Ethics form the foundation of advice, underpinning trust, long-term client relationships and a resilient, sustainable business.

Ethics in financial advice isn’t just about ‘doing the right thing’ to sleep better at night, it’s the fundamental bedrock of a sustainable business model. In this article, proudly sponsored by GSFM, the importance of ethical practice is explored.

In the world of financial advice, it’s common to speak in the language of numbers: compound returns, asset allocation, insurance, yield…

However, the true foundation of a thriving advice practice isn’t found in numbers, it’s built upon the bond of ethical integrity. When a client walks into your office, they aren’t just looking for a higher rate of return. Instead, they’re looking for a partner they can trust with their future, their legacy and, importantly, their peace of mind.

Choosing to lead with ethics is a proactive commitment to excellence. It transforms the adviser-client relationship from a transactional relationship to a partnership. By placing professional standards and the client’s best interests at the centre of every decision, an advice practice does more than just meet requirements, it creates a sense of security, important in this increasingly volatile world.

In this light, a code of Ethics is not a restrictive set of rules. It is a tool that fuels long-term business growth because it fosters deep-seated client loyalty and elevates the professionalism of financial advice.

Professional standards reforms for financial advisers were introduced to the Corporations Act 2001 in March 2017. These reforms were designed to raise the education, training and ethical standards of those providing personal advice to retail clients on ‘more complex financial products’[1]. Those reforms required FASEA (as was) to develop the Financial Planners and Advisers Code of Ethics (Code of Ethics), which came into effect in January 2020.

The introduction of the Code of Ethics came with an expectation from ASIC that Australian Financial Services licensees would take reasonable steps to ensure that their authorised representatives comply with the Code. For example, licensees must:

- Ensure their authorised representatives are aware of the need for compliance with the Code of Ethics and that this compliance is ongoing.

- Provide training and/or guidance to their authorised representatives about the types of conduct that is consistent/inconsistent with the Code of Ethics..

- Facilitate individual advisers’ ability to raise concerns with the AFS licensee about how the licensee’s systems and controls may be hindering their ability to comply with the Code of Ethics, and act on those concerns where appropriate.

- Consider whether advisers are complying with the Code of Ethics as part of their regular, ongoing monitoring of adviser conduct.

- Make any necessary changes to systems and processes to ensure compliance with the Code of Ethics and other regulatory requirements.

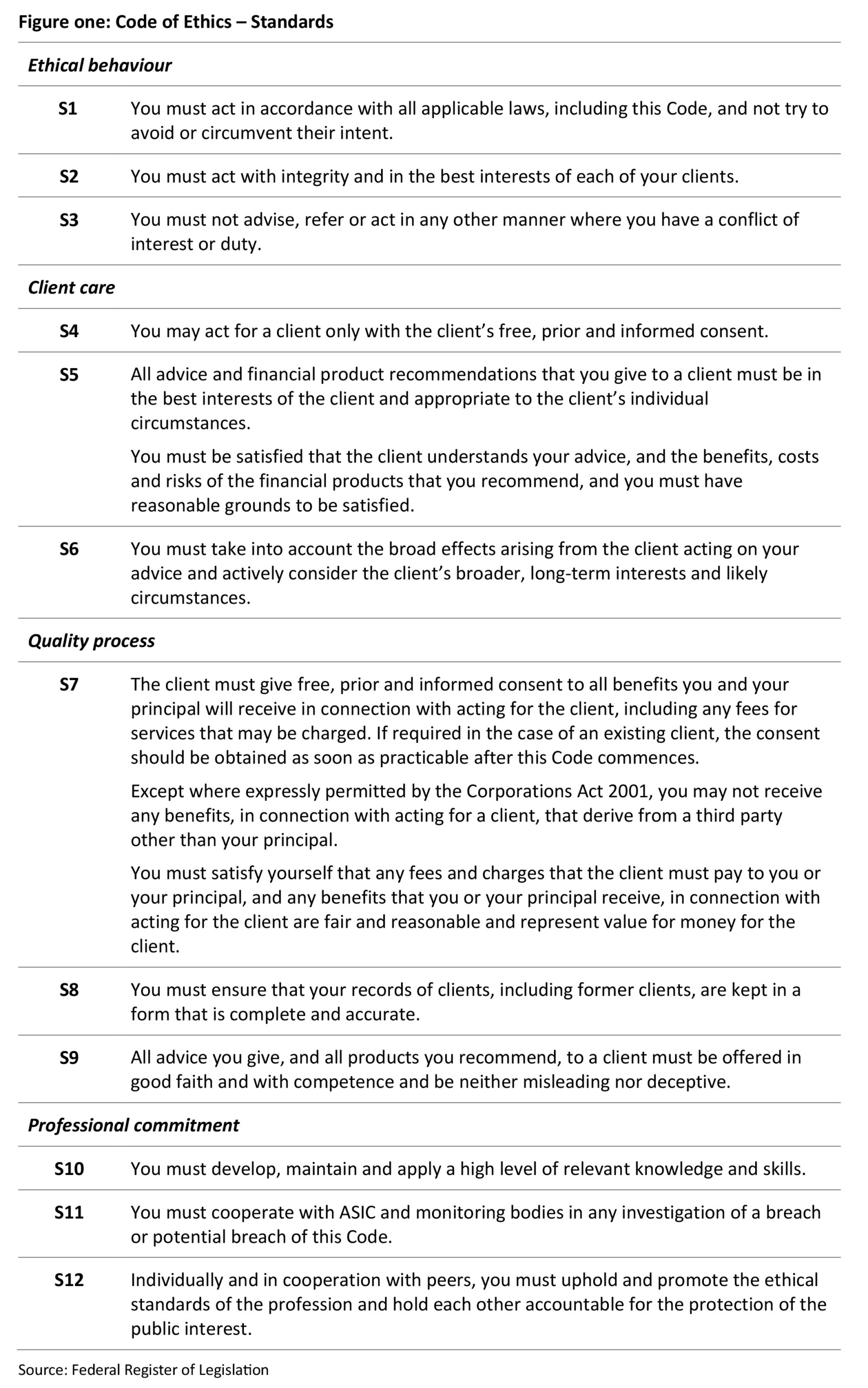

The Code of Ethics addresses five core values: trustworthiness, competence, honesty, fairness and diligence. It requires that financial advisers must act at all times and in all cases, in a manner that is demonstrably consistent with Code’s twelve ethical standards, summarised in figure one. These standards are regulated and monitored by ASIC’s approved compliance schemes.

Ethics is a ‘team sport’

An ethics-centred approach is not a solo performance by the adviser; it is a team sport played by the entire practice. From the first greeting at the front desk to the final signature on a Statement of Advice, every touchpoint is an opportunity to reinforce a culture of integrity, professionalism and care.

The ethical chain of command

To truly embed the values that underpin the Code of Ethics, every role within an advice practice must understand that ethics isn’t just the adviser’s responsibility, they need to know how the Code of Ethics translates into their roles. For example:

- The receptionist – as the face of the firm, they champion ethics through data privacy and by creating a welcoming, transparent environment for every client who walks through the door.

- The paraplanner and administrator – these ‘engineers’ of the financial plan need to ensure that every strategy is executed with technical precision and that paperwork is handled with the highest degree of integrity.

- The practice manager – by prioritising ethical training and fostering an open-door policy, they ensure that the practice’s moral compass remains calibrated as the business grows and new staff join the team.

While every staff member must perform their duties in a way that aligns with the firm’s values, the professional weight remains clearly defined. Each team member’s commitment provides the essential support that allows advisers and licensees to fulfill their regulatory obligations.

Ultimately, although the entire team builds the culture, the adviser and licensee stand as the final guardians of the practice and bear the ultimate responsibility for ensuring that every action taken meets the highest standard of care.

To establish an ethics-centric practice and minimise the risk of violating the Code of Ethics, there are a range of strategies that could be implemented. These include:

1. Code of conduct: by establishing a practice-wide code of conduct, one which encapsulates your firm’s values as well as the Code of Ethics, your team should have a clear understanding of their role and the expectations that go with it.

Any code of conduct should set clear expectations about employee behaviour when performing their role and, in an ethics-centric practice, how each of the twelve standards may specifically intersect their role. This should be a concise and accessible document that is distributed to all staff members, and which is readily available for reference.

2. Communication: establish clear communication channels within your practice to convey the importance of ethics. Regularly discuss ethical considerations during team meetings, emphasising the relevance of the Code to each staff member’s role. A collaborative environment where colleagues can monitor and support each other in upholding ethical standards is important to create and maintain an ethical practice. Encourage open discussions about ethical dilemmas and provide guidance on navigating challenging situations.

It’s also important to communicate clearly, openly and honestly with your clients. In the initial meetings, don’t simply tell them what you will do for them, but detail how you will work with them to achieve their objectives. Establish ongoing channels of communication and explain how you will communicate with them. It’s important to detail the method and frequency.

Remember that it’s important not to make promises that cannot be honoured. As well as potentially breaching the Code, it will reflect badly on the practice.

3. Set key performance indicators (KPIs): by reinforcing your company’s values, adhering to your practice’s code of conduct and behaving in a way that makes ethical behaviour central to each team member’s work will support the creation of an ethical practice. Although a value driven KPI may sometimes be more challenging to quantify than one with specific and measurable outcomes, it will highlight the importance of values and ethics to your practice.

The implementation of accountability measures will ensure that all staff members integrate ethical considerations into their daily responsibilities. Further, to recognise and reward ethical behaviour will reinforce a positive ethical culture.

4. Checklist: a checklist can be used to safeguard compliance with the Code. The questions in the checklist should be tailored to each role in the practice and include those relevant to dealing with prospective clients, new clients and existing clients.

5. Workplace training: this is essential to ensure all staff understand both the practice’s values and the obligations of the Code. Using workshops to promote ethics in your workplace will reinforce the practice’s standards of conduct and clarify behaviours and practices that do and don’t work within your own code of conduct – and within the Code.

Importantly, ethics training should not be a once off. Ethics training could be incorporated as part of a regular team meeting; for example, by using a variety of case studies that address common ethical dilemmas across the financial planning industry. It can be used to emphasise your firm’s commitment to continuous improvement in ethical practices. It also provides an opportunity to seek feedback from staff as to how the practice can better support ethical decision-making and incorporate this input into ongoing improvements.

Ideally, this workplace training should be practical as far as possible and teach team members to make good decisions that are compliant with the law and consistent with your practice’s values.

Ethics training should also be incorporated into the onboarding process for new employees.; this will ensure they receive the necessary information and guidance to understand and comply with the Code from the beginning of their tenure.

6. Feedback loop: by encouraging staff to provide honest feedback about the processes, conversations and client interactions, you are better placed to make sure you’re aware of issues that may arise that could potentially compromise your business. A feedback loop can help you identify gaps in relation to processes and procedures, and where a checklist or workplace training may be useful tools.

7. Lead by example: regardless of your position in a practice, it’s important to set a good example. For those who are senior in the practice, it’s more important to demonstrate those behaviours that are and are not acceptable. Senior advisers and personnel will set the tone for ethics in the practice; as such, they need to embody the Code in all they say and do.

8. Regular audit: These or similar strategies may have already been implemented in your practice. If so, it’s important to review the effectiveness of each. What’s working well and what’s not? If you can identify gaps in processes that may lead to a breach of the Code, it’s better to identify them ahead of time than when ASIC comes knocking on your door.

Why is an ethics-centric practice important?

An ethics-centric practice is important because it transforms the nature of financial advice from a mere commodity into a high-trust partnership. In an industry where clients often share their most intimate life goals and vulnerabilities, a firm commitment to ethical standards provides a moral compass that guides every decision, especially when regulations don’t provide a clear-cut answer.

A culture of integrity does more than just protect the firm from reputational risk; it creates a superior client experience characterised by transparency and peace of mind. Ultimately, when a practice prioritises doing the right thing, it builds a sustainable legacy where the interests of the adviser, the staff and the client are perfectly aligned. This ensures long-term success that can be measured by more than just assets under management.

Furthermore, aside from the legal obligations the Code place on licensees and advisers, ethics play a crucial role in running a successful financial advice practice. The reasons for this in more detail:

1. Client trust: ethical behaviour builds trust and clients are more likely to trust a financial adviser who demonstrates a commitment to ethical conduct. Trust is fundamental in establishing and maintaining long-term client relationships.

Each of the Code’s standards is trust building. A failure in any one area can erode trust and derail the adviser/client relationship.

2. Integrity and professionalism: an adherence to ethical practices upholds the integrity of the financial advice profession. It demonstrates both professionalism and a dedication to acting in the best interests of clients. This, in turn, enhances the credibility and reputation of the individual financial adviser, his or her practice and the industry as a whole.

While integrity underpins several of the Code of Ethic’s standards, it is a specific requirement of standard two, which requires advisers to always act with integrity.

3. Client’s best interests: financial advisers have a fiduciary responsibility to act in the best interests of their clients. Ethical behaviour ensures that financial advisers prioritise their clients’ needs and goals over their own, thereby avoiding conflicts of interest that could compromise the quality of advice provided.

Acting in each client’s best interests is aligned with several standards within the Code of Ethics, notably standards two and five that specifically reference client best interests. Other standards also align with the need to act in a client’s best interests, including standard three (avoiding conflicts of interest), standard four (acting with informed consent) and standard six (consider the long-term effects of advice).

4. Legal and compliance: ethical behaviour aligns with the legal requirements and regulations governing the Australian financial advice industry. Financial advisers who act ethically are more likely to comply with legal standards and have a reduced risk of encountering legal issues or regulatory scrutiny. Unethical behaviour can result in legal consequences, damaging both your career and the practice’s reputation.

Standard one of the Code of Ethics requires that advisers act in accordance with all applicable laws (including the Code).

5. Risk management: ethical decision-making contributes to effective risk management. By considering all advice through an ethical lens, advisers can identify and mitigate potential risks, protecting both clients and the reputation of the advice practice.

This also comes back to standard two, the requirement to act with integrity, for this is a quality that enables advisers to identify and manage risks.

6. Long-term success: ethical behaviour will contribute to the long-term success of your practice. Clients who feel well-served and that you have always acted in their best interests are more likely to remain loyal to you and provide referrals, contributing to the ongoing growth and success of your business.

7. Industry reputation: ethical conduct by financial advisers collectively enhances the reputation of the entire financial services industry. Unethical practices can lead to negative perceptions and erode public trust, affecting not only individual advisers but the industry as a whole.

The reputational damage possible to the industry is the subject of standard twelve and its requirement that individually and in cooperation with peers, advisers must uphold and promote the ethical standards of the profession.

8. Personal satisfaction: Knowing you are making a positive impact on your clients’ lives, acting in clients’ best interests and adhering to a strong ethical framework is likely to enhance the sense of purpose and professional satisfaction in your work. Replicate this across your practice and it’s a recipe for success.

Case studies

The following case studies are based on ASIC’s enforcement activities, FSCP cases or AFCA complaints; however, names and other details have been changed for privacy reasons.

Case study one: Failing to sufficiently account for client circumstances

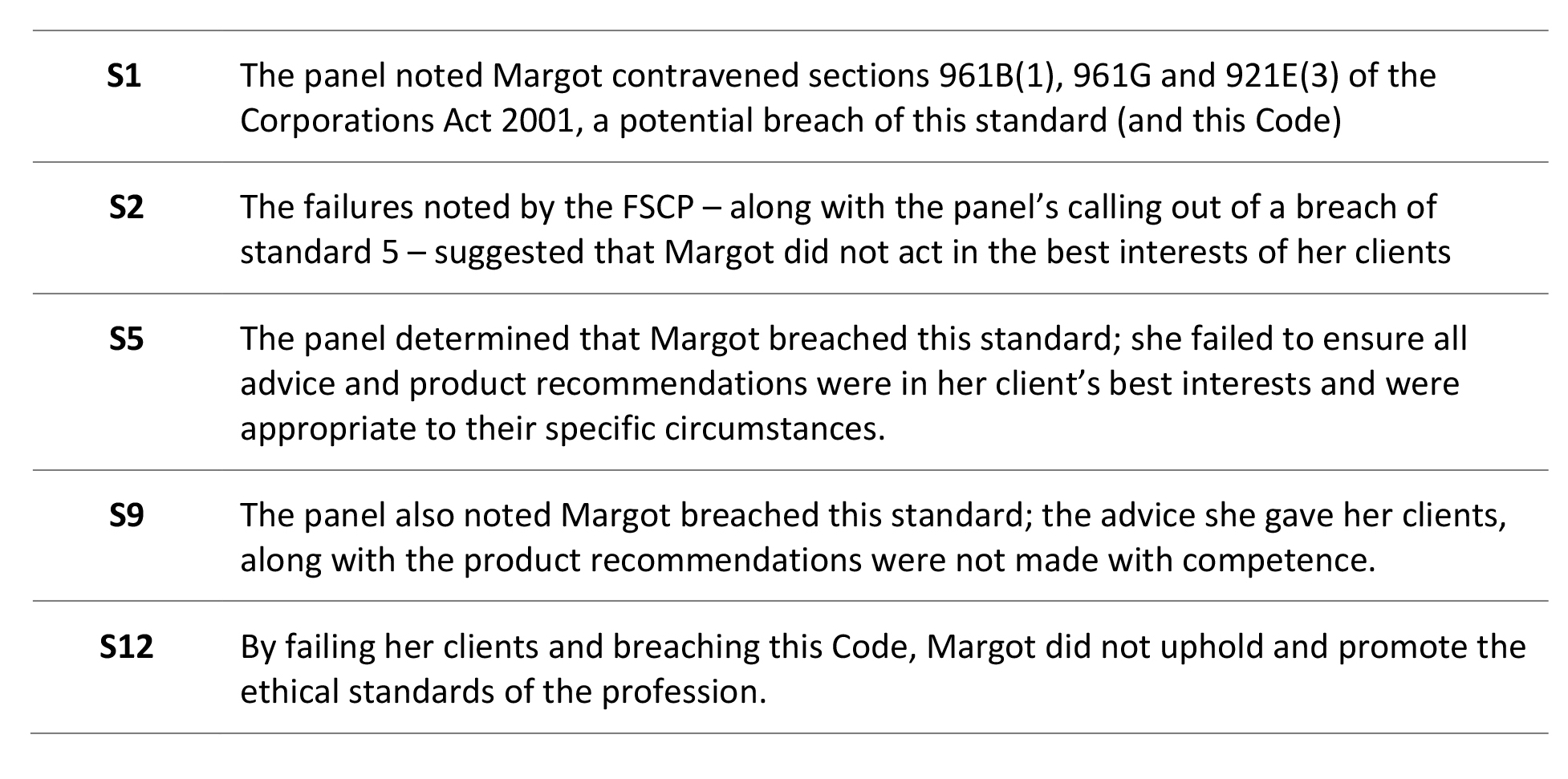

Financial adviser Margot, an authorised representative of ACME Advice, was referred to the FSCP sitting panel after ASIC became aware of allegations of misconduct. The sitting panel determined that Margot contravened sections 961B(1), 961G and 921E(3) of the Corporations Act 2001 in relation to advice provided to two of her retail clients between February 2023 and April 2024.

In relation to the first client, the sitting panel found that Margot had failed to make “reasonable inquiries to obtain complete and accurate information about whether the client held insurance through their existing superannuation before recommending that the client transfer their superannuation from one fund to another fund”.

The second case regarded Margot’s failure to base all judgements in advising the clients on their relevant circumstances. The sitting panel determined that there were “numerous errors and inconsistencies recorded in the SOA” regarding:

- where the client’s existing superannuation was held

- the client’s self-employed status

- whether the client held insurance or not.

Further, the panel commented that in providing the advice, Margot had “failed to demonstrate the Code of Ethics’ values of competence and diligence and breached Standards 5 and 9 of the Code of Ethics.”

In this instance, Margot received a written reprimand from the FSCP.

The FSCP sitting panel determined that Margot breached two standards. There are other potential standards the panel could have considered to have also been breached as follows:

Case study two: Dishonest practices

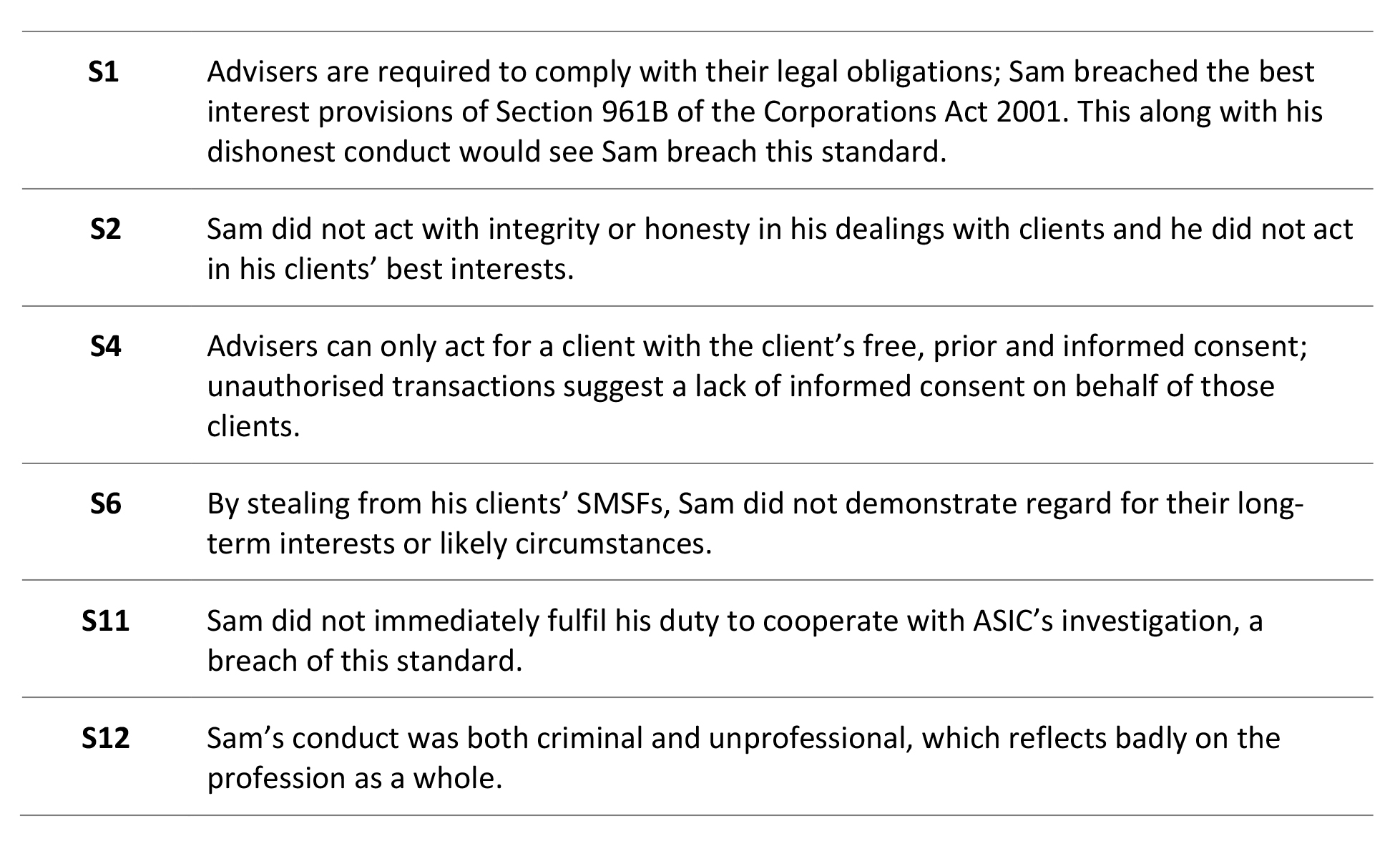

Financial adviser Sam was a sole practitioner whose financial advice practice, ACME SMSFs, focused on dealing in listed securities and advising on self-managed superannuation funds (SMSFs). He was investigated by ASIC after clients Pam and Nigel grew concerned about funds being withdrawn from their SMSF, transactions they had not authorised.

Although Sam did not initially cooperate with ASIC’s investigation, the regulator eventually exposed his dealings and found Sam had:

- made 144 unauthorised transfers, impacting 11 clients, totalling nearly $2.75 million

- used these stolen funds for personal reasons, including gambling and paying off personal debt

- made false representations to clients and other third parties about the unauthorised transfers with the intent to conceal his dishonest conduct.

Sam was convicted of 15 offences of dishonesty and sentenced to eight years’ imprisonment with a non-parole period of five years. He was also permanently banned from providing financial services or from controlling an entity carrying on a financial services business.

ASIC found Sam took advantage of the trust placed in him by his clients. The regulator determined it was appropriate to permanently ban Sam because of the seriousness of his misconduct, the impact on his clients and the need to prevent future harm to consumers.

Sam potentially breached the following standards of the Code of Ethics.

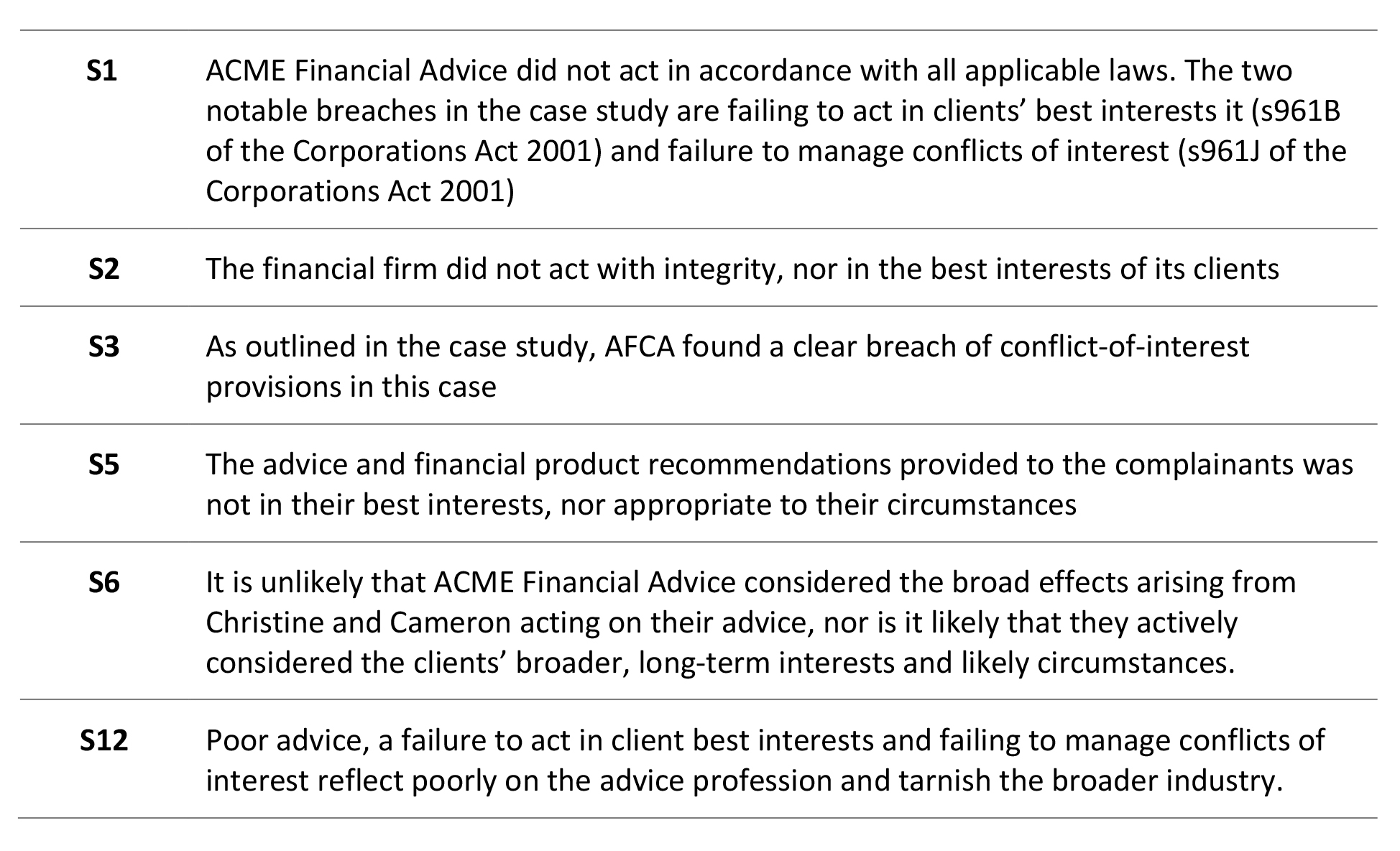

The complainants in this case, Christine and Cameron, are corporate trustees of a self-managed superannuation fund. They were clients of financial firm ACME Financial Advice from 22 October 2019 to 4 July 2025.

The complainants believe that the financial firm’s advice was not appropriate for their SMSF during this period. They cited several reasons in their complaint:

- the recommended asset allocation was too aggressive for its conservative members

- it was unnecessary to take on the degree of risk that was recommended to achieve their objectives

- the financial firm was conflicted when it made the recommendations.

The financial firm denied the allegations. Its stated case is that the recommendations were appropriate for the complainants and that it managed any potential conflicts of interest in accordance with its obligations.

AFCA’s investigation found that ACME Financial Advice did not provide appropriate advice to Christine and Cameron, nor did it act in their best interests. The findings noted that ACME Financial Advice:

- failed to provide advice within the risk parameters it set

- failed to diversify the portfolio’s growth assets, with the portfolio too heavily weighted towards property

- recommended an overly high proportion of related entity investments without justification.

AFCA found that the SMSF would have been $252,565 better off had Christine and Cameron not followed the advice provided. Consequently, AFCA’s determination was in favour of the complainants and ACME Financial Advice had to pay the complainants $252,565 compensation plus interest.

By not disclosing required information and misleading the client by omission, ACME Financial Advice potentially breached the following standards in the Code of Ethics:

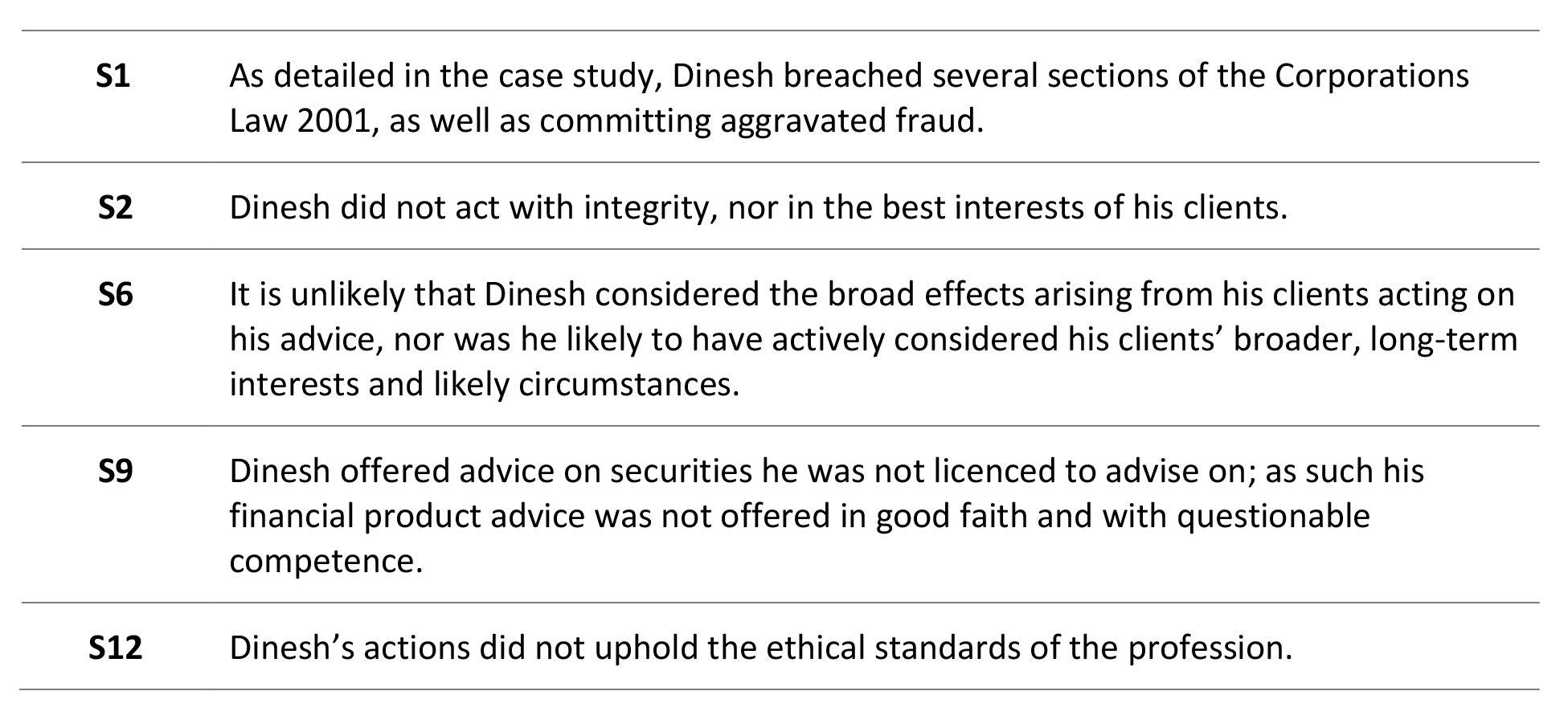

Gold Coast based financial adviser Dinesh – also a certified practising accountant, registered tax practitioner and self-managed superannuation fund auditor – was a director of ACME Financial Services & related company ACME SMSFs.

Following an ASIC investigation, it is alleged that between March 2018 and August 2024, Dinesh provided unlicensed financial services related to securities, executed unauthorised share trades on client accounts, falsified a fixed-term deposit certificate and misappropriated funds from both personal and SMSF bank accounts belonging to his clients for his benefit or the benefit of third-parties.

As a result of his conduct, it was alleged that Dinesh misappropriated funds totalling nearly $5 million and caused trading losses of approximately $1.25 million.

At the relevant time, Dinesh was authorised by ACME Financial Services Pty Ltd to provide financial product advice regarding retirement savings account products and superannuation. He was charged with two counts of dealing in securities without a licence to do so. The maximum penalty is between two and five years’ imprisonment. He was also charged with breaching each of:

- s1041G Corporations Act 2001, which requires that a person must not, in the course of carrying on a financial services business in this jurisdiction, engage in dishonest conduct in relation to a financial product or financial service.

- s1311 of the Corporations Act 2001 which establishes the general penalty provisions for offences under the Act, creating criminal liability for contravening, or failing to comply with, the Act’s requirements.

Each of these breaches carry a maximum penalty of 15 years’ imprisonment.

Dinesh was also charged with seven counts of dishonestly applying property of another to himself or another, in circumstances where the value of the property has a value of at least $100,000 (aggravated fraud). The maximum penalty for each offence is 20 years’ imprisonment.

In the constantly evolving financial advice landscape, products can be replicated and strategies can be automated, but a culture of trust and integrity remains irreplaceable. Managing an ethics-centred practice is more than a strategy for avoiding risk: it’s an investment in the most valuable asset any firm can manage…your clients and the trust relationship.

An ethics centric practice will benefit from three key synergies:

- Client retention – because trust creates the strongest bond in any professional relationship, ethical practices hold on to their clients (and grow through referral) whatever is happening in markets.

- Operational clarity – a shared ethical code simplifies decision-making for staff, as the ‘right’ path and important decision making is defined by values rather than rules.

- Professional pride – employees are more engaged and productive when they believe in the social value and honesty of their work.

When every member of your team operates with a shared moral compass, a virtuous cycle is created, one where clients feel secure, staff feel empowered and the business achieves a level of resilience that market volatility cannot shake. In this industry, doing the ethical thing is quite literally the best way to do well.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Professionalism and Ethics (0.5 hrs)

ASIC Knowledge Requirements: Ethics (0.5 hrs)

please log in to start this quiz

———

Notes:

[1] https://www.legislation.gov.au/Details/F2019L00117

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Professionalism and Ethics (0.5 hrs)

ASIC Knowledge Requirements: Ethics (0.5 hrs)

please log in to start this quiz

———