As SpaceX prepares for world’s largest IPO, investors should not overlook the June rebalance of the Russell 1000 Growth and Value Indexes, which will materially reshape exposures, especially among mega caps, says ClearBridge Investments.

Amazon, Apple and Microsoft are among the most notable shifts toward value, while Nvidia and Alphabet remain concentrated in growth.

“The rebalance will also drive meaningful sector and industry changes, most notably among semiconductor stocks, with elevated turnover across portfolios,” Elisa Mazen, ClearBridge portfolio manager says.

“As a result of these changes, trading activity within strategies tied to these two large cap indexes is expected to be higher than normal.”

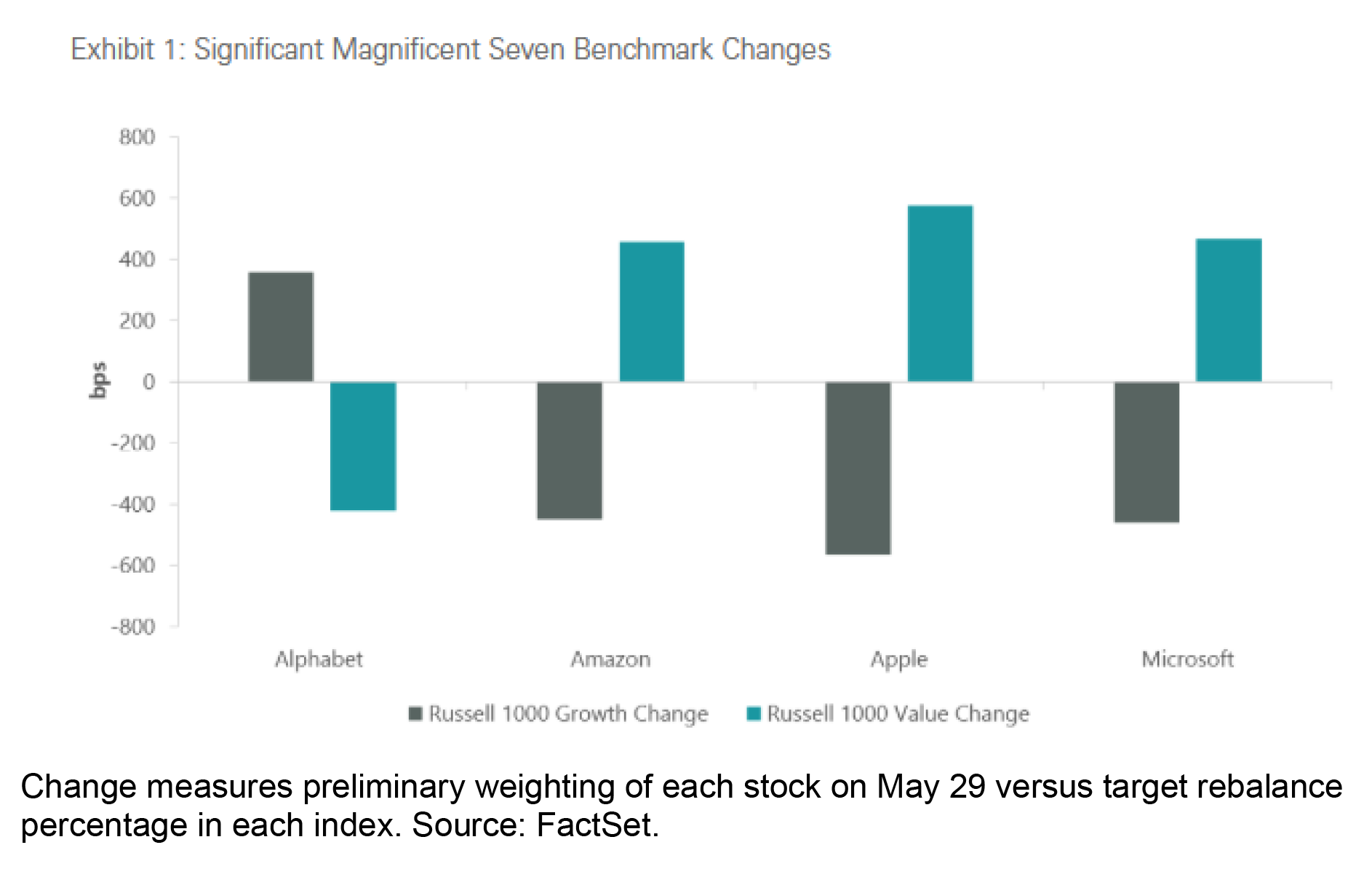

Much of the market’s attention has focused on the Magnificent Seven, where the benchmark shifts are substantial, particularly for Amazon.com. Based on preliminary projections1 through the end of May, these bellwether mega caps will see their collective weighting decline ~11.6 percentage points in the Russell 1000 Growth Index (RLG) while simultaneously gaining ~ 10.7 percentage points in the Russell 1000 Value Index (RLV).

These reclassifications will immediately impact active strategies’ weightings relative to their growth and value benchmarks.

Sector-level changes based on preliminary May 29 pricing are also expected to be meaningful. Within the RLG, overall information technology (IT) exposure changes modestly, but on the subsector level semiconductors will increase to 35.9%, led by the additions of KLA Corp. which will become the third-largest stock in the index and Micron Technology, while the software subsector will decline by 5.5%.

Additionally, communication services will increase by 3.6%, while consumer discretionary will decline by 4.9%.

Within the RLV, consumer discretionary will increase by 4.4% and IT by 2.2%, while communication services will decline by 4.6%.

Industrials and IT are expected to experience the largest net outflows as a result of the rebalance.

Mazen adds, “Turnover will likely increase in the near term as large cap portfolios adjust to the new index compositions, but this is not unique to ClearBridge. These dynamics are expected to affect both active and passive managers broadly across both growth and value mandates.”