Investment markets and key developments over the past week

- Global shares had a mixed week as investors digested the 5% or so rebound since early February amidst weather affected US data, signs the Fed will soon change its forward interest rate guidance with respect to unemployment, another fall in a Chinese manufacturing conditions PMI and as turmoil continued in the Ukraine and Thailand providing a reminder that issues remain in the emerging world. While US and Eurozone shares were basically flat, Japanese and Asian shares nevertheless saw good gains. Bond yields were also little changed, but commodity prices did see some strength with a strong rise in oil prices (partly due to poor US weather) and higher metal prices. The $A fell on the poor news from China, but only marginally.

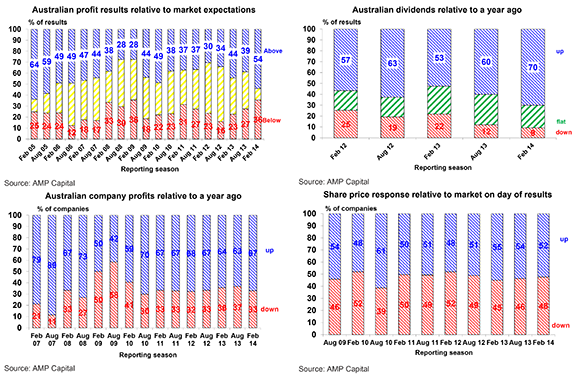

- Australian shares continue their sprint higher gaining more than 7% from their early February low with mostly good earnings results over the last few weeks providing confidence that the long hoped for rebound in earnings is finally happening and as shareholders like the news of higher dividends.

- The minutes from the Fed’s last meeting point to ongoing tapering. Cleary the Fed viewed the recent run of soft US data as largely due to poor weather, which along with comments by various Fed officials suggest little change in the pace of tapering. Of course this could change in a few months if US data has still not improved. The Fed does appear to likely soon change its forwards guidance on interest rates with the unemployment approaching the Fed’s 6.5% threshold, but at this stage there appears to be little agreement on what form the new guidance will take. Looking further out, while markets may have become a bit concerned about the reference to “a few participants” raising the possibility that it may need to raise interest rates relatively soon, this is likely to refer to the usual hawkish regional presidents of Fisher, Plosser, Lacker and George and is likely to be of little consequence for now given they don’t drive Fed policy. That said, once the US exits its weather related soft patch and as the Fed nears the end of its QE program later this year, talk of sooner than expected interest rate hikes may start intensifying…maybe later this year.

Major global economic events and implications

- US economic data presents a confusing picture at present. Freezenomics clearly played a role in depressing the NAHB home builders’ survey (along with a lack of supply), housing starts and manufacturing conditions in the New York and Philadelphia regions. But against this the broad-based Markit manufacturing conditions PMI rose 3 points to a very solid 56.7 in February with strong gains in new orders and employment suggesting the overall manufacturing sector is in good shape and on top of this jobless claims fell and the leading index rose pointing to solid growth ahead. On top of all this inflation readings remain benign, with core and headline inflation of just 1.6% year on year. So beyond the freeze the US economy still looks ok.

- Eurozone flash PMIs slipped in February but only marginally (from 52.9 to 52.7 for the composite) and do nothing to change the outlook for continued gradual economic recovery. That said growth is still not strong enough to reduce deflation risks, so more ECB easing is still likely.

- Japanese December quarter GDP growth was much weaker than expected at just 0.3%, but this was due to a surge in imports as growth in domestic demand was a solid 0.8% driven by consumption and investment. As expected the Bank of Japan made no changes to its asset purchase program or its money supply targets but it did extent or expand various measures to boost bank lending, which could be interpreted as a baby step towards further easing which we expect to see in the next few months.

- China’s flash HSBC manufacturing PMI fell yet again in February pointing to the possibility of a further slowing in economic growth. That said it could have been distorted by the Lunar New Year holiday and pollution related factory suspensions and it’s still bouncing up and down in the same range it’s been in for the last two years, which period has seen GDP growth stuck in a range around 7.5% to 8%. So at this stage we see no reason to change our 2014 growth forecast of 7.5%.

Australian economic events and implications

- In Australia, a fall in annual wages growth to a record low of 2.6% through 2013 provides further confirmation that the labour market is very weak and means that poor household income growth will remain a constraint on consumer spending. Fortunately it also adds to confidence that inflation will remain low thanks to soft growth in wages costs and so adds to confidence the RBA can keep interest rates down. There is also a bit of light at the end of the tunnel for the labour market with skilled vacancies rising for the fifth month in a row in January

- The minutes from the RBA’s last meeting provided nothing new but by dropping any reference to the possibility of further easing, they confirmed that its bias on interest rates is now neutral. We remain of the view that the RBA will keep interest rates on hold out to around September with gradual rates hikes thereafter.

- The corporate earnings news was a bit more mixed over the last week. As is often the case the companies with great results often go first followed by those not doing so well. That said, with around 70% of companies having reported, overall results remain pretty good and confirm the profit cycle has now turned up. So far 54% of companies have exceeded expectations (compared to a norm of 43%); 67% of companies have seen their profits rise from a year ago (compared to a norm of 66%); 70% of companies have increased their dividends from a year ago (compared to an average of around 62% in the last two years); but only 52% of companies have seen their share price outperform the day they released results. Key themes are a massive turnaround for the resources stocks (notably Rio and BHP) leaving the sector on track for circa 35% earnings growth this financial year, banks doing very well (with good results from CBA, ANZ and NAB), help coming through from the lower $A, ongoing cost control, signs of improvement from some cyclicals (like Boral, JB Hi Fi, Fairfax and Seek) and strong growth in dividends. The surge in dividends – which are up about 15% from a year ago – is a good sign that companies are confident about the outlook. The bottom line is that Australian earnings look to be on track for growth of around 15% this financial year, with a 35% surge in resources’ profits, a 10% rise in financials’ profits and a 6% rise in profits for the rest of the market.

- In the US, house price data (due Tuesday) for December is expected to show continued strength but poor weather is likely to have weighed on January new home sales (Wednesday) and possibly consumer sentiment (Friday). Poor weather could also give a subdued result in durable goods orders (Thursday) and December quarter GDP growth is likely to be revised down to 2.5% annualised from the 3.2% initially reported thanks to softer trade and retail sales data than had originally been allowed for. Fed Chair Yellen’s delayed Senate testimony (Thursday) will be watched closely for any hint of a taper slowing following recent mixed data.

What to watch over the next week?

- In the Eurozone, confidence data (Thursday) is likely to confirm the continuing gradual economic recovery. Unfortunately the recovery to date is unlikely to have been strong enough to have pushed the January unemployment rate (Friday) below the 12% level.

- Japanese January data for household spending, the labour market and industrial production are likely to show continued growth, and a continuing rising trend in inflation (all due Friday).

- The official Chinese manufacturing PMI (Friday) is likely to have followed the HSBC flash PMI slightly weaker.

- In Australia, December quarter construction (Wednesday) and business investment data (Thursday) will provide important building blocks for the December quarter GDP data to be released on March 5. Both are likely to be a bit softer than was the case in the September quarter. The capex data will also provide a guide as to how quickly mining investment is slowing and whether non-mining investment is picking up. Private credit growth (Friday) is likely to have shown a continuing modest pick-up in growth. A speech by RBA Governor Glen Stevens (Wednesday) will likely reiterate the case for interest rates to remain on hold for now.

- This will be the final week of the Australian December half 2013 earnings reporting season with 60 major companies due to report, including Worley Parsons, Harvey Norman and Woolworths.

- Investment markets will also digest the outcome of the G20 finance ministers meeting to be held on February 22-23. G20 meetings are a great opportunity for a talkfest – and this one will see lots of interesting discussion around issues such as the impact of Fed tapering on emerging countries, global growth targets, boosting infrastructure investment, financial regulation and tax base erosion – but in the absence of a global crisis to fix, it’s hard to see it having much impact on financial markets. While ongoing concerns from some emerging markets about the Fed’s tapering of its stimulus program create interest, there’s virtually zero chance that the Fed will do anything differently and nor should it as it has to do the right thing by the US economy and emerging market problems are largely of their own making. And it can hardly be claimed that the Fed failed to communicate its plans to start tapering – in fact then Fed Chair Bernanke started flagging his tapering plans back in May last year, nearly six months before the Fed started doing anything.

Outlook for markets

- While returns will be more constrained and volatile, shares will nevertheless push higher this year helped by reasonable valuations, improving earnings on the back of improved economic growth and easy monetary conditions helping to entice investors to switch out of cash and bonds and into shares. With the current earnings reporting season pointing to solid earnings growth this year, the ASX 200 is on track to meet our year-end target of around 5800 by year end.

- The recent decline in global bond yields should be seen as a correction against the backdrop of a slow rising trend in yields on the back of gradually improving global growth. This will mean subdued returns from government bonds. Cash and bank deposits also continue to offer pretty poor returns given low interest rates/yields.

- The broad trend in the $A remains down on the back of softer commodity prices, a reversion to levels that offset Australia’s relatively high cost base and a decline in Australia’s growth relative to that in the US. However, short positions in the $A still remain excessive and so it could still have a bit more of a bounce before the downtrend resumes.

By Dr Shane Oliver, Head of Investment Strategy & Chief Economist

———-