The perceived value of financial advice differs across generations.

Introduction

“Clients don’t all value advice the same way. Expectations differ across generations”.

(Value of an Adviser, 2025, Russell Investments).

Understanding and articulating the value of financial advice remains a perennial challenge for the advice profession. The concept of value underpins the willingness of clients to engage with advice, their preparedness to be open and forthcoming (which can enable advice to be more effective), and their willingness to pay multi thousand-dollar fees for that advice.

Responding to this challenge, several foundational research projects have sought to identify and quantify the value of financial advice. Of these studies, both Russell’s ‘Value of an Adviser[1]’ and Vanguard’s ‘Adviser Alpha[2]’ research have consistently found that a financial adviser can improve a clients’ returns by 1.5 to 3.0 per cent or more per annum. Across both studies, a high proportion of this ‘alpha’ was attributed to coaching and mentoring clients, helping them avoid the poor decision making associated with behavioural biases.

But as useful as these value formulas and headline numbers can be – and certainly they can help advisers feel more confident in their value as professionals – they tell only part of the story. Value is not static, nor is it the same across different generations. The aspects of advice that are important to a Baby Boomer are not valued the same way by Millennials. And with a $5 trillion generational wealth transfer already underway, understanding these differences – and adapting one’s advice proposition accordingly – is now an existential imperative.

According to research[3], around four in ten Australian financial advisers believe the generational wealth transfer is a threat to their business, with a quarter saying they have already lost significant assets through generational attrition. That same study found almost half (45 per cent) of advisers to be concerned they won’t retain the assets from clients’ heirs, reporting retention of assets 71 per cent of the time when a spouse inherits, compared to only 38 per cent when children inherit.

In the final article of our three-part series on the value of advice, we therefore turn our attention to the ways different client generations experience and perceive the value of financial advice.

Drawing extensively on the 2025 Value of an Adviser Report, published by Russell Investments, and supplemented by other respected sources, we will set out to explore the different aspirations, money behaviours, and engagement preferences that characterise the current and future generations of advice clients. In doing so we aim to equip advisers with the means to better understand, serve, and form enduring relationships across generations, helping futureproof their businesses.

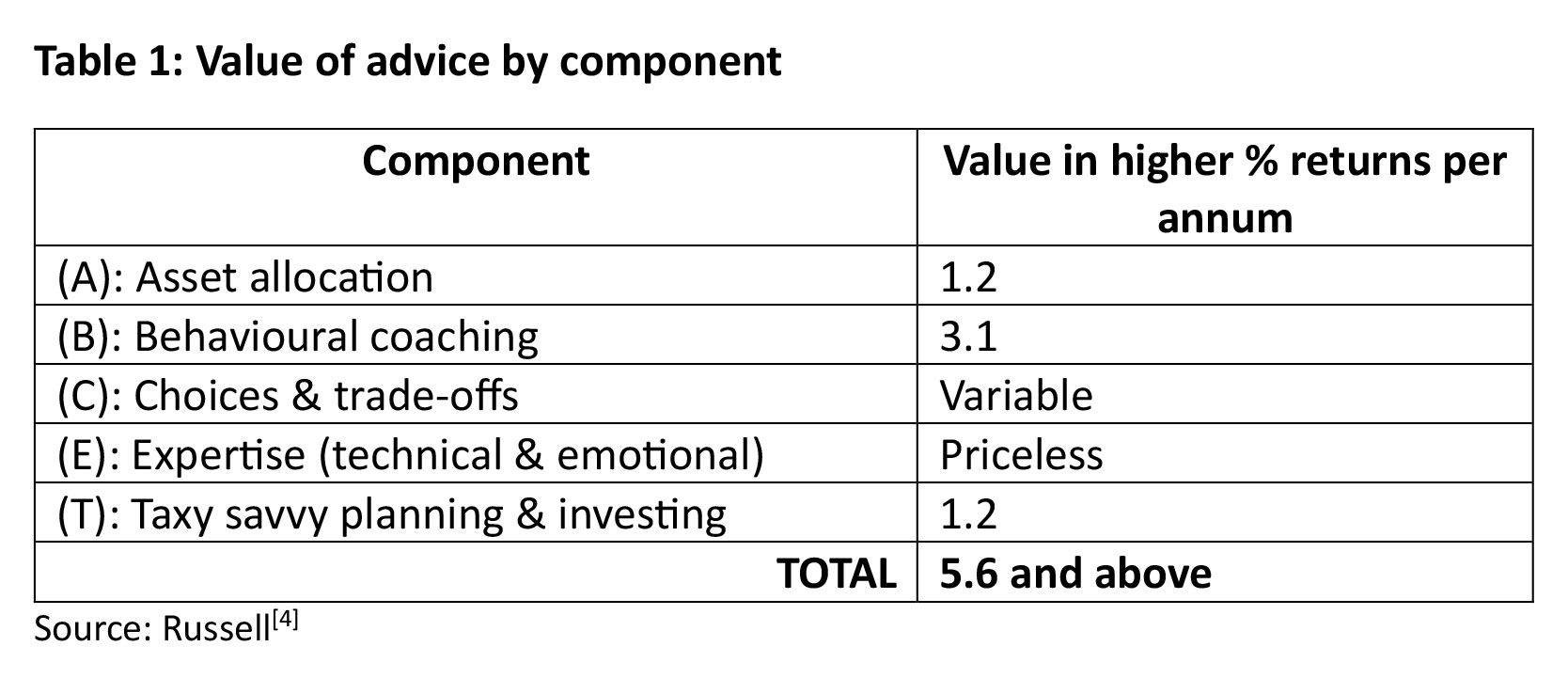

A formula for advice value

Over more than a decade, Russell’s Value of an Adviser (VoA) research study has tracked and quantified the value of financial advice around the world. Underpinning their methodology has been their VoA formula, which breaks advice value down into several components and attributes a potential value to each of those components.

Those components, along with their 2025 measured values, are shown in the table below.

But the numbers only tell part of the story

As explained in an earlier article in this series, a problem constantly faced by advisers is that much of their work is behind the scenes and invisible. This can manifest as a lack of client understanding and appreciation of what value the adviser is adding, which can in turn make conversations about financial advice fees challenging. In this context, being able to quantify the value added each year is clearly helpful. But focusing on value in purely quantitative terms ignores the fact that – from a client’s perspective – the real benefits of advice are emotional.

In Russell’s 2025 survey, 89 per cent of advised clients said feeling more confident and knowledgeable about their finances was the #1 most important benefit of advice, while 86 per cent rated feeling more in control of their finances as a top benefit. 85 per cent of clients said feeling supported in financial decision making was also important.

Are adviser misreading their clients?

Russell’s research also highlights an important gap between how advisers often frame their value and how clients actually experience it. While advisers may instinctively emphasise investment skill, portfolio construction and technical rigour, Russell’s findings consistently point to non-technical outcomes as the primary drivers of perceived value across life stages. For example, while 70 per cent of advisers strongly agree that avoiding costly mistakes is the primary financial benefit of advice, only 28 per cent of clients share that view. Similarly, the importance of feeling in control was underappreciated by advisers, with only 48% rating it highly (compared to 86% of clients).

These findings suggest that the emotional outcomes of advice are often delivered but under-articulated. While clients report benefits such as confidence, reduced anxiety and improved decision-making, it seems advisers do not always explicitly link these outcomes to the advice process. Russell’s findings suggest that value is more readily recognised when advisers help clients connect advice to these lived experiences, rather than assuming the benefits are self-evident.

Advice and quality of life

The FAAA’s 2024 Value of Advice Consumer Research[5] reinforces many of Russell’s findings. Across all generations, advised Australians reported higher quality of life, greater financial confidence and lower financial stress than those without advice. More than nine in ten advised clients reported reduced financial worries and stress, while around half reported positive impacts on their mental health and family life. These are real, powerful outcomes that sit well beyond portfolio performance alone.

Importantly, these emotional benefits are not incidental; they are central to how clients experience advice and how they judge the value of a service that can otherwise be seen as intangible. Recognising where clients see value (and tailoring one’s approach accordingly) can help advisers delink their value from purely financial outcomes (such as returns) and make their client relationships deeper and more impervious to shocks.

Equally crucially, while these emotional benefits are widely experienced, the way they are prioritised, articulated and valued varies significantly across life stages and generations, as we will now explore.

Generational differences in advice value

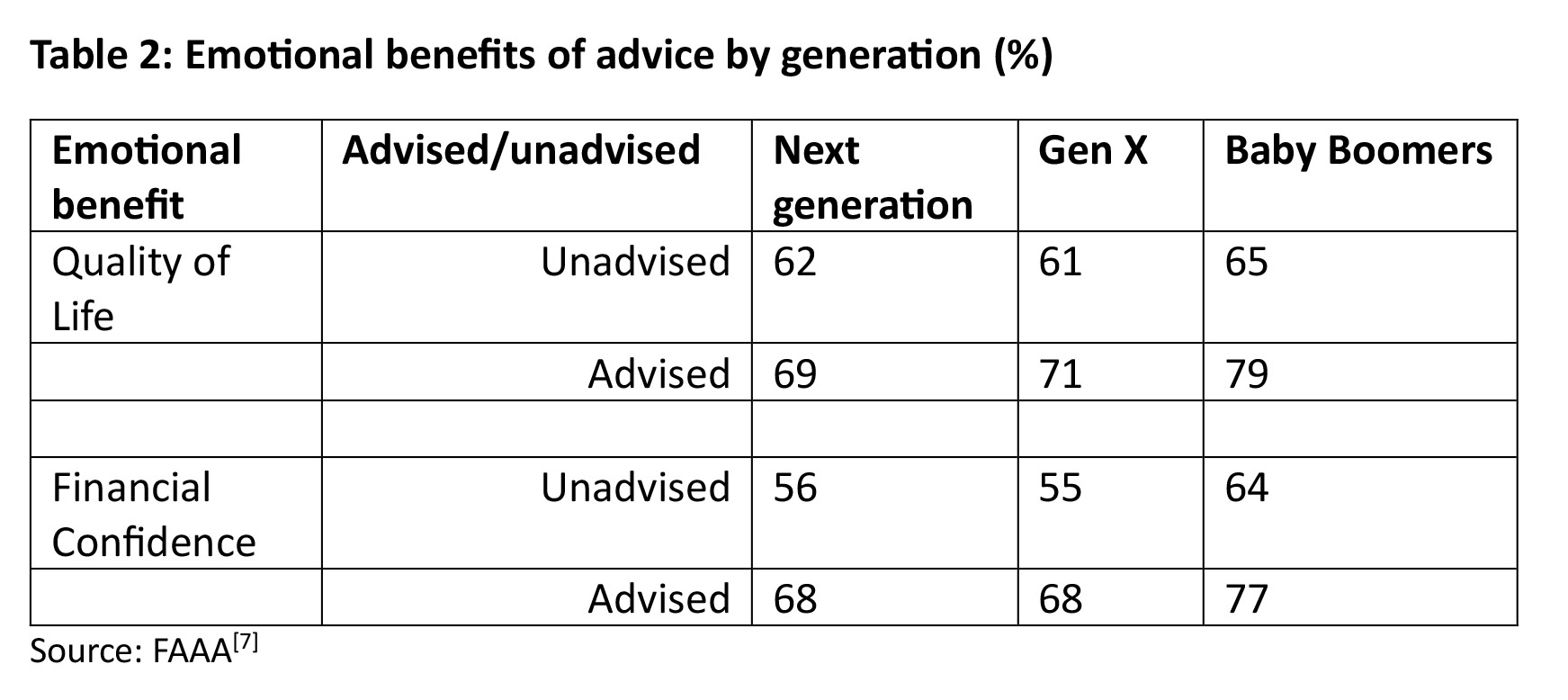

FAAA’s 2024 research demonstrates that the perceived value of advice is not uniform across generations. Its findings show that Baby Boomers are most likely to associate advice with reduced financial stress and retirement confidence, Generation X with decision support and managing competing priorities, and next generation clients (Gen Y and Gen Z) with improved understanding and confidence to act[6]. Emotional uplift across dimensions such as quality of life, financial confidence and financial satisfaction are also experienced differently across generations. These differences highlight that while advice delivers value across all age groups, the outcomes clients value most shift meaningfully with life stage, as shown in Table 2 below.

Baby Boomers: confidence and peace of mind amid high complexity

For many Baby Boomers, the value of financial advice crystallises most clearly at the point where financial decisions feel both irreversible and deeply personal.

As clients move into retirement or the years immediately surrounding it, the focus of advice shifts away from accumulation and optimisation and towards certainty, sustainability and peace of mind.

Retirement is unquestionably the most complex life stage from an advice perspective. Navigating complex and ever-changing rules around superannuation and income streams, Centrelink, tax, and aged care can be almost impossible without expert help.

The value of that expert help can be stark, with the FAAA study finding 88 per cent of advised Australians are satisfied they have enough money to last through their retirement, compared to 62 per cent of unadvised Australians.

Questions about income adequacy, longevity risk, health costs and supporting adult children bring emotional weight as well as financial complexity. In this context, advice is less about maximising returns and more about reducing anxiety, providing clarity and enabling clients to feel confident that their financial position can support the life they want to live, consistent with the values that are important to them. It is at this stage that the emotional benefits of advice, reassurance, reduced stress and confidence in decision-making become most visible, and most highly valued.

A preference for human led engagement

A notable difference between Boomers and younger generations can be found in attitudes to engagement and communication, with Boomers exhibiting a stronger preference for face to face, human-led engagement.

Close to 3 in 5 Baby Boomers prefer human-led advice only, which only decreases to 1 in 2 among Gen Y[8]. A total of 4 in 5 Baby Boomers believe that personalised guidance can only be provided by humans as opposed to digital-only advice, compared to fewer than 3 in 5 Gen Ys and Gen Xs.

Similarly, Baby Boomers are also more likely to believe experience and judgement, tailored risk assessments, and motivation to follow through can only be provided by human financial advisers compared to the younger generations.

Block out the noise

As the generation that has more time on their hands, and more time to check their balances, Boomers can be more susceptible to short term thinking and more easily distracted by the ‘noise’ around investment markets – from the tv, from Facebook, and from their friends at the golf club. Helping them ignore this noise – by focusing on progress towards goals and the specifics of their own plan – is critical to keeping them on track.

Keeping language simple and jargon free is also important. Jargon doesn’t make you look like an expert; it simply looks like a cloak that undermines trust. Complexity increases anxiety without improving outcomes.

GenX: the sandwich generation managing competing pressures

While Baby Boomers value advice primarily for reassurance and retirement certainty, Generation X tends to value advice for a different reason: help managing competing priorities at a time of peak responsibility. Often described as the ‘sandwich generation’ – stuck in the middle between their children and parents – Gen X clients are more likely to be balancing senior career roles, dependent children, ageing parents, mortgages, school fees and long-term retirement planning simultaneously. While they may be at or near their peak earning capacity, they are also time-poor and mentally overloaded, with little margin for financial mistakes.

FAAA’s research reflects this reality. Compared to Boomers, Gen X clients place relatively greater emphasis on decision support, confidence in trade-offs and having a trusted sounding board. The value of advice for this cohort is less about long-term reassurance and more about helping them make good decisions under pressure. Advice is experienced as a way to reduce mental load, clarify priorities and navigate competing demands, rather than simply as a source of technically driven financial optimisation. This aligns closely with Russell’s identification of ‘choices and trade-offs’ as a core component of advice value.

Information overload

For many GenX clients, the challenge is not a lack of information, but an excess of it. Decisions around how much to save versus spend, whether to help children financially, how to manage debt, or how to adjust risk as careers evolve all involve trade-offs with no single correct answer. In this environment, advice adds value by providing a structure for making decisions, testing scenarios and checking goal alignment.

From an adviser perspective, this has important implications. Gen X clients often respond best when advice is framed as complexity reduction, not just recommendation delivery. Reviews that focus on scenario planning, prioritisation and decision frameworks can feel more valuable than detailed performance commentary. Flexibility and responsiveness also matter: this cohort is more likely to experience sudden changes in income, employment or family circumstances, and values advice that can adapt quickly as life evolves.

Convenience is paramount for the time poor generation

From an engagement perspective, Gen X tends to be more comfortable with digital channels than Boomers. They also tend to be more time poor, meaning the convenience and efficiency of digital engagement and communication channels is more highly prized, as is more flexibility in meeting times (such as after hours).

Unsurprisingly, research has found GenX to be enthusiastic early adopters of digital advice solutions. According to Natixis[9], the proportion of Gen Xers who signalled a preference for digital advice over in-person services had grown strongly, particularly post pandemic, and was now in the vicinity of 50%.

Next Generation advice clients: engagement, transparency and confidence

While Generation X values advice as a way to manage competing pressures, Millennials and Gen Z tend to engage with advice through a different lens again. For these ‘next generation’ clients, the value of advice is closely tied to access, understanding and trust, rather than longevity planning or complexity management alone. Many are earlier in their wealth journey, with shorter financial histories and fewer established reference points, which shapes both what they seek from advisers and how they prefer to engage.

FAAA’s research indicates that younger clients place a relatively stronger emphasis on confidence to act, understanding financial decisions and feeling informed, rather than reassurance alone. This aligns with broader industry observations that Millennials and Gen Z want to understand the ‘why’ behind recommendations, not simply receive them. Advice is valued as an educational and confidence-building process, helping clients make progress toward tangible goals such as saving, investing, managing debt and balancing lifestyle choices.

Russell’s research adds an important dimension to this picture. It shows that advice value is often experienced when advisers help clients articulate priorities and navigate trade-offs in a way that reflects personal values, including views on sustainability and responsible investing. For younger clients in particular, alignment between financial decisions and personal values can meaningfully influence trust and engagement, even where balances are still modest.

Earlier engagement improves retention

We started this article referencing the existential risk posed by the intergenerational wealth transfer, and as the beneficiaries of a sizeable portion of this transfer, it is worth reinforcing the importance of engaging next generation clients as early as possible.

Financial advisers who actively encourage clients’ children to be involved in the intergenerational wealth transfer conversation have higher retention rates, research from Australian Ethical has shown[11].

Specifically, 31 per cent of advisers who involved clients’ children in these conversations retained more than 75 per cent of their clients, more than twice the rate of those who didn’t (14 per cent).

Get there before TikTok

Engagement style is a critical differentiator for this cohort, with next generation clients expecting transparent, responsive and hybrid (human/digital) engagement. While they still value one-on-one adviser relationships, they are more comfortable interacting through digital channels, and more likely to consume financial information from a wide range of sources outside the advice relationship. This creates both an opportunity and a risk for advisers: younger clients are highly engaged with financial content[12], but that content is not always reliable, consistent or aligned with their personal circumstances. (Or legal!). The challenge for the advice profession is to get to them before TikTok does!

In this context, advisers add value by acting as curators and translators, helping younger clients make sense of conflicting information and apply it to their own situation. Clear explanations, plain-English summaries and open discussion of fees, trade-offs and risks are central to building trust. Rather than positioning advice as a once-a-year event, advisers may find greater engagement by offering more frequent, lighter-touch interactions that reinforce progress and maintain momentum.

For Millennials and Gen Z, trust is built through transparency, accessibility and shared understanding. Advisers who demonstrate responsiveness, explain decisions clearly and align advice to clients’ personal values and goals are better placed to establish enduring relationships with this cohort, and to differentiate professional advice from the noise of finfluencers and peers.

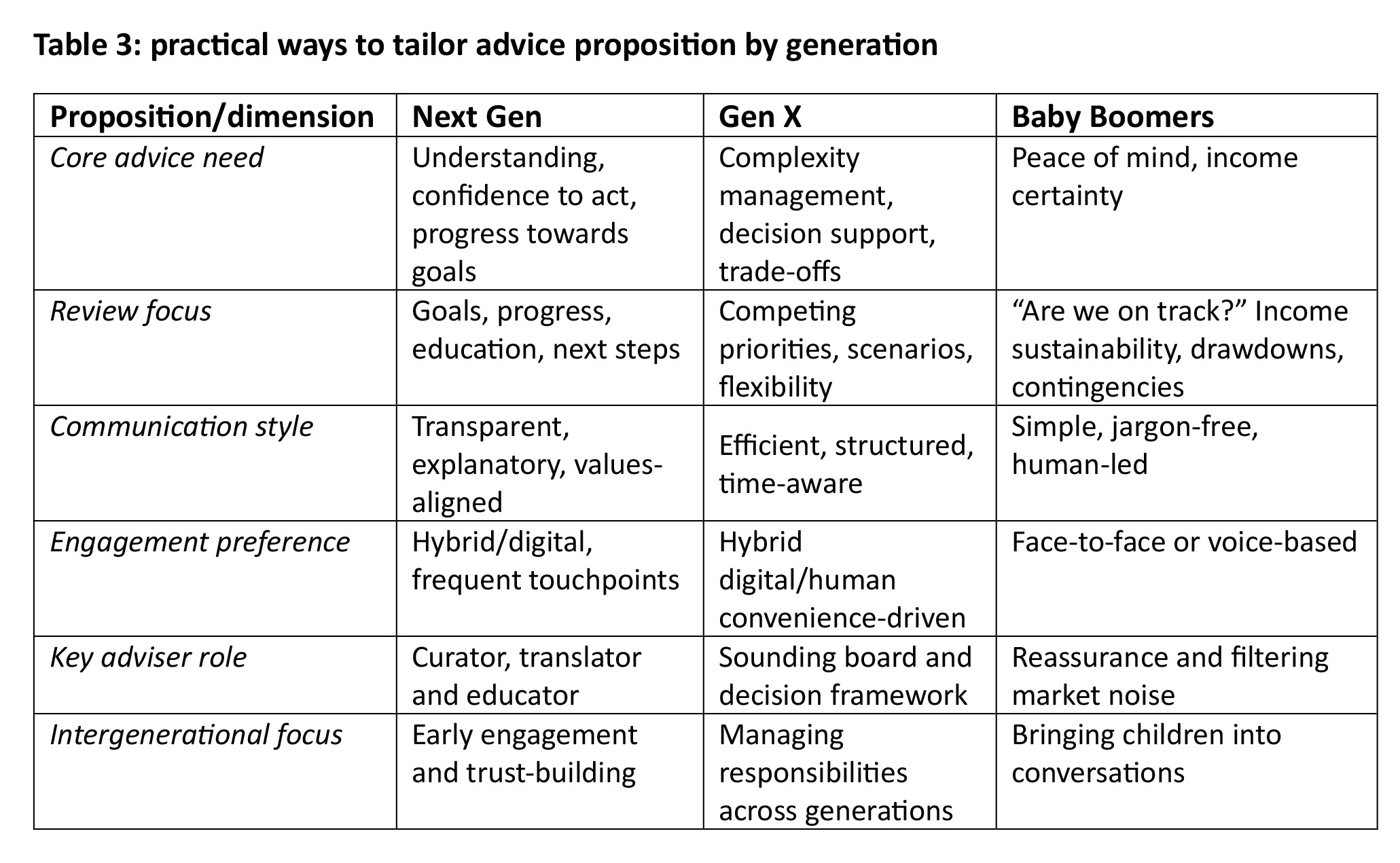

Practical implications for advisers: tailoring advice across generations

The research is clear that while financial advice delivers value across all generations, how that value is experienced varies meaningfully by life stage. Advisers who adopt a one-size-fits-all approach to reviews, communication and engagement risk under-serving clients whose priorities and pressures differ markedly.

Table 3 below distils these key differences down into practical ways to tailor the advice proposition by each generation.

Across generations, advisers should consciously adjust how reviews are structured, how information is communicated, and how value is articulated.

This includes:

- structuring reviews around outcomes and decisions, not performance in isolation

- keeping communication simple and jargon-free, particularly where complexity adds anxiety rather than insight

- providing context rather than commentary, helping clients filter external noise from media, peers and social platforms

- explicitly reinforcing progress and stability, even where no changes are required

- anchoring advice to personal values, including lifestyle, family and, for younger clients, sustainability and responsible investing

- using engagement channels that reflect clients’ time constraints and comfort with technology

- involving the next generation where appropriate to support continuity and trust across the wealth transfer.

Taken together, these adjustments do not require a fundamentally different advice process for each cohort, but they do require advisers to be deliberate about how advice is framed, delivered and reinforced for different generations.

Conclusion: futureproofing advice by understanding value

While financial advice delivers meaningful value across all life stages, that value is experienced, prioritised and articulated differently by different generations. Confidence, control, understanding and peace of mind matter to all clients, but the weight given to each outcome shifts as circumstances, responsibilities and goals evolve. Advisers who assume value is static, or who rely on a single narrative to explain their role, risk misalignment at precisely the moments when trust and relevance matter most.

The implication for the profession is not that advisers must reinvent their advice process for every cohort, but that they must become more deliberate about how advice is framed, communicated and reinforced. Russell’s Value of an Adviser research shows that value is most visible when advisers help clients make better decisions, navigate trade-offs and feel confident in their financial lives. FAAA’s findings reinforce that these emotional and quality-of-life outcomes are central to how clients judge advice.

Advisers who understand what different generations truly value, and adapt their engagement accordingly, will be better placed to build enduring, multi-generational relationships. In doing so, they not only futureproof their own businesses, but also strengthen the profession’s ability to deliver advice that is trusted, valued and relevant across generations. In the context of a generational wealth transfer already underway, this matters more than ever.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Client Care & Practice (0.5 hrs)

ASIC Knowledge Requirements: Skill Requirements (0.5 hrs)

please log in to start this quiz

Read the full series:

- CPD: The advice value unlocked by trust – 5.6% and counting – Value of Advice (Part 1)

- CPD: Transparency and communication – making the value of advice visible (Part 2)

- CPD: Futureproof – what different generations really value in advice (Part 3)

———–

References:

[1] https://russellinvestments.com/content/ri/au/en-gb/financial-professional/tools-and-education/business-solutions/value-of-adviser

[2] https://www.vanguard.ca/content/dam/intl/americas/canada/en/documents/gas/quantifying-your-value-to-clients-advisor.pdf

[3] https://www.adviservoice.com.au/2024/10/impending-great-wealth-transfer-threat-to-advisers-finds-natixis-investment-managers/#:~:text=With%20an%20estimated%20$3.5%20trillion,is%20crucial%20to%20retaining%20assets.

[4] https://russellinvestments.com/content/ri/au/en-gb/financial-professional/tools-and-education/business-solutions/value-of-adviser

[5] http://faaa.au/wp-content/uploads/2024/09/FAAA-Value-of-Advice-2024-Report.pdf

[6] Ibid.

[7] Ibid.

[8] https://faaaconnection.au/q4-2025/financial-advisers-continue-to-be-highly-valued-by-clients/

[9] https://www.moneymanagement.com.au/gen-x-drive-early-adoption-digital-advice/

[10] https://www.moneymanagement.com.au/engaging-next-generation-advice

[11] https://www.ifa.com.au/the-time-is-now-for-the-wealth-transfer-conversation-research-shows

[12] https://www.moneymanagement.com.au/engaging-next-generation-advice

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Client Care & Practice (0.5 hrs)

ASIC Knowledge Requirements: Skill Requirements (0.5 hrs)

please log in to start this quiz

Read the full series:

- CPD: The advice value unlocked by trust – 5.6% and counting – Value of Advice (Part 1)

- CPD: Transparency and communication – making the value of advice visible (Part 2)

- CPD: Futureproof – what different generations really value in advice (Part 3)