CPD: Ethics and client best interests

The intersection of ethical practice and the best interests duty underpins client-focused financial advice.

In financial advice, acting in a client’s best interest isn’t just a regulatory rule, it’s the foundation of a trusting, successful partnership. This article, proudly sponsored by GSFM, examines the strong links between your clients’ best interests and running an ethical advice practice.

Navigating complex financial choices can be daunting, which is why people turn to professional advisers to help secure their short- and long-term lifestyle goals. Clients place immense faith in an adviser’s expertise and integrity, expecting tailored strategies that mirror their personal values and unique circumstances. By consistently prioritising the client’s best interests, advisers do more than just build trust – they cultivate enduring relationships and solidify their own professional reputation. Ultimately, putting clients first isn’t simply an ethical duty; it is the bedrock of client satisfaction and long-term business growth.

As defined by the Australian Corporations Act 2001 (the Act), the best interests duty requires financial advisers to act in the best interests of their clients when providing personal financial advice. This duty is enshrined in Section 961B of the Act and requires advisers to take reasonable steps to ensure that the advice they provide is appropriate to the client’s individual circumstances, including their financial situation, needs and objectives.

The best interests duty is designed to ensure that financial advisers provide advice that is objective, unbiased and is tailored to the client’s needs. This fosters trust and confidence in the financial advisory industry and is of critical importance in the regulatory framework that governs the delivery of financial advice.

Best interests obligations

ASIC describes the best interests duty and related obligations as:

“…designed to ensure that retail clients receive advice that meets their objectives, financial situation and needs, and that you act in the best interests of your clients when providing advice.”

Financial planning, at its core, demands that practitioners always act in their clients’ best interests: with competence, honesty, integrity and fairness. Put simply, it’s the standard of care any of us would expect from a trusted professional.

The Quality of Advice Review (QAR) recommendations seek to modernise the best interests duty by abolishing the process-driven ‘safe harbour’ steps, replacing them with a principles-based, outcomes-focused fiduciary duty. However, as that has yet to find its way into law, the following steps as outlined in Section 961B of the Corporations Act 2001 (as amended) remain the benchmark requirement to satisfy the ‘best interests’ duty:

- To identify the client’s financial situation, objectives and needs; these should be provided to the adviser by the client.

- To identify the subject matter of the advice sought by the client (whether explicitly or implicitly).

- To identify the client’s relevant circumstances – the objectives, financial situation and needs that would reasonably be considered as relevant to the advice sought on the identified subject matter (i.e. the client’s relevant circumstances).

- To ensure this information is complete and correct and make reasonable enquiries should be made if gaps or inconsistencies are apparent.

- To assess whether you have the expertise required to provide the client advice on the subject matter sought and, if not, decline to provide the advice.

- When considering the advice sought, whether it would be reasonable to consider recommending a financial product. If a financial product is deemed relevant, a recommendation should only be made after thoroughly investigating the most appropriate products relevant to the client’s circumstances.

- When advising the client, the financial adviser must base all judgements on the client’s relevant circumstances.

- Take any other step that, at the time the advice is provided, would reasonably be regarded as being in the best interests of the client, given the client’s relevant circumstances.

Number eight is a last catch-all statement that encapsulates the spirit of the legislation; regardless of the client’s requirements, the advice must be underpinned by knowledge of the client and their circumstances. While the best interests duty applies to retail clients, a similar fiduciary duty is required for dealings with wholesale clients. To meet obligations under section 961B of the Corporations Act 2001, is indisputably to act ethically in all dealings with clients.

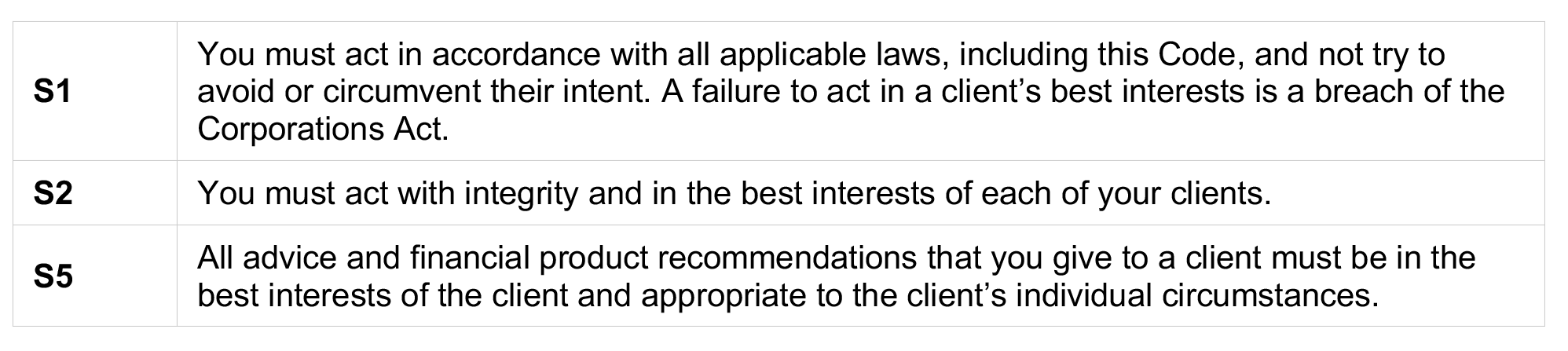

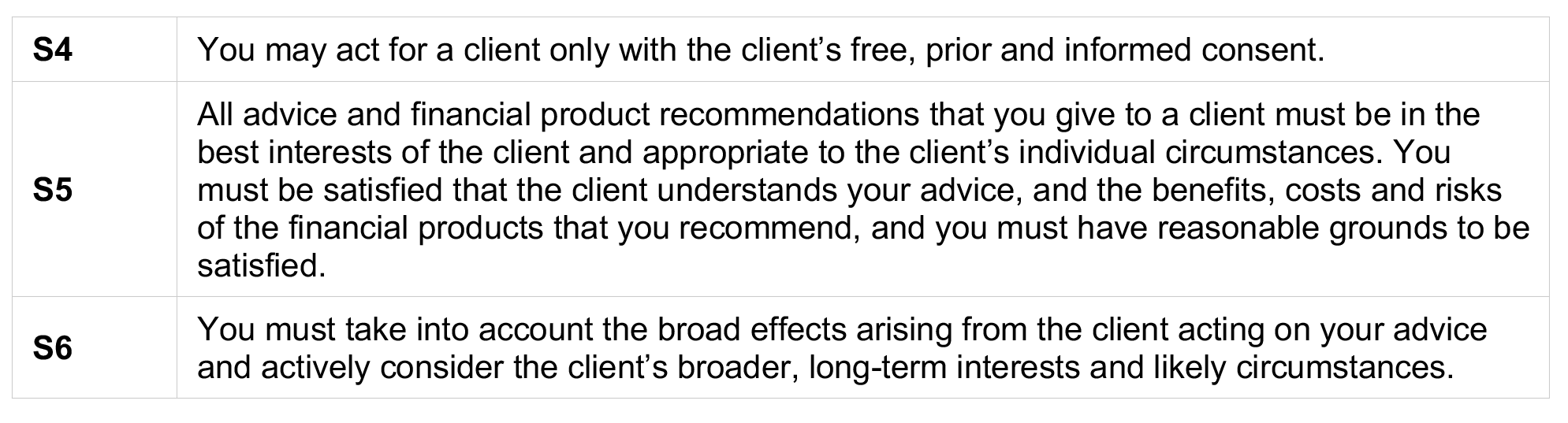

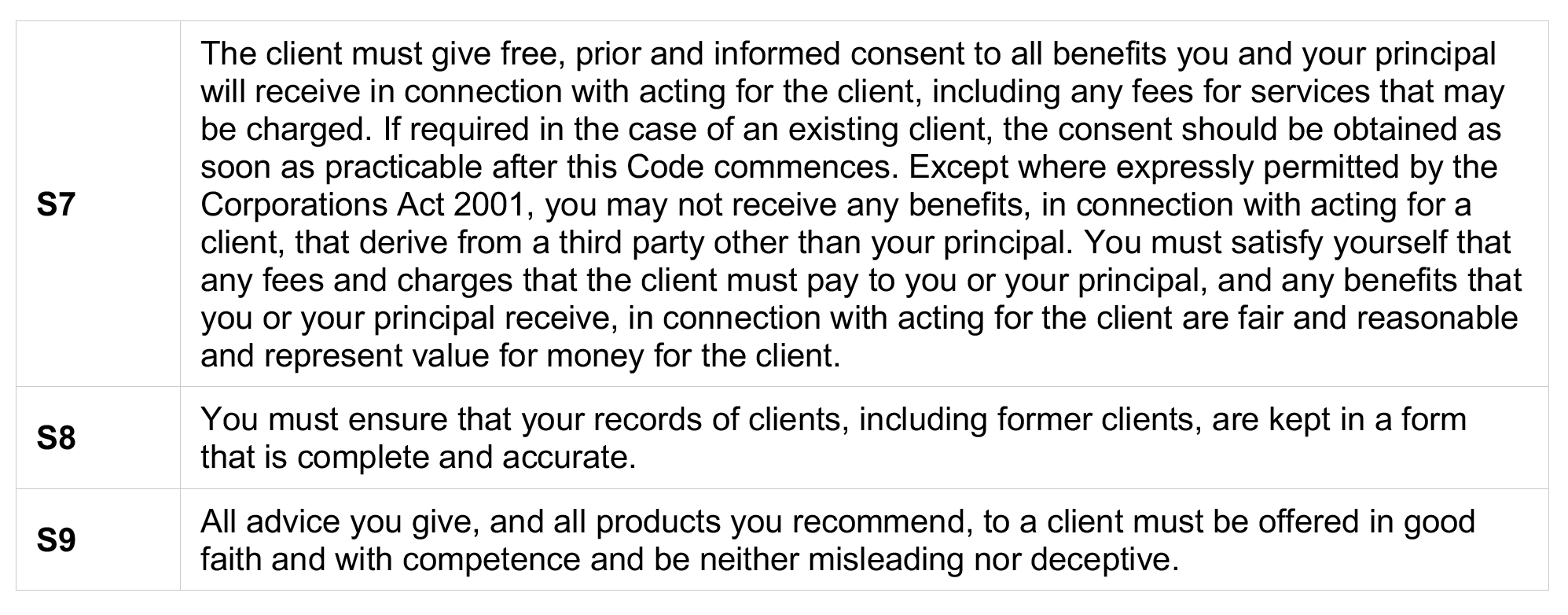

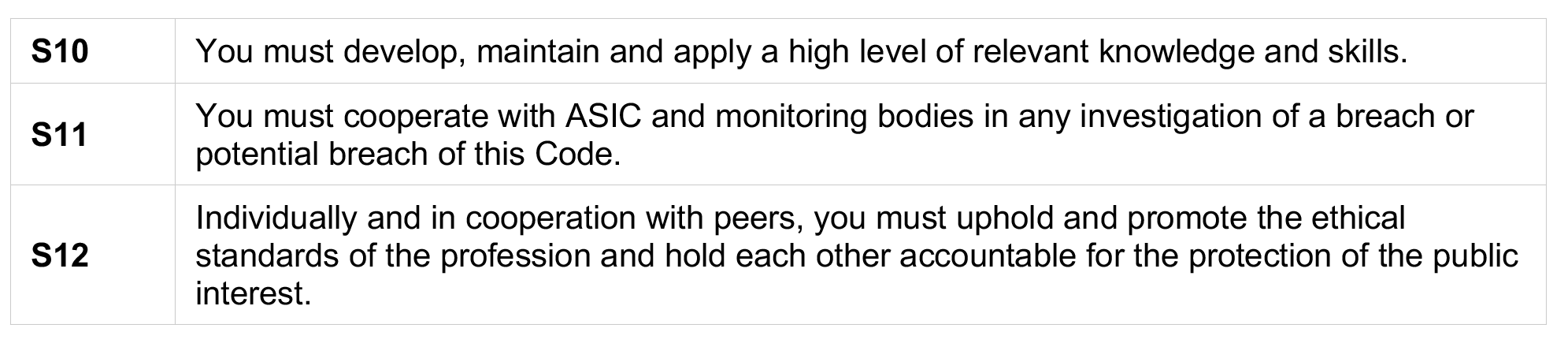

A failure to act in a client’s best interests would not only breach section 961B of the Corporations Act 2001, it would also breach several standards in the Financial Planners and Advisers Code of Ethics (Code) notably:

Best interests and the ethical practice

Most professionals enter their field with good intentions and a genuine commitment to ethical practice. And while ethics can sometimes occupy a grey area, putting the client first is rarely one of them.

For financial advisers, this obligation has a name – the best interests duty – and it carries real weight. Enshrined in the Code of Ethics (figure one), it requires advisers to place their clients’ needs above their own, those of their practice, or their licensee. In practice, this means delivering advice that is appropriate, personalised to each client’s financial situation and goals, and free from conflicts of interest.

Figure one: Code of Ethics – Standards

Ethical behaviour

Client care

Quality process

Professional commitment

Acting in clients’ best interests is the foundation of ethical financial advice. Because financial decisions can shape lives for decades, clients place enormous trust in their advisers. They trust that your guidance is genuine, considered and focused squarely on their wellbeing.

This duty also serves as a critical safeguard. By requiring that recommendations are based solely on what is right for the client, it protects against conflicts of interest and the potential for exploitation. That protection matters beyond the individual – it builds confidence in the advice profession and empowers clients to make informed decisions, knowing the guidance they receive is free from bias.

The benefits extend further still. When advisers consistently prioritise their clients, misconduct decreases, professional reputations strengthen and the industry as a whole moves closer to the regulatory ideals of fairness, transparency and consumer protection.

In practice, meeting this standard means being transparent, honest and diligent in every client interaction. These are also some of the values on which the Code of Ethics is based. It means taking the time to genuinely understand each client’s circumstances, and recommending strategies – and where appropriate, financial products – that truly serve their interests. It also means that advisers commit to ongoing education and stay current and competent, so the advice provided to clients continues to meet both professional and regulatory benchmarks.

While enshrined in law and in the Code of Ethics, there are actions all advisers can take to support practice-wide ethical behaviour, maintain a strong ethical business culture and ensure client’s best interests always come first. These include:

1. Establish a practice-wide code of conduct

One which encapsulates your business’s values and aligns with the Code of Ethics. A well-crafted code sets clear expectations for how your people behave in carrying out their duties, with client-first thinking at its heart.

Critically, this isn’t a document to file and forget. Every member of your team should have a thorough understanding of all twelve standards within the Code of Ethics, not just in general terms, but in ways that are relevant to their specific role. When staff can draw a direct line between each standard and their day-to-day responsibilities, putting clients’ interests first becomes less a compliance exercise and more an embedded part of how your practice operates.

2. Lead by example

Employees will look to the key individuals in the practice to understand what conduct is and isn’t acceptable. Senior advisers and personnel set the tone for ethics in the practice; accordingly, they need to demonstrate your business’s code of conduct in all they say and do. When the team sees you putting your clients’ best interests first, they are more likely to do the same.

3. Invest in workplace training

Workplace training is a positive way to ensure all staff understand both the practice’s values and the obligations of the Code of Ethics. Provide regular training sessions on ethical behaviour, regulatory compliance, conflict of interest and integrity. Training should cover both theoretical aspects and practical, real-world scenarios.

Case studies are a powerful way to bring your code of conduct to life. Walking your team through scenarios where a client’s best interests could be compromised helps reinforce expected standards and draws a clear distinction between what does and doesn’t align with your practice’s values.

Workshops and role-playing exercises take this a step further, placing staff in realistic situations where ethical dilemmas might arise and guiding them through how to respond in line with the Code of Ethics. Weaving this kind of training into regular team meetings, drawing on case studies that reflect common challenges across the financial planning industry, keeps ethical practice front of mind and ensures it remains an ongoing conversation rather than a one-off tick-box exercise.

The AFCA website is a good source of cases and decisions made by AFCA to form the basis of discussion. You can search specifically for decisions related to failing to act in a client’s best interests, as well as other issues not aligned with ethical behaviour.

It’s important that ethics training is not a one off; ideally, training should teach team members to make good decisions that are compliant with the law and consistent with your practice’s values.

4. Make ethical behaviour a KPI

Ethical behaviour should be a key performance indicator (KPI); by reinforcing and potentially rewarding staff for embodying your values, adhering to your practice’s code of conduct and behaving in a way that makes ethical behaviour central to their work will create an ethical practice. Although a values-driven KPI can be harder to quantify than one with specific and measurable outcomes, it will highlight to staff the importance of values and ethics to your business.

5. Ensure clear communication channels

Ensure clear communication channels within your practice. Encourage open dialogue to create a culture of transparency where employees can discuss ethical concerns without fear of retaliation. Create regular feedback loops, whereby employees provide honest feedback about the processes, conversations and client interactions to ensure you are aware of all issues as they arise. Surprises can potentially compromise your business.

Bringing your peers on the ethical journey is important. The licensee and adviser will carry the responsibility of any breach of the Code, but implementing strategies such as those outlined above can help mitigate the risk of breaching ethical standards.

Consider enforcing a zero-tolerance policy for ethical violations to make clear that breaches are taken seriously. Define relevant disciplinary actions for unethical behaviour and apply them consistently across all levels of the practice. Consistency is key; without it, credibility and fairness are quickly undermined.

When integrity, education, transparency and accountability are genuinely embedded in your culture, something important follows. Colleagues align around a shared set of ethical standards, trust builds from the inside out, and the practice becomes one where putting every client’s interests first is simply the way things are done.

Case studies

The following case studies are based on real events; however, the names of people and organisations have been changed, and some details altered. The case studies have been drawn from ASIC or AFCA. For each, potential breaches of the Code of Ethics are identified. These case studies represent examples of those that would be of value for the business to discuss as part of its workplace training.

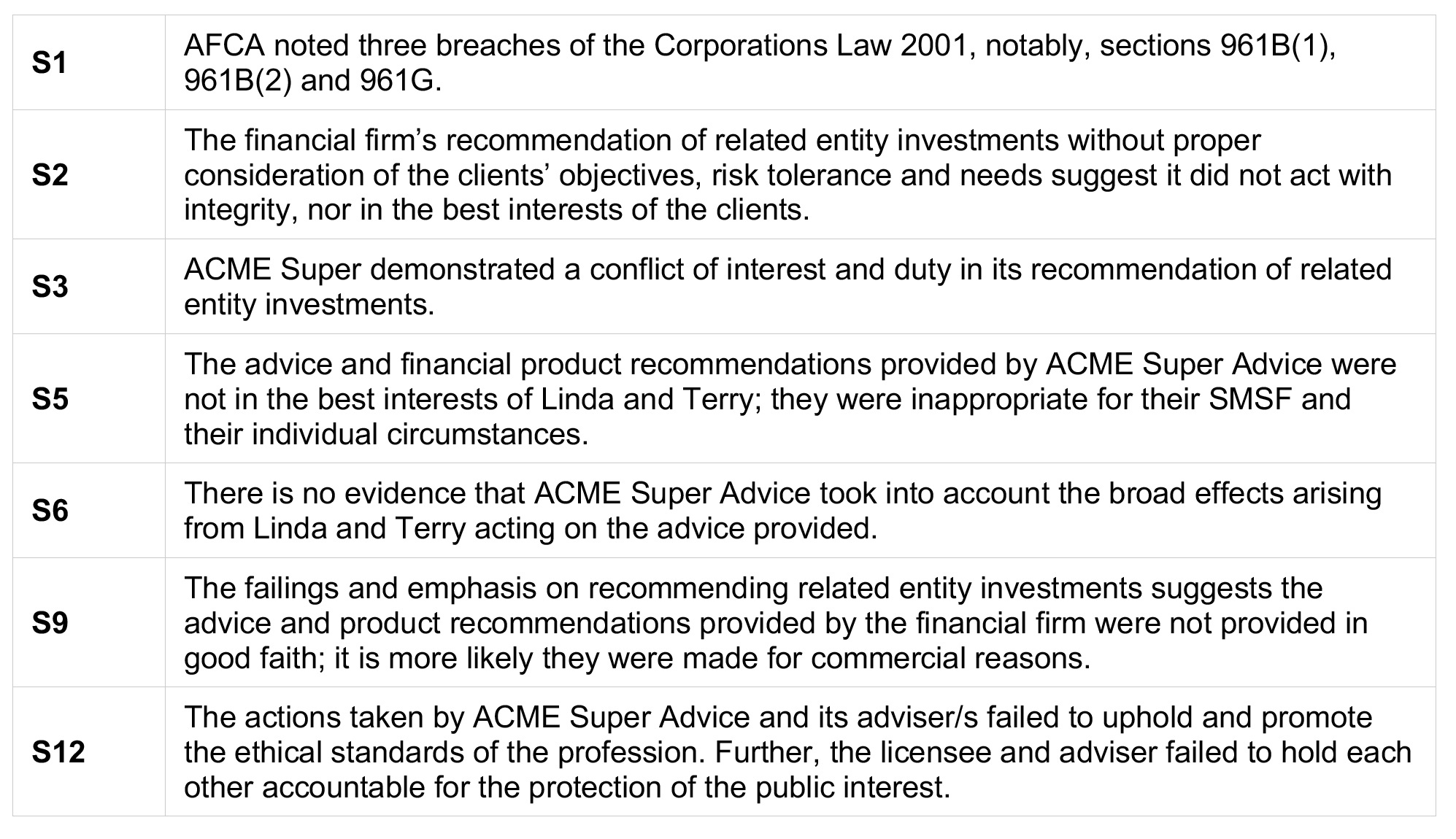

Case study one: Failure to act in clients’ best interests #1

The complainants are corporate trustees of a self-managed superannuation fund (SMSF), directors Linda and Terry. The couple sought and received personal advice from the financial firm ACME Super Advice. They were a client of ACME Super Advice from March 2011 to January 2024, during which time the couple received an investment strategy and investment advice in relation to their SMSF investments.

Linda and Terry claimed that ACME Super Advice provided inappropriate advice because the financial firm was conflicted in making investment recommendations. As a result, the couple claimed their SMSF suffered significant losses.

An AFCA investigation found that ACME Super Advice did not provide appropriate advice, nor did it act in the complainants’ best interests. It was found that ACME Super Advice:

- failed to provide advice within the risk parameters it set

- failed to diversify the portfolio’s ‘growth’ assets, instead recommending a portfolio heavily weighted towards residential property

- recommended an overly high proportion of related entity residential property investments without justification.

ACME Super Advice failed to establish that it prioritised the complainants’ interests over its own. The proportion of related entity investments compared to non-related entity investments was found to be excessive. The related entity investments recommended by the financial firm carried significantly more risk than Linda and Terry understood to be the case and were not aligned with the couple’s risk profile. Finally, the investigation found the fees to be excessive when compared to alternative investment products.

The determination noted that ACME Super Advice failed to act in the best interests of their clients and breached the following sections of the Corporations Act 2001 – 961B(1) best interests duty; 961B(2) failure to demonstrate best interests by following ‘safe harbour’ steps; 961G it would be reasonable to conclude that the advice is appropriate to the client had the provider satisfied the best interests duty.

AFCA found that the financial firm’s failure to provide appropriate advice and act in the complainants’ best interests resulted in Linda and Terry’s SMSF being $885,545 worse off. Accordingly, the final determination was that ACME Super Advice was required to compensate the complainants for losses incurred.

The adviser and ACME Super Advice potentially breached the following standards in the Code of Ethics:

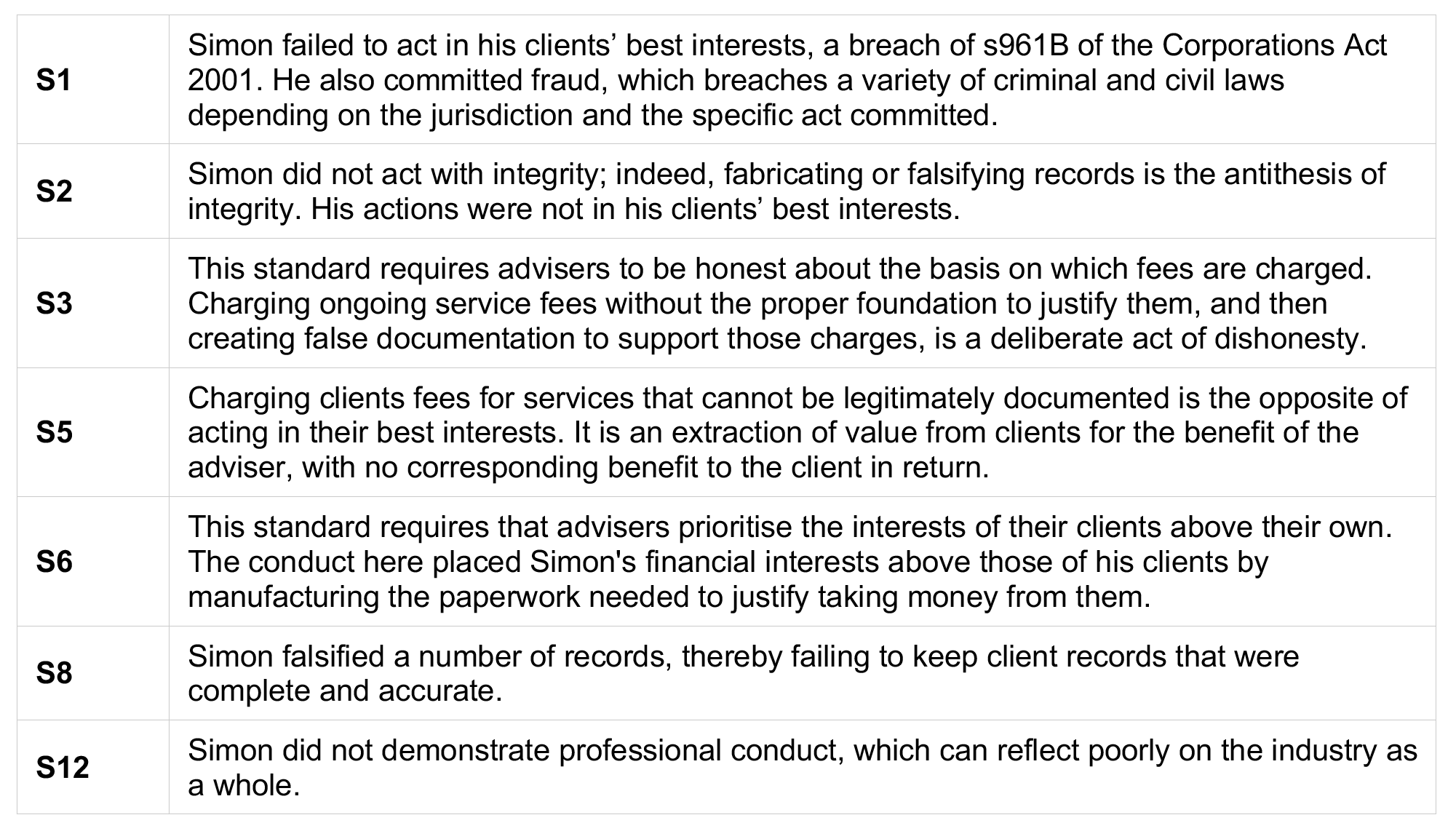

Case study two: Failure to act in clients’ best interests #2

Simon was a financial planner and the sole director of ACME Wealth Services, an advice practice holding both an Australian Financial Services Licence and an Australian Credit Licence. Simon had operated within the financial services industry for a number of years, having previously been an authorised representative of a large dealer group, during which time he was also the sole director of ACME Financial Services Pty Ltd, a corporate authorised representative of that dealer group.

An ASIC investigation uncovered that, on three occasions, Simon relied on service agreements that included client signatures that ASIC determined had not been provided by the clients themselves. In addition, ASIC found that Simon had created, or caused to be created, file notes that did not accurately reflect actual client interactions. The purpose of both courses of conduct was the same: to justify the charging of ongoing service fees. Clients were being charged for services that could not be legitimately substantiated, and the documentation used to support those charges had been fabricated or altered.

ASIC determined that, having regard to this conduct, Simon did not meet the statutory requirements to be a fit and proper person to participate in the credit and financial services industries.

In this case, Simon was potentially in breach of the following ethical standards:

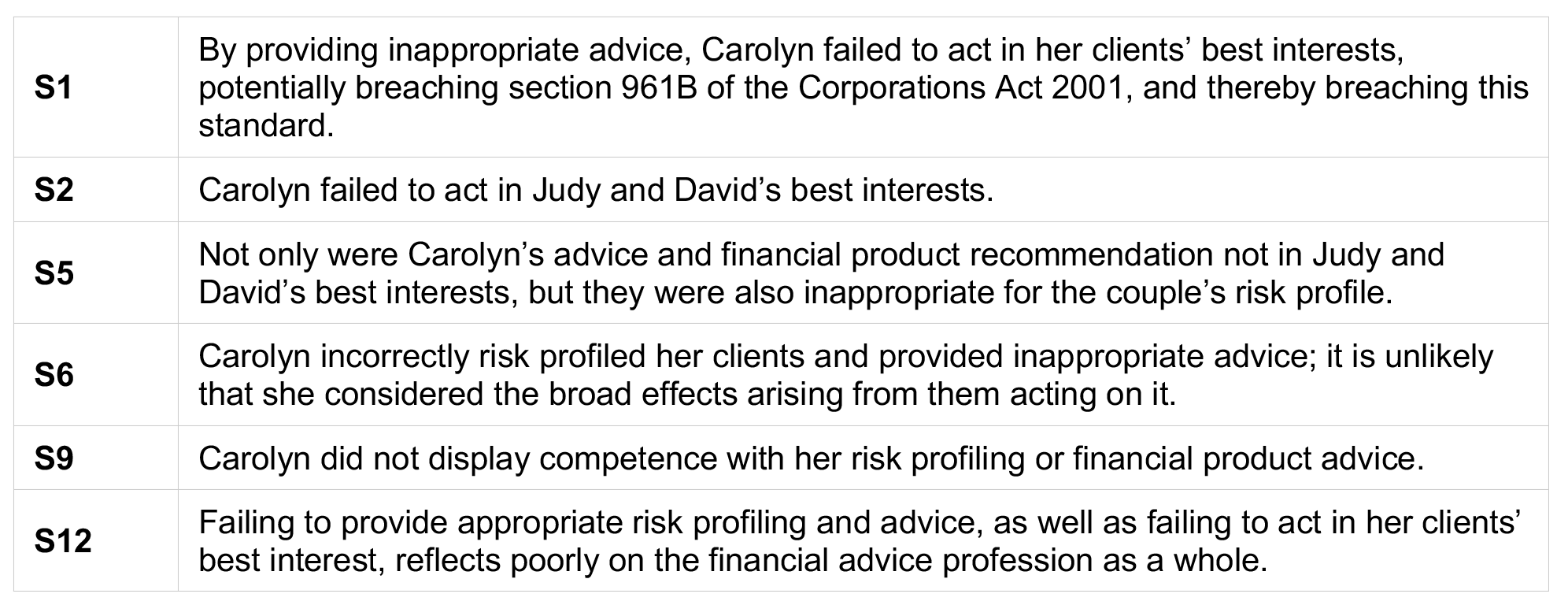

Case study three: Inappropriate advice #1

The complainants, Judy and David, were 72 and 75 at the time of seeing adviser Carolyn, an authorised representative of financial firm ACME Advice.

Carolyn recommended that Judy and David invest in a Capital Protected Fund (the A Fund). At the time David had $450,000 and Judy had $345,000 to invest.

Judy and David were classified by Carolyn as ‘Assertive – Balanced’ investors. This risk profile resulted in a recommended asset allocation of 30% defensive assets and 70% growth assets. The complainants say they understood from Carolyn that the A Fund was capital protected, and that they would get the highest return for the year locked in for the remainder of the period.

They later found out that they would only get the return available at the anniversary of the product. They claimed had they known this was the way the product worked, they would not have invested because returns were significantly lower than they had been led to expect. Judy and David also claimed that Carolyn charged higher fees than initially declared.

An investigation by AFCA determined that Carolyn failed to adequately explain how the A Fund worked. Had the complainants properly understood the level of uncertainty associated with the product, they would not have invested.

The determination also noted that Carolyn failed the best interests duty by not providing appropriate risk profiling and advice to her clients. Finally, AFCA accepted that the complainants would have been conservatively invested if appropriately advised, which resulted in a total loss of $97,495.

AFCA’s determination found in favour of the complainants; total compensation equating to the couple’s loss, plus 1.5% interest per annum compounding annually from the determination to the date of payment, was ordered.

By inadequately describing how the product worked and failing to provide appropriate risk profiling and advice to her clients, Carolyn potentially breached the following standards in the Code of Ethics:

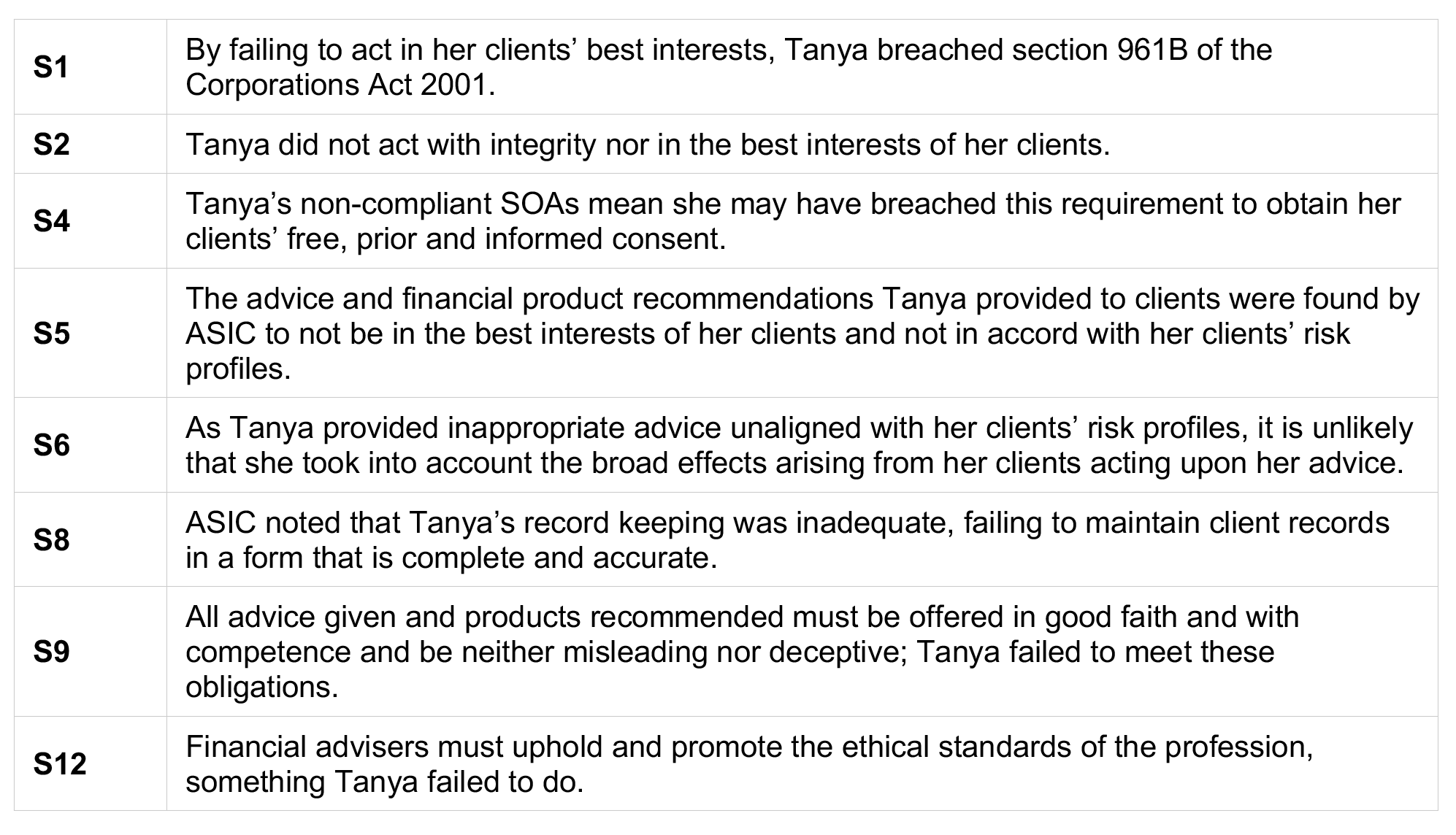

Case study four: Inappropriate advice #2

Tanya was an experienced financial adviser with ACME Financial Planning. She was subject to a series of client complaints and an investigation by ASIC. The investigation revealed a pattern of misconduct, which resulted in severe consequences for Tanya’s career and her reputation within the financial services industry.

ASIC identified the following issues:

- Inappropriate recommendations – Tanya demonstrated a strong tendency to make recommendations not aligned with her clients’ risk profiles. ASIC noted concerns about the subsequent suitability of the investment strategies she proposed, potentially exposing clients to excessive risk.

- Non-compliant Statements of Advice – ASIC’s investigation discovered that Tanya had provided some clients with non-compliant SoAs, which can hinder clients’ ability to make informed decisions about their finances.

- Inadequate record keeping – there were repeated instances of Tanya’s failure to maintain adequate records. Proper record-keeping is essential in the financial services industry to ensure transparency, accountability and regulatory compliance. The lack of proper documentation raised concerns about the integrity of Tanya’s practices.

- Failure to act in her clients’ best interests – Tanya breached this most fundamental obligation on several occasions.

As a result of ASIC’s investigation, Tanya was banned from providing financial services for a period of five years.

According to the information provided, Tanya potentially breached the following standards:

Acting in every client’s best interests is the cornerstone of any ethical financial advice practice. It fosters trust, builds long-lasting relationships and safeguards the integrity of the profession. When clients feel confident that their adviser is genuinely in their corner, they are better placed to make informed financial decisions – and that empowerment leads to sustainable outcomes for both the client and the business.

The Code of Ethics exists not as a burden, but as a framework that supports advisers in doing what most entered the profession to do in the first place: make a meaningful difference in their clients’ financial lives. Its twelve standards provide clear guidance on what ethical practice looks like in action, and when embraced wholeheartedly rather than treated as a compliance obligation, they become a genuine competitive advantage.

In an industry where trust is everything, the advisers who consistently place their clients first are the ones who stand apart. They attract clients who value integrity, retain them through the strength of the relationship, and build practices with reputations that speak for themselves. Referrals follow. Loyalty follows. Longevity follows.

Ultimately, ethical practice is not a constraint on success. It is the foundation of it. For financial advisers, the best interests duty and the Code of Ethics are more than regulatory requirements. They are a professional standard worth upholding, a commitment to clients worth keeping and a standard of care the industry should be proud to deliver.

Take the FAAA accredited quiz to earn 0.75 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Professionalism and Ethics (0.75 hrs)

ASIC Knowledge Requirements: Ethics (0.75 hrs)

please log in to start this quiz

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Professionalism and Ethics (0.75 hrs)

ASIC Knowledge Requirements: Ethics (0.75 hrs)

please log in to start this quiz

Have feedback on this article? Contact Us

Earn CPD Points

CPD: The spectrum of growth

CPD: The spectrum of growthCompanies that generate strong, sustainable growth are valuable sources of long term capital appreciation in a portfolio, but these businesses are rare, difficult to identify and exist on a broad [...]

CPD: Record-keeping in financial advice – the key to compliance and consumer protection

CPD: Record-keeping in financial advice – the key to compliance and consumer protectionIntroduction The financial services regulatory framework is a key pillar of financial consumer protection. Regulatory compliance is therefore not merely about avoiding penalties, but is a critical step in building [...]

CPD: Trust and ethics in financial advice

CPD: Trust and ethics in financial adviceIn 2024, trust in financial advisers reached an all-time high. This article, proudly sponsored by GSFM, explores the inseparable links between trust and ethical practice when providing financial advice. Defined [...]

CPD: Retirement Income Strategies

CPD: Retirement Income StrategiesIt has been almost 40 years since award superannuation was introduced in Australia, and 33 years since the introduction of mandatory occupational superannuation. This means the next decade will see [...]

CPD: Free cash flow works

CPD: Free cash flow worksThe difference between earnings and free cash flow is an important investment concept, one explained here by GSFM’s investment partner TD Epoch. Earnings have long played a dominant role in [...]