How does the Code of Ethics govern and interact with the advice provided to clients regarding the establishment and ongoing operation of SMSFs?

The appropriate establishment of SMSFs has recently come under increased scrutiny by ASIC and, at around the same time, AFCA’s Annual Review noted SMSFs elicited the highest number of investor complaints. This article, proudly sponsored by GSFM, examines ethical considerations relevant to advisers recommending SMSFs to their clients.

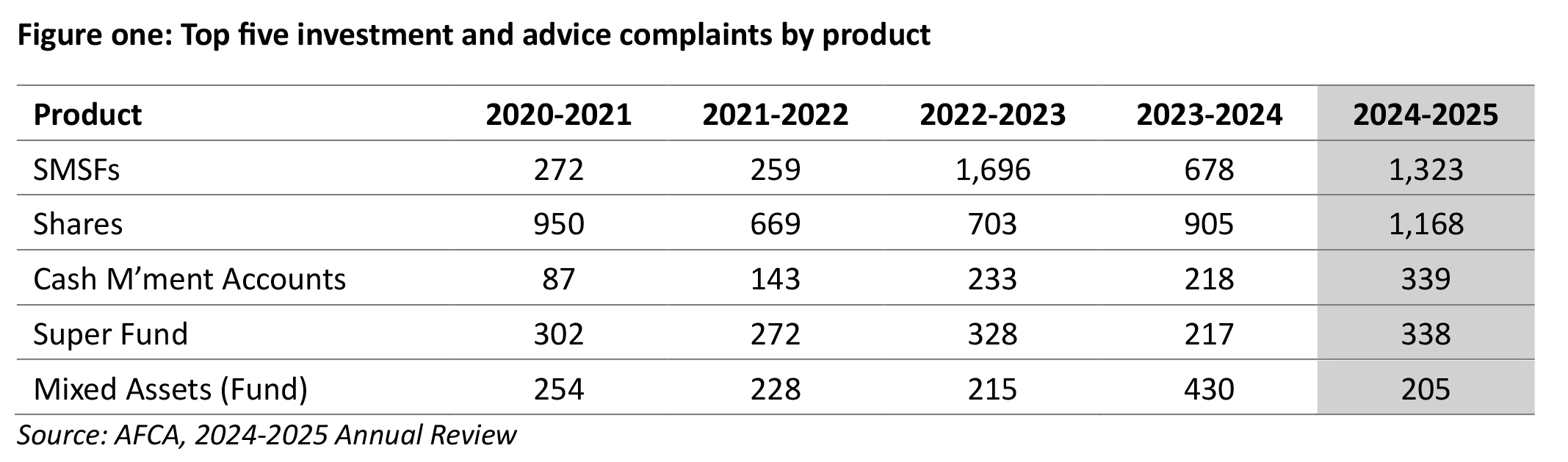

The recent release of the Australian Financial Complaints Authority’s (AFCA) 2025 Annual Review contained some unwelcome numbers for the advice profession. Investment and advice complaints increased to 18 per cent over the 2024–25 financial year, hitting 4,193. While representing around 4 percent of the total number of complaints received by AFCA, it nevertheless makes for uncomfortable headlines.

The current rise in complaints follows a 26 percent decline in the previous Annual Review, where the total number of investment and advice complaints dropped to 3,559. Further, when the numbers are examined by product, SMSFs top the list of the most complained about, with 1,323 complaints lodged, nearly double the number of complaints received the previous year (figure one).

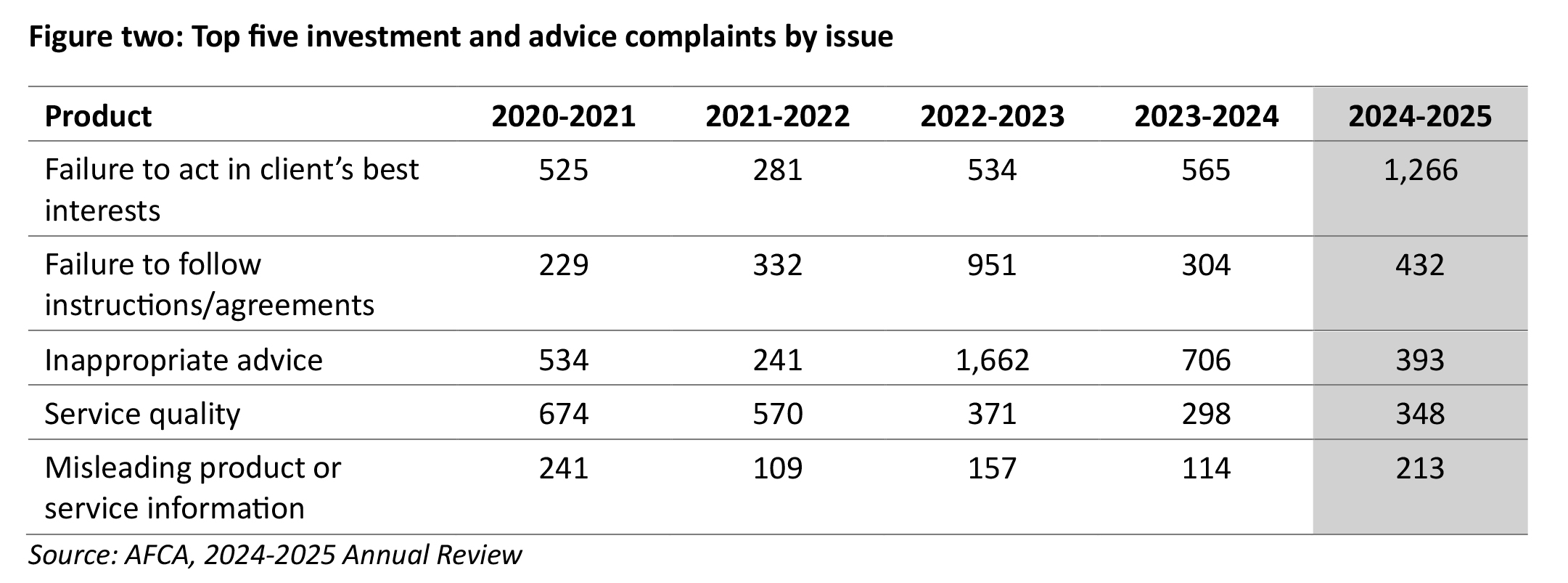

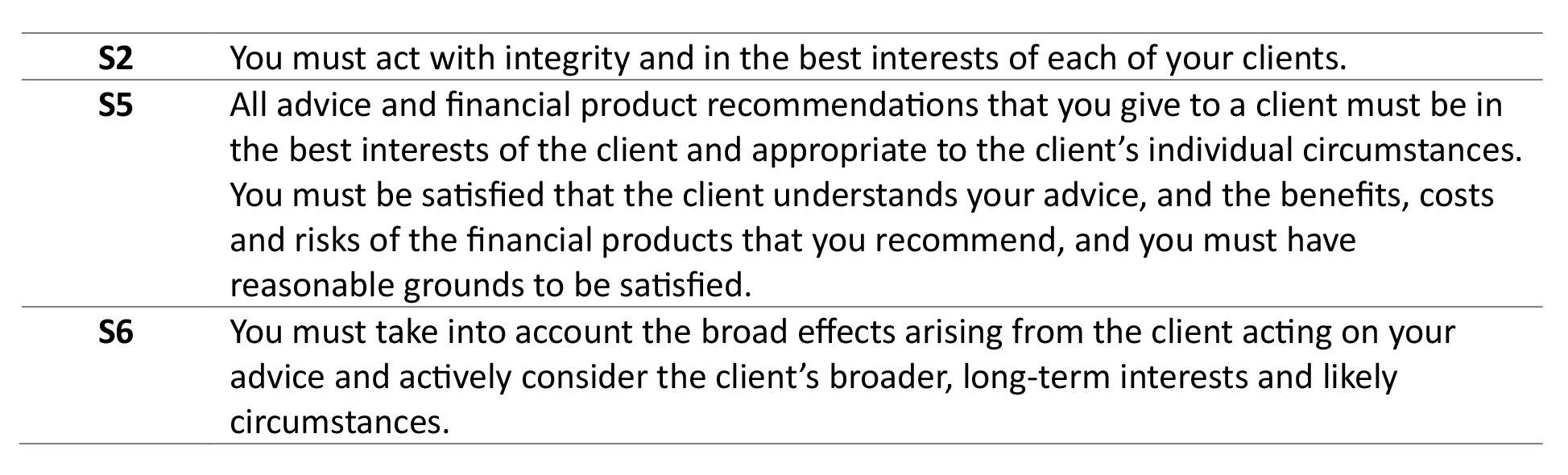

AFCA’s Annual Review cited the primary driver of the recent increase in overall complaints as a failure to act in the clients’ best interests. This specific issue saw a 124 percent surge in financial year 2025, with 1,266 complaints (figure two). While implied in many of the twelve standards that make up the Financial Planners and Advisers Code of Ethics 2019 (Code of Ethics), acting in the client’s best interests is specifically referenced in standards two and five.

Other issues of note were:

- Failure to follow instructions or agreements

- Inappropriate advice

AFCA noted a range of other factors that contributed to the overall rise in investment and advice complaints, which included concerns about advice business models such as:

- Cold-calling and pressured sales tactics

- Conflicted advice

- Undiversified and common product recommendations being made to the majority of a firm’s clients.

ASIC recently published Report 824: Review of SMSF establishment advice (released November 2025)[1], which raised serious concerns about the quality of advice financial advisers are providing to retail clients regarding the establishment of Self-Managed Superannuation Funds (SMSFs).

The report’s key findings and concerns were as follows:

- Failure rate – ASIC reviewed a risk-based sample of 100 financial advice files relating to SMSF establishment. It found that 62 percent of the files failed to demonstrate compliance with the Best Interests Duty and related obligations. This in itself would have breached several standards in the Code of Ethics.

- Client detriment – more alarmingly, more than one-quarter of the files raised significant concerns about client detriment, meaning the recommendation to set up an SMSF was unsuitable and potentially detrimental to the client’s retirement outcomes.

- Mis-selling ‘control’ – ASIC found advisers often justified the SMSF recommendation solely on the client’s desire for ‘control’” without adequately exploring what that notion meant for the client’s actual needs, skills and time commitment. ASIC noted that other superannuation vehicles may offer the desired level of control without the client taking on the additional responsibilities and risks of an SMSF.

- Acting as ‘order-takers’ – advisers failed to provide rigorous, well-considered advice and instead acted as ‘order-takers’, recommending an SMSF and its proposed investments (such as off-the-plan properties via limited recourse borrowing arrangements) without properly investigating whether the SMSF or the associated high-risk investments were suitable for the client.

- Conflicts of interest – in many files of concern, ASIC was worried that the financial adviser failed to prioritise the client’s interests above their own or those of their advice licensee or an associate, particularly where the advice involved establishing an SMSF to facilitate the purchase of specific assets.

- Ineffective pre-vetting – even when advice licensees had mandatory pre-vetting systems in place to review SMSF establishment advice before it reached the client, these systems were frequently ineffective. Out of 47 pre-vetted files reviewed, 33 still contained advice that failed to comply with the best interests duty.

ASIC emphasised that poor SMSF advice puts retirement savings at risk for two key reasons:

- Loss of protection – clients who move their super from an APRA-regulated fund to an SMSF lose important consumer protections, including the benefits of prudential regulation and the ability to complain about the fund’s trustees to the Australian Financial Complaints Authority (AFCA).

- Suitability and complexity – SMSFs are not suitable for everyone, regardless of the balance, and require trustees to have the time, skills, and interest to meet complex compliance obligations.

ASIC stressed that this report serves as a serious warning to both financial advisers and advice licensees to improve their practices when advising on SMSF establishment. The regulator provided specific action points for the industry to ensure that SMSFs are only recommended when genuinely suitable and in the client’s best interests.

ASIC has a specific role in regulating SMSFs. The regulator considers contraventions of the Corporations Act, the SIS Act and the ASIC Act, and is responsible for regulating the following harms:

- Dishonest conduct and fraud (section 1041G of the Corporations Act)

- Misleading and deceptive conduct (sections 769C, 1041E, 1041F and 1041H of the Corporations Act; sections 12DA–12DC, 12DF–12DG and 12BB of the ASIC Act)

- Unlicensed advice (section 911A of the Corporations Act)

- Contraventions of the relevant conduct and disclosure obligations, including the best interests duty and related obligations (sections 961B, 961G–961H and 961J of the Corporations Act)

- Contraventions of the Code of Ethics (section 921E of the Corporations Act), and

- Contraventions relating to SMSF auditors (sections 128D–128H and 130F of the SIS Act).

SMSFS and ethics

An SMSF is a private retirement vehicle established solely to provide benefits to its members. Capable of having between one and six members, SMSFs are highly regulated and subject to numerous, frequently changing rules and compliance obligations. ASIC Information Sheet 274 (INFO 274)[2] provides guidance to Australian financial services (AFS) licensees and their representatives who provide personal advice to retail clients about SMSFs. INFO 274 provides tips to help advisers comply with their legal obligations when giving advice about SMSFs, including:

- Understanding obligations when providing SMSF advice

- Using professional judgement to assess whether an SMSF is appropriate for the client

- Consideration of the risks associated with an SMSF

- Consideration of the costs associated with running an SMSF

- Factors to consider when advising a client to withdraw their superannuation from a fund regulated by the Australian Prudential Regulation Authority (APRA) to set up an SMSF.

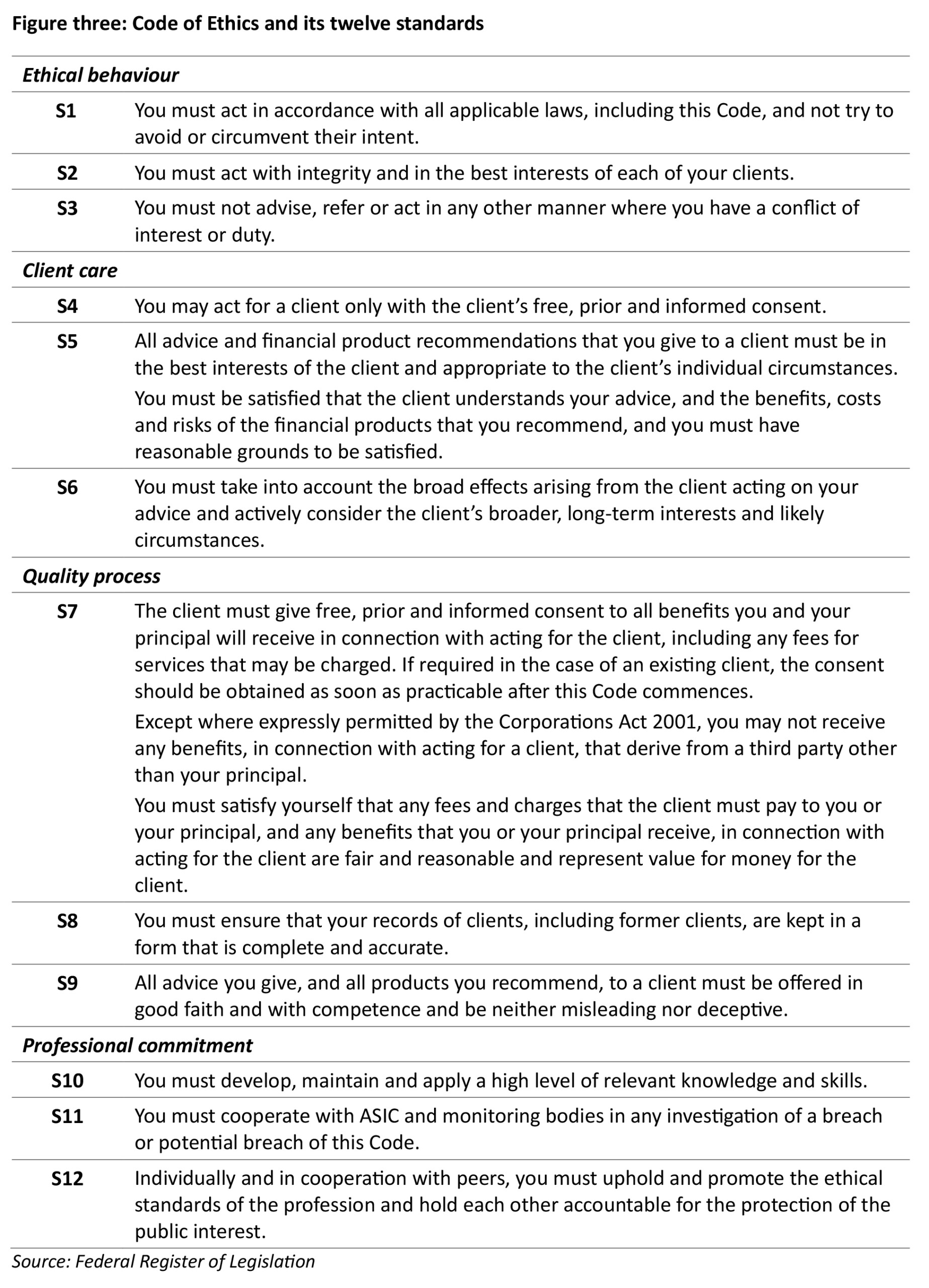

This article will review the recommendations for each subject matter area outlined in INFO 274, specifically examining them through the lens of the Code of Ethics and its 12 standards (figure three).

Understand obligations when giving SMSF advice

Any adviser providing SMSF advice to their clients must comply with numerous laws, including:

- The conduct and disclosure obligations in Parts 7.7 and 7.7A of the Corporations Act 2001 (Corporations Act)

- The Financial Planners and Advisers Code of Ethics

- The Superannuation Industry (Supervision) Act 1993 (SIS Act).

Importantly, when providing personal advice to clients – including advice about establishing and managing an SMSF – advice providers must meet the best interests duty and related obligations:

- Act in the best interests of the client (section 961B)

- Provide appropriate personal advice (section 961G)

- Warn the client if advice is based on incomplete or inaccurate information (section 961H)

- Prioritise the interests of the client (section 961J).

The first standard of the Code requires advisers to comply with all relevant laws including the Code. While acting in accordance with all laws applies to all areas of financial advice, there are additional regulations specific to SMSFs that advisers must comply with. ASIC holds AFS licensees directly accountable for their advice processes, especially concerning SMSFs.

The regulator expects licensees to tailor their compliance systems and controls to meet both:

- The general obligations under section 912A of the Corporations Act.

- The specific advice obligations set out in section 961K or 961L.

Crucially, ASIC also mandates that licensee processes must be robust enough to proactively detect and address two high-risk activities:

- The potential for dishonest conduct, fraud, or misleading and deceptive client communications. Exercise professional judgement to assess SMSF suitability

- The risk of unlicensed advice, ensuring authorised representatives never act outside the scope of the AFS licence conditions or authorisations.

Before recommending an SMSF, you must diligently assess the client’s existing superannuation arrangements and investigate whether those, or other retail or industry funds, might better meet their long-term retirement funding goals.

It is essential to consider the client’s full circumstances and ensure they fully grasp the implications of the SMSF advice. Establishing an SMSF can have serious consequences regarding their retirement savings, insurance coverage and associated responsibilities.

When providing SMSF advice, you should consider a range of factors, including the following:

What types of professional advice are appropriate?

Clients considering the suitability of an SMSF may benefit from advice from various professionals. When referring clients to SMSF specialists, it is important to comply with standard three and avoid any conflicts of interest that could arise due to the referral.

Providing personal advice to clients about SMSFs requires specialist knowledge. Before providing SMSF advice it’s important that you have and maintain SMSF knowledge and expertise, as required by standards nine and ten.

Before your client transfers their retirement savings from an APRA-regulated superannuation fund to an SMSF, you must ascertain that the SMSF is an appropriate retirement savings vehicle for that client, based on their objectives, circumstances and needs.

By doing this, you will ensure that you meet the requirements of standards two, five and six:

- to ensure the SMSF is in your client’s best interests

- that you have reasonable grounds to be satisfied your client understands your advice, the benefits and risks of using an SMSF, as well as the ongoing costs involved

- in making the recommendation to establish an SMSF, you have considered the client’s longer-term interests and likely circumstances.

Suitability is paramount because, without it, an adviser fails to act in the client’s best interests. This is not only a breach of the Corporations Act (and thus standard one of the Code) but also explicitly breaches standards two and five and underlies many other ethical duties within the Code.

ASIC provides the following as factors to consider when determining the suitability of an SMSF for your client:

- Your client must understand and accept that although they may outsource their SMSF responsibilities to professional advisers (such as accountants or audit specialists), as the SMSF trustee your client is responsible for ensuring compliance with superannuation, corporations and tax laws

- Your client must have the time, skills, general interest, and experience to meet their trustee responsibilities

- The cost-effectiveness of an SMSF considering your client’s existing arrangements, relevant circumstances and other SMSF members

- Any relevant vulnerabilities your client may be experiencing, such as cognitive impairment, accessibility constraints or coercion/elder abuse

- Other arrangements that may provide some of the benefits of an SMSF, such as ‘a member directed investment facility’ within an APRA-regulated superannuation fund.

Finally, you must have reasonable grounds to be satisfied that your client fully understands the advice, including the complete spectrum of benefits, costs, and risks associated with establishing and running an SMSF. A key area of concern for ASIC is when an SMSF is recommended without proper consideration of whether the client possesses (or can realistically develop) the time, skills, and knowledge necessary to effectively operate as an SMSF trustee.

APRA-regulated superannuation funds versus SMSFs

Compliance with the best interests duty and related standards require you to ensure the client understands and accepts the unique risks and responsibilities of an SMSF compared to an APRA-regulated fund. This detailed disclosure is specifically necessary to meet standard four (informed consent). If the client does not fully grasp the fundamental differences and the burden of the SMSF trustee role, the legal requirement for informed consent has arguably not been met.

Prior to SMSF establishment, you must ensure the client fully understands their trustee obligations and the serious penalties that apply for non-compliance. For instance, failure to follow SMSF regulations can result in breaching numerous ATO requirements. Critically, failing to properly inform your client about these onerous long-term duties could result in a breach of standard six, which requires you to consider and act in the client’s broader, long-term interests.

Some of the differences between SMSFs and APRA-regulated funds that you should discuss with clients include:

Protections in the event of theft or fraud

- Access to statutory compensation will differ; an SMSF does not have the same protections as an APRA-regulated fund and is not eligible for government compensation.

- While the client may have legal options in the event of theft or fraud, there is no certainty that compensation will be awarded. However, members of APRA-regulated funds are generally eligible for compensation in the event of theft or fraud.

Trustee complaints and resolution

- SMSF trustees (and members) may be required to resolve their own complaints.

- Clients should be aware of situations where disputes may arise, including:

- in the event of trustee relationship breakdown

- where member death benefits must be paid

- if a trustee/s considers that they have received unsuitable professional advice.

- Access to AFCA is only available to SMSF investors in certain circumstances, such as if they received advice from a licensed financial adviser and their complaint relates to the financial advice about the suitability of an SMSF, the SMSF investments or insurance products.

Client’s legal responsibilities as trustee

- You must be confident your client understands and accepts that as trustee, they are personally responsible for running their SMSF according to its trust deed and must ensure the fund complies with superannuation, corporations and tax laws.

- Your client must understand that:

- while trustees can use professionals or rely on other trustees to help run their SMSF, responsibility for SMSF compliance remains with the trustees

- all trustees share responsibility equally

- SMSFs are regulated by the ATO

- professionals who provide tax agent services must be on the Tax Practitioners Board register

- SMSF auditors must be registered with ASIC as an ‘approved SMSF auditor’ on the SMSF auditor register before they can sign off on SMSF audit reports

- all financial advisers who provide personal advice on SMSFs must be licensed by an AFS licence and registered with ASIC.

- Clients need to understand that a failure to comply with their obligations under superannuation and taxation laws can have significant consequences, such as the loss of tax concessions. All trustees are equally required to comply with trustee responsibilities and obligations and are liable for the actions of other trustees.

Your clients also need to be aware of the penalties they can face for non-compliance with superannuation, corporations or tax laws, including:

- Tax consequences, such as their SMSF losing its concessional tax treatment.

- Being disqualified from their role as trustee – this means they can no longer be members of the SMSF, and they are unable to start a new one.

- Civil or criminal penalties, depending on the seriousness of the breach.

The ATO can disqualify an SMSF trustee, or director of a corporate trustee, if:

- The trustee has contravened the rules.

- The ATO considers the trustee not to be a ‘fit and proper’ person for the role, having regard to the trustee’s personal character and circumstances.

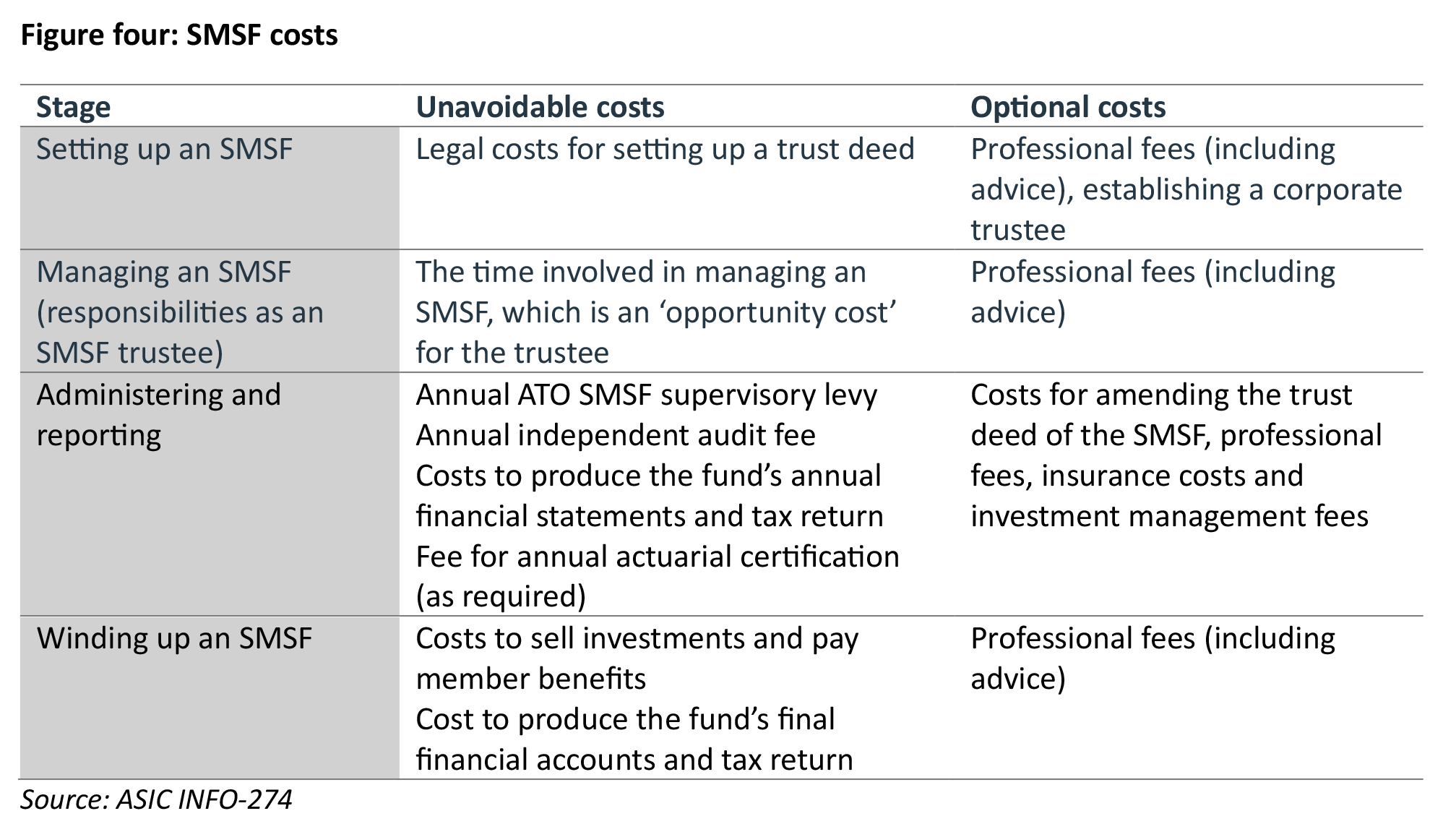

SMSF costs

It is crucial that your client understands the costs of an SMSF throughout its lifecycle. These costs will vary based on your client’s relevant circumstances; examples are set out in figure three.

The second part of standard five requires you to be satisfied that your client understands the costs, risks and benefits associated with your advice. With an SMSF, there can be a cost-benefit trade-off between the time taken to appropriately administer the SMSF versus the expected returns and benefits. To comply with this standard, you need to have reasonable grounds to be satisfied with respect to this cost-benefit trade off.

The starting balance of an SMSF is one of several factors you should consider when recommending an SMSF, as this is relevant to its cost-effectiveness (and compliance with standard five). Statistical data[3] shows that fund expenses are proportionally higher, and net returns lower, for lower balance funds.

However, it’s important to note that there may be circumstances when an SMSF with a higher starting balance is not in your client’s best interests. This may be because it does not meet your client’s objectives, financial situation or needs, or requires time and/or knowledge that the client does not have. Neither situation would be in the client’s best interest and a potential breach of standards two and five.

Suitable trustee structure

A core component of appropriate SMSF advice is recommending the most suitable trustee structure, whether that be corporate or individual. This decision is crucial due to its lasting impact on the client’s tax profile and succession planning. It is important to remember that changing structures after the fund is operational is often costly and complex.

The regulator is particularly concerned about poor practice here, including the failure to document consideration of the appropriate structure or simply directing a client to one option. Providing your client with a clear comparison of the risks and benefits of both structures meets the demands of several ethical standards, including best interests (standards two and five), long-term interests (standard six) and competence (standard nine). Discussion points to consider during the client conversation about a suitable trustee structure may include:

- Cost, including the potential cost of changing the trustee structure in the future

- Compliance with the SMSF trust deed, superannuation, corporations and taxation laws, the company’s constitution and the Corporations Act

- Administration and reporting requirements

- Trustee succession planning

- SMSF asset ownership considerations.

Trustee succession planning and exit strategy should be considered at establishment; this can help to reduce the impact of ‘unexpected’ events. They also need to understand the steps required to wind up an SMSF. This is relevant to standard six of the Code.

It can be helpful for clients to understand the reasons why they may need to wind up their SMSF, which can include:

- The SMSF proves not to be cost-effective

- Trustee responsibilities become too onerous or too costly

- A trustee dies or becomes incapacitated

- Disputes between trustees.

The investment strategy

As trustees, SMSF members are responsible for developing, maintaining, and reviewing a written investment strategy to ensure the fund is positioned to meet members’ retirement needs. Crucially, trustees remain responsible for all investment decisions, even when those decisions are based on advice from professionals.

It is important to remember that with a maximum of six members, an SMSF typically lacks the scale of large public funds. This size limitation can restrict investment opportunities, such as direct infrastructure or private equity, which usually require significant capital.

You must ensure your client understands the following key obligations:

- An investment strategy must be in place before any investments are made, and it must be regularly reviewed.

- All changes to the strategy must be documented in writing.

- Trustees should actively consider whether to hold appropriate insurance cover.

While you can assist the client in developing investment objectives and a suitable strategy, they must ultimately understand that as trustee, they are legally responsible for managing investments in the best financial interests of all SMSF members and in accordance with the law. When documenting the SMSF’s investment strategy, the following points should be considered and discussed with your client:

- The fund’s investment objectives

- Investment strategy and whether it is consistent with the trust deed

- Members’ risk tolerance

- The types of investments the fund can make, including the likely risk/return profile of these investments

- Implementation of investment decisions

- Diversification

- Death benefit nominations

- Liquidity requirements to meet fund expenses, including retirement benefits.

ASIC’s guidance notes the importance of adequately consider and inform your clients about:

- The benefits associated with diversification

- The restrictions that apply to SMSF investments

- Whether to hold insurance cover

- Prohibited transactions, including lending the fund’s money or providing financial assistance to a member of the fund or their relatives.

Importantly, you ought to ensure your clients understand the costs associated with implementing your SMSF advice recommendations, including ongoing fees. As well as best practice, standard five explicitly requires you to be satisfied your client understands the costs associated with your advice.

- Best interests (standards two and five)

- Long-term interests (standard six)

- Competence and good faith (standard nine)

Death benefit nomination

It is essential to ensure your client has a valid death benefit nomination in place and fully understands the consequences of failing to maintain one. This nomination must be reviewed regularly, especially whenever the client’s personal circumstances change, to ensure it remains effective.

Case studies

The following case studies are based on real events; however, the names of people and organisations have been changed, and some details altered. The case studies have been drawn from ASIC or AFCA and for each, potential breaches of the Code of Ethics are identified.

Case study one: Appropriate advice to establish an SMSF

A middle-aged couple, Bill and Jess, were new clients of ACME Advice and adviser Susan. The couple had two dependent children. When they first met with Susan, they mentioned the possibility of buying a property through an SMSF, including borrowing. Bill and Jess owned their home, some shares and an investment property, and had some existing debt.

In conversation with the clients, Susan determined the couple had the skills to manage an SMSF, a general interest to do so and the ability to take on the responsibilities of operating an SMSF.

Further, Susan believed her clients were suited to establishing an SMSF for the purpose of investing in direct property using an LRBA. She recorded sufficient detail on the client file to indicate that although borrowing and investing into a property through an SMSF would be on the upper end of their risk tolerance, the likely long-term retirement result was superior and in accordance with their desire to build financial independence by taking on extra risk.

Susan also considered the SMSF’s expected cash flow position following the proposed LRBA and property purchase and obtained information from Bill and Jess about their health before providing the SMSF advice and recommending an increase to their life insurances. Susan also recommended that a sizable component of the SMSF be retained in liquid, diversified assets to help mitigate the illiquidity and concentration risk of the leveraged direct property.

Upon audit, ASIC determined that the client file demonstrated that the SMSF with LRBA strategy was expected to help the client meet their retirement objectives and that the client was expected to benefit from the SMSF establishment advice.

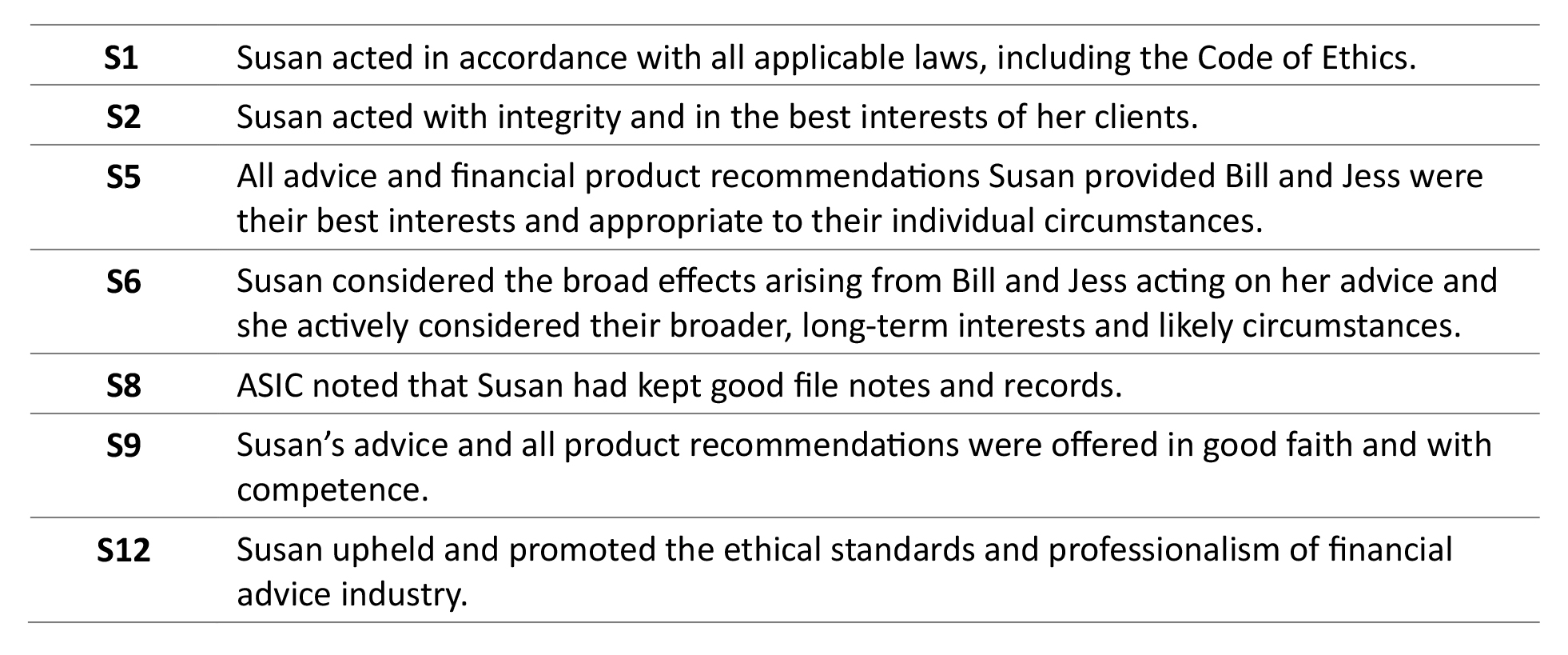

Consequently, Susan’s advice to Bill and Jess did not breach the Code of Ethics. In particular, the relevant standards she upheld were:

Monique and Peter complained to AFCA in their personal capacities and on behalf of the corporate trustee of a self-managed superannuation fund. The complainants were referred to Toby, an authorised representative of ACME SMSFs in 2020. Monique and Peter complained that the advice they received to establish an SMSF and use it as a vehicle to make a geared investment in a residential property was not in their best interests and was inappropriate. The complainants want to be compensated for $224,050 for the losses related to the SMSF to resolve this case.

However, ACME SMSFs denies responsibility for the claimed losses as it believes that its representative Toby did not make a specific property recommendation. It also claims:

- The advice was in the complainant’s best interests and was appropriate

- Monique and Peter would have proceeded with the geared property investment strategy in any event

AFCA determined that ACME SMSFs did not demonstrate that the advice to establish an SMSF and a property investment strategy was in the best interests of the complainants, as objectives and financial goals were inadequately investigated. Because the SMSF establishment was the core element of Toby’s advice, AFCA determined the advice fees should be refunded.

However, Monique and Peter were unable to establish that they would not have proceeded with the property investment irrespective of the establishment of the SMSF. Toby’s notes recorded that the couple articulated their wish to make this investment, hence his recommendation to establish the SMSF.

Accordingly, AFCA’s recommendation took the view that the complainants should be compensated $24,500, representing the advice fees paid by the SMSF between the 2020 SOA and the end of the advice relationship in 2024. However, the other aspects of the 2020 SOA were deemed to be appropriate and therefore no other refund or compensation was required.

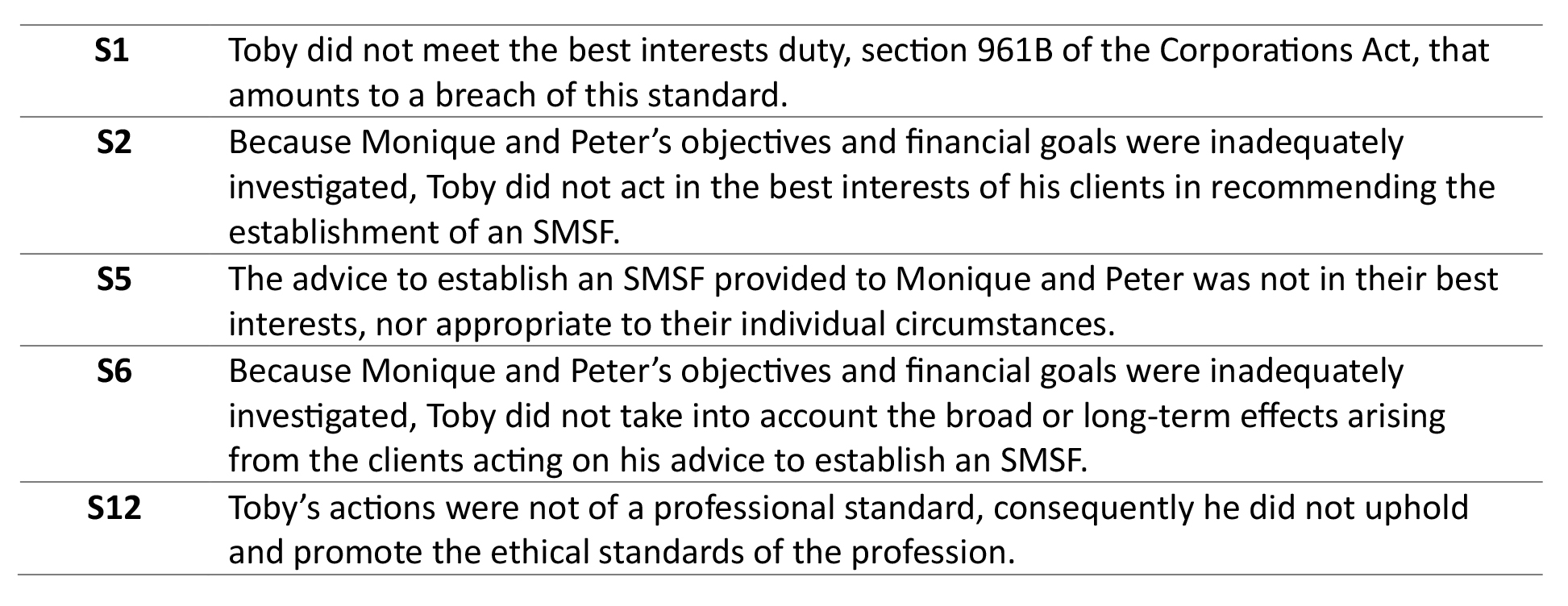

From the details provided in the case study, Toby and ACME SMSFs potentially breached the following standards in the Code of Ethics.

Case study three: Failure to act in clients’ best interests

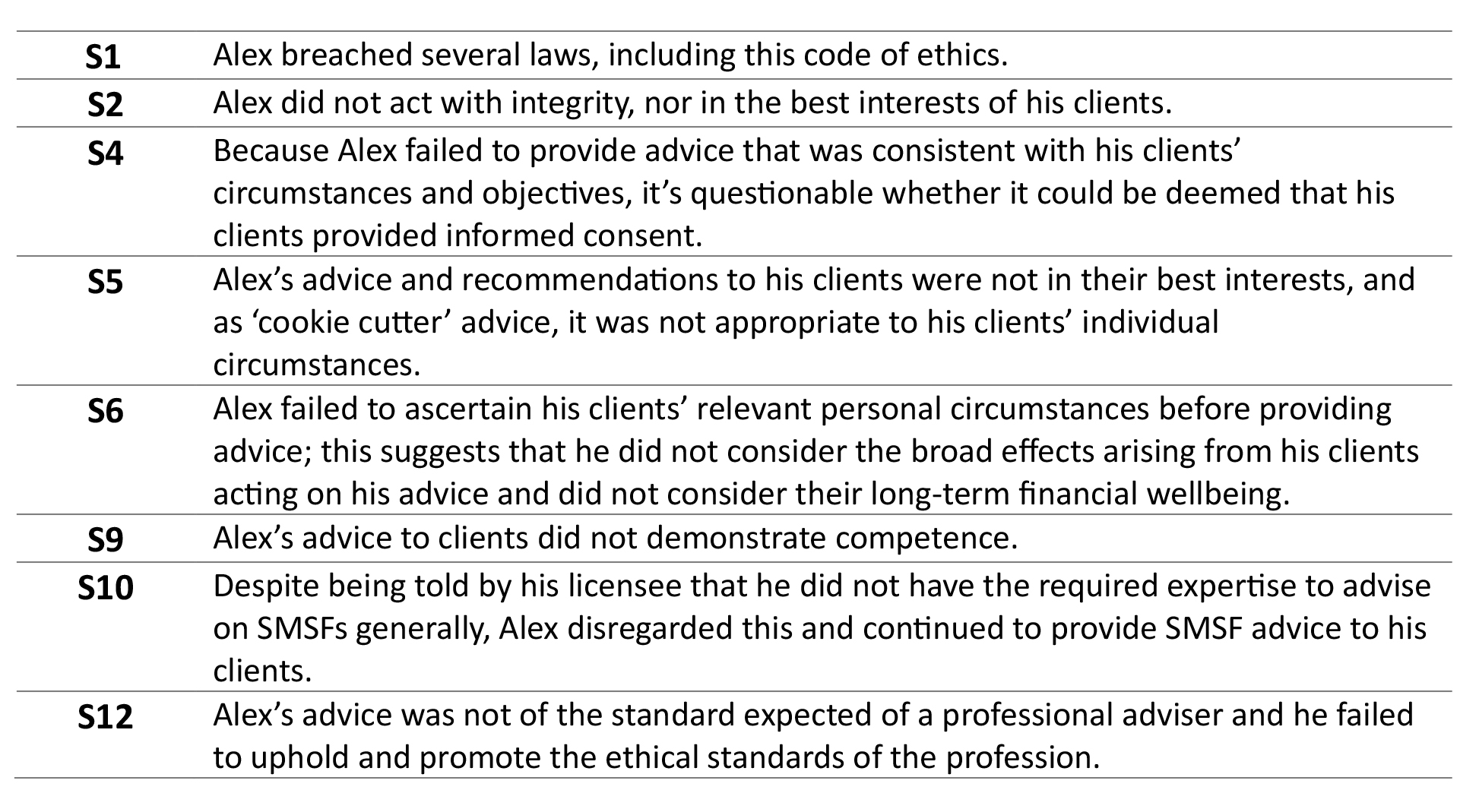

Alex was an adviser with ACME Financial Advice and referred several of his clients to an SMSF administrator to facilitate the establishment of SMSFs. He did this without providing any advice as to the roles of SMSF trustees and without ascertaining the clients’ capability to act as trustees. Alex then advised those clients to rollover their existing APRA-regulated super funds into their recently established SMSFs.

An ASIC investigation found that Alex failed to prioritise his clients’ interests and consistently failed to act in their best interests because:

- Alex provided ‘cookie cutter’ advice rather than the required personal advice. Consequently, the advice he provided was not appropriate to his clients’ circumstances, financial objectives or needs, nor was it appropriate to the subject matter of the advice sought by his clients

- Alex failed to make reasonable inquiries to obtain complete and accurate information about his clients’ relevant circumstances

- Alex focused his advice on rolling over superannuation savings from APRA-regulated super funds to SMSFs without adequately considering alternative options, such as whether his clients would be better off retaining their existing APRA-regulated super funds

- Alex failed to adequately consider and provide information about the risks, costs and obligations of taking on the role of SMSF trustee

- Alex had been informed by his licensee that he did not have the required expertise to advise on SMSFs generally but still proceeded to provide SMSF advice to his clients.

Consequently, ASIC banned Alex from providing financial services for eight years. From the details provided in the case study, Alex potentially breached the following standards in the Code of Ethics.

SMSFs can be a powerful vehicle for clients seeking greater control and investment flexibility. However, this control comes with a heavy regulatory cost. The associated time, financial expense, complex compliance obligations and significant personal liability imposed on trustees often outweigh the perceived benefits for many. Consequently, SMSFs are frequently an unsuitable option for individuals lacking the necessary financial expertise or the capacity to dedicate substantial time to ongoing administration and compliance.

For financial advisers, recommending an SMSF establishment demands deep due diligence. It requires a thorough understanding of the client’s unique circumstances, financial situation, long-term goals and risk tolerance. It is essential to meticulously assess whether the perceived flexibility and control truly align with the client’s best interests throughout their entire retirement horizon.

The decision to establish an SMSF is not a one-size-fits-all solution and should never be taken lightly. The role of professional advice is paramount. You must ensure clients are fully informed about the inherent responsibilities, risks and potential rewards. Ultimately, the adviser’s focus must remain on delivering a tailored retirement strategy that safeguards the client’s long-term financial wellbeing.

Take the FAAA accredited quiz to earn 1.0 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 1.0 hour.

Legislated CPD Area: Professionalism & Ethics (1.0 hrs)

ASIC Knowledge Requirements: SMSF (1.0 hrs)

please log in to start this quiz

———

Notes:

[1] https://www.asic.gov.au/regulatory-resources/find-a-document/reports/rep-824-review-of-smsf-establishment-advice/

[2] https://asic.gov.au/regulatory-resources/financial-services/giving-financial-product-advice/tips-for-giving-self-managed-superannuation-fund-advice/]

[3] https://www.ato.gov.au/About-ATO/Research-and-statistics/In-detail/Super-statistics

[4] ABS, Retirement and Retirement Intentions, Australia, October 2025

CPD Quiz

The following CPD quiz is accredited by the FAAA at 1.0 hour.

Legislated CPD Area: Professionalism & Ethics (1.0 hrs)

ASIC Knowledge Requirements: SMSF (1.0 hrs)

please log in to start this quiz

———