What are the frameworks used to quantify the value of advice and the role of trust and transparency in unlocking value.

Introduction

Quantifying and articulating the value of advice has long been one of the biggest challenges facing the financial advice profession. Advice is an ‘intangible’ service where the benefits are not always obvious or immediate. It is also an increasingly expensive service, typically costing several thousand dollars at a time. Having clients – and prospective clients – understand the value they are receiving in exchange for these fees is therefore critical to attracting and retaining clients within the advice ecosystem.

Over the years, many studies have attempted to quantify the value add – the ‘alpha’ – of financial advisers. One of the most longstanding and respected studies is the annual ‘Value of an Adviser’ (VoA) research conducted by Russell Investments, the 2025 edition of which was launched in September of this year[1]. As well as breaking down the advice process into several components, and measuring the value of each, Russell’s 2025 report digs deeper, examining the role of trust as a facilitator of value, the ways a client’s perspective of value can differ from that of their adviser, and how the differing needs of emerging client segments will require a more nuanced approach.

In this article, the first of a series of three examining the findings and implications of the Russell Value of an Adviser report, we will explore the measured Value of Advice (VoA) across 5 key components, from both the adviser and client perspectives. The findings will be compared with those of other studies conducted on this topic – including the FAAA ‘Value of Advice’ study released in 2024. We will also introduce the concept of trust as the bedrock of value in advice, one of the key findings of the Russell report, and the subject of the next article in this series.

Why articulating the value of advice is so important

Despite the obvious life changing financial and emotional benefits of financial advice, most adult Australians do not use the services of an adviser. Indeed, one survey[2] from 2022 estimated just one in six, around 16%, currently use a financial adviser or planner, leaving over 80% unadvised.

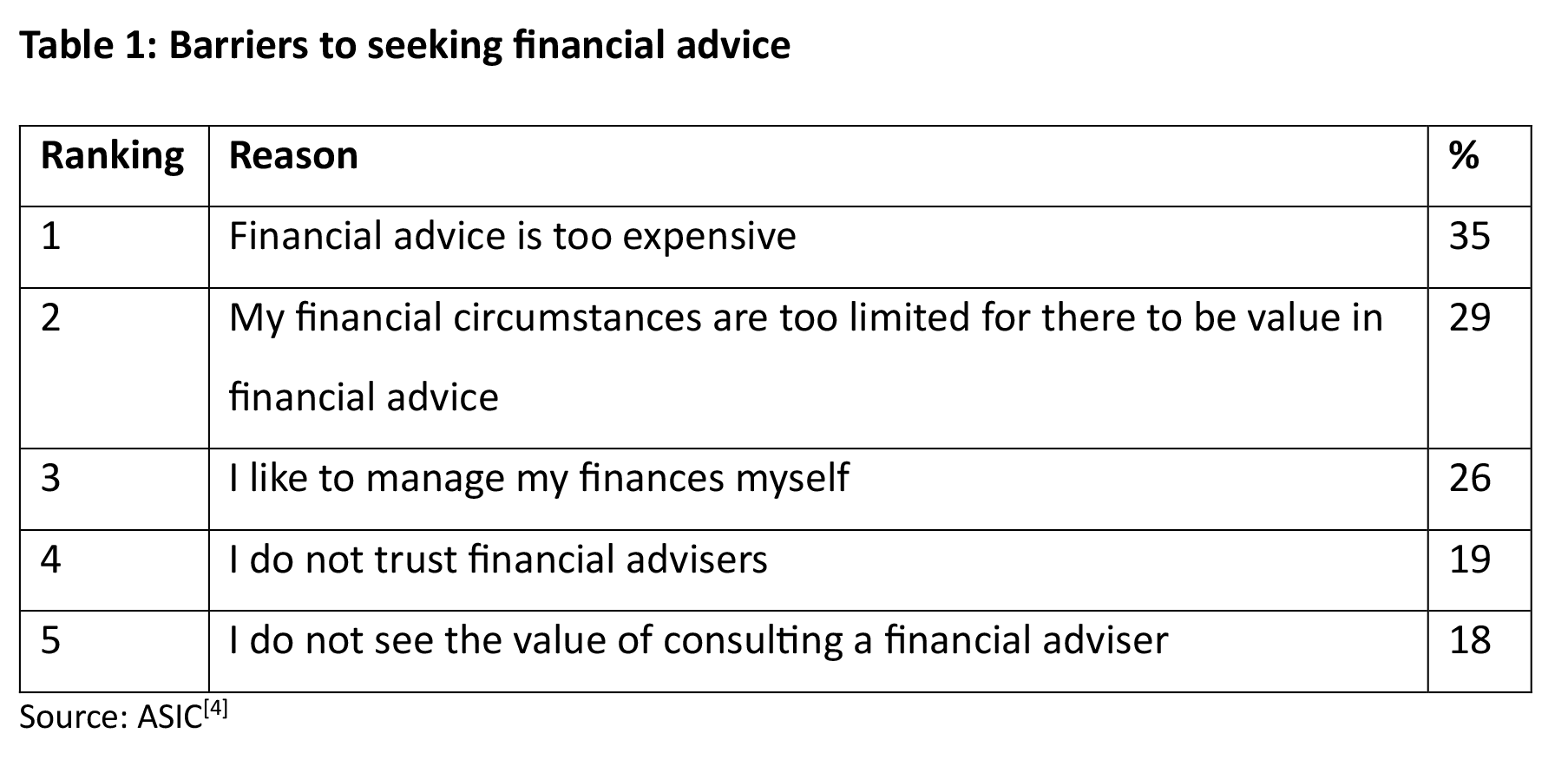

To better understand the barriers to people seeking advice, it is useful to reference the comprehensive study released by ASIC in 2019, via Rep 627 ‘Financial advice: What consumers really think’[3].

Among the questions asked of the respondents was the reasons why they ‘did not or might not’ get financial advice, to which the following responses were the most common:

While the perceived lack of value appears twice in the most mentioned barriers (in reasons 2 and 5), the view that advice is ‘too expensive’ is itself linked to a lack of perceived value. While it is true that for some people the cost of advice is simply unaffordable, assessing a product or service as cheap or expensive is often a construct linked to our perceptions of the value that product or service will provide us.

Value, and perceptions of it, also figure prominently in the factors that cause clients to leave their adviser. According to Morningstar[5], the top reasons clients leave their adviser include:

- the quality of the advice (32%)

- the quality of the relationship (21%)

- the cost of the advice (17%).

To the extent that perspectives on cost and quality are driven by the perceived value added by the financial advice, being able to demonstrate and communicate the value of financial advice is clearly critical to both starting and maintaining client relationships.

The value of advice – what the numbers say

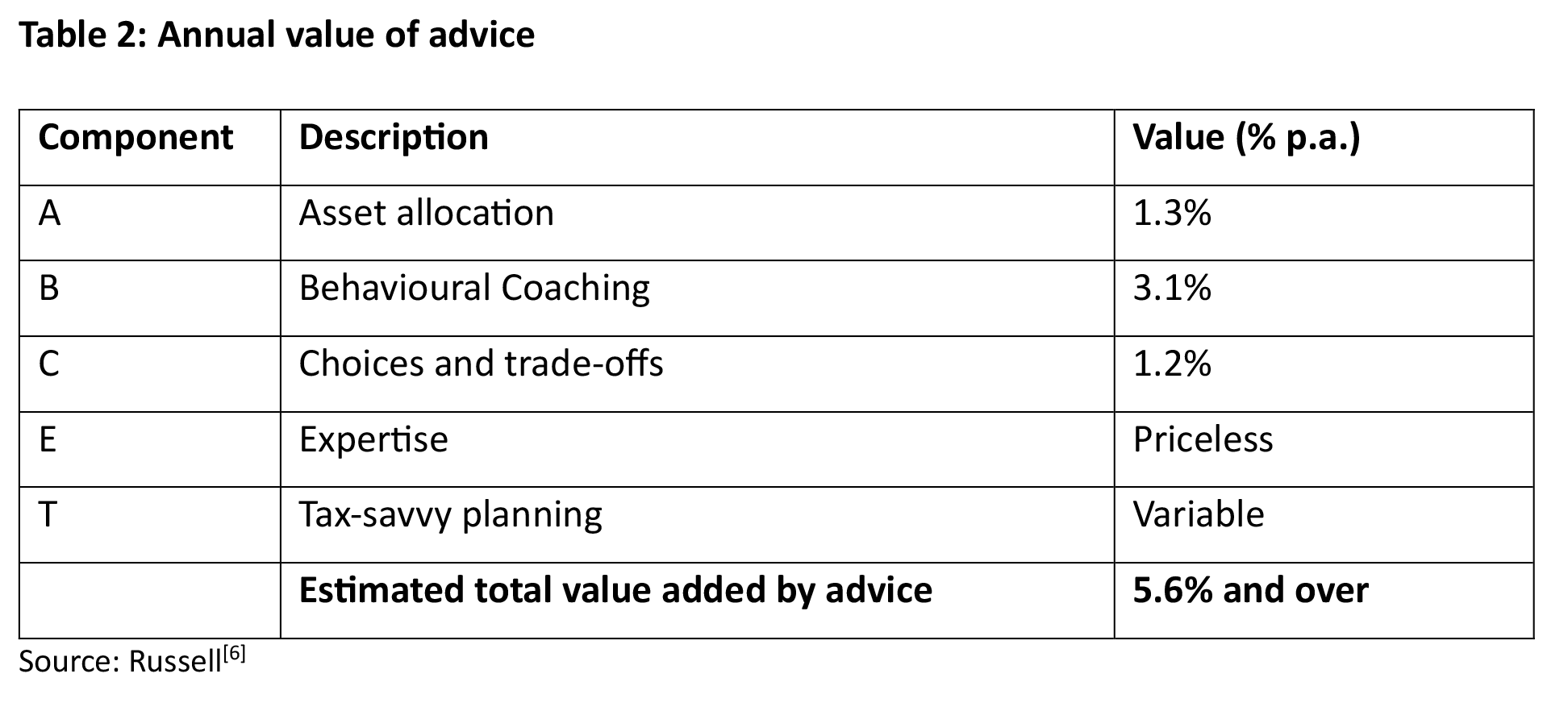

The Russell VoA methodology for quantifying the value of advice is based on a formula which breaks down the components of advice into 5 key areas and then estimates what each component adds, expressed as incremental % returns, or wealth growth, each year.

These components, and the 2025 results, are shown below:

The detail behind the numbers

A: Asset allocation

Asset allocation remains the biggest contributor to long‑term returns, and its influence cannot be underestimated. Against a backdrop of US policy uncertainty, geopolitical tensions, the Deep Seek AI disruption, and stubbornly elevated interest rates, global investment markets continue to shrug off bad news and have quickly returned to their peaks time and time again. Clients in default options within super, or those who are actively defensive, may have asset allocations poorly aligned with their risk tolerance and investment timelines. They are also likely to have left a lot of growth on the table, With Russell quantifying the value of effective asset allocation to be an additional 1.3% return p.a.

Advisers add value by designing portfolios aligned to each client’s risk tolerance, goals and time frame. They often diversify across a broad range of assets to optimise returns while managing risk, ensuring that clients capture market opportunities rather than sit on the sidelines. The following simple case studies demonstrate this point.

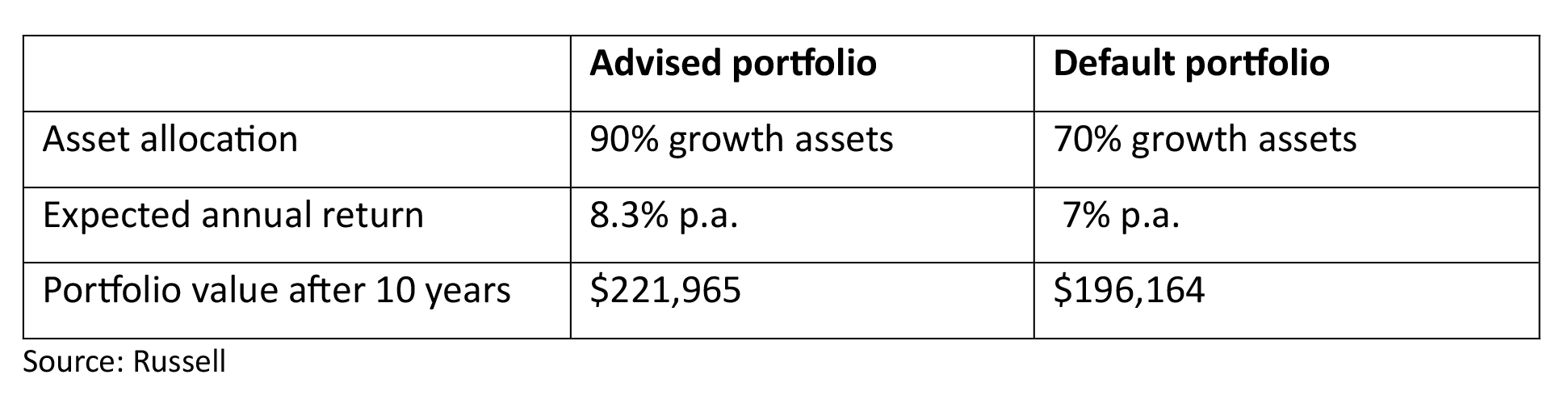

Case study 1- Emma

Emma increased her allocation of growth assets to 90% on her adviser’s suggestion. Based on historic returns her super may grow by an extra 1.3% per annum more than the typical balanced default super fund. Over 10 years this equates to almost $26,000 based on her circumstances.

Case study 2 – Ben

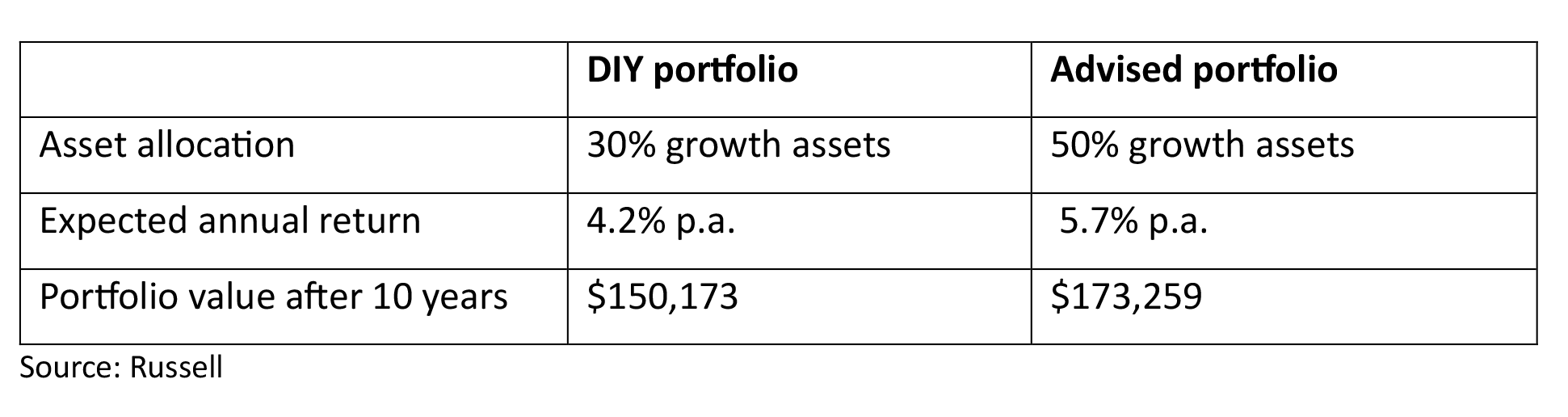

Ben started an SMSF as he liked the idea of control, but he is not an experienced investor and tends to have a more conservative allocation as a result. He holds 70% of the fund’s assets in cash, earning just 4.2% p.a. If he had sought advice and shifted to 50% growth assets (appropriate to his age and retirement plans), he could have achieved annual growth of 5.7% p.a., leaving him $23,000 better off after 10 years.

B: Behavioural Coaching

Renowned investor Benjamin Graham once said: “The investor’s chief problem – even his worst enemy – is likely to be himself.”[7]And indeed, most individuals are poor investors, hostage to complex emotions and behavioural biases that generally see them buy assets when they are expensive (fear) and sell them cheaply (fear). Loss aversion, recency bias, overconfidence and herding behaviour all undermine the ability of ‘amateur’ investors to stay invested and optimise returns.

Aside from buying high and selling low, other common mistakes made by investors include staying out of the market too long (thus missing out on returns) and chasing past winners.

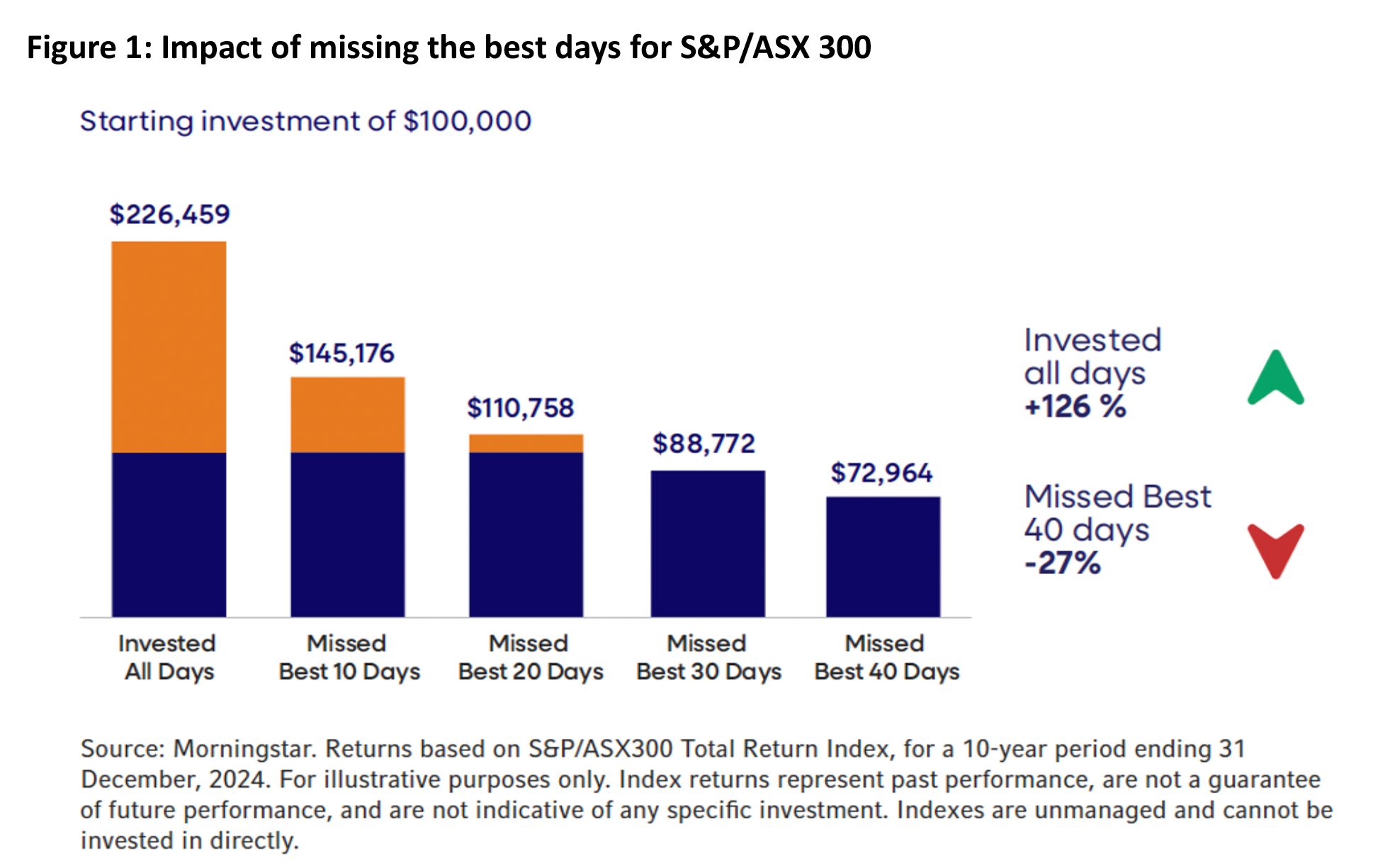

Data suggests the speed of market recoveries seems to be increasing, reinforcing the folly of trying to time market re-entry.

For example, as shown in the chart below (sourced by Russell from Morningstar), missing just the best 10 days of the S&P ASX 300 over the 10 years ended 31 December 2024, would have seen you forfeit around 64% of the total growth achieved over that period. Missing the best 20 days would have cost 91% of the total returns possible. Missing the best 30 days or more would have seen the investor go backwards.

By educating clients about these biases, and the wealth destroying consequences of emotionally charged investment decisions, advisers will be helping their clients stay calm and stay invested, leading to better financial outcomes overall.

Russell’s 2025 survey (of Australian investors) quantified the value of this behavioural coaching at 3.1% p.a. in incremental growth – a substantial amount in anyone’s language.

Other studies have similarly identified significant ‘alpha’ from adviser coaching. For example, Vanguard research[8] estimated an uplift of 1.5% to 2% p.a. from the same source.

C: Choices and trade-offs

Financial advice goes well beyond investments. Life presents a web of challenges: juggling mortgage repayments with HECS debts, supporting ageing parents while raising children, assisting single older women with limited super, or managing the demands of impatient inheritors. Great advisers operate like elite coaches, combining technical knowledge with insight into each client’s personality and motivations. They guide clients through competing priorities and informed trade-offs over a lifetime, from buying a first home to planning aged care and estates.

This value isn’t measured in a percentage return; it shifts with the goals advisers help each person pursue.

E: Expertise

Advisers combine technical expertise with emotional intelligence to build trusted relationships. Their experience spans investing, Centrelink, retirement incomes, estate planning and beyond, giving clients guidance across every stage of life.

Financial products are complex, and the rules governing them shift constantly. Adviser skills are therefore critical when rules change (as regularly happens with super) ensuring client strategies remain optimised. Advisers also step in as advocates during disputes or negotiations (insurance claims for example), allowing families to concentrate on what matters most in difficult times.

With their trust, foresight and advocacy, advisers provide value that cannot be measured in percentages; it is an essential part of the Value of an Adviser formula that gives clients lasting confidence and peace of mind.

T: Tax-savvy investing

Selecting tax optimal structures – across investing, retirement savings, wealth transfer and insurance – is a cornerstone of quality financial advice, extending well beyond negative gearing, capital gains, or personal deductions. Advisers create value by optimising asset allocation across vehicles such as superannuation, investment bonds, family trusts and other structures, while designing tax-efficient strategies that deliver lasting benefits.

Russell’s research estimates advisers add around 1.2% per year through effective tax planning, but it can easily be so much more. Tax rules are complex and constantly shifting. Without expert guidance, it’s easy to misinterpret regulations and incur penalties. Skilled advisers help clients remain compliant while maximising after-tax wealth, a role that delivers measurable and enduring value.

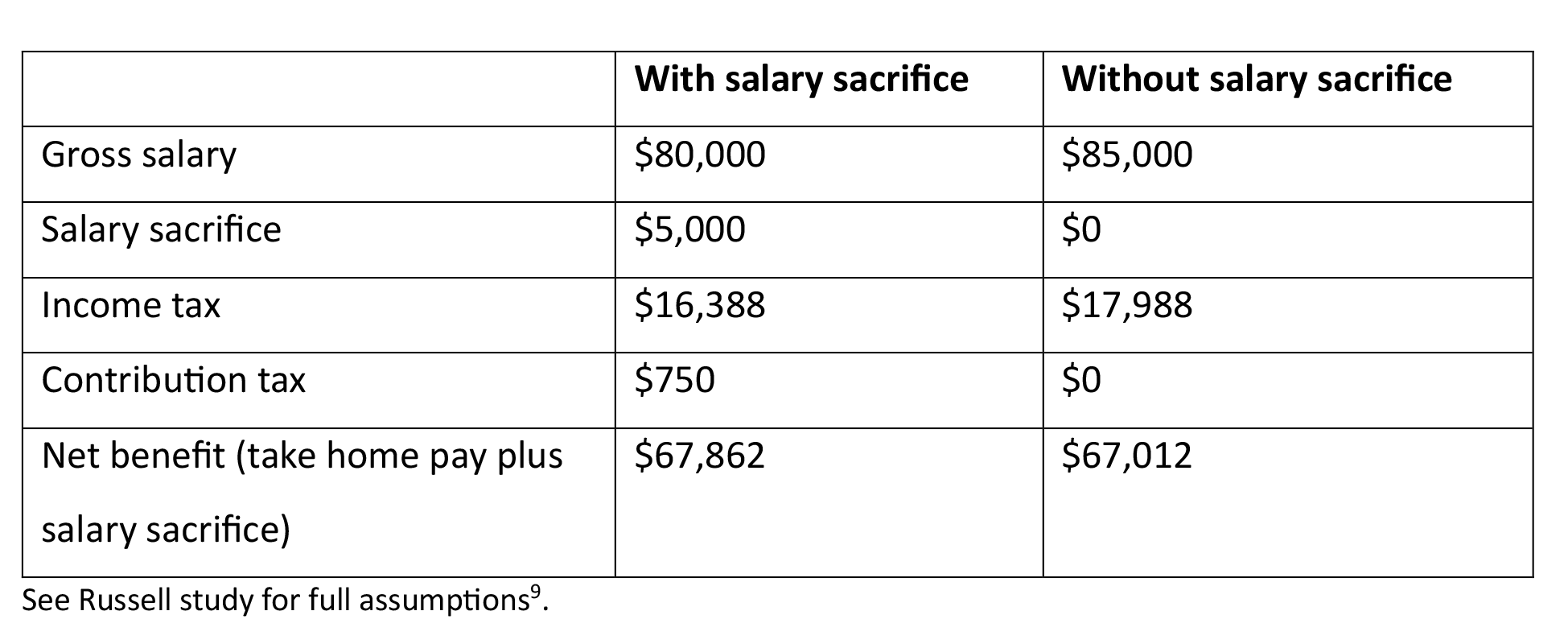

Case study 3 – Sam

Sam’s salary is $85,000. If he sacrifices $5,000 to super, he will pay $750 in contributions tax instead of $1,600 in income tax, giving him $850 more to invest.

The emotional value of advice

To this point we have looked at the functional – quantifiable – value advice can add, measured in terms of its incremental impact on annual growth. But many would argue that the true benefits of advice are emotional, giving clients peace of mind, clarity, a sense of being in control.

The emotional benefits from advice have been extensively researched, with many common themes emerging. Research[10] conducted by Coredata for IOOF (now Insignia) found an advice dividend in areas including:

- Peace of mind and reduced stress

- 88% of advised clients said financial advice freed them from financial worries and stressors

- 95% reported greater peace of mind financially

- Confidence and control

- 92% felt greater control over their financial situation

- 90% had greater confidence in making financial decisions

- Mental and physical health

- One in two advised clients cited direct benefits to their mental health

- Two in five reported benefits to their family life

- Other cited improvements included social life and physical health.

Benefits were also identified in areas such as relationships, happiness, and overall life satisfaction.

The 2024 FAAA Value of Advice Index research[11] found advised clients better off across metrics including Quality of Life, Financial Confidence, and Financial Satisfaction.

More recently Russell’s 2025 study[12] found that advised clients reported the following benefits:

- 89% felt more confident and knowledgeable

- 86% felt more supported in lifestyle and values decisions

- 80% had peace of mind about their finances

- 86% had a structured plan for the future.

By contrast, unadvised clients were less confident, and 76% admitted they would feel more in control if they had expert advice.

Ranking the benefits – the VoA index

For advisers to be able optimally frame their value, it is crucial to understand what aspects of advice have the most impact on client satisfaction, and for this reason, Russell introduced a new metric to their annual study, the Value of an Adviser Index.

Not only does this show what clients value the most from the advice relationship, it also helps shine a light on any variations – or gaps – to what advisers believe clients value the most.

These satisfaction drivers were assessed against each other and then scored against a benchmark level of 100.

Russell found that in 2025, the top drivers of satisfaction were technical and emotional expertise (E) – with a score of 118 – and appropriate asset allocation (A) with a score of 113. These significantly outpaced tax‑savvy planning (T) at 92, behavioural coaching (B) at 91 and choices and trade‑offs (C) at 88.

Readers may be surprised to see that clients didn’t value behavioural coaching as highly as asset allocation, in contrast to its actual measurement which was found to be higher than both asset allocation and tax savvy planning. This variation perhaps reflects the fact that clients are unaware that the calm, reassuring messages, and the encouragement to ‘stay the course’ and ‘stick to the plan’ that their adviser gives them is indeed a form of coaching.

Alternatively, it could simply reflect the overconfidence seen in many amateur investors, who don’t believe they are susceptible to the flawed decision making and biases described earlier. This could explain why the Russell study also found that while 70% of advisers felt they added value by helping clients avoid costly mistakes during periods of market volatility, only 28% of clients recognised this benefit.

Trust and transparency – the bedrock of it all

Russell’s researchers (Honeycomb strategy) identified two dimensions of advice relationships that are the key enablers of advice value – dimensions which effectively unlock the 5-part VoA formula central to their study. These were Trust and Transparency.

Trust emerged as the single biggest driver of client satisfaction, outranking technical expertise and asset allocation.

Fee clarity is another area where perceptions diverge. Clients rate the importance of transparent, easy to understand fees at 8.2 out of 10 but rate advisers’ delivery in this area at 7.9 (advisers rate their own performance in this area at 8.4). Clearly explaining fees without jargon can strengthen trust and reinforce value. Taking time to walk clients through each cost, checking for understanding before moving on, and linking fees to outcomes can build confidence in the advice process.

Why trust matters

Trust is described in the VoA study as the ‘bedrock’ of the advice relationship, and there are many reasons trust is foundational to advice relationships. To the extent that a mistrust of financial advisers is a barrier to individuals seeking advice, then conversely, trust is essential to attracting and retaining clients.

The more information a client shares with their adviser, the more tailored and effective that advice is likely to be. Clients are likely to be more open and forthcoming when they trust their adviser, in contrast to the reservations identified by ASIC in their Rep 627 research:

“Some participants had reservations about providing personal information to someone who is essentially a stranger. A number of participants talked about ‘drip feeding’ or only partially sharing information with financial advisers, until they either built up sufficient trust, or as a means to retain a sense of control”.[12]

Clients who trust their adviser are more likely to accept their recommendations, value their expertise, and respond positively to their coaching and reassurance during market turbulence. They are also more likely to refer/recommend that adviser to their friends and other family members.

Trust becomes even more crucial in certain client scenarios. Retirement is one such example, and indeed 40% of both advised clients and unadvised investors say it is the single biggest reason to seek advice14. When pre-retirees meet with an adviser for the very first time, it is likely that they are entrusting them with the largest asset they have outside of their home. Their retirement savings will underpin their quality of life for the next 30 years or more, so growing it and protecting it are crucial. Clients in these circumstances will understandably exhibit a higher degree of vigilance when choosing an adviser.

Trust isn’t one dimensional or organic. It’s not enough to simply ‘be trustworthy’. Trust needs to be systemised, built into your processes and communication. Building trust with different client segments requires different strategies and approaches. It is not a case of one-size-fits all. And it is hard won but easily lost, meaning it needs to be constantly worked at.

The next article in this series will take a more in depth look at trust and transparency as drivers of value in advice.

Conclusion

Financial advice delivers substantial and multifaceted value, both quantifiable and intangible. From the measurable uplift in portfolio performance through asset allocation, behavioural coaching, and tax-savvy strategies, to the life-shaping guidance advisers provide in navigating complex choices, the benefits of advice extend well beyond dollars and percentages. Just as importantly, there are emotional dividends, including peace of mind, confidence, and a sense of control, which underscore why advice is not merely a service, but an essential partnership in achieving life goals.

Ultimately, the foundation that unlocks the full spectrum of this value is trust. Trust fosters openness, strengthens the advice relationship, and enables advisers to guide clients through both financial and emotional uncertainties. For advisers, building and maintaining trust through transparency, empathy, and demonstrated expertise is not just a professional obligation, it is the bedrock of enduring client relationships and sustainable business success. As the profession continues to evolve, those who can effectively articulate, deliver, and reinforce the value of advice will be best positioned to grow, thrive, and make a meaningful difference in the financial and personal wellbeing of their clients.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Client Care & Practice (0.5 hrs)

ASIC Knowledge Requirements: Financial Planning (0.5 hrs)

please log in to start this quiz

Read the full series:

- CPD: The advice value unlocked by trust – 5.6% and counting – Value of Advice (Part 1)

- CPD: Transparency and communication – making the value of advice visible (Part 2)

- CPD: Futureproof – what different generations really value in advice (Part 3)

———–

References:

[1] https://russellinvestments.com/content/ri/au/en-gb/financial-professional/tools-and-education/business-solutions/value-of-adviser

[2] https://www.finder.com.au/share-trading/financial-advice-statistics

[3] https://download.asic.gov.au/media/5243978/rep627-published-26-august-2019.pdf

[4] Ibid.

[5] https://morningstarinvestments.com.au/why-do-investors-break-up-with-their-financial-adviser/

[6] https://russellinvestments.com/content/ri/au/en-gb/financial-professional/tools-and-education/business-solutions/value-of-adviser

[7] https://faculty.haas.berkeley.edu/odean/Video%20Transcripts/Individual%20investors%20part%201%20heuristics.pdf

[8] https://www.vanguard.ca/content/dam/intl/americas/canada/en/documents/gas/quantifying-your-value-to-clients-adviser.pdf

[9] https://russellinvestments.com/content/ri/au/en-gb/financial-professional/tools-and-education/business-solutions/value-of-adviser

[10]https://www.bridges.com.au/content/dam/bridges/docs/the-true-value-of-advice-research-paper.pdf

[11] http://faaa.au/wp-content/uploads/2024/09/FAAA-Value-of-Advice-2024-Report.pdf

[12] https://russellinvestments.com/content/ri/au/en-gb/financial-professional/tools-and-education/business-solutions/value-of-adviser

[13] https://download.asic.gov.au/media/5243978/rep627-published-26-august-2019.pdf

[14] https://russellinvestments.com/content/ri/au/en-gb/financial-professional/tools-and-education/business-solutions/value-of-adviser

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Client Care & Practice (0.5 hrs)

ASIC Knowledge Requirements: Financial Planning (0.5 hrs)

please log in to start this quiz

Read the full series:

- CPD: The advice value unlocked by trust – 5.6% and counting – Value of Advice (Part 1)

- CPD: Transparency and communication – making the value of advice visible (Part 2)

- CPD: Futureproof – what different generations really value in advice (Part 3)