Key points

- While the global economy is looking better than it has for years, relatively low investment yields from most major asset classes mean the medium term return outlook remains constrained compared to the long term bull market in shares and bonds that started in the 1980s. For example, 7.5 to 8% pa for a diversified mix of assets, not double digits.

- For investors the implications are: have realistic return expectations; asset allocation remains critical; focus on assets providing decent and sustainable income flows. Australian shares still remain attractive for income flows but for growth Asian ex-Japan shares come out best.

Introduction

Most investment analysis and commentary is focused on the here and now and the implications for investment markets just a little bit ahead. But getting a handle on the return potential for major asset classes over the medium term, ie the next five years or so, is of value from several perspectives. First, such return projections are a critical driver of the strategic asset allocation (SAA) to each asset class (shares, bonds, property, etc) within traditional diversified investment funds.

Second, and more fundamentally, it gives a great guide to return potential between asset classes, which helps inform asset allocation generally. For example we use medium term return projections as part of our Dynamic Asset Allocation process.

Finally, it can help provide a guide to what sort of returns investors can expect beyond the short term. After a couple of years of double digit returns from shares and balanced growth superannuation funds there may be a temptation to assume we have now returned to a world of ongoing double digit returns. But this could be mistaken if it’s not sustainable.

This note takes a look at the medium term return potential for major asset classes and what that means for investors.

Getting a handle on return potential

The first thing to note is that simply taking a long term average of historical returns for each asset class and using that as a guide may be use, but often offers little guide to their medium term outlook given the significant impact of starting point valuations (eg, if current yields are significantly lower than normal then this will constrain returns relative to any long term norm) and the broad economic environment. Another approach may be to come up with a bunch of themes and start from there. But without a framework in which to place them this can simply lead to a muddle.

So our approach is to go back to basics, recognising firstly that the components of the return flowing from an asset are the yield (or income flow) it provides and capital growth and secondly that the starting point yield is key, ie, the higher the better. Then apply themes around this where relevant. We also prefer to avoid a reliance on forecasting and to keep the analysis as simple as possible. Complicated adjustments can lead to compounding forecasting errors without any value in terms of the broad message.

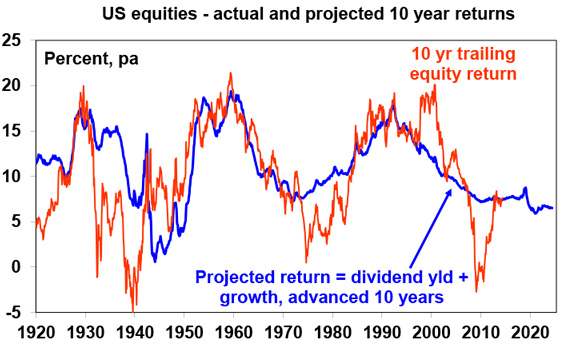

- For equities, a simple model of current dividend yields plus trend nominal GDP growth (as a proxy for earnings and capital growth) does a good job of predicting medium term returns. This approach allows for current valuations (which are picked up via the yield) but avoids getting too complicated.[1] The next chart shows this approach applied to US equities, where it can be seen to broadly track big secular swings in returns.

Source: Thomson Reuters, Global Financial Data, AMP Capital

- For property, we use current rental yields and likely trend inflation as a proxy for rental and capital growth.

- For unlisted infrastructure, we use current average yields and capital growth just ahead of inflation.

- For bonds, the best predictor of future medium term returns is the current five year bond yield. In other words capital growth is zero because if a five year bond is held to maturity its initial yield will be its return.

Medium term return projections

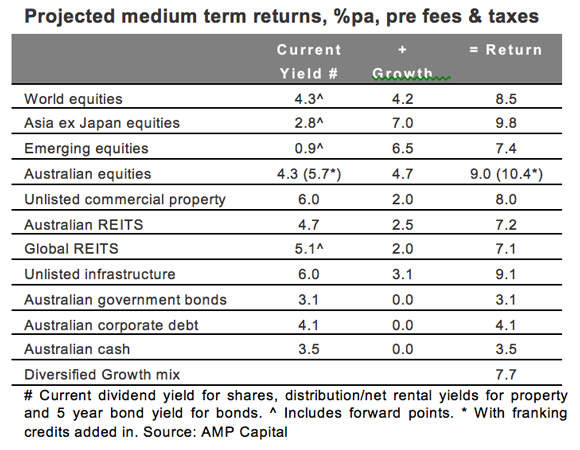

This framework results in the return projections shown in the next table. The second column shows each asset’s current income yield, the third their five year growth potential and the final column their total return potential. Note that:

- We assume central banks meet their inflation targets over time, eg, 2.5% in Australia and 2% in the US.

- We allow for forward points in the return projections for global assets based around current market pricing – which adds 1.8% to the return from world equities (Australian interest rates above that in other advanced countries) but detracts 1.9% from emerging equities.

- The Australian cash rate is assumed to average 3.5% over the next five years. This is one asset where the current yield is of no value in assessing the asset’s medium term return potential because the maturity is so short. So we assume a medium term average. Normally, for cash this would be around a country’s medium term nominal growth rate, but we have made an allowance to adjust for higher than normal bank lending rate margins over the cash rate and higher debt to income ratios which have increased the interest sensitivity of households, and in turn pulled down the neutral cash rate.

- The Australian equity return adjusted for franking credits (that adds about 1.4% pa) is shown in brackets.

Thematics

Several themes have been reflected in these projections:

- Low inflation – while inflation worries abound reflecting the quantitative easing programs of the last few years, this is likely to be offset by continued global excess savings and spare capacity along with central banks being mandated to meet inflation targets.

- Aging populations – resulting in slower labour force growth than seen over the last twenty or so years and a demand for yield bearing assets with less focus on capital growth.

- Slower household debt accumulation – the surge in household debt growth seen in the decades prior to the GFC looks to have run its course with tougher bank lending standards and more cautious consumer attitudes.

- The commodity super cycle has turned down – on the back of slower growth in China and increased commodity supply. This will act as a constraint on growth for some emerging markets (eg South America) but benefits commodity user regions (such as Asia, Europe and Japan). It also means the terms of trade has gone from a tailwind for Australian growth and profits to a headwind. To allow for this we have reduced nominal capital growth potential by 0.5% pa for Australian shares.

- Technological innovation – with its intensified focus on labour saving (eg robotics, 3D printing) it is likely good for productivity and corporate margins but ambiguous for consumer spending.

- Reinvigorated advanced countries versus emerging markets – while the emerging world still has a higher growth potential (reflecting its lower starting point) it’s likely to be slower over the decade ahead than last decade reflecting a slowdown in economic reforms but at the same time the US, Europe and Japan appear to be reinvigorating themselves after a tough decade (or two in the case of Japan).

- A multi-polar world – the end of the cold war and the stabilising influence of the US as the dominant power helped drive globalisation and the peace dividend post 1990. Now China’s rise and Russia’s retreat are arguably resulting in a more difficult environment geo-politically.

- Backtracking on free markets in parts of the world – a greater scepticism of unfettered markets and increased focus on regulation post the GFC.

Most of these will likely have the effect of constraining returns. But not universally so. Technological innovation remains positive for profits and the renaissance in the US, Europe and Japan is very positive.

Observations

Several observations flow from these projections.

- While advanced countries may have exited a secular bear market, return potential is still constrained. The starting point for returns today is less favourable than when long term bull markets started in bonds and equities in 1982 (with much lower investment yields today) & the thematic backdrop is less favourable. Our medium term return projections imply a 7.7% pa return from a diversified mix of assets. This is well below the 11.9% pa return Australian super funds saw over the 1982-2007 period which was underpinned by the combination of high starting point investment yields and very favourable investment thematics with the shift from high to low inflation, deregulation, easy credit, globalisation, the peace dividend, the IT revolution, favourable demographics and finally for Australia a surge in commodity prices.

- Sovereign bonds offer low return potential – after a thirty year secular decline in bond yields the combination of very low yields and the risk they will rise resulting in capital loss implies low medium term return potential.

- Unlisted commercial property & infrastructure continue to come out well reflecting their relatively high yields – but don’t forget their illiquidity.

- Australian shares stack up well on the basis of yield, but it is hard to beat Asian ex-Japan shares for growth potential and traditional global shares offer improved prospects.

Implications for investors

There are several implications for investors:

- First, have reasonable return expectations. The world is in far better shape today than at any time since the GFC but don’t expect year after year of double digit returns.

- Second, asset allocation remains critical reflecting: the relatively constrained medium term return potential; a likely wide range in returns between major asset classes; continued bouts of volatility (eg as extreme monetary policy conditions in the US and elsewhere are eventually unwound); and as the correlation between bonds and equities remains low (in the absence of a common driver like falling inflation provided in the 1980s and 1990s).

- Third, there is still a case for a bias towards Australian shares, particularly for yield focused investors, but with traditional global shares looking a bit healthier after a long tough patch have a bit more offshore. Asian ex-Japan shares are preferred relative to emerging market shares generally.

- Fourth, focus on assets providing decent sustainable income as it provides confidence regarding returns. Commercial property, infrastructure, quality yield shares and investment grade credit stack up well here.

Dr Shane Oliver, Head of Investment Strategy and Chief Economist AMP Capital

——–

[1] For example, adjustments can be made for: dividend payout ratios (but history shows that retained earnings often don’t lead to higher returns at the country level so the dividend yield is the best guide); the potential for PEs to move to some equilibrium level over time (but this relies on forecasting the equilibrium PE correctly which can be hard and in any case extreme dividend yields send a strong enough valuation signal anyway); and adjusting the earnings/capital growth assumption for some assessment regarding profit margins (but again this has been shown to be very hard to get right at the country level, eg US profit margins have been strengthening for decades and it’s hard to see what will turn this around). So we prefer to keep any reliance on forecasts to a minimum and to keep it simple.