CPD: Transparency and communication – making the value of advice visible (Part 2)

Addressing adviser–client perception gaps using transparency is a key driver of value in advice.

A perennial challenge for advisers, and indeed the advice profession overall, is to articulate the value of financial advice.

From a client’s perspective, advice can seem like a complex, jargon heavy, black box, with much of the work, and value, neither visible nor understood.

Add to that the fact that many clients will have had limited exposure to other advisers – and therefore lack any basis for comparison – and it is easy to understand why many clients are unsure whether they are receiving value commensurate with the fees they are paying.

From an adviser’s perspective, inability to articulate their value can lead to a crisis of confidence. Angst over justifying fees of many thousands of dollars can become deep seated, especially in years where investment returns are negative. This in turn can see advisers massively undervalue themselves and undercharge for their services, threatening the financial viability of their businesses.

Understanding the true value of advice is therefore critical for the long-term sustainability of advice relationships and the profession overall.

Russell Investments have – for several years – conducted in-depth research into the underlying drivers of value in financial advice. Over this period, they have been able to distil value down to a simple equation:

Value of Advice = A(sset allocation) + B(ehavioural coaching) + C(hoices and trade-offs) + E(xpertise) + T(ax savvy investing).

In a previous article we explored these individual value drivers and touched on a new finding from the 2025 edition of their ‘Value of an Adviser’ report[1] – the importance of trust and transparency in unlocking these individual components of advice value.

Having covered the role of trust in our earlier article, this second article in the series will explore the foundational role of transparency and communication in helping clients understand and appreciate the value of advice – primarily by making the generally unseen drivers of value more visible.

Where the value of advice lies

The robust methodology of Russell’s ‘Value of An Adviser’ study has been honed over many years and tens of thousands of data points.

This approach has enabled them to quantify the value of advice in terms of additional annual % returns, and in 2025 the results were as follows:

![]()

One of the regular standouts in their analysis is the value of ‘behavioural coaching’, measured at 3.1% per annum in terms of additional value for 2025. While some find this figure surprisingly high, there is a wealth of supporting data that reinforces the role advisers play in saving clients from making poor investment decisions, generally in market downturns. These include Vanguard’s Adviser Alpha study[2] – which also put a value on behavioural coaching – as well as studies by Dalbar[3] and Morningstar[4] that show how poor timing, panic selling, and return chasing see most average investors underperform the market.

But whilst telling clients to sit tight and do nothing in a falling market may literally save them thousands of dollars, that ‘value’ may not always be attributed to the adviser – the client may forget the conversation by the time their annual review comes around, or they may simply not be conscious of the adviser’s influence in their decision to ‘sit tight’.

This brings to light a bigger challenge for advisers – the fact that client perceptions about where the value in advice lies may differ substantially from what we know to be true.

The client perception gap

Indeed, when advice clients were asked what aspects of advice they valued the most – there was quite a divergence, not only compared with the quantified value of advice formula (Table 1), but also with what advisers perceived to be most important to clients.

This difference was articulated by Russell in their inaugural ‘Value of an Adviser’ (VoA) Index, which ranked scores against a baseline index of 100.

According to clients, the top drivers of their satisfaction were technical and emotional expertise (E) with an index score of 118 and appropriate asset allocation (A) with 113. These significantly outpaced tax‑savvy planning (T) at 92, behavioural coaching (B) at 91 and choices and trade‑offs (C) at 88.

In terms of the emotional benefits of advice, advisers continue to rate the value of their own reassurance, clarity and behavioural coaching highly, while clients still prioritise control, understanding and personal relevance.

According to Russell’s report, 70 per cent of advisers say helping clients avoid costly mistakes is the top financial benefit of advice, but only 28 per cent of clients agree. Likewise, while 99 per cent of advisers believe reassurance is a key emotional benefit, just 78 per cent of clients share that view. Instead, 86 per cent of clients nominate ‘feeling in control of their finances’ as the greatest emotional payoff of advice, a benefit advisers tend to underestimate.

More alignment was found around the importance of advisers in supporting clients to make financial decisions. 98 per cent of advisers believe this to be the second most important emotional benefit of their advice, a view shared by 85 per cent of clients.

What advisers say versus what clients hear

The Russell report is not the first to pick up on these perceptual gaps.

One recent and highly relevant study of adviser communication skills also found clients and advisers were on different pages.

The study[5] by Money Quotient, reported by Institutional Investor, found that advisers consistently over-estimate their own communication skills. Across key areas such as explaining goals, investment trade-offs and financial values, planners rated themselves 15 to 36 percentage points higher than clients did. While 84 per cent of advisers said they “carefully consider the terms and language they use”, only 51 per cent of clients agreed.

Why these gaps matter

Having a distorted picture of what clients value can lead to misdirected efforts and a false sense of security around their satisfaction and loyalty.

When advisers believe they’re communicating clearly, but clients still feel uncertain or confused, trust slowly erodes, not because of performance, but because of perception. The ‘illusion of communication’, can leave clients feeling uninformed even when the adviser believes every message has landed.

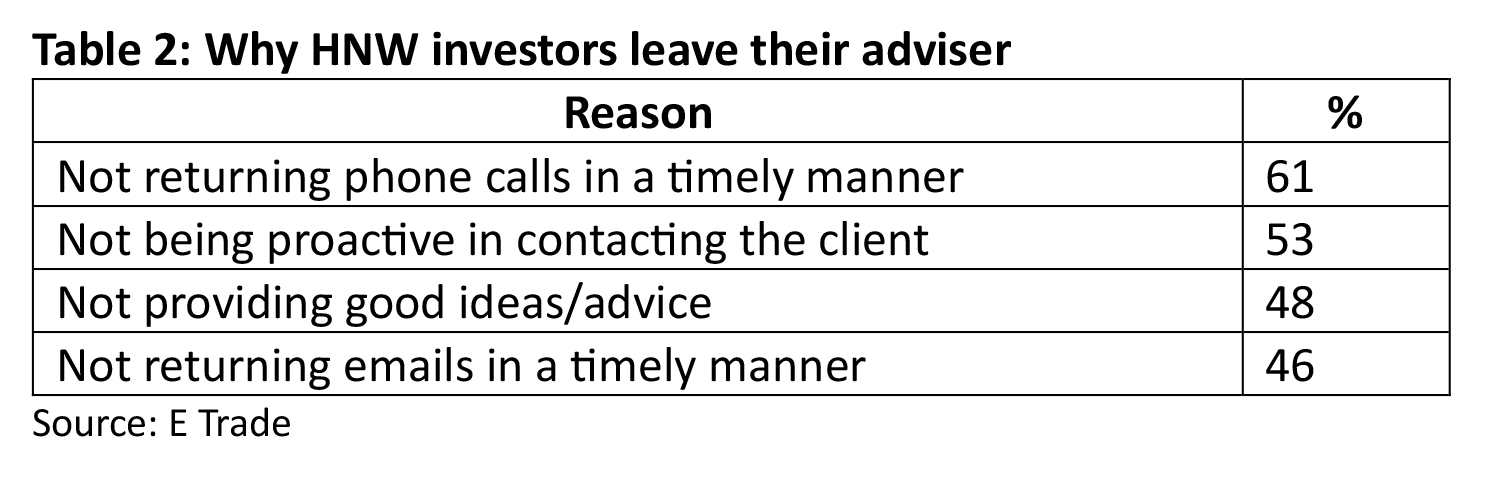

This can become an existential issue for advisers – an E Trade study[6] of HNW investors found that 3 of the top 4 reasons for them to leave their advisers were communication related:

Transparency as communication in action

Transparency as communication in action

Transparency, along with trust, was identified as critical to unlocking the value of advice. This was found to be especially true in relation to advice fees, and here again the Russell data reveals a perceptual gap.

Clients rate the importance of transparent, easy to understand fees at 8.5 out of 10 but rate advisers’ performance at 8.2. Advisers rate their own performance higher (8.7) than their clients rated it.

![]()

It seems obvious that clearly explaining fees without jargon can strengthen trust and reinforce value. Taking time to walk clients through each cost, checking for understanding before moving on, and linking fees to outcomes can build confidence in the advice process.

But there is more to transparency than just fees. Transparency is about having clients understand exactly what is happening and why. Transparency – through more effective communication – is the adviser’s chance to make the often-invisible work they do and the value they add, visible.

Communication: the right channel and frequency can accelerate trust

Russell’s 2025 report highlights the tangible link between communication methods and client engagement.

While 91 per cent of advisers still rely primarily on in-person meetings, phone calls, and emails, those who use secure client portals or video calls connect an average of five times per year, compared with an overall average of 3.6 times across the survey. That difference in frequency, enabled by technology, correlates directly with higher perceived transparency and satisfaction.

Digital platforms and client portals can also help make the process and value of advice more visible. Being able to access dashboards, reports, portfolio updates and strategy notes in real time not only helps clients feel in control, it also demonstrates transparency and accountability, which can accelerate trust.

Transparency in this context doesn’t mean constant updates or information overload, it means recognising that a substantial financial knowledge gap creates a power imbalance, one which can leave clients feeling anxious and lacking control. Transparency which helps inform and educate clients helps reduce this imbalance, as well as being an opportunity to shine a light on some of the ‘behind the scenes’ work done by advisers.

Show the thinking behind decisions

The ‘Choice and Trade-offs’ component of the VoA formula is the most underappreciated driver of value in the eyes of clients, with an index score of just 88.

There is no question advisers create significant value by helping clients navigate competing priorities, such as liquidity versus growth, risk versus opportunity, tax efficiency versus simplicity.

But this value can vanish in translation if the client doesn’t see the deliberations behind the decisions. Transparency in this context means explaining the ‘why’ not just the ‘what’ of decisions.

While this approach is theoretically embedded into compliant advice processes – RG 175 requires advisers to show a concise statement of the reasons why “the advice and recommendation were considered appropriate, including in light of the alternative options considered”[7] – it is not necessarily something that advisers draw attention to (and the extent to which clients engage with the SOA is questionable to say the least). Proactively discussing this process with clients underscores that every recommendation is the result of deliberate analysis. It demonstrates that advice is not transactional, but the product of disciplined reasoning and informed judgement.

Tax-smart transparency

With an index score of 92, the tangible financial benefit advisers deliver through tax-smart planning – the ‘T’ in the VoA formula – is also underappreciated, perhaps because tax rules are so complex and much of the work to optimise a client’s tax position is ‘quiet work’, such portfolio rebalancing to harvest losses, contribution timing, or offsetting gains in other accounts.

Proactively communicating and explaining these actions and articulating tax efficiency into dollar terms will give clients a clearer sense of the after-tax value of advice.

Beyond information – the role of empathy

Transparency is not a data-transfer exercise. Clients process information emotionally first and rationally second, meaning that over-communication without context can overwhelm. Empathy is critical.

Russell’s behavioural coaching framework underscores this: advisers add value not only by ‘what’ they say but by ‘how’ and ‘when’. Calming communication during volatility, celebrating milestones, and acknowledging client emotions are all part of behavioural transparency, showing clients that their adviser genuinely cares about them, and understands mindsets as well as markets.

Transparency without empathy is just a data dump, whereas empathetic transparency helps put clients at ease and builds trust.

Practical ways to systemise transparency

As the Money Quotient research found, there is often a divergence between what advisers believe they have said and what landed with clients. So, while some believe they are being effective at simplifying complex topics and relating strategies to personal goals, clients may be experiencing those same conversations as rushed or overly technical.

Bridging this divide requires a shift from assuming clarity to confirming it -in other words, ‘it’s about genuinely informed consent.

Simple tools, post-meeting summaries written in plain English, confirmation emails highlighting key decisions, or end-of-quarter recaps that explicitly restate agreed actions can all close the loop. In fact, any communication that is truly tailored to the client – rather than a generic one-size fits all piece – can help.

Some advisers are adapting evidence-based communication techniques such as ‘teach-backs ’to confirm client understanding. Asking clients to explain a concept back in their own words is not a test; it’s a trust check. When clients can articulate the rationale themselves, it signals that communication has truly connected.

Language is another layer. Financial services is a complex sector with its own jargon. But using this jargon to demonstrate your competence to clients, actually creates a barrier to trust, by reinforcing the information asymmetry – the knowledge gap – that exists between adviser and client. Using jargon-free language and being prepared to educate clients shows you are not using knowledge as power, or to build their dependency on you, but as a bridge, turning expertise into understanding and empowering clients.

This point was reinforced by a Morningstar study[8] of the adviser behaviours which cause the most frustration to clients – use of jargon was a top 5 annoyance.

Conclusion: making the invisible visible

Transparency and communication are not peripheral to advice, they are how advice becomes visible, credible, and valued. The more advisers illuminate the reasoning behind their recommendations, clarify the trade-offs they have made, and explain outcomes in language clients understand, the more the unseen work of advice will be recognised for what it is: professional judgement exercised in the client’s best interests.

Ultimately, trust and transparency are foundational to advice. Trust allows clients to believe in the advice process, while transparency allows them to see it. In a profession where so much of the value lies beneath the surface, these two qualities ultimately allow the light in, allowing clients to see, understand, and appreciate, the true value of advice, and their adviser.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Client Care & Practice (0.5 hrs)

ASIC Knowledge Requirements: Client Engagement (0.5 hrs)

please log in to start this quiz

Read the full series:

- CPD: The advice value unlocked by trust – 5.6% and counting – Value of Advice (Part 1)

- CPD: Transparency and communication – making the value of advice visible (Part 2)

- CPD: Futureproof – what different generations really value in advice (Part 3)

———–

References:

[1] https://russellinvestments.com/content/ri/au/en-gb/financial-professional/tools-and-education/business-solutions/value-of-adviser

[2] https://aemdam.assets.vgdynamic.info/assets/intl/australia/fas/documents/resources/Vanguard_Advisers_Alpha_RS23.pdf

[3] https://www.loricapartners.com.au/insights/how-investor-behaviour-undermines-long-term-success

[4] https://www.morningstar.com.au/personal-finance/how-to-earn-1-7-more-a-year-than-the-average-investor

[5] https://www.institutionalinvestor.com/article/2aucrzsa72lr93zd2kc1s/ria-intel/advisors-think-they-are-good-communicators-a-study-shows-clients-feel-differently

[6] https://www.fa-mag.com/userfiles/ads_2019/ETRADE_May_2019/AI_Report_Client_Retention_ver2.pdf

[7] https://download.asic.gov.au/media/pqpe0hwc/rg175-published-21-november-2024-20241219.pdf

[8] https://www.professionalplanner.com.au/2025/05/the-most-irritating-behaviours-exhibited-by-advisers/

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Client Care & Practice (0.5 hrs)

ASIC Knowledge Requirements: Client Engagement (0.5 hrs)

please log in to start this quiz

Read the full series:

- CPD: The advice value unlocked by trust – 5.6% and counting – Value of Advice (Part 1)

- CPD: Transparency and communication – making the value of advice visible (Part 2)

- CPD: Futureproof – what different generations really value in advice (Part 3)

———–

References:

[1] https://russellinvestments.com/content/ri/au/en-gb/financial-professional/tools-and-education/business-solutions/value-of-adviser

[2] https://aemdam.assets.vgdynamic.info/assets/intl/australia/fas/documents/resources/Vanguard_Advisers_Alpha_RS23.pdf

[3] https://www.loricapartners.com.au/insights/how-investor-behaviour-undermines-long-term-success

[4] https://www.morningstar.com.au/personal-finance/how-to-earn-1-7-more-a-year-than-the-average-investor

[5] https://www.institutionalinvestor.com/article/2aucrzsa72lr93zd2kc1s/ria-intel/advisors-think-they-are-good-communicators-a-study-shows-clients-feel-differently

[6] https://www.fa-mag.com/userfiles/ads_2019/ETRADE_May_2019/AI_Report_Client_Retention_ver2.pdf

[7] https://download.asic.gov.au/media/pqpe0hwc/rg175-published-21-november-2024-20241219.pdf

[8] https://www.professionalplanner.com.au/2025/05/the-most-irritating-behaviours-exhibited-by-advisers/

Have feedback on this article? Contact Us

Earn CPD Points

CPD: The spectrum of growth

CPD: The spectrum of growthCompanies that generate strong, sustainable growth are valuable sources of long term capital appreciation in a portfolio, but these businesses are rare, difficult to identify and exist on a broad [...]

CPD: Record-keeping in financial advice – the key to compliance and consumer protection

CPD: Record-keeping in financial advice – the key to compliance and consumer protectionIntroduction The financial services regulatory framework is a key pillar of financial consumer protection. Regulatory compliance is therefore not merely about avoiding penalties, but is a critical step in building [...]

CPD: Trust and ethics in financial advice

CPD: Trust and ethics in financial adviceIn 2024, trust in financial advisers reached an all-time high. This article, proudly sponsored by GSFM, explores the inseparable links between trust and ethical practice when providing financial advice. Defined [...]

CPD: Retirement Income Strategies

CPD: Retirement Income StrategiesIt has been almost 40 years since award superannuation was introduced in Australia, and 33 years since the introduction of mandatory occupational superannuation. This means the next decade will see [...]

CPD: Free cash flow works

CPD: Free cash flow worksThe difference between earnings and free cash flow is an important investment concept, one explained here by GSFM’s investment partner TD Epoch. Earnings have long played a dominant role in [...]