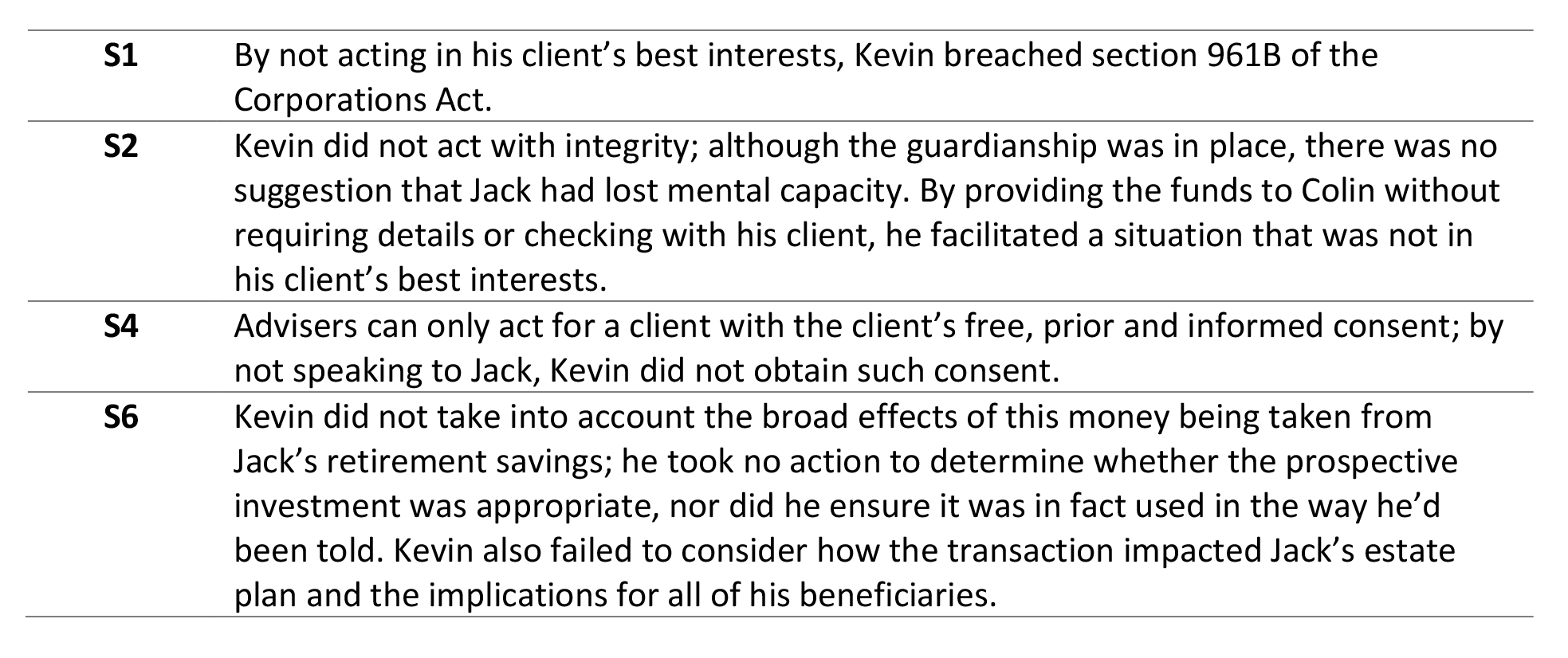

Jack is in his early 90s and a client of ABC Finance. A few years ago, his investment banker son Colin established an enduring power of attorney and guardianship should his father require stewardship in his later years. His financial adviser Kevin was aware of this and met Colin with Jack at several meetings spanning 3-4 years. Although frail, Jack has always displayed great mental acuity.

Because of Colin’s financial services background, he has taken a great interest in his father’s financial affairs and was heavily involved in his estate planning process. Jack planned to leave his estate split equally between his three children.

Five years after the guardianship was established, Colin contacted Kevin to transfer a significant sum of money from an investment account Jack held, to one in his own name. He told Kevin he was going to add the money to a sum of his own and invest it in a limited opportunity, one which would yield a good return for Jack. Kevin accepted Colin’s explanation and actioned the transfer.

It transpired that the funds were used to fund a business for Colin’s wife and not for Jack’s benefit. Jack complained that the transaction had occurred without his consent, and it meant that his other children would be negatively affected because it involved a significant amount of the capital that he intended to bequeath them.

Although AFCA acknowledged that employees of financial firms are not expected to be detectives, it is their duty to exercise reasonable care and skill, which includes an obligation to question the client’s authorisation of a transaction. This includes circumstances where there’s a possibility that a client is being financially abused or the use of funds is not consistent with the customer’s wishes or for their benefit.

Through his actions, Kevin potentially breached the following standards in the Code of Ethics:

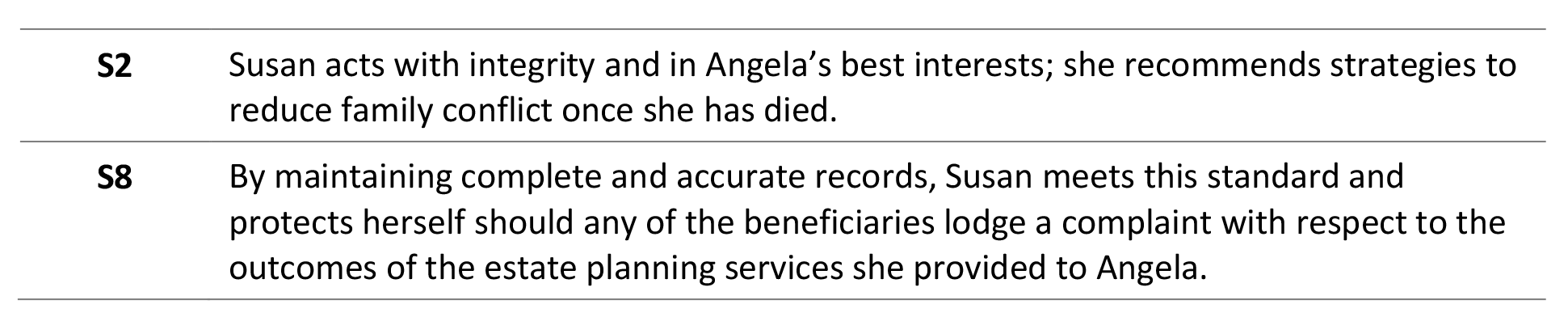

Angela is a widow with three adult children. Two of her children are financially secure; they hold good jobs, own their own home and are generally ‘doing well.’ However, her youngest has struggled with employment and relied on Angela for ongoing financial support. Angela wishes to leave a larger share of her estate to the financially vulnerable child.

Angela visits ACME Financial & Estate Planning, where she consults with adviser Susan. She explains the situation and her rationale for wanting to favour her youngest and financially insecure child. As well as her family home, Angela has a number of financial assets.

Susan recognises the risk of conflict: the two older siblings may see this as unfair. Susan’s ethical duty is to respect Angela’s wishes while minimising the likelihood of disputes. Consequently, Susan encourages Angela to:

- Document her reasoning in a letter of wishes.

- Consider leaving the family home and non-financial items of sentimental value equally.

- Discuss her intentions with her children during her lifetime, if she feels comfortable.

Further, Susan maintains meticulous records of their conversations and keeps a copy of Angela’s letter of wishes on file. By combining respect for Angela’s autonomy with practical steps to reduce conflict, Susan upholds both ethical and professional standards, notably:

Case study three: The carer

Julie is in her early 80s and a client of ACME Advice. A few years ago, Julie’s son Peter and daughter Amelia established a joint enduring power of attorney should their mother require assistance and stewardship in her later years. Julie’s financial adviser Kate is aware of the POA and has met with both children.

Following a recent stroke, Julie’s mental capacity started to decline and she became unwilling and less able to leave her home. While waiting for a government funded home care package, Amelia became her default carer. Consequently, Amelia dropped her work from full to part time hours.

Amelia contacted Kate and asked to see her. She knew that Kate had worked with Julie on her estate planning. When Amelia arrived, she presented Kate with a new Will from Julie. It had been prepared using a DIY kit and witnessed by friends of Amelia. This new Will had one significant change; Amelia was now the sole beneficiary of her mother’s home, with the other financial assets still split equally between her and her brother. The reason Amelia explained to Kate, was that she had reduced her working hours to care for Julie and was therefore entitled to be remunerated for it.

Kate contacted Julie at a time she knew Amelia would be at work to enquire about the new Will. While Julie seemed to be aware that she had signed a new document, she did not seem to be aware of the change that gave Amelia 100 percent interest in the family home. Kate was concerned this had come about via coercion and that Julie did not have the capacity to sign the legal document.

By engaging with external medical and legal experts, it was determined that Julie did not have the capacity to sign the new Will and that her previous Will would stand. Amelia was advised that her actions could constitute elder abuse, but no further action was taken.

Through her actions, Kate acted in Julie’s best interests to deliver outcomes consistent with her wishes. However, had she simply accepted the new Will, she would have potentially breached the following standards:

Case study four: The blended family

David, 75, is married to Deborah, 60. They each have adult children from previous marriages: David has two daughters, while Deborah has a son. Together, they have built a life over the last 15 years, pooling assets but also retaining some separate property. Their combined estate is worth around $3.5 million, including the family home, an investment property and superannuation.

David’s priority is to ensure Deborah can remain financially secure if he predeceases her, but he also wants his daughters to eventually inherit his share of the estate. Deborah, meanwhile, wishes her son to inherit the family home.

The couple engages Jim from ACME Advice to help structure their estate plan. They express the following wishes:

- Deborah is to remain in the family home for life, but they cannot agree as to who will inherit the home.

- David’s investment property is to go directly to his daughters.

- Joint assets, such as their superannuation, to be split evenly between all three children.

- A joint bequest of $100,000 to their preferred charity.

This provides some challenges for Jim. For example, David and Deborah’s wishes reflect a tension: Deborah wants her son to inherit the family home, while David wants his daughters to eventually receive it. Since both David and Deborah are Jim’s clients, he owes duties to each. He recommends that the home be left to all three children.

Jim explains the risks of disputes in blended families and highlights structures such as life interest trusts that would allow Deborah to stay in the home while ensuring it ultimately passes to all three children. He provides the couple with cash flow modelling to demonstrate how Deborah can be financially secure without needing outright ownership of all assets.

Through his approach, Jim acted in both David and Deborah’s best interests to deliver an estate plan and outcomes consistent with their wishes. In particular, Jim upheld the following standards:

Jim also makes a referral to an estate planning lawyer to draft legally binding arrangements and the Will; this will ensure clarity in property ownership and superannuation nominations.

Importantly, Jim documents all instructions and discussions, including potential areas of disagreement, to demonstrate impartiality and his adherence to professional duty. While the arrangement may not eliminate future family tension, the documentation and legal structures significantly reduce the risk of a successful challenge.

Through his approach, Jim acted in both David and Deborah’s best interests to deliver an estate plan and outcomes consistent with their wishes. In particular, Jim upheld the following standards:

Estate planning is never just about distributing wealth; it is about honouring values, relationships, and legacies. For financial advisers, it often means navigating a landscape where ethical dilemmas are inevitable. Conflicts of interest, issues of capacity, questions of fairness, and the tension between confidentiality and transparency can all test an adviser’s judgement.

However, the guiding principle is clear: the client’s wishes must always be considered and explored, supported by professional duty and ethical integrity. By approaching estate planning with empathy, transparency and careful documentation, advisers can help clients make decisions that not only protect assets but also preserve family harmony.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Professionalism and Ethics (0.5 hrs)

ASIC Knowledge Requirements: Estate Planning (0.5 hrs)

please log in to start this quiz

———

Notes:

[1] https://www.abc.net.au/news/2025-07-13/economist-warns-about-intergenerational-wealth-in-australia/105517036

[2] https://www.dementia.org.au/about-dementia/dementia-facts-and-figures

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Professionalism and Ethics (0.5 hrs)

ASIC Knowledge Requirements: Estate Planning (0.5 hrs)

please log in to start this quiz

———