Mano Mohankuma

Super funds had a tremendous May with the median growth fund (61-to-80% in growth assets) rising by 2.1% over the month. Taking into consideration market movements in June so far and with less than two weeks of the financial year remaining, Chant West estimates that the median growth fund return for FY26 to date is at 9%.

Head of Super Investment Research, Mano Mohankumar, says that the strong FY25 performance to date has largely been powered by international listed shares.

“It also helped that all asset classes have delivered positive returns over the period with the exception of Australian REITs, to which super funds have very little exposure.

“The FY26 experience is another timely reminder of the importance of maintaining a long-term perspective and not getting distracted by short-term market noise. In late March, a return in the vicinity of 9% for growth funds would have appeared unlikely following the significant share market pullback, sparked by the US-Iran conflict and concerns around interest rates amid rising inflation.

“However, since then we’ve seen international share markets rebound strongly, albeit with some volatility, supported by robust corporate earnings, optimism around easing tensions in the Middle East and continued enthusiasm for AI investment.

“A final return close to 9% would mark four consecutive years of strong performance, following returns of 9.2% in FY23, 9.1% in FY24 and 10.4% in FY25. It would also represent the 15th positive year out of the last 17. Most importantly, super funds continue to meet their long-term return and risk objectives,” he said.

For further context, Chart 1 plots the year-by-year performance of the median growth fund over the previous 33 full financial years since the introduction of compulsory super in July 1992, as well as the 2026 financial year-to-date return.

Since the introduction of compulsory super, the median growth fund has returned 8% p.a. The annual CPI increase over the same period was 2.7%, giving a real return of 5.3% p.a. – well above the typical 3.5% target. Even looking at the past 20 years, which includes three major share market downturns – the GFC in 2007-2009, COVID-19 in 2020, and the high inflation and rising interest rates in 2022 – super funds have returned 6.8% p.a., which is still comfortably ahead of the typical objective.

“On the risk side, there have only been five negative years over the entire period, which translates to close to one year in every seven. Again, funds have done better than their typical long-term risk objective which is one negative return in every five years, on average,” said Mohankumar.

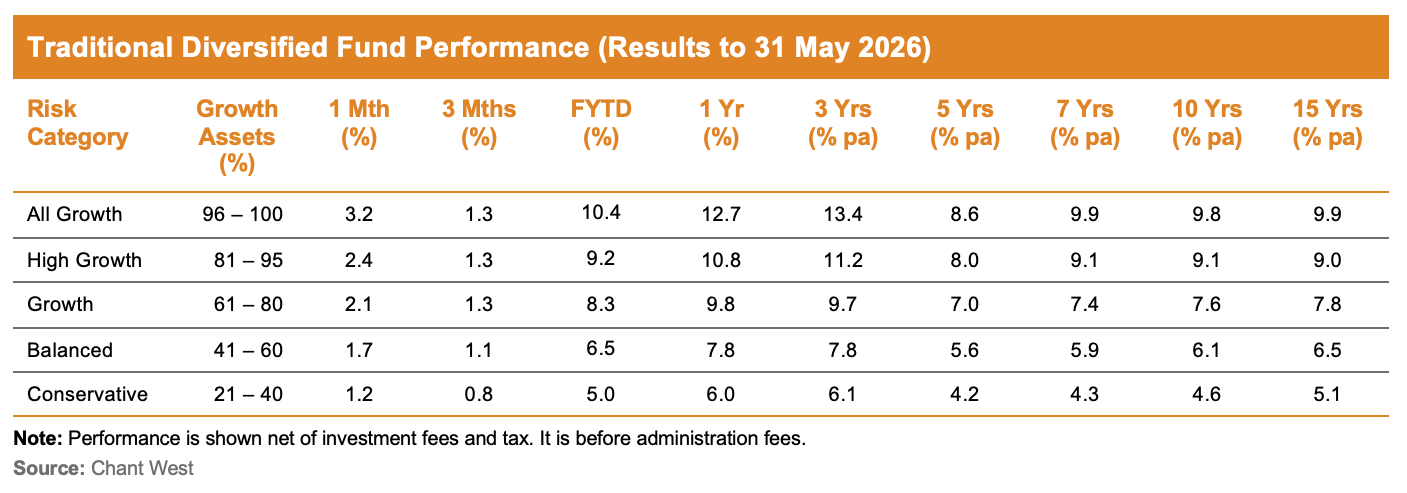

The table below compares the median performance to the end of May 2026 for each of the traditional diversified risk categories in Chant West’s Super Fund Performance Survey, ranging from All Growth to Conservative. It doesn’t include any estimated performance for June to date. All risk categories have generally met their typical long-term return objectives, which generally range from CPI + 1.5% for Conservative funds to CPI + 4.25% for All Growth.

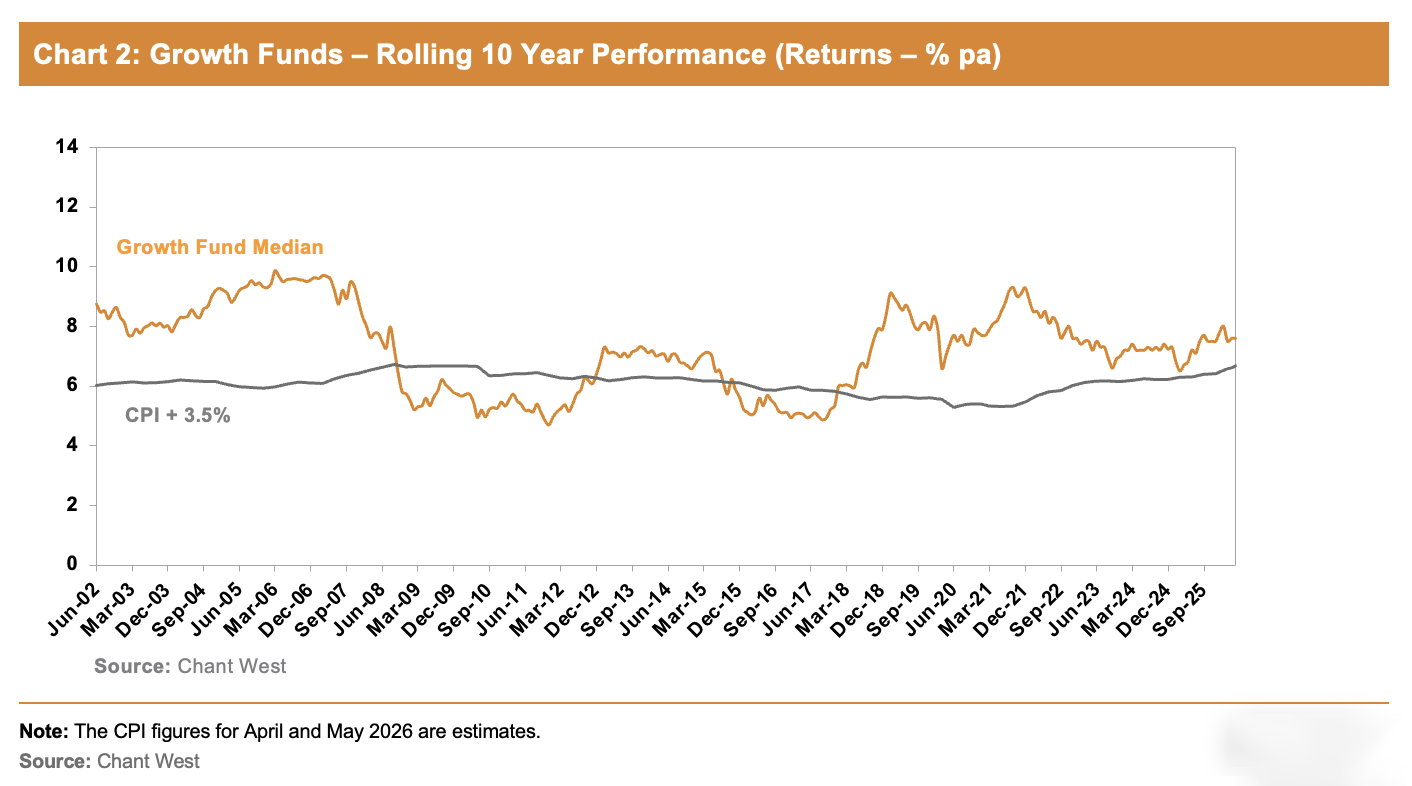

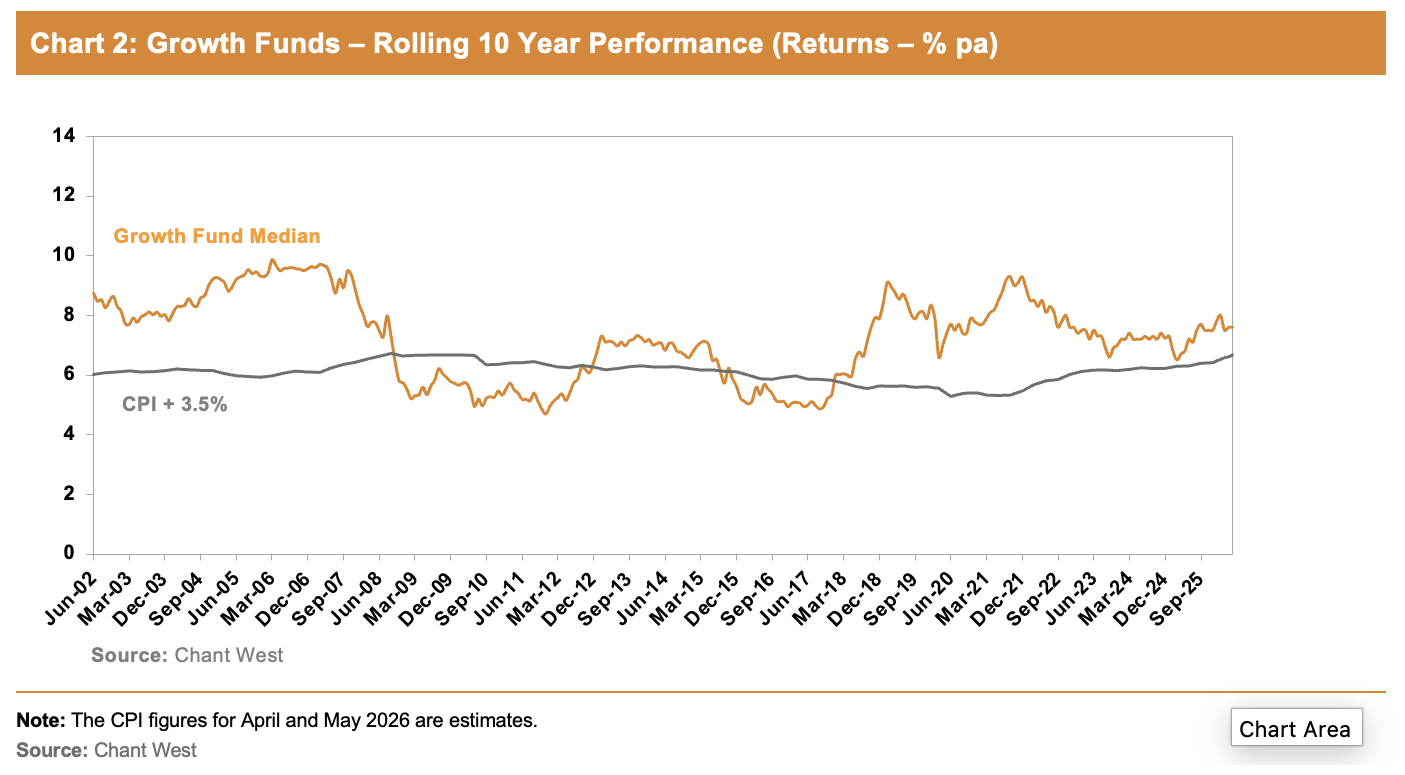

Chart 2 below shows that for most of the time, the median growth fund has exceeded its return objective over rolling 10-year periods, which is a commonly used timeframe consistent with the long-term focus of super. The exceptions are two periods between mid-2008 and late-2017, when it fell behind. This is because of the devastating impact of the 16-month GFC period (end-October 2007 to end-February 2009) during which growth funds lost about 26% on average.