For decades, retirement income strategies have been built around account based pensions, annuities and the Age Pension.

Retirement planning has long been framed as a numbers exercise. How much someone needs to accumulate, what returns can be achieved and how long that capital needs to last. However, for many retirees, the real issue isn’t whether the numbers stack up on paper – it’s whether they have enough confidence to live like they do.

Advisers regularly see clients who can afford to spend more, but don’t. Despite careful modelling, conservative assumptions and contingency planning, fear of living too long or encountering the ‘wrong’ market conditions tends to keep many clients in a holding pattern. The result is often cautious drawdowns, defensive portfolios and a retirement that is technically funded, but often, not fully enjoyed with confidence.

As longevity increases and retirement horizons extend, this confidence gap has become one of the most challenging issues in retirement planning. The value of advice lies not just in building wealth, but in ensuring clients feel confident enough to spend in retirement.

The difference between knowing the money won’t run out and merely hoping it won’t have a profound impact on how retirement is experienced. This is where innovative lifetime income streams are starting to reshape the conversation.

The problem traditional strategies don’t fully resolve

For decades, retirement income strategies have been built around account based pensions, annuities and the Age Pension. Each plays an important role but only addresses part of the retirement confidence problem.

Account based pensions provide flexibility, liquidity and control. They allow retirees to retain full access to capital and adjust income as circumstances change. However, they also place the burden of managing longevity risk, sequencing risk and spending discipline on the individual. For many retirees, this leads to underspending, driven by fear of running out later in life.

In contrast, traditional annuities address longevity risk, but do so with reduced flexibility and access to capital. For many people, that trade off can feel too restrictive and has historically reduced their appeal.

And, while the Age Pension provides a valuable safety net, it’s means tested, subject to policy change, and rarely sufficient on its own to support the lifestyle many retirees aspire to.

The result is a retirement income landscape defined by trade-offs. Innovative retirement income streams emerged in response to help bridge the gap.

A new way to think about retirement income

Innovative lifetime income streams are best understood not as a single product type, but as a different way of thinking about, and solving for, the retirement income confidence gap.

Rather than replacing existing strategies, they are designed to complement other sources of retirement income by providing stability and certainty that can work alongside more flexible retirement investments and other income sources.

They were born from a recognition that retirement is not just about accumulating savings, but guiding how those savings are drawn down over time to help retirees optimise retirement income consumption needs, while managing the fear of running out.

The rules that define a retirement income stream (and therefore eligibility for tax concessions) have been broadened, allowing a wider range of lifetime income solutions to emerge, including deferred income streams. Since 2022, the Retirement Income Covenant has also required trustees to formulate and regularly review a retirement income strategy, with a focus on supporting members to maximise income while managing key risks, including longevity risk.

While not mandating specific products, these developments have created a stronger foundation for innovation in how retirement income is delivered.

At a high level, innovative lifetime income streams support retirement income in three ways. Firstly, they introduce a component of income that’s guaranteed to continue for life, providing greater confidence that the Age Pension will not need to be relied upon as the sole source of retirement income. Secondly, by securing an amount of guaranteed future income, they promote greater confidence in drawing down from account based pensions and other retirement savings, in the earlier years of retirement. Finally, depending on the specific product, they can also significantly improve Age Pension entitlements through concessional means test treatment.

A deeper dive: how innovative income streams actually work

At a high level, innovative lifetime income streams may be offered by life companies or super funds (sometime in combination).

Income payments are generated from capital, investment returns, as well as the reallocation of capital from members who exit the pool with remaining balances (often referred to as ‘mortality credits’ or bonuses).

Despite being grouped under a single category, products differ significantly. Key variables include:

- the timing of income (including whether income payments start immediately or can be deferred for a specified period)

- investment options, and whether income is fixed, indexed or investment linked

- level of access to capital, including any death and exit benefits, and

- whether the structure satisfies the requirements for concessional social security means test treatment.

Opting in during accumulation

Some providers may allow members a choice to opt into these structures in accumulation. While the account operates as an ordinary accumulation account, from a product perspective the person is within a framework that supports the future commencement of a lifetime income stream. Contributions and rollovers made to the account are compounded using the upper deeming rate, rather than actual investment returns, to determine the purchase price of the future lifetime income stream for social security purposes. This may lead to an uplift in benefits under the assets test. Further concessions may also apply, further reducing the assessable asset and income value, and potentially improving Age Pension entitlements even further. This is explained in more detail below.

Income for life

If a person enters the lifetime income framework in accumulation phase, once a condition of release is met, they can generally choose whether to commence a lifetime income stream with some or all of their funds or can make a lump sum commutation (including to commence a regular account based pension). Commutations need to be completed within 14 days of meeting a condition of release, after which time capital restrictions commence.

Some products may also offer the ability to defer commencement of a lifetime income stream for a specified period of time, rather than commencing it immediately. Deferral can play an important role in managing longevity risk, as income starting later in life requires less upfront capital and provides protection when the risk of outliving savings is greatest. Additional contributions during the deferral period may also be possible, allowing retirement savings to continue to grow. However, after deferral, access to capital is restricted (see below).

Once income payments commence, no further capital can be added to the income stream, and income is then paid for life. The amount of income depends on the product design and rules and may be impacted by the initial investment, the person’s age, gender, whether the income stream is investment linked, and whether a death or exit benefit option has been selected.

Payments must be made at least annually and, unlike account based pensions, are not subject to standard minimum drawdown requirements. Instead, payments are determined by the trustee, within the product’s rules designed to prevent unreasonable deferral of income.

The amount that can be accessed as a lump sum or commuted and rolled over reduces over time, eventually reaching a point where no voluntary withdrawals are permitted. This is effectively the trade-off for certainty of lifetime income.

Restricting capital access to support certainty of income

Limiting access to capital is a requirement under super law, which effectively ensures that sufficient capital remains available to fund income payments for those who live longer than expected.

The Capital Access Schedule (CAS) governs how access to capital changes as the individual ages. Broadly speaking, rather than requiring retirees to give up access to capital immediately and permanently, access is progressively restricted over time. Beyond life expectancy, voluntary access typically ceases. This flexibility distinguishes innovative lifetime income streams from the annuities that came before them.

Death and exit benefits

Many existing innovative lifetime income streams offer some form of death benefit, exit benefit, or both, which must be limited to no more than the legislated amount. It’s important to note that these features are optional and vary between products. Where death or exit benefits are offered, lifetime income is generally reduced.

Some products allow retirees to opt out of death benefits entirely in exchange for higher income. Others provide stepped or capped benefits that decline over time in line with the CAS. In effect, retirees are able to decide how much liquidity they are willing to trade for certainty.

How social security fits into the picture

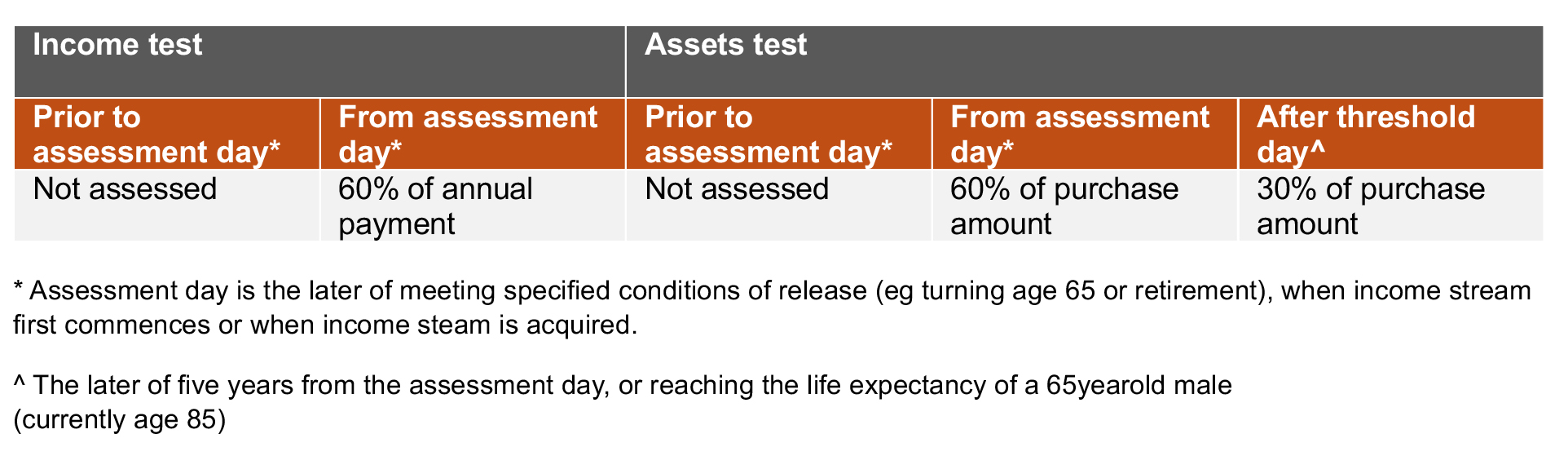

Where an innovative lifetime income stream[1] satisfies certain requirements and meets the definition of an ‘asset tested lifetime income’, concessional treatment under both the asset and income test may significantly improve social security entitlements. Specifically, this requires the income stream to conform to the CAS rules which limits the surrender value and death benefits payable. While all lifetime income streams must restrict access to capital under superannuation rules, only those that meet stricter requirements under social security law are eligible for concessional social security treatment.

As explained previously, if the person enters a lifetime product in accumulation phase, a notional account balance (based on the upper deeming rate rather than the actual returns on rollovers and contributions to the account) ultimately forms the basis for the purchase price for the social security assets test. Given that calculation often results in an assessable purchase price that is lower than the actual account balance, this can provide a higher entitlement under the assets test.

A further concession is available to further reduce the amount of the purchase price that is assessed under the assets test, and the amount of income that is assessed. This also applies to innovative income streams that aren’t commenced in accumulation.

Therefore, means testing outcomes are often more favourable when compared to holding the same amount in an account based pension.

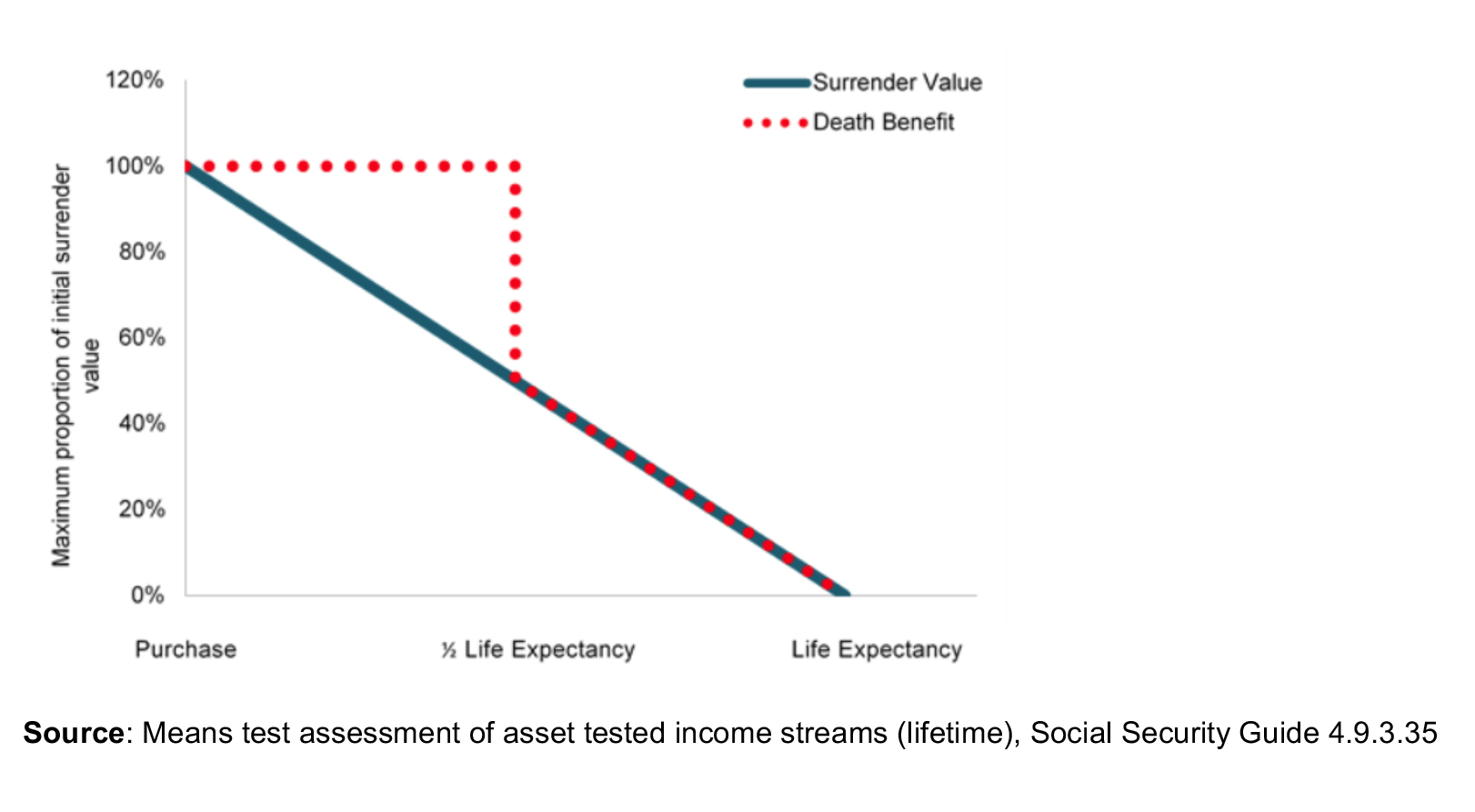

The graph below shows the maximum limits on access to capital to qualify for concessions, based on life expectancy. The surrender value decreases over time and is equal to 50% of the surrender value at halfway to life expectancy, reducing to nil once a person reaches life expectancy. The amount that can be received as a death benefit is limited to 100% of the initial surrender value to halfway to life expectancy, reducing on a straight-line basis thereafter.

They often suit clients seeking greater certainty. That is, those who find the idea of drawing down capital uncomfortable, even when it’s entirely appropriate to do so. They can be particularly valuable for clients with a reasonable level of assets who are unlikely to rely fully on the Age Pension, but who still benefit from optimising how their assets are assessed

over time.

They may also appeal to clients who want to simplify decision making later in life. Having a portion of income that is effectively ‘set and forget’ can reduce cognitive load as clients age, and provide reassurance not just for them, but for their families. This may include through the provision of reversionary options, subject to the product rules.

They may be less suitable where full flexibility and access to capital is the overriding priority, or where estate planning objectives require assets to remain fully accessible.

But for many clients, the question is no longer whether these solutions have a role – it’s how much of their total retirement savings should be allocated to them.

Final note

Innovative income streams recognise that flexibility alone does not create confidence, and that longevity risk may often need to be addressed structurally rather than managed through conservative behaviour. Their role is becoming increasingly clear, not as a replacement for what already works, but as a carefully designed component that helps bridge the gap between flexibility and certainty. For many retirees, that difference determines whether retirement is merely funded, or genuinely lived.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Retirement (0.5 hrs)

please log in to start this quiz

———

Notes:

[1] Applies to lifetime income streams purchased on or after 1 July 2019. Grandfathering applies to lifetime income streams purchased before this date.

Disclaimer: This article has been prepared by IOOF Investment Management Limited (IIML) ABN 53 006695 021, AFSL 230524, RSE License No. L0000406 as Trustee of the IOOF Portfolio Service Superannuation Fund ABN 70 815 369 818. IIML is part of the Insignia Financial Group of companies, consisting of Insignia Financial Ltd ABN 49 100 103 722 and its related bodies corporate. The information in this document is factual information or general advice only and does not consider any individual‘s needs or objectives. Any calculations are for illustrative purposes only. The information in this document has been given in good faith and has been prepared based on information believed to be accurate and reliable at the time of publication. Before making any decisions, advisers and their clients should consider the relevant Product Disclosure Statement, which together with the Target Market Determination is available to view and download at myexpand.com.au.

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Retirement (0.5 hrs)

please log in to start this quiz———

Notes:

[1] Applies to lifetime income streams purchased on or after 1 July 2019. Grandfathering applies to lifetime income streams purchased before this date.

Disclaimer: This article has been prepared by IOOF Investment Management Limited (IIML) ABN 53 006695 021, AFSL 230524, RSE License No. L0000406 as Trustee of the IOOF Portfolio Service Superannuation Fund ABN 70 815 369 818. IIML is part of the Insignia Financial Group of companies, consisting of Insignia Financial Ltd ABN 49 100 103 722 and its related bodies corporate. The information in this document is factual information or general advice only and does not consider any individual‘s needs or objectives. Any calculations are for illustrative purposes only. The information in this document has been given in good faith and has been prepared based on information believed to be accurate and reliable at the time of publication. Before making any decisions, advisers and their clients should consider the relevant Product Disclosure Statement, which together with the Target Market Determination is available to view and download at myexpand.com.au.