Understanding of the benefits of allocating a portion of client portfolios to actively managed Australian mid-cap equities.

When it comes to Australian equities, attention and capital tend to concentrate at the extremes. Stocks within the S&P/ASX 20 dominate portfolios, by virtue of the sheer size of their market capitalisations. Australia’s top twenty companies form the core of many investors’ Australian equity exposure – whether as individual shareholdings, within their super fund or as part of a managed fund or ETF.

Many Australian equity fund managers benchmark their performance against Australia’s leading share market index, the S&P/ASX 200. Because it is a capitalisation weighted index, it means these managers will naturally have a significant exposure to its largest stocks. For some investors, this end of the market is prized for its liquidity and scale. At the other end of the market, the S&P/ASX Small Ordinaries captures the imagination of growth-focused investors who chase opportunity and the next ‘tenbagger[1]’.

This traditional focus means that the middle ground – the mid-cap sector – is often overlooked and structurally underrepresented in broader Australian equity portfolios. However, for investors seeking a superior balance of growth, stability and diversification, the mid-cap sector could be described as the market’s ‘sweet spot’.

The S&P/ASX MidCap 50 Index is a mid-cap index that contains companies ranked 51 to 100 largest by market capitalisation in the Australian listed environment. While market caps fluctuate, the mid cap segment generally captures businesses valued between, approximately, $2 billion and $10 billion. No longer promising start-ups, these are companies that are established, profitable entities that are often industry leaders that still have considerable scope to grow market share. It’s a part of the market that offers a unique blend of corporate maturity and growth potential. It’s also a sector that is well positioned to deliver a superior profile of long-term, risk-adjusted returns compared to its smaller and larger peers.

The mid-cap advantage – diversification, earnings growth and performance

There are three broad arguments for mid-cap investing:

- Diversification across sectors and avoiding the concentration of financials and resource stocks that dominate the S&P/ASX 20

- Accessing earnings power capable of driving enhanced total returns to investors

- A wider dispersion of returns, giving active managers greater scope to add value through stock selection

Diversification

That the top 20 companies of the S&P/ASX-200 dominate that index will come as no surprise; the market cap of those 20 companies comprises more than half (58 percent) of the market cap of the entire 200 companies in the index[2]. The sectors that dominate the S&P/ASX-20 index also dominate the broader index (figure one).

Therefore, a significant risk in passively tracking the primary ASX indices is this concentration of the S&P/ASX-20 companies in the broader indices. Similarly active Australian equity managers that are ‘benchmark aware’ will also typically have portfolios skewed to those larger stocks. We will examine passive versus active management in more detail later in the article.

Conversely, the S&P/ASX Midcap 50 offers an important diversification benefit, significantly reducing a portfolio’s reliance on the cyclical pressures of:

- commodity prices arising from the dominance of materials

- domestic credit growth that comes from a significant exposure to Australia’s big four banks.

Instead, the S&P/ASX MidCap 50 (figure two) provides access to the next generation of Australian economic leaders in high-growth sectors that are underrepresented in Australia’s top 50 stocks. This is where companies focused on technology, healthcare and specialised industrials are often found. These businesses are typically driven by powerful, secular growth trends, such as the digital transformation of businesses, global demographic shifts or niche global supply chain specialisation. This sectoral breadth makes the mid-cap index a more accurate and dynamic reflection of the modern Australian economy.

Earnings growth

Mid-caps can be seen to embody the best of both worlds: they exhibit the maturity and financial discipline associated with larger companies – after all, the mean total market cap of stocks in the S&P/ASX Midcap 50 is $7,959 million[3]. At the same time, most mid-cap stocks retain a considerable runway for expansion that’s typical of smaller enterprises. They may not yet dominate their respective industries but can often achieve sustained and superior earnings per share (EPS) growth rates compared to their large-cap peers, whose market penetration may be at or close to saturation point.

Compounding EPS growth is the primary determinant of stronger total returns over extended periods, proving that the fastest-growing part of a portfolio is often the established company that is scaling (figure three).

A performance edge

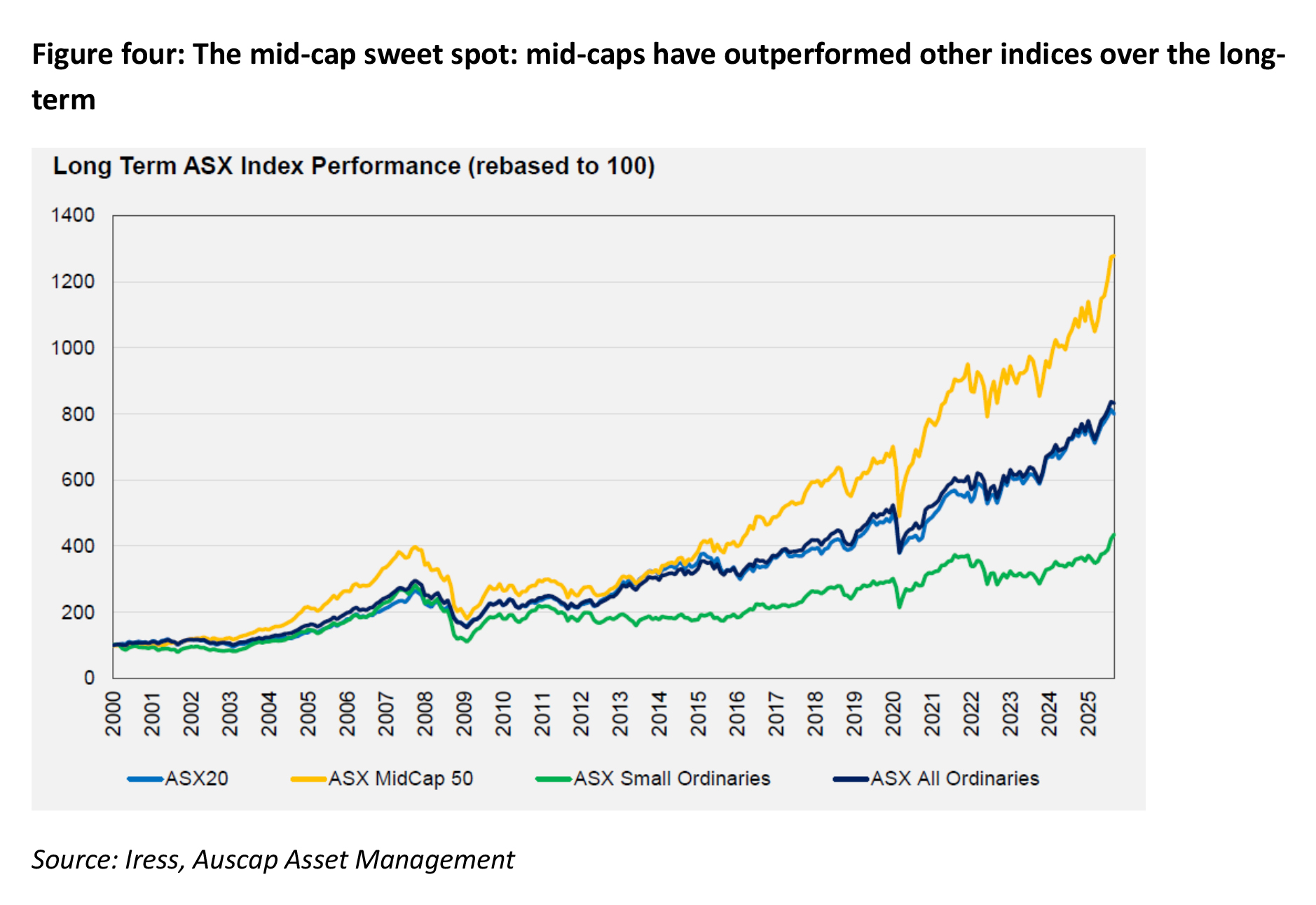

Earnings growth is one of the most important indicators of future returns. Not only do many mid-caps deliver strong earnings growth, but the sector has also demonstrated its ability to outperform both its larger and smaller peers (figure four).

This persistent outperformance is not a cyclical anomaly but a reflection of the sector’s unique position in the business life cycle, often described as the market’s ‘growth engine.’ Mid-caps represent companies that have successfully navigated the high volatility of their start-up phase, possess established business models, have proven management teams and benefit from greater access to capital than their smaller counterparts. In addition, mid-cap stocks often enjoy strong organic growth prospects that can be funded from earnings rather than having to tap investors via additional capital raisings.

A strong alignment and focus within mid-cap companies is a key qualitative advantage. Management often retain significant equity stakes in the business and have a long tenure, directly linking the success of the company to their personal wealth. This owner-operator mentality promotes prudent financial management, a focused strategic vision and a dedication to capital allocation that maximises long-term shareholder value.

Another positive attribute and contributor to performance in the mid-cap sector is merger and acquisitions (M&A) activity. These companies are profitable, scaled and often possess unique technology or market positions, making it fertile ground for M&A. These companies are typically big enough to provide a meaningful growth injection for a global major but remain small enough to be financially digestible. For investors, M&A activity provides a fundamental uplift, as corporate acquisitions often occur at a significant premium to the company’s trading price. This ‘takeout premium’ acts as an ongoing, non-cyclical catalyst that is often absent among the more saturated larger companies.

Active versus passive… and where do mid-caps fit?

Over the last decade, the debate over passive versus active management has been overwhelmingly persuasive in favour of passive strategies globally. This trend is reflected in the US, where passive equity strategies absorbed US$457 billion last year alone, while US$325 billion exited active funds. The reason for this US passive dominance is simple: the structure of the S&P 500.

Ten years ago, the S&P500 index was dominated by the technology, financials, healthcare and consumer discretionary sectors (figure five), and was dominated by fast-growing companies such as the five tech behemoths.

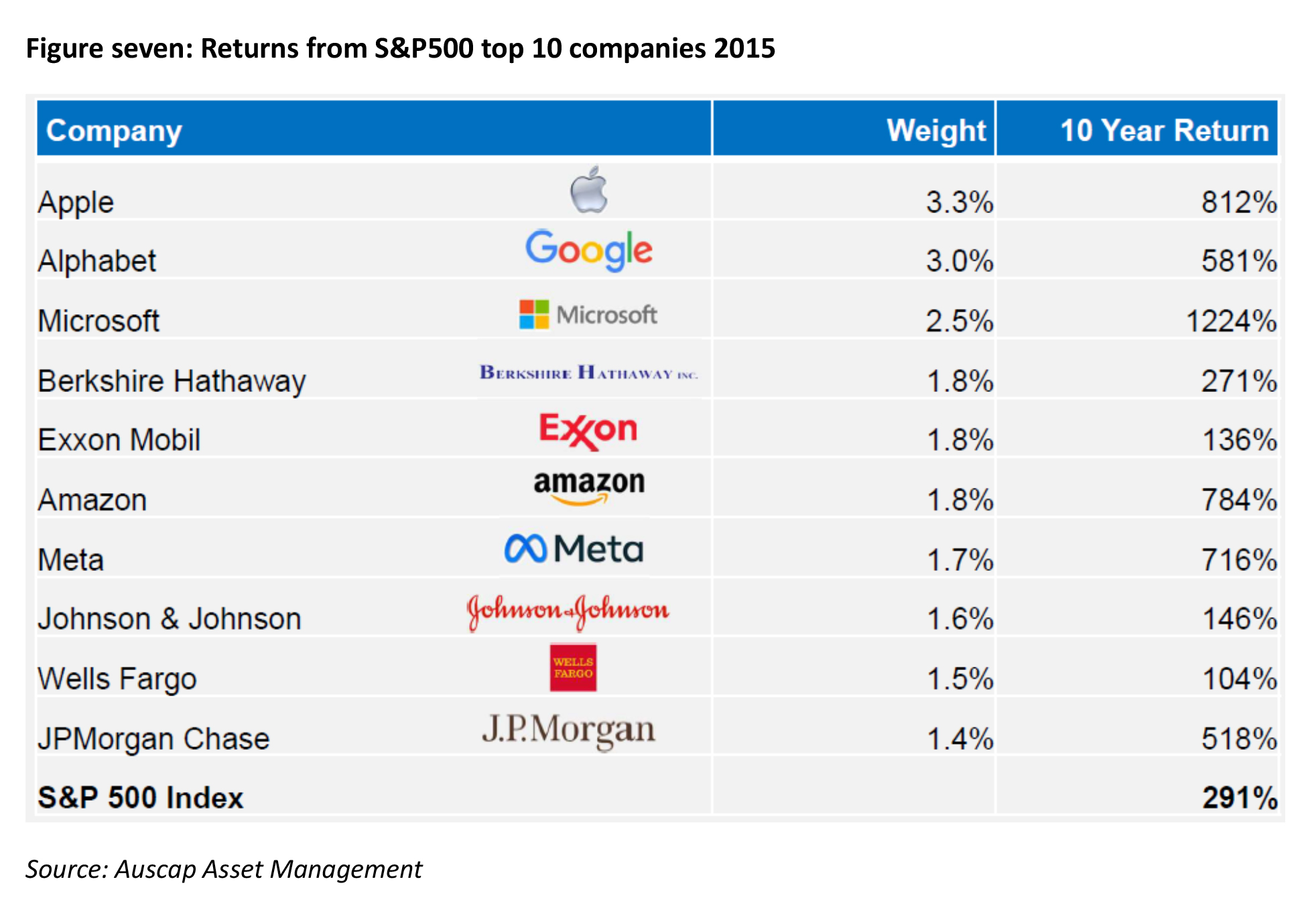

The top ten companies alone represented over one-fifth of the index (figure six) and would go on to deliver returns multiple times that of the broader market, led by names like Microsoft, which saw returns exceeding 1,200%. The ten largest companies were responsible for over 35 percent of the total return of the index (figure seven).

Aside from the technology sector, passive investors were heavily exposed to financials; however, rather than being the traditional banks, the largest overweights were companies such as JP Morgan, Visa and MasterCard. Healthcare exposure was led by Eli Lilly and Johnson & Johnson.

This portfolio of sustained, superior earnings growth created the ideal environment for passive investing, making it nearly impossible for most active managers to outperform the index on a post-fee basis.

The Australian experience

If the best environment for passive management is a high-growth, concentrated index, the best environment for active management must be the inverse: an index full of low-growth, old-world companies facing structural and cyclical headwinds. The S&P/ASX All Ordinaries today presents a fundamental challenge to passive strategies, with over 50 percent of the index concentrated in just two sectors: financials and materials.

For active managers, this concentrated structure is an opportunity. The big four banks have failed to grow earnings for a decade, weighed down by rising IT, compliance and capital costs. Critically, they now face fierce competition from agile players like Macquarie, which was recently responsible for 39 percent of the growth in total mortgage balances across all banks in a single month, a rate six to seven times its current market share[4]. Starting from historically high valuation multiples, the outlook for the banks remains challenging.

Similarly, the major iron ore miners face a peak demand scenario. Chinese steel consumption appears to have peaked five years ago and is expected to decline for the next couple of decades. This weakening of demand coincides with the opening of what’s been described as the ‘Pilbara Killer’, a major supply increase coming from the Simandou iron ore mines in Guinea. This demand/supply imbalance is a negative for future earnings.

For those investors passively exposed to the S&P/ASX 20 or 200 index, they will be heavily invested in these two largest components of the domestic market, both of which are facing significant earnings headwinds.

The mid-cap solution

The Australian index’s focus on low-growth, mature companies creates the necessity for active stock selection. While many investors look to the Small Ordinaries, that segment is often fraught with high-risk, cash-burning companies and is overweight speculative mining companies.

The true opportunity lies in the mid-cap sector, which has delivered superior long-term returns (figure four) when compared to the S&P/ASX 20, the S&P/ASX All Ordinaries, and the S&P/ASX Small Ordinaries. As described earlier in this article, this outperformance is driven by superior long-term EPS growth, the key determinant of total returns over extended periods.

Because of Australia’s heavily concentrated, low-growth index structure, it is difficult for passive strategies to capture market growth. Consequently, active managers – particularly those focused on the high-quality mid-cap segment – are best positioned to outperform.

Mid-caps and active management

While the long-term growth story is compelling, the sector is not a passive haven. Mid-caps inhabit a transitional zone in the market that necessitates an active investment approach and thoughtful stock selection. This is because of three areas of elevated risk and complexity.

1. Increased volatility

Mid-cap stocks are generally less established and less liquid than the large caps that inhabit the S&P/ASX 50 index. This can result in increased volatility, particularly during periods of economic uncertainty or a ‘risk-off’ environment. When global sentiment turns negative – maybe due to the interest rate cycle or geopolitical events – mid-cap stocks may experience more amplified price corrections than their large cap peers.

2. The analyst coverage gap

Mid-cap stocks are not as well covered as their large cap counterparts. They receive significantly less comprehensive coverage from investment banks and sell-side research analysts and so, because of this reduced coverage, the mid-cap sector is inherently less efficient and often less accurately valued by the market. This complexity is a risk for passive investors who rely solely on index weights, but it creates a powerful opportunity for active management. Those managers who possess the resources and expertise to conduct deep, proprietary fundamental research and uncover mispriced assets with high conviction have a decided edge over simply ‘buying the index’.

3. Sensitivity to financial health

While the growth engine of a mid-cap company can often rely on earnings to scale operations, many companies may also rely on external funding. Consequently, mid-caps can be sensitive to changes in financing costs and balance sheet strength. In a rising interest rate environment or during an economic downturn, mid-caps with high debt loads or weak cash flows may be more vulnerable than their large-cap peers. A rigorous focus on balance sheet quality and free cash flow generation is essential when building a mid-cap portfolio.

The combined effect of these factors makes an active management approach essential for mid-cap equities. The amplified price movements and higher transaction costs inherent in mid-caps demand sensible risk management that a passive strategy can’t provide. Crucially, the less comprehensive sell-side research creates a fertile ground for mispricing, allowing active managers with the resources to conduct deep, proprietary fundamental research to uncover value and high-conviction opportunities missed by the broader market.

The investment case for Australian mid-cap equities is clear and compelling. They represent the market’s ‘sweet spot’, offering a proven, long-term premium in total returns driven by a superior EPS growth profile. They provide a crucial diversification benefit, moving portfolios away from the heavy concentration of banks and miners into the dynamic, new-economy sectors set to lead Australia’s future.

However, the analysis of risk is equally clear: this is not a segment for passive, set-and-forget investing. The inherent inefficiencies caused by the analyst coverage gap, combined with the genuine risks of volatility and balance sheet sensitivity, create a market where the dispersion between winners and losers is vast.

It is precisely this environment – one of high potential and high complexity – where skilled, active management provides its greatest value. An approach that focuses on the market leaders in each sector, companies with a long runway of growth and opportunities to grow earnings at attractive rates.

Such an approach allows your clients to harness the powerful growth of Australia’s future leaders, while actively avoiding the vulnerable companies that may falter on their journey. This is the best way for clients to benefit from the benefits of the mid-cap sweet spot.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Securities (0.5 hrs)

please log in to start this quiz

———

Notes:

[1] A tenbagger, a term introduced by legendary investor Peter Lynch, is an investment that appreciates ten times its purchase price

[2] S&P/ASX Index Fact Sheets at 31 October 2025

[3] S&P/ASX Midcap 50 Fact Sheet, 31 October 2025

[4] AFR, Macquarie is winning 40pc of all new home loan business, 4 September 2025

The information included in this article is provided for informational purposes only and is general advice only. It does not take into account an investor’s own objectives. The information contained in this article reflects, as of the date of publication, the current opinion of Auscap Asset Management Ltd ABN 11 158 929 143, AFSL 428014 (Auscap) and is subject to change without notice. Sources for the material contained in this article are deemed reliable but cannot be guaranteed. We do not represent that this information is accurate and complete, and it should not be relied upon as such. Any opinions expressed in this material reflect our judgment at this date, are subject to change and should not be relied upon as the basis of your investment decisions. All reasonable care has been taken in producing the information set out in this article however subsequent changes in circumstances may occur at any time and may impact on the accuracy of the information. Neither Auscap, GSFM Pty Ltd, their related bodies nor associates give any warranty nor makes any representation nor accepts responsibility for the accuracy or completeness of the information contained in this article. Auscap is the responsible entity of the Auscap High Conviction Australian Equities Fund ARSN 615 542 213 and the Auscap Ex-20 Australian Equities Fund ARSN 671 901 821(together, the ‘Funds’). Before deciding whether to acquire, or to continue to hold, units in a Fund, a prospective or existing investor should fully review the information, the disclosures and the disclaimers contained in all relevant Fund documents, including in particular the relevant Fund’s Product Disclosure Statement (PDS) and any update to that document, and consider obtaining investment, legal, tax and accounting advice appropriate to their circumstances. Copies of the PDSs for the Funds are available at www.auscapam.com or by calling Auscap on +61 2 8378 0800. Copies of the Target Market Determinations for the Funds, prepared by Auscap in connection with the Design and Distribution Obligations, are available on request or at www.auscapam.com.

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Securities (0.5 hrs)

please log in to start this quiz

———