This article provides advisers with a comprehensive guide to global small and medium-sized companies, covering key facts, risks and how an allocation can add value to client portfolios.

Advisers seeking long-term growth for clients often look beyond the blue-chip large cap stocks to the more dynamic small and mid-cap (SMID) sector. While many portfolios include Australian SMIDs, you could be missing the forest for the trees.

The global SMID universe offers the same diversification and return-boosting potential, but its opportunity set is exponentially larger. However, global SMIDs remain a significantly under-allocated asset class.

Through careful stock selection and active management, an exposure to global SMIDs can substantially boost portfolio growth. Their potential is fuelled by rapid innovation, revenue growth and the ability to gain market share. Although the focus of the past two years has been on large-cap titans, notably the ‘mag 7’, it’s important to remember that today’s giants all started as disruptive small or mid-cap companies. The next Apple, Nvidia or Google is almost certainly a SMID today. And importantly, each of these mega caps is circled by a myriad of SMIDs providing integral products and services.

SMID characteristics

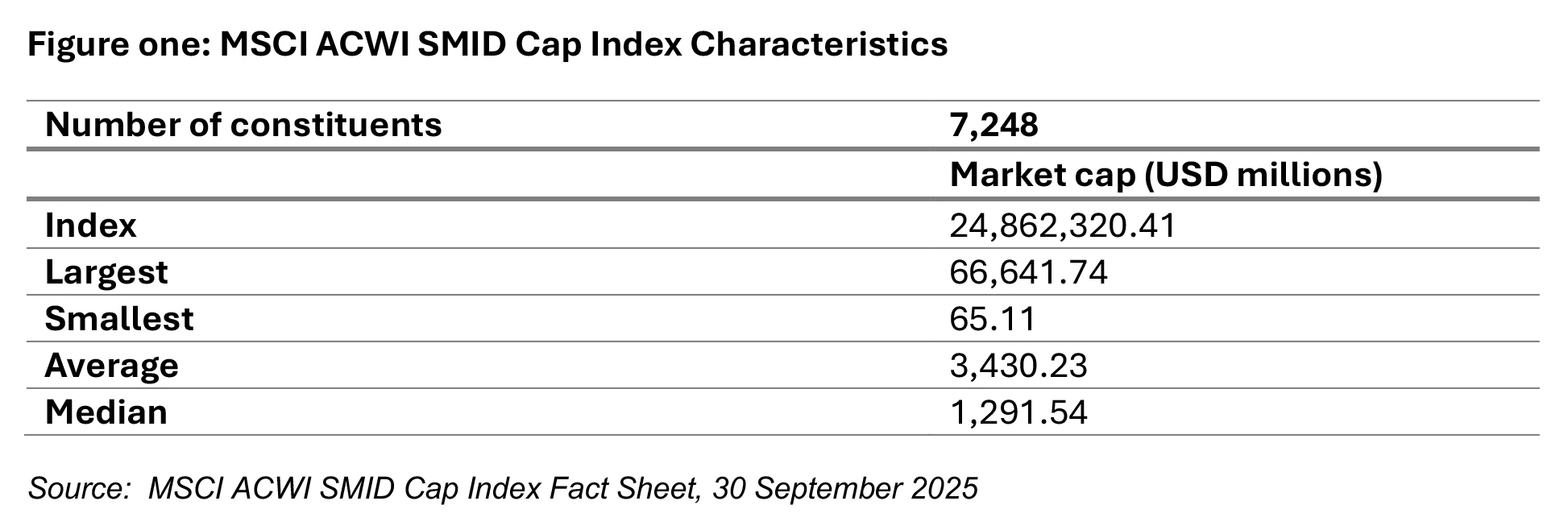

Using the MSCI ACWI SMID Cap Index to illustrate the investment potential of the SMID sector, there are 7,248 constituents across small and mid-cap companies across 23 developed markets and 24 emerging markets countries. The index covers approximately 28% of the free float-adjusted market capitalisation in each country[1].

As illustrated in figure one, the average market cap of companies in the MSCI ACWI SMID Cap Index universe is a little over US$3.4 billion.

It is important for investors to understand that small and mid-cap stocks will generally have different characteristics relative to their large cap peers, as outlined in figure two.

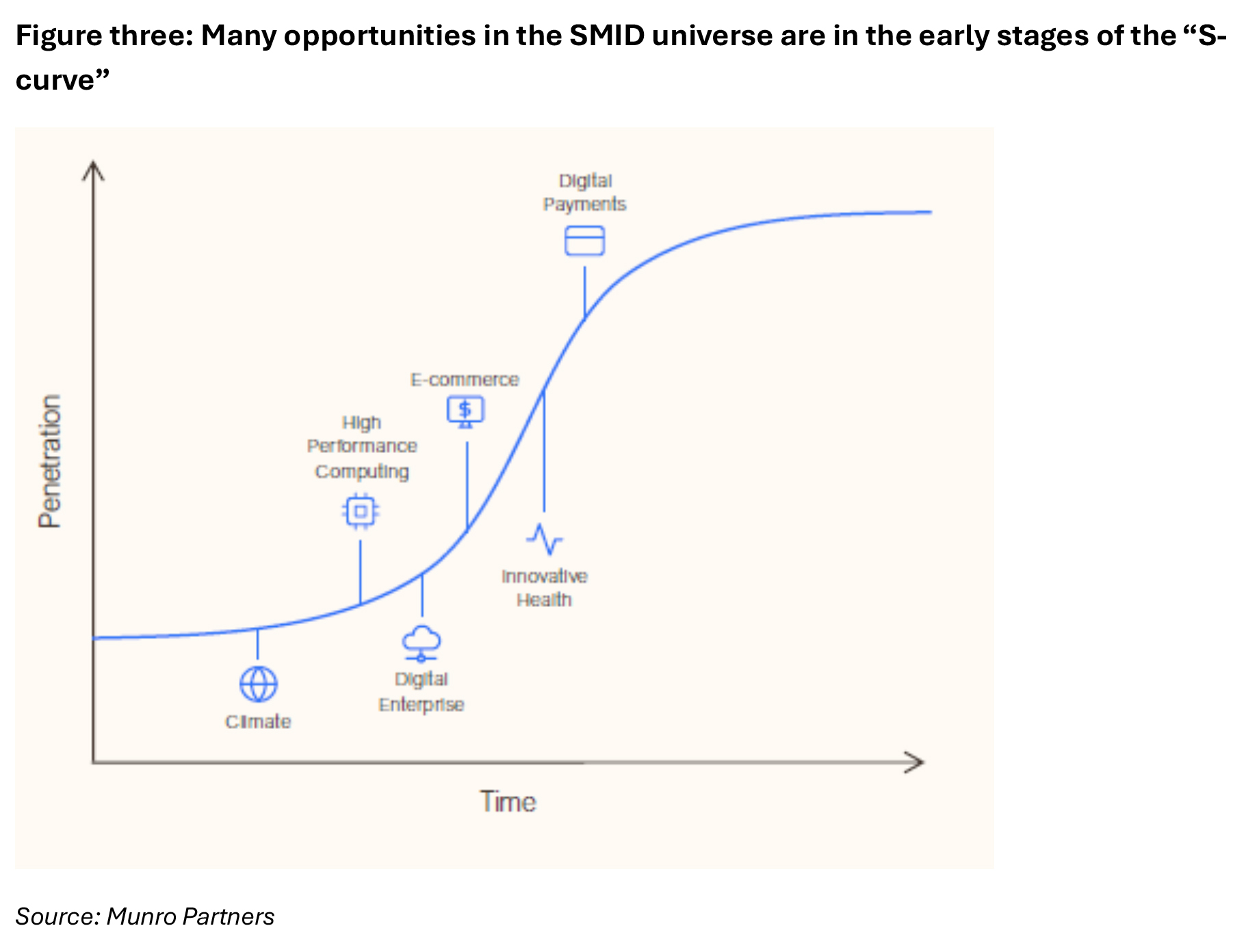

The SMID universe is full of early-stage opportunities, but the key to unlocking wealth isn’t just growth – it’s structural change.

While only a few of today’s SMIDs will become tomorrow’s leaders, the investment manager’s goal is to find them at the base of that curve, the “S-curve”, not at the peak (see figure three).

Success means identifying the next major structural tailwinds – trends such as AI and high-performance computing, as well as climate – and the companies set to ride them, just as the S-curve begins to steepen. SMID investing is precisely about capturing this early potential in the innovative growth stories of the future.

How can exposure to global SMID stocks benefit your clients?

There are many good reasons to invest in global SMID stocks. The reasons often cited for investing in small and mid-cap Australian companies hold for their global counterparts:

- Diversification – some growth areas, such as climate and high-performance computing have greater representation in the MSCI ACWI SMID Cap Index. Because there are so many of them, SMID companies are generally under-researched by stock analysts, which makes the potential for mispricing higher than large cap companies.

- Opportunity for growth – investing in a SMID company in its early stages of development, staying invested while it expands and grows, can potentially provide substantial returns

- SMID companies tend to be more nimble and better able to adjust to change – or indeed disrupt their larger competitors by being agents of change.

- SMID companies are often the target of merger and acquisition activity, which is generally positive for the company’s share price.

- It’s common for the company’s founder/s to remain on the management team and maintain a significant equity stake, thereby creating a strong alignment between management and shareholders.

Let’s explore each of these elements in greater detail.

Diversification

By spreading investments across different companies, industries and geographies, investors can reduce their overall risk exposure. This is especially important in today’s interconnected world, where economic events or structural change in one part of the world can have far-reaching effects in others.

Because Australian investors typically have a ‘home bias’ in their investment behaviour, diversification is important. Figure four compares the sector weightings of two indices – the MSCI ACWI SMID Cap Index and S&P/ASX200. Each of the indices has different weightings to the GICs sectors, with the largest in each highlighted.

Investors in Australian equities often have significant exposure to financials and materials; the global SMID market provides representation across a broader range of sectors, including higher exposure to industrials, consumer discretionary, such as companies in the luxury goods or travel industries and information technology, including those industries supporting AI.

An exposure to global SMID also provides diversification benefits relative to global large cap markets. The MSCI World Index has a 27.4 percent exposure to information technology stocks, four of which are in the top 10 stocks and comprise 16.7 percent of the total index[2].

While there seems no stopping the growth of technology heavyweights such as Nvidia, Apple and Microsoft (the top three stocks in the MSCI World Index), it’s a relatively safe bet that the next technology superstar will emerge from the SMID universe.

Beyond just stock and sector diversification, global SMIDs provide the benefit of responding differently to the economic cycle than their large-cap peers. Because SMID companies are typically more exposed to their domestic economies, they are often less sensitive to global macroeconomic factors such as geopolitical tensions and global economic turbulence. While this domestic focus can make them more vulnerable in a bear market, it also means they tend to outperform larger companies at the beginning of a market rebound.

Under-researched

With a universe with 7,248 constituents to choose from, research analysts cannot possibly cover each and every stock. This presents opportunities for astute investment managers to cherry pick the best opportunities and identify those companies that meet their investment criteria and are best placed to deliver value to investors.

Opportunities for growth

Large companies start as smaller businesses and grow. It’s far easier for a small or medium-sized company to double in size than a larger one; a company in its early stages has significant room for expansion, particularly those at the beginning of an S-curve.

Smaller companies may target niche markets or benefit from emerging trends that larger, more established companies aren’t as agile in capitalising upon. Additionally, global SMIDs can tap into growing consumer markets in developing economies, further fuelling their growth.

By identifying the next generation of SMIDs with durable competitive advantages, strong markets, and solid management, investors can benefit. These are the businesses likely to grow faster and eventually graduate into the large-cap segment.

Consider Nvidia, which graduated into the MSCI US Large Cap Index in 2001. Before then, it was a constituent of the MSCI US Small Cap and Mid Cap indices. Today[3], it is the largest company in the MSCI World Index, with a weighting of 8% and a market cap in excess of US$5 trillion.

Nimble

We are in an era of change and rapid disruption; a trend reflected in the S&P 500. A 2021 forecast projects the average company’s tenure on the index will shrink to 15-20 years this decade, down from 30-35 years in the late 1970s[4]. This implies that roughly half of the S&P 500’s current constituents will be replaced in the next ten years.

Such “creative destruction” is often driven by smaller, more agile companies. SMIDs can innovate and pivot their business strategies far more quickly than large incumbents, who are often slowed by bureaucracy.

This characteristic is especially beneficial during periods of economic and structural change. As this turnover reshapes the S&P 500 and MSCI World Index, it stands to benefit the smaller companies that are either perpetrating the disruption or adapting to it most effectively.

Demographic trends

SMIDs are uniquely positioned to tap into powerful structural trends and shifts in consumer behaviour. This agility allows companies in high-growth areas – such as climate, high performance computing and security – to benefit directly as these societal trends accelerate.

Access to niche markets

Global SMIDs often serve niche markets or specific segments within larger industries. Consider the rapid growth of data centres which, by nature, consume huge volumes of electricity. There are many smaller companies that enable energy efficient data centres (figure five). These specialised market segments can often provide insulation from broader economic downturns and create a loyal customer base, whether business to business or business to consumer, that values the unique products or services provided by these companies.

M&A activity

Good quality SMID companies have long been targets for merger and acquisition activity; this is sometimes the end game for a smaller company’s management team and can add value to investors.

Management engagement

Global SMID companies often have a more focused line of business and higher rates of management with significant shareholdings in the business. This results in greater alignment of interests between the owners and shareholders.

Capacity

While Australian small cap funds can reach capacity quite quickly because of the much smaller investment universe, global SMID funds have a much larger universe from which to select. Consequently, Global SMID strategies rarely face capacity issues.

Global SMIDs and the current environment

The investment case for global SMIDs in the current environment can be summarised by four key points.

The first is that the sector is cheap, with the valuation gap between SMIDs and their large-cap peers at its widest point in 20 years, a level not seen since the dot-com bubble. As illustrated in figure six, global SMIDs are significantly cheaper than their large cap counterparts.

The second, and most significant, point is earnings acceleration. While large companies typically dominate industries, periods of major structural change create openings for smaller companies to “break through.” This dynamic is currently visible in a number of large industries, with SMID earnings already accelerating in 2024 and 2025, even before potential tailwinds like interest rate cuts or a return of M&A activity.

The third argument is diversification. These structural growth themes are not concentrated in technology but are spread across uncorrelated industries and geographies, with examples in defence, semiconductors and innovative health. This provides diversification within the SMID asset class and adds a layer of diversification to a client’s total portfolio – as discussed earlier, this diversification is one of the major benefits of exposure to the asset class.

The final point is that the sector is “unloved”. In other words, this compelling combination of low valuations and accelerating, diversified growth is currently overlooked by the market, which creates a myriad of opportunities for astute investment managers.

The SMID sector has a massive dispersion in returns; the gap between winners and losers is far wider than in the large-cap world. Recent volatility proves that success here requires finding quality companies at the start of their growth curve, not just buying the entire index.

Active management is important

Market volatility of the past couple of years has underscored the importance of investing in quality companies, especially those at or near the beginning of their S-curve and poised to exploit a structural trend.

This is where active management in the SMID sector becomes critical. The SMID universe is significantly under-researched by sell-side analysts compared to large caps. This creates an “informational advantage” for active managers who conduct their own proprietary research, allowing them to be highly selective across countries, sectors and companies.

Conversely, a passive fund includes “allcomers,” irrespective of balance sheet strength, debt or earnings potential. The SMID sector is known for its high dispersion of returns – in other words, a wide gap between winners and losers. Active management is essential to filter for quality and focus on those companies best positioned to thrive in our rapidly changing world. This is why an active approach is so advantageous.

An allocation to global SMIDs offers a compelling way to enhance a portfolio’s risk-return profile. While a domestic approach offers benefits, a global strategy amplifies the opportunity, providing all the advantages of small-cap investing – diversification, innovation and high growth potential – but on a significantly larger scale. This allows investors to access a deeper, less efficient part of the market and, most importantly, align their portfolios with the powerful structural trends driving the next wave of growth.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Securities (0.5 hrs)

please log in to start this quiz

———–

References:

[1] MSCI ACWI SMID Cap Index Fact Sheet, 30 September 2025

[2] MSCI World Index Fact Sheet, 30 September 2025

[3] Data as at 30 October 2025

[4] Innosite 2021 Corporate Longevity Forecast, May 2021

The information included in this article is provided for informational purposes only and is general advice only. It does not take into account an investor’s own objectives. The information contained in this article reflects, as of the date of publication, the current opinion of Munro Partners and is subject to change without notice. Sources for the material contained in this article are deemed reliable but cannot be guaranteed. We do not represent that this information is accurate and complete, and it should not be relied upon as such. Any opinions expressed in this material reflect our judgment at this date, are subject to change and should not be relied upon as the basis of your investment decisions. All reasonable care has been taken in producing the information set out in this article however subsequent changes in circumstances may occur at any time and may impact on the accuracy of the information. Neither Munro Partners, GSFM Pty Ltd, their related bodies nor associates gives any warranty nor makes any representation nor accepts responsibility for the accuracy or completeness of the information contained in this article.

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Securities (0.5 hrs)

please log in to start this quiz