AI is reshaping bond markets, driving divergence in outcomes and signalling a greater need for active, research-driven investment strategies.

Key takeaways

The Artificial Intelligence (AI) revolution has a number of clear implications for bond investors:

- The Sovereign bond investor – AI has the potential to have a marked effect on the shape of sovereign yield curves. A long-term productivity boost from AI could help advanced economies address debt sustainability as well as achieve higher growth with lower inflation. In turn, this could drive flatter curves over time and reinforce the safe-haven status of these institutions. However, debt burdens are likely to worsen before the productivity benefits from AI manifest, which could lead to higher term premia and steeper yield curves in the short term. Additionally, high dispersion of outcomes across economies is expected based on their ability to benefit from the AI productivity boost.

- The income and credit investor – Implications for credit markets are expected to be highly idiosyncratic and evolving. Developments such as those in the Digital Infrastructure Asset Backed Securities (ABS) space offer interesting opportunities for differentiated sources of yield. However, issuance trends, new debt structures and securitised pools, as well as the effect of AI adoption across industries and regions, need to be monitored.

- The active bond manager – While AI has the potential to democratise information and provide a greater number of investors with more power to make decisions, it can also lead to commoditised insights. In our view, the key to taking active risk remains in fundamental and proprietary research, enhanced by the use of AI, to drive differentiated insights. Additionally, trading in fixed income is set to undergo a transformation with AI, meaning dedicated trading capabilities to stay ahead of these trends become vital.

Artificial Intelligence (AI) has the potential to rapidly reshape our lives, including the way we work, learn and interact with one another. Understandably, the potentially transformative nature of this technology has already impacted financial markets. But importantly, the investment-related effects of AI are far more wide-reaching than tech stocks; AI’s impact on bonds, for instance, can be easily overlooked.

For instance, AI’s effect on debt sustainability, growth and inflationary trends has potentially profound effects on bond yields, curve shape and credit spreads. In the corporate bond context, AI can have huge impacts on issuers themselves, which affects spreads and their ability to service their debt obligations. Additionally, AI could also have profound impacts on adjacencies associated with trading and execution, as well as the role of active management in fixed income investing.

While some of these themes may seem more indirect and have thus far seen less immediate impact on market prices, we believe the long-term implications for bond investors are too big to ignore today.

The sovereign bond investor – Can AI flatten the curve?

One profound implication of AI could be its influence on long-term sovereign debt levels.

Since the Global Financial Crisis (GFC) of 2008, we have seen a seismic shift in debt dynamics globally, where, in effect, developed market governments have taken on the burden of debt from corporates and households.

Across developed markets, corporates and households both embarked on a period of fiscal consolidation after the GFC. On the corporate side, regulations and investor appetite increasingly rewarded companies that demonstrated balance sheet repair, while on the consumer side, stricter lending standards and stable wage growth meant less credit exuberance. This resulted in lower levels of overall leverage being taken on by these cohorts.

In contrast, developed market governments generally saw a significant increase in debt levels, largely driven by a need to stimulate their economies with fiscal spending post the crisis. This trend has continued through the COVID period due to a combination of 1) populist governments increasingly promoting more accommodative policies and 2) increased defence and infrastructure spending after years of austerity.

The current significant level of debt, is further exacerbated by three forces:

- Projected fiscal deficits across developed economies,

- Increased interest expense burdens as rates have risen since 2021

- An aging demographic across many developed market countries

These forces have left many investors concerned about debt sustainability across developed markets. From a fixed income investor’s perspective, any rising doubt about an economy’s ability to repay its debt obligation is reflected in a higher term premium, resulting in higher and steeper yield curves over time. Such doubts also reduce a bonds’ effectiveness as a diversifier in risk sell-off environments. This is because higher levels of debt put pressure on investors’ perception of government bonds being a true safe-haven asset class.

AI could be an unsuspecting saviour for the sovereign debt issues currently facing investors.

Productivity and its effect on long-term bond yields

In the recent paper The Great Global Restructuring, Capital Group experts discussed the radical effect that AI can have on global productivity. In short, AI’s ability to transform productivity across economies has the potential to lift trend global growth beyond current estimates.

While the positive impact of higher productivity transcends asset classes, its effects can be profound in the fixed income context. Higher productivity typically exerts downward pressure on unit labour costs and inflation, allowing an economy to produce more goods and services with the same or fewer inputs. In other words, an economy is able to achieve the perfect growth scenario: higher levels of nominal growth without corresponding inflationary pressure.

This in turn suggests that a sustained productivity uplift can flatten yield curves, as long-term growth expectations rise but inflation remains contained. This means long-term interest rates may not need to rise as much as they would if growth were driven by demand-side factors, which tend to be more inflationary.

Productivity and its effect on debt and deficits

But AI productivity’s benefits don’t just stop at inflationary effects, it could also provide governments with the opportunity to achieve debt sustainability.

A technical definition of debt sustainability is the ability for an economy to have nominal growth outpacing interest burdens. If AI were able to promote higher productivity, as suggested above, this could improve fiscal sustainability by expanding nominal GDP faster than debt accumulation, essentially enabling economies to “grow out” of elevated debt burdens. This scenario reduces pressure on sovereign borrowing costs and mitigates concerns about debt-to GDP ratios.

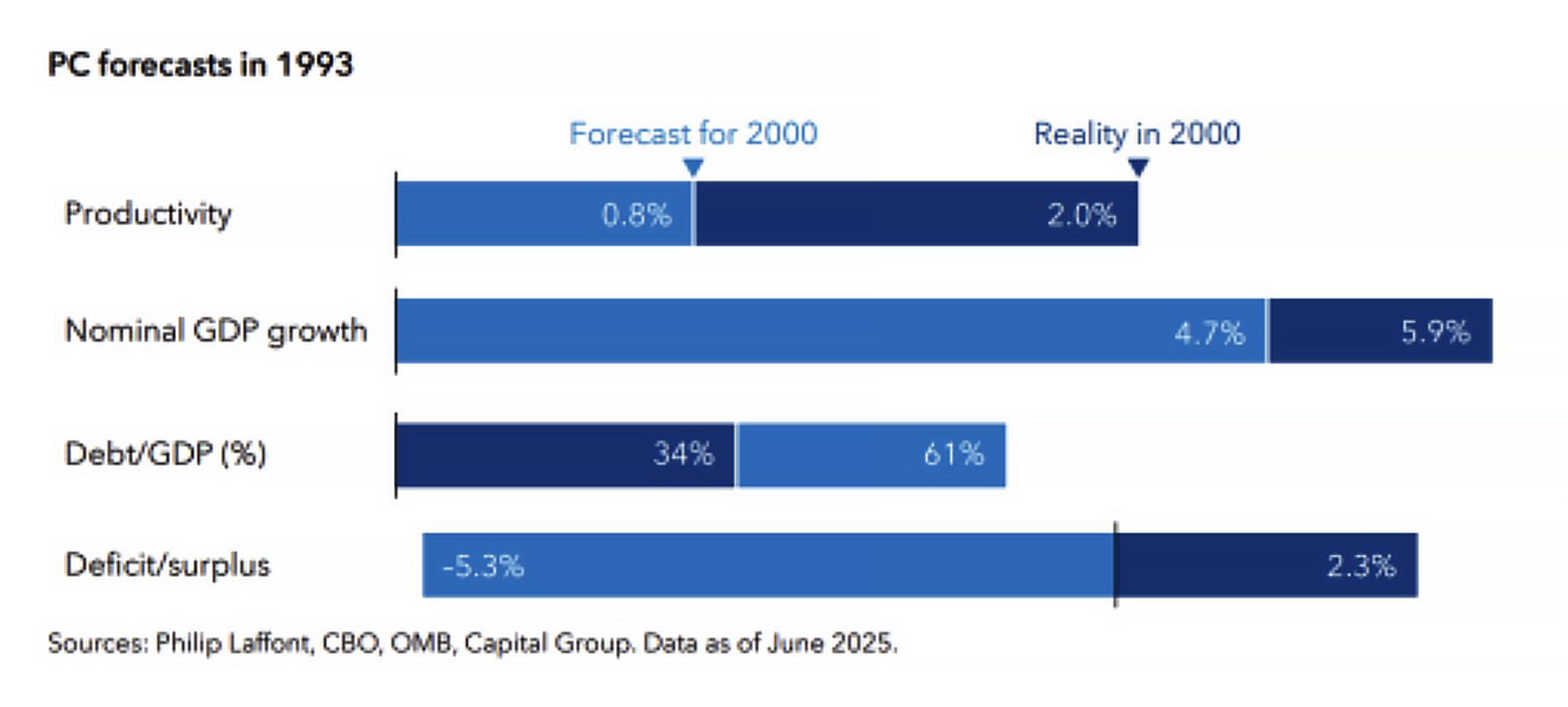

Analysis produced for our Great Global Restructuring paper demonstrates how we have historically underestimated the productivity boosts from new technologies. A case study from the PC era demonstrates that underestimating productivity contributed to a greater than expected benefit to both debt-to-GDP and the current account in the US.

For fixed income markets, this interplay shapes sovereign credit spreads, term premia, and demand for safe assets. If the same phenomenon as the PC era capitalgroup.com 4 were to happen again, AI could also give developed economies a solution to growing global debt sustainability issues, with the net result being lower-than expected debt ratios and therefore lower term premia as the perceived credit risk is lower. In turn, this reinforces the role of sovereign debt as a safe haven asset.

Sovereign bond implications and regional considerations

Whether AI has the ability to command these benefits is too early to be determined. Even if AI’s ability to flatten yield curves is clear, the transition phase is likely to be uneven. Initial capital expenditure (capex) surges and supply-chain bottlenecks could create short-term inflationary impulses before productivity gains materialise. While a sustained productivity uplift could flatten curves as outlined above, cyclical volatility in adoption phases may steepen curves temporarily.

Additionally, regional considerations are important. Some economies have demonstrated better efficiency at implementing new technologies and harnessing productivity boosts, thus curve flattening benefits could accrue unevenly across regions.

- US: The US has historically demonstrated an ability to rapidly adopt new technologies, reallocate capital efficiently, and translate innovation into productivity gains. This puts the US in a strong position to benefit from the flattening yield curve AI gains described above. However elevated fiscal deficits, potential fiscal expansion and the expected large capex cycle could pressure yield curves in the short term.

- Europe: Europe has experienced persistent productivity underperformance since the global financial crisis due to structural rigidities in labour markets, lower technology investment, and regulatory complexity. AI adoption could offer a much‑needed productivity uplift, but the pace is likely to be uneven across countries. Europe also risks having AI‑driven productivity gains that are not sufficient to materially improve debt trajectories, thereby limiting the extent of curve flattening in the short term. Investors should watch for decisive structural reform to determine if Europe’s productivity trend is to improve.

- Japan: High public debt, an aging demographic and strengths in manufacturing makes Japan a strong candidate for outsized AI-related gains. However, Japan, like Europe, has faced long-term productivity challenges, suggesting productivity gains could take time to materialise.

- Emerging markets: The potential for AI productivity boosts across emerging markets remains high but very heterogeneous. A wide dispersion of institutional quality, fiscal starting points, demographics and the ability to integrate into the global supply chains means there are likely to be many winners and losers. Investors should focus on economies that are able to improve digital infrastructure, introduce appropriate AI policies and correctly monetise AI gains (i.e. improve tax collection).

AI’s effects on sovereign curves, while profound, are likely to be uneven, dispersed and evolving. For sovereign bond investors, this dynamic introduces uncertainty around neutral rate (r*)[1] and term premia considerations. The timing and magnitude of AI-driven growth matters. If adoption lags or fiscal multipliers disappoint, debt dynamics could remain challenging, compromising curve flattening effects.

Additionally, country selection, curve positioning, and duration management are increasingly important

Emerging markets (EM)

AI’s impact on EM fixed income is poised to be highly differentiated, reflecting the uneven pace of adoption and integration across countries.

Those EM economies that successfully embed themselves in the AI value chain, whether through data centre buildouts, semiconductor manufacturing, or digital infrastructure, are likely to experience stronger fundamentals, improved credit profiles, and enhanced market access. This integration can attract capital inflows, compress spreads, and support sovereign and corporate issuers in the short term. However, this also introduces a new layer of dependency: countries that become overly reliant on AI-driven sectors may face heightened volatility if global AI investment cycles slow or if technological shifts render certain assets obsolete.

Conversely, EM countries unable to participate meaningfully in the AI build-out risk being left behind, facing slower growth and potential crowding-out as capital gravitates toward AI-linked opportunities.

For fixed income investors, this means that country selection and sector allocation will become even more critical, with a premium placed on adaptability and rigorous due diligence as AI adoption is only likely to widen the divergence across the EM universe.

The income and credit investor – A spread tightener?

Credit markets are set to be transformed by AI, the impacts of which manifest in a number of ways across sectors.

Corporate bonds

We have begun to see a significant increase in capex on data centres, energy and cooling systems and specialised semiconductor processors by the big tech hyperscalers, a trend expected to continue in the near future. The strong cash flow generation of hyperscalers in recent years has meant that, so far, cash flows have outpaced their AI capex needs. However, a spike in net supply for in the latter part of 2025, largely attributable to AI capex, indicates that this might be changing.

A short-term challenge for investors will be how to absorb new supply of debt. A recent Goldman Sachs survey found that 70% of corporate issuers expect more than US$500bn worth of AI-related corporate bond issuance over the course of 2026. By way of comparison, 2025 saw roughly US$200bn of such issuance, which was already more than double the prior year’s level.

Increased issuance offers more investment opportunities for investors at the forefront of AI infrastructure but also presents risks of technical headwinds on spread levels of new supply as well as higher leverage and pressure on cash flow margins.

For companies, AI is a major disruptor to existing business models that is set to create both winners and losers. On the one hand, AI adoption has the potential to transform company margins and productivity. However, as the market is capitalgroup.com 6 starting to test, AI agents could also have serious implications for the viability of some business models.

Software application companies have been the first to face this challenge with companies in the sector seeing an aggressive rerating of their equity following the launch of powerful AI models such as Anthropic’s Claude.

While exposure to software-related issuance in both investment grade and high yield corporate bond markets remains low, other sectors of credit, such as leveraged loans, Collateralised Loan Obligations (CLOs) and private credit, have demonstrated higher exposures to these areas, which warrant monitoring.

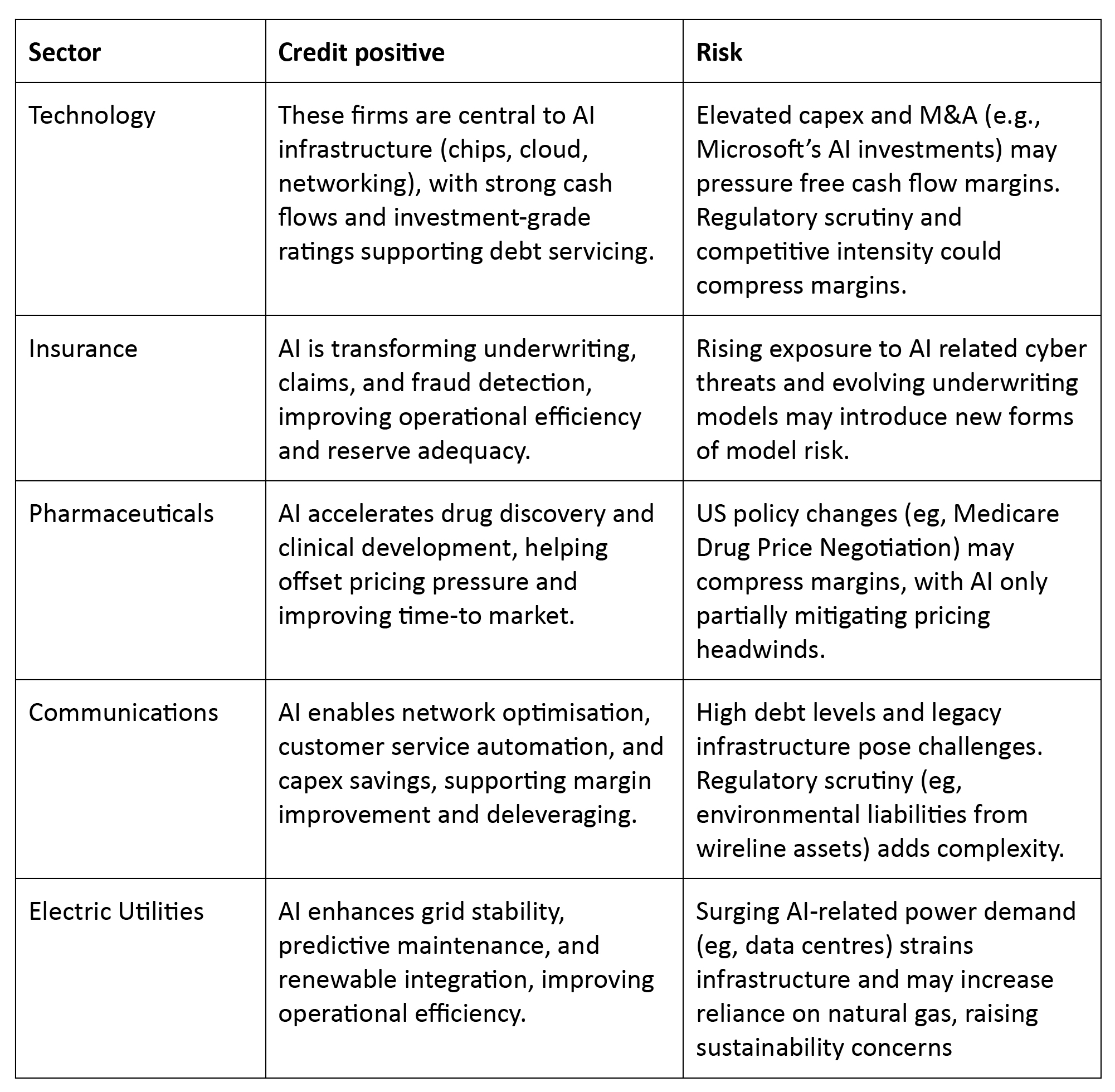

The following table highlights some of the emerging themes we have already identified across key sectors.

A sector level insight into AI

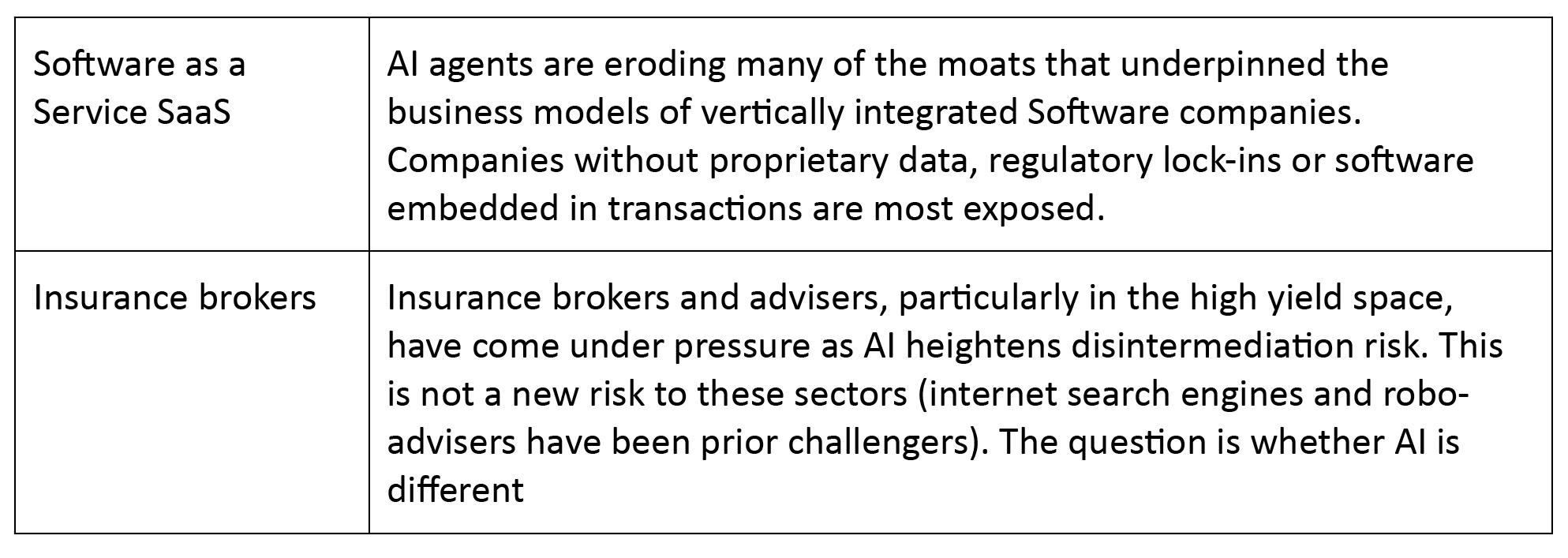

And some industries already on the AIO frontline

Selection remains critical in corporate bond markets. Not just deciding between sectors, but also the companies within sectors that can better harness the benefits of AI in their business models.

Securitised markets

If the trend to finance AI infrastructure continues to transition from equity or cash-funded models to debt-funded strategies, this could also affect securitised markets. Capital Group expects strong issuance of both Digital Infrastructure Asset Backed Securities (ABS), incorporating both data centre and fibre ABS, and data centre-backed commercial mortgage-backed securities (CMBS) over the coming few years. This trend points to important considerations to watch in securitised markets that present both opportunities and challenges.

As a starting point, an expanded securitised bond market provides investors with a broader and more diversified investment universe from traditional securitised pools, which are typically driven by consumer revenue (credit card, student loan, auto loan, residential mortgages) or commercial real estate revenue (retail, hospitality, office).

New pools backed by AI-related mission-critical assets like data centres and fibre infrastructure act as a nice complement to existing opportunities for investors. The structures also provide another stream for investors to access the AI revolution more directly and, given their essential role in AI workloads, should broadly be seen as resilient in a world where the prominence of AI is justified.

However new structures also present challenges and risk. Any general hesitation on the adoption of AI could quickly make these assets obsolete, and their success becomes heavily tied to the direction of the AI trend. Additionally, the new structures introduce complexity in risk assessment, requiring advanced analytics and dynamic management to understand the risks. Finally, similar to the corporate bond space, the level of issuance is yet to be determined, and this could cause volatility from a technical perspective.

Ultimately, for securitised credit investors, the investment landscape is set to offer a wider range of opportunities in the years ahead; however, capturing value will depend on a commitment to thorough due diligence, careful examination of collateral, and the ability to adapt to shifting benchmarks and liquidity environments. As an example in the case of data centre ABS, proximity to regional hubs to reduce latency and energy costs are key considerations to determine not only the effectiveness of a digital asset, but also its reusability if it needs to be recommissioned to a non-AI purpose.

The Active Bond Manager

Investment research

Alongside the investment implications outlined above, AI is rapidly transforming the landscape of active fixed income investment management by empowering professionals with advanced tools for synthesising and summarising large, fragmented data sets.

This capability allows managers to efficiently process vast amounts of information from diverse sources, such as central bank judgments, economic data releases, company earnings announcements and policy documents. Additionally, AI tools can assist in producing cash flow analyses and forecasts more efficiently. In the not-too-distant future, AI could potentially be an important tool used in risk management, anticipating market movements and identifying emerging risks with greater precision.

However, as AI tools become more accessible and widely adopted, there is a growing risk of proliferation of commoditized insights, which we believe increases the value of fundamental, proprietary, and individualised research.

For instance, understanding policy makers’ objectives becomes vital in anticipating future moves of central banks, while understanding the true risk of a corporate’s ability to pay back its obligations requires a close understanding of the company’s future prospects and direction of travel. Some of these insights can only be gleaned from experience with these institutions and direct engagement with policy makers and company management. As such, active managers who combine AI-powered analytics with unique qualitative insights can better understand risk and generate enhanced returns.

Trading and execution

While there have been significant developments in the world of bond trading over the last few decades, the majority of the fixed income world remains a largely over-the-counter (OTC) market. This is partly due to the sheer breadth and depth of markets (over 30,000 issues in the Bloomberg Global Aggregate Bond Index), and the relatively short life-span of bonds.

These factors contribute to issues with price discovery, liquidity and timely execution, issues that are exacerbated by increasing dealer balance-sheet constraints since the GFC and, more recently, the prominence of private credit.

By accelerating price discovery through alternative data and predictive analytics, AI could enable market participants to identify opportunities and risks with greater speed and precision.

Algorithmic strategies powered by AI can also play a significant role in concentrating trading flows, which can amplify both liquidity and volatility, especially during periods of heavy issuance or market stress.

For investors, understanding these evolving liquidity regimes and transaction cost dynamics is critical for effective execution and risk budgeting in an AI augmented fixed income landscape. We believe to maintain an edge in fixed income amid these developments, dedicated and experienced trading capabilities able to harness these tools are vitally important.

Conclusion

AI’s influence on fixed income markets is only just beginning. Its eventual effects will become more apparent as time progresses. Even at this point, however, certain conclusions can already be reached.

Our analysis suggests that, over time, productivity gains from AI could lead to flatter yield curves, but in the interim, uncertainty, increased spending and heavy government debt burdens are likely to add steepening pressure to curves. The impact on credit markets will be diverse, shaped by issuance, business models and levels of AI adoption.

For investment management, differentiated research and dedicated trading capabilities will likely become increasingly important for success.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Fixed Interest (0.25 hrs) and Managed Investments (0.25 hrs)

please log in to start this quiz

———

References:

[1] The neutral real interest rate (r*) is the real short-term rate consistent with an economy operating at full employment and stable inflation, such that monetary policy is neither expansionary nor contractionary and the economy is in long-run equilibrium.

Statements attributed to an individual represent the opinions of that individual as of the date published and may not necessarily reflect the view of Capital Group or its affiliates. This communication is intended for the internal and confidential use of the recipient and not for onward transmission to any other third party. This communication is of a general nature, and not intended to provide investment, tax or other advice, or to be a solicitation to buy or sell any securities. All information is as at the date indicated and attributed to Capital Group unless otherwise stated. While Capital Group uses reasonable efforts to obtain information from third-party sources that it believes to be accurate, this cannot be guaranteed. In Australia, this communication is issued by Capital Group Investment Management Limited (ACN 164 174 501AFSL No. 443 118), a member of Capital Group, located at Suite 4201, Level 42 Gateway, 1 Macquarie Place, Sydney, NSW 2000 Australia. All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company. All other company names mentioned are the property of their respective companies. © 2026 Capital Group. All rights reserved.

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Fixed Interest (0.25 hrs) and Managed Investments (0.25 hrs)

please log in to start this quiz———