Investment markets and key developments over the past week

The past week was mixed for shares with Eurozone shares up on good economic data and expectations for further ECB easing, Japanese and US shares basically flat and Chinese and Australian shares down with Australian materials stocks under pressure again. Turkey’s downing of a Russian fighter jet caused some angst but it was quickly forgotten about by investors. Bond yields fell but oil and metal prices managed very modest gains and the $A fell fractionally as the $US rose marginally.

The downing by Turkey of a Soviet era Su-24 Russian fighter jet (that may not have even known it had crossed the exact border into Turkey), provides a reminder of the risk of conflict between foreign powers in the seemingly free for all shootout that has become Syria, but it’s not going to trigger WW3 or anything close. Sure, it’s something new for investors to worry about, but its best put in the geopolitical furphies basket. Russia will continue with its war of words and may impose some token sanctions on Turkey, but is not going to get into a war with NATO and its options economically are limited because Turkey takes 13% of its gas exports and has the ability to disrupt or stop 35% of its oil exports. Rather the rest of NATO will try and calm Turkey down as it focuses on trying to build a more coordinated attack on it and Russia’s common enemy, IS. So far so good with France and Russia agreeing to coordinate their attacks on IS in Syria.

Business friendly Mauricio Macri’s election as Argentina’s President is a positive sign potentially signalling that the tide may be turning against populist policies that have helped put it and some other emerging countries into a mess. But it’s not a green light (yet) to invest in Argentina/EMs: sensible economic reforms will likely see Argentina’s economy and peso worsen before they get better, populists still control the Senate and are likely to slow or stall reformist legislation and other EMs like Brazil are a long way behind Argentina. So a good sign, but too early to get too excited.

It’s almost certain that on Monday the IMF will include the Renminbi in its basket of Special Drawing Right currencies). While its inclusion as an SDR currency won’t have a major direct impact on global financial markets or Chinese economic prospects it will provide a huge symbolic boost for the Renminbi – encouraging its use as a reserve currency and as currency for use in trade.

Looks like the Australian Treasury is now following the RBA in revising its estimate of Australia’s potential growth rate to around 2.75%, largely on the back of slower population growth. This is an old story really as we have been using lower potential growth in Australia for the last few years. It will have the effect of further slowing the projected return to a budget surplus though with some estimates putting the hit to the budget from each 0.25% reduction in growth at $5bn pa.

Political momentum appears to be building to look at limiting some tax concessions, including in relation to superannuation. Putting aside the specific merit of such changes, it is very important that they be considered in the context of the whole tax system. Even with the various tax concessions the Australian income tax system is highly progressive compared to other comparable countries (see The Australian Government’s Tax Discussion Paper, page 30). Our marginal tax rates are relatively high (eg the top MTR is 49% versus 33% in NZ and 20% in Singapore) and despite the tax concessions this is leading to just 17% of tax payers paying a high 63% of income tax revenue raised by Canberra (based on 2011-12 data). Limiting tax concessions without reducing marginal tax rates and/or increasing the income thresholds will only see this burden increased further, which in turn will reduce work incentive and reduce the size of the economic pie making it even harder to sustain government services and social safety nets. Fortunately the Government appears to recognise this.

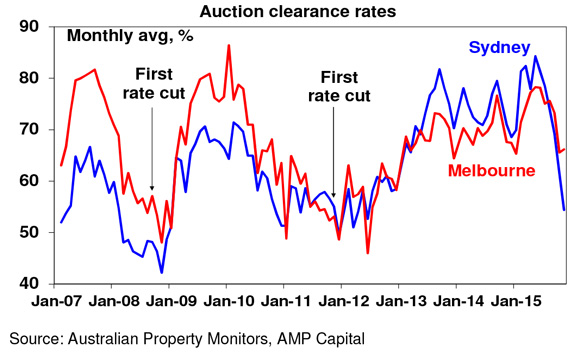

With a Super Saturday on the way for auction listings this weekend, the recent fall in clearance rates suggests there could be disappointment in Sydney where clearances have plunged to 2011-12 cycle lows. Melbourne is a bit stronger.

Major global economic events and implications

US data was mostly solid with strong durable goods orders, trade data, new home sales and service sector conditions, falling unemployment claims, rising home prices and an upwards revision to September quarter GDP growth. But it’s not universally so with weakness in existing home sales, manufacturing conditions, consumer confidence and consumer spending and the core private consumption deflator remaining stuck well below the Fed’s target at 1.3% year on year. The overall flow of data supports the case for a December Fed rate hike but the moderate nature of growth along with continued sub-target inflation suggests that the Fed will continue to stress that future rate hikes will be gradual.

Eurozone business conditions PMIs rose further in November and October money supply and lending accelerated pointing to an improvement in growth ahead.

In Japan, household spending remains weak and core inflation fell back to 0.7% year on year, but some indicators are looking quite good with a further rise in the manufacturing PMI, the job to applicant ratio remaining at its highest since 1992 and the unemployment rate falling to its lowest since 1995. PM Abe’s plan to increase minimum wages by 3% pa for several years could further help end deflation expectations.

Australian economic events and implications

Australian construction and capital spending data for the September quarter were very weak as mining investment continues to fall back to earth and non-mining investment remains poor. Capex plans remain over 20% down on expectations from a year ago, with this mainly due to slumping mining investment but the outlook for non-mining investment also remains soft. So while the economy has been successfully rebalancing away from reliance on mining for growth, we are still waiting for the final piece of the puzzle, ie a pickup in non-mining investment, to fall into place. As such, the economy looks like it might still need a bit more help in the form of lower interest rates and a further fall in the value of the $A.

What to watch over the next week?

In the US, the main focus will be on the jobs data (Friday) as a guide to whether the stronger jobs growth and wages pick up seen in October continued. These will take on added significance because they will be the last jobs figures before the Fed considers raising interest rates in mid-December. Congressional testimony by Fed Chair Yellen (on Wednesday and Thursday) is expected to reinforce expectations for a rate rise before year end and that subsequent rate rises will be gradual. Expect payrolls to show a 200,000 gain with wages growth rising to 2.3% year on year. In terms of other data, expect pending home sales (Monday) to rise 2%, the ISM manufacturing conditions index (Tuesday) to improve slightly from the 50.1 reading seen last month and the ISM non-manufacturing conditions index (Thursday) to remain strong.

Financial markets will also be focussed on the ECB (Thursday) which is expected to announce further monetary easing. This is likely to take the form of an expansion of its quantitative easing program and another 0.10% reduction in its deposit rate taking it to -0.3%, all designed to pump more cash into the Eurozone economy and encourage banks to lend it out with the aim of ensuring inflation will head higher. However, such a move is not assured as not all ECB officials are in favour and there is risk that the ECB will simply indicate an ongoing bias to ease more. Eurozone inflation data for November (Wednesday) is expected to show that inflation remains well below target.

In Australia, the RBA is expected to leave interest rates on hold again (Tuesday). The RBA has an easing bias with Governor Steven’s indicating “I’m more than happy to lower [the cash rate] if that actually helps” but for now seems content to “chill out and see what the data says.” September quarter capex data was clearly poor but given the strong October jobs report and signs of better September quarter GDP growth, the capex data is unlikely to have been enough to move the RBA’s dial towards another cut just yet. Nevertheless, the RBA is likely to reiterate that the benign inflation outlook provides scope to ease if necessary and I lean to the view that further help for the economy will still be needed in the form of another easing at some point as the boost to growth from the housing sector runs its course and non-mining investment remains poor.

A data avalanche in Australia will start Monday with October credit data expected to show a further slowing in investment loans. Tuesday’s September quarter trade data are expected to show a strong 1.2 percentage point contribution to GDP growth but public spending data is likely to show a fall, building approvals are likely to show further signs of having peaked and Core Logic/RP Data figures for home prices may show price falls in Sydney. September quarter national accounts (Wednesday) are expected to show GDP growth bouncing back to a solid 0.7% quarter on quarter or 2.3% year on year, driven by net exports and consumer spending offsetting weak business investment. Expect the October trade balance (Thursday) to have remained in deficit and retail sales (Friday) to show continued modest growth.

Outlook for markets

While the run-up to the Fed’s interest rate setting meeting in mid-December could see more volatility in share markets, it’s starting to look like investors are becoming less worried about it and that a Fed hike will actually be a vote of confidence in the US economy. The absence of one way bad news out of China or the emerging world may also be helping keep investment markets more settled. As such any near term correction in share markets could prove to be limited.

Looking further out, share markets are likely to see the normal “Santa Claus” rally into year-end particularly in the last two weeks of the year and the broad trend in shares is likely to remain up. Shares are cheap relative to bonds; monetary conditions are set to remain easy and the Fed is unlikely to do anything to threaten global growth; and this in turn should help see the global economic recovery continue. We continue to see the ASX 200 rising to around 5500 by year end.

Low yields point to soft medium term government bond returns, although they’re a great portfolio diversifier.

While the $A could still have a short term bounce up to around $US0.75, perhaps on expectations that the Fed will be gradual, the broad trend in the $A is likely to remain down as the interest rate differential in favour of Australia is set to narrow and the trend in commodity prices remains down. This is expected to see the $A fall to $US0.60 in the next year or so.

By Shane Oliver, AMP Capital

——-