Since the 2010s, digital innovation has taken centre stage.

Key takeaways

- While change is normal in the global economy, today’s environment stands apart for its confluence of transformational and multi-generational shifts.

- As a result of this rare convergence, the next decade and beyond could present a richer and more diverse set of investment opportunities.

- It is therefore important to identify investment strategies that can flexibly navigate significant structural shifts while keeping true to their objectives and philosophy.

If we look back at equities over history, markets have tended to move in decadal mega cycles, where one major ‘theme’ has dominated.

This is especially evident when we examine the years since Capital Group began investing globally.[1] Tracing the evolution through the decades, we see that each era has been defined by a prevailing trend: the 1970s were characterised by energy and commodities; the 1980s and 1990s saw the rise of computing and mobile technology; the 2000s were marked by global trade and the emergence of China; and, since the 2010s, digital innovation has taken centre stage.

Being on the right side of these trends has proven extremely beneficial for investors. Over the past decade, one of the most pronounced trends has been the dominance of a select group of US-based, mega-cap technology companies. Supported by an environment of low interest rates, these companies have driven a substantial share of equity market returns, resulting in increasingly concentrated market leadership. However, that has begun to change as a new era of higher inflation and interest rates, and rising geopolitical tension, is marking the beginning of a prolonged shift, the scale of which we typically only see every 10 to 15 years.

A unique point in history?

What is particularly unique, and exciting for investors, about this current juncture is that there appears to be a confluence of transformational and multigenerational shifts occurring simultaneously. In this paper, we will discuss four key areas and examine how we are identifying the long-term investment opportunities that they present.

We expect these powerful forces to drive far broader market leadership and a much richer, more diverse set of investment opportunities over the next decade and beyond. However, this does not mean stocks that benefited from previous trends, such as large-cap US technology companies, cannot continue to produce strong returns. These companies, having shaped earlier cycles and established substantial competitive advantages, may still benefit from ongoing structural shifts. Nevertheless, they could be joined by businesses from other sectors and regions, each exposed to different structural tailwinds. In other words, this could be particularly fruitful for bottom-up, global stock pickers.

1. Artificial Intelligence

Artificial intelligence (AI) is set to be one of the most disruptive technological forces of our generation. Its potential as a “general purpose technology,” a category defined by wide-reaching applications across many sectors with the capacity to drive substantial productivity gains and foster further innovation, places it alongside transformative developments such as the steam engine, electricity and the internet.

One of the most attractive features of AI is its potentially huge total addressable market (TAM). Estimates vary considerably, but a 2025 report from UN Trade and Development (UNCTAD) projected that the global AI market will soar from US$189 billion in 2023 to US$4.8 trillion by 2033.[2] However, from our experience over prior technology cycles, it remains crucial to separate short-term hype (or noise) from longer-term opportunities. Establishing a framework to analyse the different opportunities and evaluating their current as well as future investment potential may therefore prove beneficial.

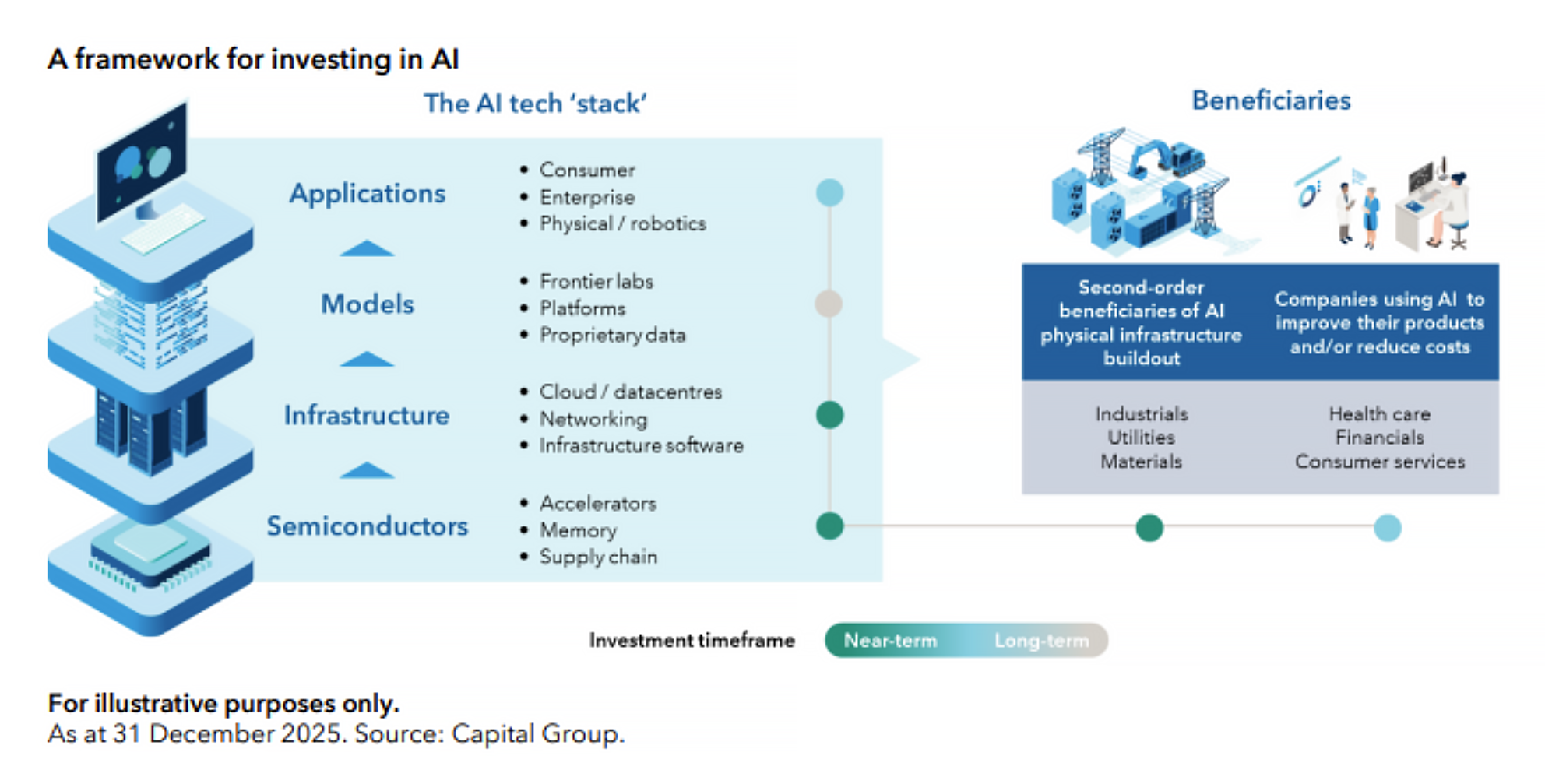

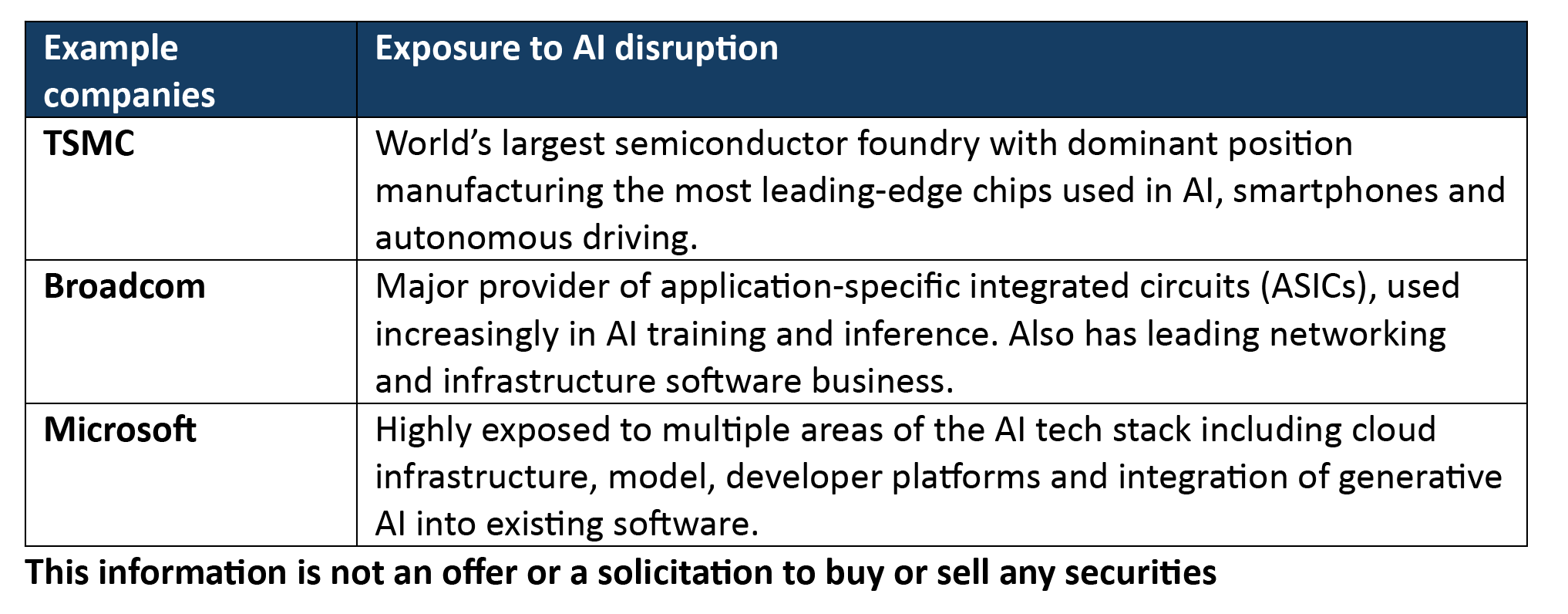

Our investment professionals are evaluating companies at the forefront of AI enablement and development by examining them through a four-layer technology stack. At present, their primary focus is on businesses operating at the foundational levels of this stack, often described as the “picks and shovels” providers of AI. This includes the global semiconductor ecosystem, which serves as the essential building blocks, alongside companies delivering the digital infrastructure, most notably, the cloud hyperscalers.

Looking further up the stack, the landscape becomes more dynamic and less predictable. The rapid evolution of large language models means it is uncertain which, and how many, will ultimately establish themselves as long-term leaders. At the top of this stack is the application layer, comprising companies that deliver AI-powered services directly to end users.

In the short term, we see compelling opportunities among established software providers as they embed AI capabilities to enhance customer experience and operational efficiency. However, over the longer term, we anticipate significant disruption within this segment. AI is likely to give rise to entirely new categories of applications as well as innovations that are difficult to fully envisage today. This is reminiscent of the paradigm shift following the launch of the first iPhone in 2007, when few could have predicted the advent of transformative platforms such as Uber or Airbnb.

Beyond the core technology sector, a wider range of companies stand to benefit from the expansion of AI. Secondary beneficiaries are emerging because of the accelerating development of datacentres. Notably, close to half of the capital expenditure allocated to datacentres is directed towards areas other than semiconductors, such as the construction of the physical facility, implementation of power infrastructure, and installation of advanced cooling systems.

Demand for raw materials is becoming increasingly pronounced, with a typical datacentre requiring between 5,000 to 15,000 tonnes of copper and extensive networks of glass fibre cables stretching millions of miles.[3] Power generation is set to become a critical area, as projections indicate demand over the next three years equal to adding more than Japan’s annual electricity use to global consumption each year.[4] Should traditional electricity grids struggle to meet this surge in demand, alternative solutions, including small modular nuclear reactors, may gain significant traction.

Further along the value chain, tertiary beneficiaries are leveraging AI to strengthen their competitive edge, whether by enhancing product and service offerings or streamlining operational costs. The potential for AI-driven transformation extends across all sectors, though industries such as healthcare, financials, and consumer-facing services appear particularly well placed. For instance, JPMorgan Chase reported in May 2025 that operational efficiencies generated by AI resulted in cost savings of US$1.5 billion. That said, the impact is unlikely to be uniformly positive for all companies, making rigorous research essential to identify those organisations adopting AI swiftly and effectively, and distinguish them from those lagging behind.

Given the rapid pace of technological change, maintaining a disciplined approach to valuation and remaining adaptable to evolving market dynamics will be crucial for investors seeking to capitalise on opportunities presented by AI.

2. Industrial renaissance

The decade following the global financial crisis was marked by ultra-low interest rates and bond yields. During this period, investors seeking long-term capital growth tended to favour asset-light, digitally focused disruptors and innovators. In contrast, companies operating in more traditional or cyclical sectors, particularly those engaged in manufacturing physical goods, were largely overlooked.

Since then, profound shifts in both financial and geopolitical landscapes have emerged, potentially paving the way for well positioned industrial businesses to thrive. Evidence is mounting of an “industrial renaissance” fuelled by several enduring themes, setting the stage of a significant capital expenditure cycle not seen for many years. As a result, old-economy cyclical manufacturers could become critical enablers in shaping the future economy and, in doing so, have the potential to evolve into secular growth businesses.

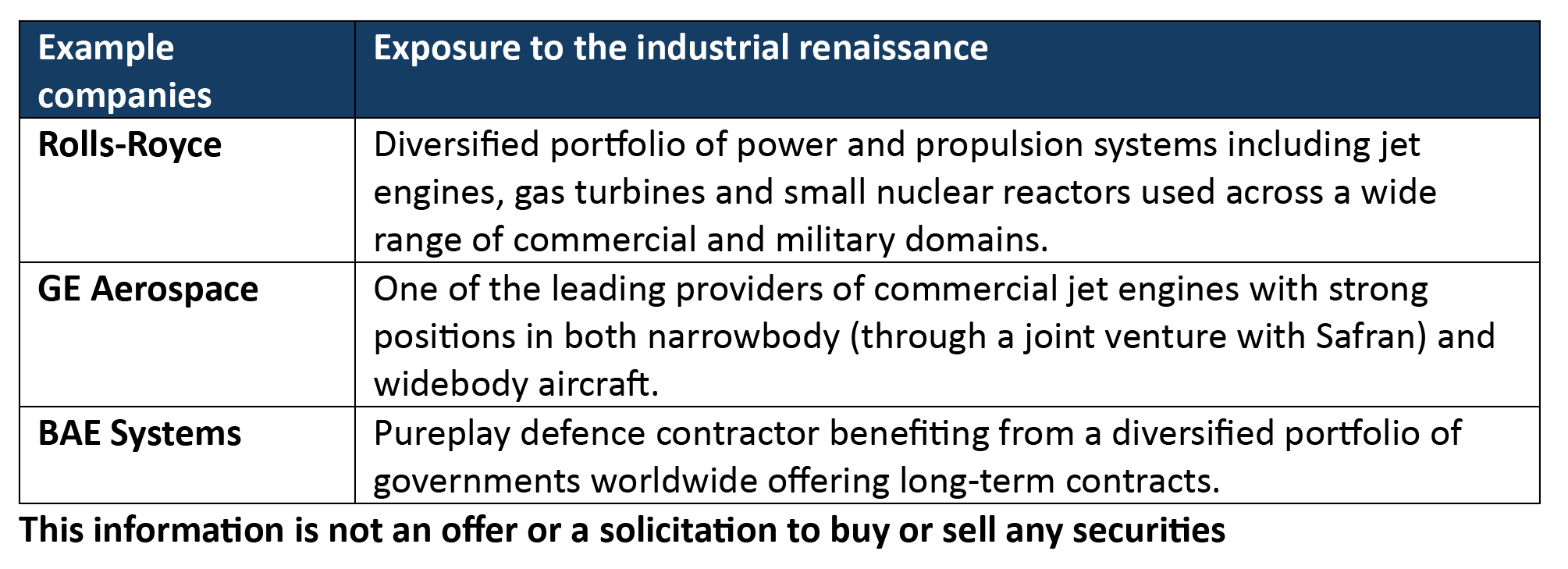

One area poised to benefit is the aerospace and defence sector, where companies are supported by favourable long-term supply and demand dynamics. Commercial aviation, for example, has rebounded from the pandemic and is once again experiencing demand growth that outpaces global GDP growth. Defence businesses also stand to gain from structurally higher government expenditure as geopolitical tensions remain elevated and alliances shift. The sector’s consolidated nature and substantial barriers to entry afford incumbents robust competitive advantages and pricing power. Additionally, revenue streams in this industry are attractive, with contracts often secured years in advance and routine maintenance providing dependable cashflow visibility.

Electrification represents another powerful driver underpinning growth across industrials. Beyond the imperative to decarbonise, electrification supports energy security and independence, facilitates the ongoing digital transformation of the global economy, and enhances operational efficiency while reducing costs. Enduring trends such as electric and autonomous vehicles, factory automation, and the continued proliferation of data centres are expected to persist. This environment presents compelling investment opportunities in businesses supplying power generation equipment, energy management solutions, and automation technologies.

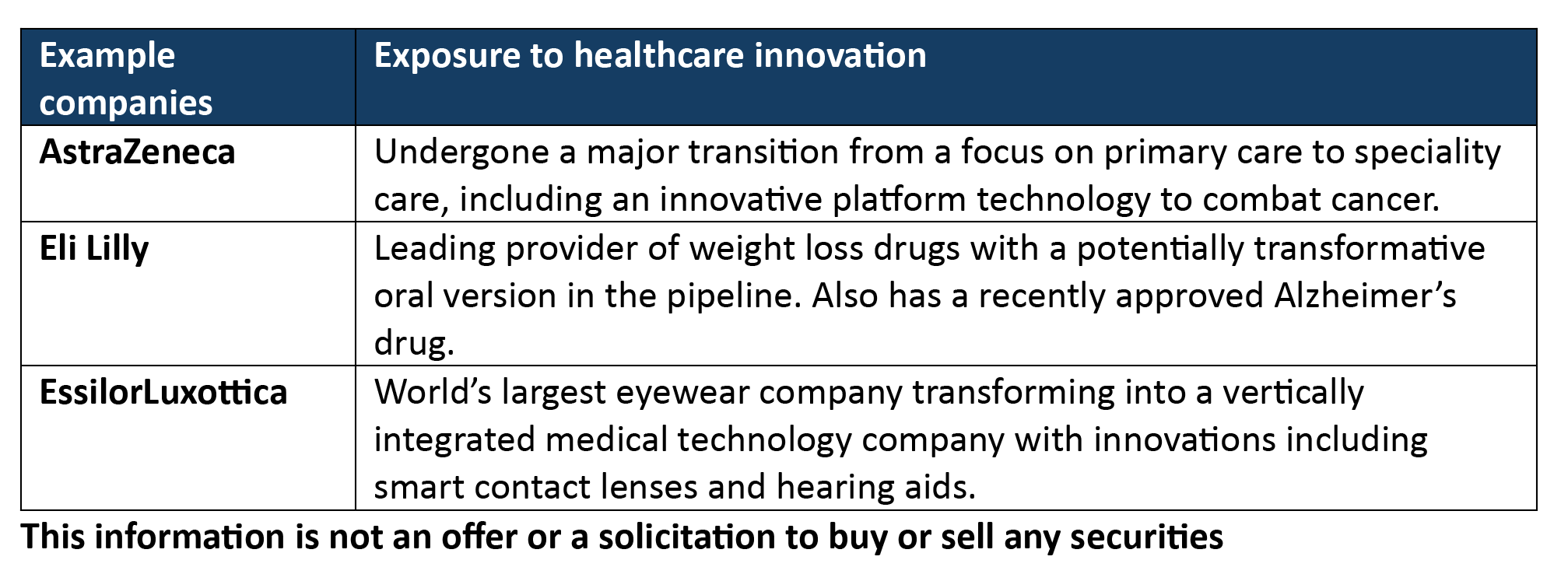

A barrage of external factors such as the potential impact of tariffs, drug pricing reforms and uncertainty at the Food and Drug Administration (FDA) have weighed on the health care sector over recent years. Nevertheless, when taking a long-term perspective, many of our health care analysts remain optimistic about the multi-decade innovation tailwinds from which the sector stands to benefit. While medicine has advanced significantly over the past century, several of the most common and life-limiting diseases still lack effective treatments, representing substantial potential market opportunities. We anticipate meaningful progress in areas such as cancer, obesity, cognitive impairment, and pain management over the coming years.

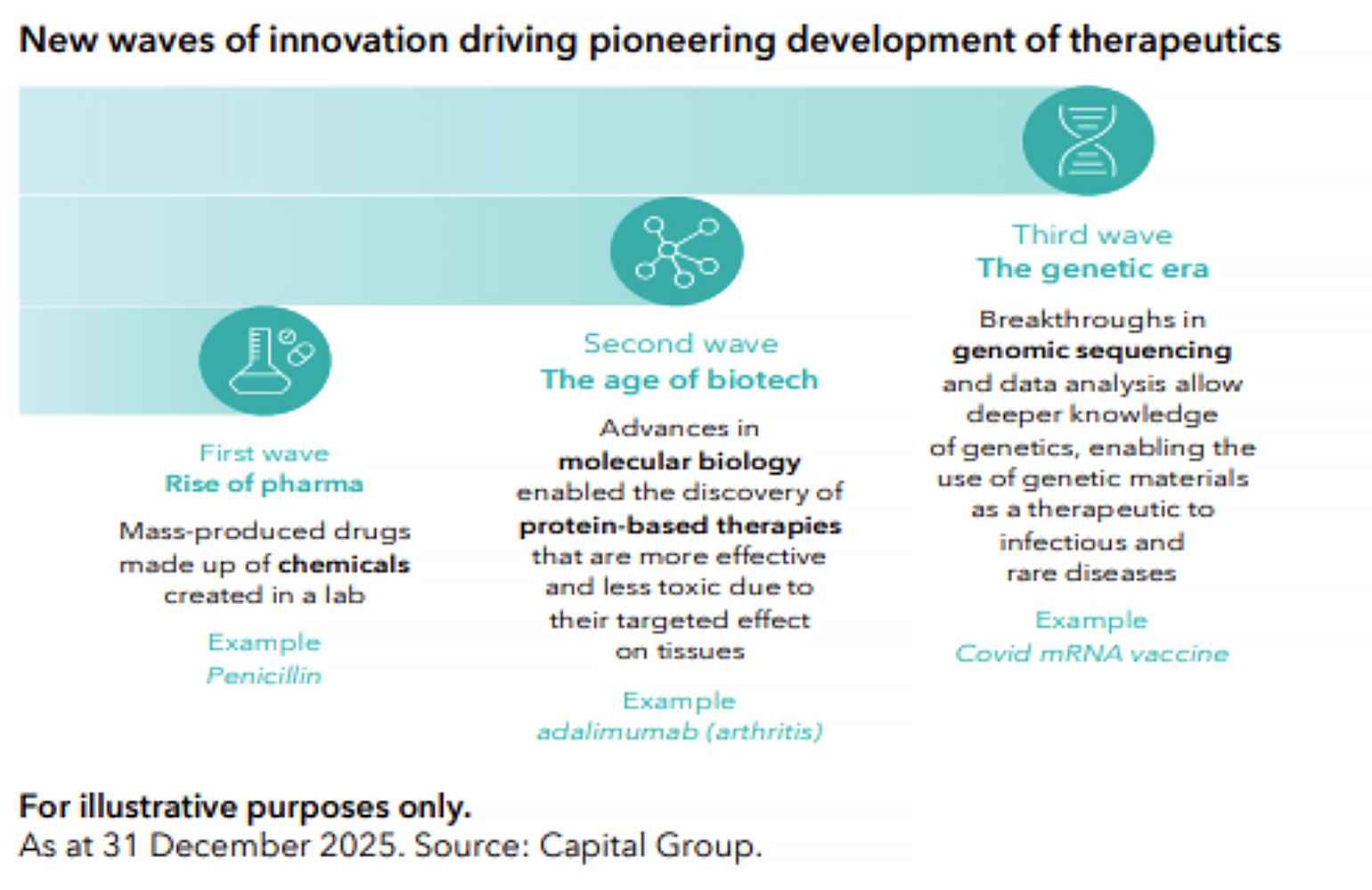

Additionally, breakthroughs in genomic sequencing and data processing are allowing drug companies to research, develop and deliver highly targeted interventions for illnesses, marking what we believe to be a “third wave” of biopharma innovation. For instance, RNA interference (RNAi) technology allows scientists to correct errors in genetic code by identifying defects and effectively silencing them. Gene therapy involves replacing missing or defective genes with functional ones to treat disease, while gene editing allows for the precise modification of specific genome sequences.

This genetic era is unfolding alongside the emergence of another transformative technological advancement − AI. Currently, over 90% of all experimental medicines in development are expected to fail[5] but studies suggest using AI to expedite drug discovery could improve the R&D efficiency of drug exploration and could lead to 50 additional novel therapies over the next decade[6] .

Innovation within the health care sector is further supported by companies supplying essential tools and services to laboratories, presenting attractive pick and shovel opportunities. In addition, medical devices such as robotic surgical systems and smart eyewear may offer a broader range of investment prospects, each with distinct growth dynamics compared to the core biopharma segment.

4. Evolving consumer trends

The consumer sector stands out as fertile ground for companies that are enabling, driving, or benefitting from long-term transformational global trends. Given that household consumption accounts for approximately 67% of global GDP[7] , the sheer scale of the sector amplifies the impact of ongoing changes. Unprecedented shifts, such as structural demographic transitions, rapid technological advancements, and evolving lifestyles and habits, are collectively generating a diverse range of long-term investable themes. These opportunities span developed and emerging markets and encompass a variety of segments, including consumer discretionary, consumer staples, communication services, financials, and industrials.

One compelling development for long-term investors is the rise of the “experience economy”, which reflects a shift in consumer preferences towards valuing memorable experiences over material possessions. This is being fuelled by rising disposable incomes, the amplifying effects of social media, and changing demographic preferences, particularly among younger generations. For instance, cruise travel tends to foster strong customer engagement and brand loyalty, supporting recurring revenue streams and pricing power. Such businesses are generally more resilient to commoditisation and can benefit from network effects, offering attractive growth prospects over the long term.

The acceleration of online and mobile services is particularly evident in the retail space, as time-constrained consumers seek convenience alongside an enhanced experience. E-commerce platforms are using data analytics and personalisation to drive customer engagement and conversion, while scalable logistics and payment systems create significant barriers to entry. The integration of technologies such as AI, augmented reality, and social media is further enhancing user experience and encouraging higher consumer spend, allowing platform-based ecosystems to compound value over time.

Heightened health awareness, increased demand for plant-based and functional foods, and concerns regarding environmental impact are reshaping global dietary trends. Food and beverage companies that are repositioning their portfolios towards more nutritious products and sustainable supply chains are well placed to command premium pricing and foster greater brand loyalty.

A subset of companies could be better placed to navigate these changes

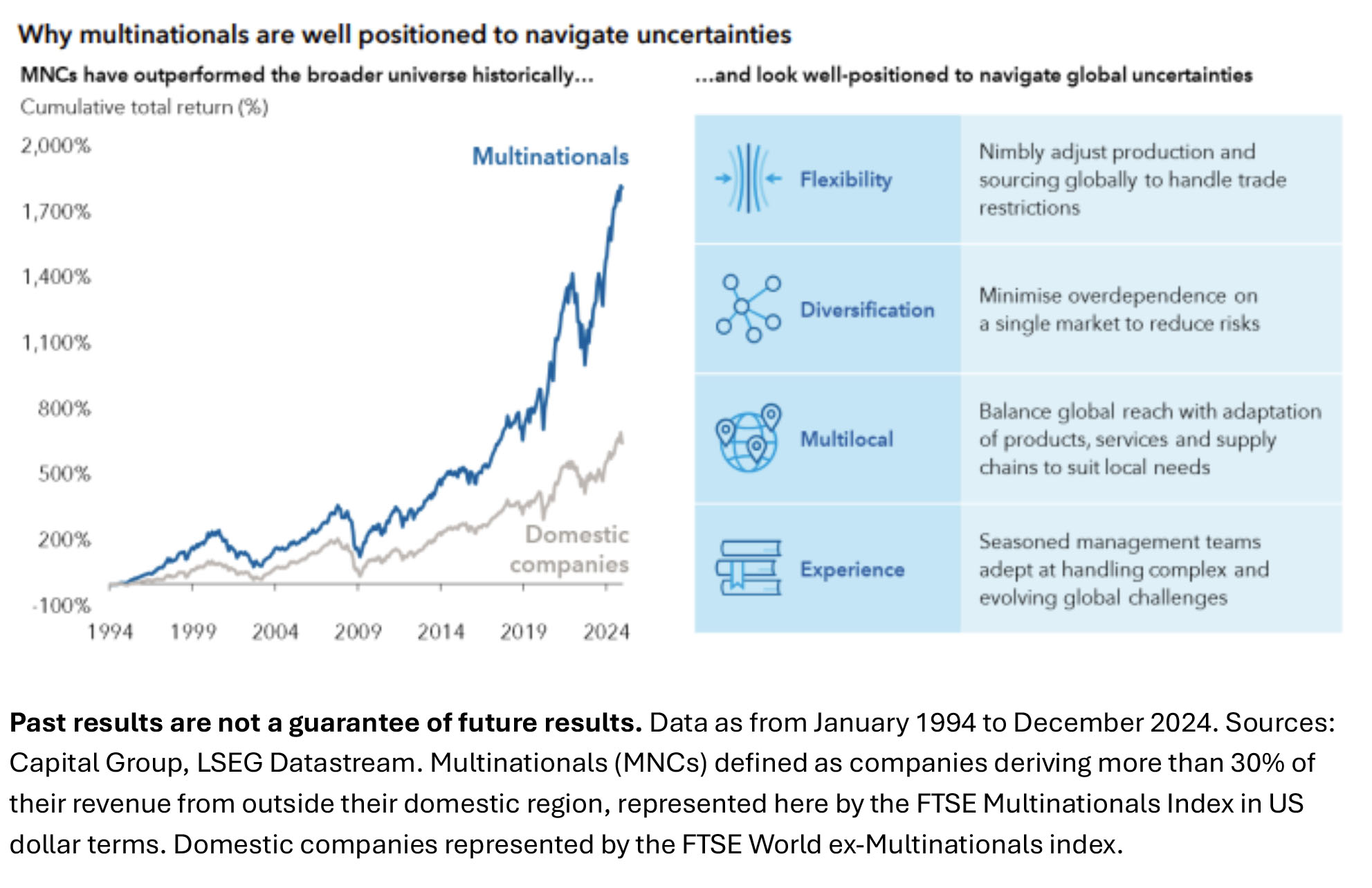

A cohort of companies that has proved particularly effective in responding to change is multinationals, with such global businesses typically well equipped to deal with uncertainty and disruption. For the most part, they have strong and experienced management teams, capable of navigating different − even hostile − environments. They are also used to conducting business across the world, finding ways to succeed by responding effectively to local competition.

An unpredictable environment can often play to the strengths of multinationals, which have the expertise and resources to adapt quickly. If we consider the shifting trade backdrop, for example, the larger the company, the easier it can be to reconfigure supply lines, manufacturing location and final selling point.

Investing in structural change: The Capital Group approach

It is clear, then, that the next decade and beyond could present a rich and more diverse set of investment opportunities versus the previous decade. But that also means it is important to find investment strategies that can navigate significant market shifts, while keeping true to their objectives and philosophy.

At Capital Group, there are certain features of or investment philosophy that have remained consistent for over 90 years:

- Our deep fundamental research allows us to focus on the companies that we believe are best placed to successfully navigate these changes.

- A structurally flexible approach. Investing from the bottom-up allows our portfolios to reposition over the long term to capture the potential global champions of the next cycle and generation, as the macro and geopolitical environment evolves

- Our long-term focus allows us to look beyond short-term noise and market volatility, in keeping with the long horizons over which transformational changes unfold.

We believe these principles are more relevant than ever as we enter this profound period of change.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Managed Investments (0.5 hrs)

please log in to start this quiz

——–

Notes:

[1] Capital Group was one of the first US-based firms to invest outside North America in 1953 occurring simultaneously.

[2] Source: UN Trade and Development (UNCTAD) based on various online market research reports.

[3] Data as at 8 December 2025. Source: Forbes.

[4] Electricity 2025, a report published in October 2025. Source: IEA (International Energy Agency)

[5] Data as at February 2022. Source: National Library of Medicine

[6] Data as at March 2023. Source: Morgan Stanley Research.

[7] Average household consumption as a percent of GDP across 102 countries in 2024. Source: The World Bank.

Statements attributed to an individual represent the opinions of that individual as of the date published and may not necessarily reflect the view of Capital Group or its affiliates. This communication is intended for the internal and confidential use of the recipient and not for onward transmission to any other third party. This communication is of a general nature, and not intended to provide investment, tax or other advice, or to be a solicitation to buy or sell any securities. All information is as at the date indicated and attributed to Capital Group unless otherwise stated. While Capital Group uses reasonable efforts to obtain information from third-party sources that it believes to be accurate, this cannot be guaranteed. In Australia, this communication is issued by Capital Group Investment Management Limited (ACN 164 174 501AFSL No. 443 118), a member of Capital Group, located at Suite 4201, Level 42 Gateway, 1 Macquarie Place, Sydney, NSW 2000 Australia. All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company. All other company names mentioned are the property of their respective companies. © 2026 Capital Group. All rights reserved.

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Managed Investments (0.5 hrs)

please log in to start this quiz——–