Investment markets and key developments over the past week

The past week has seen shares under pressure again as worries about a Fed rate hike next month driving the $US up, putting downwards pressure on commodity prices and reigniting worries about the emerging world returned. Resources shares led the way down as oil and iron ore prices head back towards their recent lows. This in turn has seen Australian shares fall almost back to their September lows, even though global shares remain well above them. While US, Eurozone, Asian, emerging market and Australian shares fell over the week Japanese and Chinese shares rose. Despite the fall in commodity prices the $A actually rose helped by stronger than expected Australian jobs data. Bond yields rose in Australia on the back of the jobs data but fell in the US, Japan and particularly Europe where talk of ECB easing is weighing.

Back to worries about a rising $US and its impact on US growth, commodities and the emerging world. With heightened expectations the Fed will now raise interest rates in December we are seeing a return to the worries of August and September that a stronger $US will weigh on commodities and accentuate the risk of a crisis in the emerging world and that this will all blow back and harm the US. If the Fed is not careful this could see a re-run of September where the Fed is forced yet again to back down from its plans to raise US rates. To minimise the risk of such a re-run, key Fed officials are trying to sound a bit more dovish, emphasising that the pace of hikes will be very gradual. This was particularly evident in a speech by NY Fed President Dudley, and is all aimed at damping down upwards pressure on the value of the $US. As the path of least resistance of the $US is up (as the Fed moves to hike and other central banks like the ECB and BoJ continue to ease), expect more dovish talk of a gradual approach from the Fed and also bear in mind that the $US will be a big brake on how much the Fed will be able to tighten. So it’s worth keeping an eye on.

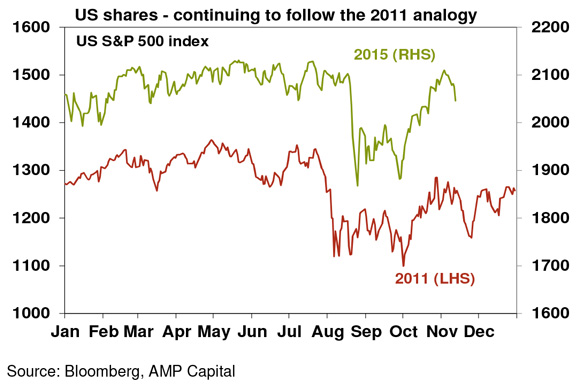

US shares still following the 2011 analogy. After a strong gain through October, the 2011 analogy now points to a pull back through November. Fed worries are likely to be a key driver of this. But once the Fed is out of the way expect a decent rally into year-end as investors get more comfortable that the Fed is not going to be aggressive and is allowing for the impact on the $US and global growth. Global share markets generally are likely to follow a similar pattern, but with Australian shares remaining a relative underperformer as commodity price weakness continues to weigh.

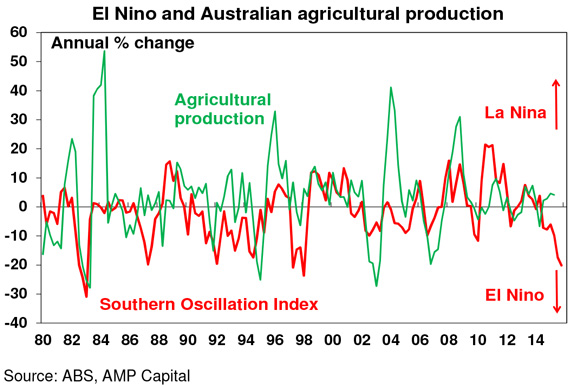

El Nino and the Australian economy – should we be worried? Indicators of the risk of a serious El Nino weather phenomenon have been getting more concerning. An El Nino sees trade winds that normally blow across the Pacific to the west (La Nina) weaken or reverse causing more rain in the east Pacific and less rain/drought in the west. It is commonly measured by the Southern Oscillation Index which measures sea surface pressures across the Pacific and it is nearing levels seen around the last major El Nino of 1997-98 and so warning of drought in Asia and the east coast of Australia, pointing to lower farm production and higher food prices. For Australia, the link from El Nino to farm production varies, eg farm production was little effected by the severe 1997-98 El Nino but was more affected by weaker El Nino’s last decade. See the next chart.

And swings in farm production don’t have the impact they used to on the economy as it is now only just above 2% of GDP. That said a severe El Nino drought induced slump in Australian farm production at a time when growth is sub-par would not be good. For example a 20% slump in farm production (as occurred in the 1982-83 severe El Nino) would knock around 0.45 percentage points off GDP growth. While food prices may see some upwards pressure, the hit to growth would likely dominate the RBA’s thinking supporting the case for lower rather than higher interest rates.

Major global economic events and implications

US data was a bit light on with no major economic releases and mixed signals. Jobs data remains solid with ultra-low jobless claims and strong job openings supporting the case for a Fed rate hike. Against this though, small business optimism held steady at a moderate level, wholesale stockpiles rose more than expected and import prices fell more than expected in October. Rising US interest rates at time when Europe and Japan are still easing will only mean a rising US dollar which in turn will mean downwards pressure on US import prices and hence inflation making it harder for the Fed in meeting its objective to get core inflation back to 2%.

In Europe, there was more talk of ECB easing in December and industrial production fell again in September.

Japanese economic data was a bit better with a rise in current conditions according to the Eco Watchers survey and a decent rise in machinery orders in September. The underlying improvement in the Japanese economy is evident in a collapse in Tokyo’s office vacancy rate to 4.5% from 9.4% in 2012.

Chinese economic data was a mixed bag consistent with a stabilisation in growth, but no improvement. Export and import data fell more than expected in October and industrial production slowed a bit further but retail sales, car sales and investment picked up. Sales tax cuts for small vehicles are clearly helping and fiscal stimulus is evident in a 36% rise in fiscal expenditures over the 12 months to October. Credit data was weaker than expected but after adjusting for local government bond issuance still showed an acceleration in terms of annual growth rate. More stimulus is needed though and with non-food inflation of just 0.9%yoy and producer prices falling 5.9%yoy, there is plenty of scope for the PBOC to provide more monetary easing next month (on its easing every two months cycle). Finally a surprise rise in China’s foreign exchange reserves suggests the capital outflows that had been triggered by August’s RMB devaluation have come to an end.

Australian economic events and implications

The past week has seen a run of mostly better Australian economic data, culminating in a blowout jobs report. Business conditions held above average levels according to the latest NAB survey (although confidence is subdued), consumer confidence recovered to long term average levels presumably helped again by the “Turnbull factor” and jobs growth was unbelievably strong. While the October jobs report (+60,000 jobs in one month and unemployment back to 5.9%) was too good to be true, with a payback likely at some point, the underlying trend in jobs growth suggests that the economy is holding up reasonably well helped by a rebalancing away from WA to the population rich states of NSW and Victoria. As a result a December rate cut is now looking very unlikely and we will need to see a run of softer data to get a rate cut early next year now. Meanwhile, housing finance data for September showed a further fall in lending to investors only partly offset by increased lending to owner occupiers.

What to watch over the next week?

While the G20 leaders’ summit in Turkey will no doubt generate lots of coverage, just bear in mind that such events rarely have any real market moving impact (those in the GFC aside). Whatever, happened to the 2% boost to global GDP that was supposed to flow from last year’s summit?

In the US, the minutes from the last Fed meeting (Wednesday) will no doubt be watched closely regarding prospects for a December rate hike but they have been superseded by the strong October jobs report with the market still seeing a 66% probability of a hike by year end. Meanwhile, expect inflation to remain benign at 0.1% year on year for headline and 1.8% yoy for core, industrial production to show a small gain, the NAHB home builder’s conditions index to remain strong at 64 (all Tuesday), housing starts to have fallen back a bit after surging in September but building permits to be stronger (both Wednesday).

The Bank of Japan meets Thursday and is still under some pressure to undertake further monetary easing, but not enough has changed since the last meeting to bring on a move yet. September quarter GDP (Monday) is likely to fall 0.1%qoq.

In Australia, the Minutes from the RBA’s last Board meeting are unlikely to add much given that its Statement on Monetary Policy was released a few days after. Meanwhile, expect the September quarter Wage Price Index to show that wages growth remains very subdued at 0.5% quarter on quarter or 2.2% year on year.

Outlook for markets

After the strong share market recovery through October, a pause or pullback was inevitable as US shares in particular became overbought, some complacency had crept back in and as worries about a Fed driven rise in the $US and its flow on to commodities and emerging market currencies re-emerge. This is now underway and looks like it will have further to go. In contrast to the September quarter though, there is likely to be less concern this time around about China.

But after a messy November share markets are likely to see the normal “Santa Claus” rally into year-end through the last two weeks of the year and the broad trend in shares is likely to remain up. Shares are cheap relative to bonds; monetary conditions are set to remain easy and the Fed is unlikely to do anything to threaten global growth; and this in turn should help see the global economic recovery continue. While it looks distant at the moment, we continue to see the ASX 200 rising to around 5500 by year end.

Low bond yields point to soft medium term returns from bonds, although government bonds remain a great portfolio diversifier.

The broad trend in the $A remains down as the Fed is likely to raise interest rates sometime in the next six months whereas the RBA is more likely to cut rates again than hike them and the trend in commodity prices remains down. This is expected to see the $A fall to $US0.60 in the next year or so.

By Shane Oliver, AMP Capital