CPD: Discretionary trusts, testamentary trusts and tax

Understand detailed insights into the function and best application of discretionary and testamentary trusts to manage tax matters for your clients.

Trusts are often perceived as tools exclusively for the extremely wealthy. However, they are accessible to a broad spectrum of clients and serve numerous purposes, most notably effective tax management. This article, which examines the strategic relationship between trusts and tax, is proudly sponsored by Allianz Retire+.

In the complex ecosystem of Australian wealth management, trusts stand out as one of the most powerful and versatile tools for asset protection, succession planning and, critically, tax-effective income distribution. For individuals and families seeking to manage wealth across generations or structure a business with maximum flexibility, a foundational understanding of trust mechanics is essential.

While various trust structures exist, two types of trust command particular attention due to their unique features and distinct tax implications: the discretionary trust (featured in this article, with a focus on family trusts) and the testamentary trust. The former is established during a person’s lifetime to govern ongoing business and investment activities, while the latter is a unique structure established via a Will, taking effect only upon death.

Successfully navigating the use of these trusts – from establishment and ongoing administration to crucial year-end resolutions – is vital to mitigate risk, maximise the tax advantages and ensure the financial wellbeing of beneficiaries.

Trust mechanics

A trust is a legal arrangement where a person or entity (the trustee) holds and manages property or assets for the benefit of designated individuals or entities (the beneficiaries). This structure is a highly versatile tool; it provides benefits in asset management and protection, estate planning and tax optimisation.

While a trust is generally not considered a separate legal entity, it is treated as a taxpayer entity for all tax administration purposes. The flexibility and control trusts offer over asset management and distribution make them invaluable tools commonly employed in investment and estate planning, as well as business contexts.

A trust is an obligation imposed on a person or other entity to hold property for the benefit of beneficiaries. It should have its own tax file number, which the trustee uses when it lodges income tax returns for the trust. A trust is also entitled to an Australian Business Number if the trust is carrying on an enterprise.

Each Australian state and territory has its own specific trust legislation that governs the creation, administration and termination of trusts. The jurisdiction of a trust is therefore determined by the laws of the state or territory under which it is established, generally specified in the trust deed. However, it’s important to note that federal legislation overrides state legislation for complying superannuation funds.

There are two main parties in a trust, the trustee and the beneficiaries. You may also see reference to the settlor, who is the person who creates the trust and transfers property or assets into it.

Key parties and obligations of those parties

The trustee, who can be an individual or a company (known as a corporate trustee), is the central figure responsible for managing the trust’s assets.

The trustee is legally bound to manage the trust property according to two key documents: the trust deed – which outlines the intentions of the settlor – and relevant laws, including all tax legislation.

Under trust law, trustees are personally liable for the debts of the trusts they oversee. However, they are generally entitled to be indemnified from the trust property for liabilities incurred when acting properly within their powers. This right to indemnity is forfeited if a breach of trust has occurred.

Under tax law, the trustee manages the trust’s entire tax affairs. This includes:

- Registering the trust within the tax system

- Lodging the required trust tax returns

- Paying certain tax liabilities on behalf of the trust

The beneficiaries are the individuals or entities entitled to receive the benefits of the trust, which typically include distributions of income or capital.

Beneficiaries can be a broad range of parties, including:

- Individuals (for example, family members)

- Companies

- Other trusts

A trustee may also be named as a beneficiary. However, a key rule to ensure the trust remains valid is that the same person cannot be the sole trustee and the sole beneficiary. This conflict of interest is avoided if there are multiple trustees.

Tax and trust earnings

For tax purposes, a trust is treated as a distinct taxpayer entity. However, the burden of taxation is generally passed on: the way the trust’s income is taxed depends primarily on the beneficiaries’ entitlements to that income. If there is no beneficiary presently entitled to trust income, the trust can accumulate income, but the trustee must pay tax on it at the highest marginal rate. This ensures the trust’s purpose, to distribute income to beneficiaries, is fulfilled.

Distribution principle: Trusts typically distribute their annual earnings to beneficiaries. The beneficiaries are then taxed on their respective share of the trust’s net income, even if the cash has not yet been physically paid. This is known as present entitlement.

Calculating net income: The trust’s net income – the amount taxable in the beneficiaries’ hands – is calculated according to tax law: it is the assessable income minus allowable deductions. This calculation is performed as though the trustee were a resident of Australia, regardless of their actual residency status. Crucially, these two amounts may differ because trust income is defined by the trust deed while net income is defined by tax law.

Trustee responsibility: The trustee is responsible for all administrative tax matters, including lodging the trust’s tax return and ensuring overall compliance.

The structure of trust taxation allows for strategic tax management:

Proportional taxation: A beneficiary is taxed on their proportionate share of the trust’s net income. For example, a beneficiary entitled to 50% of the income is taxed on 50% of the net income.

Streaming concessions: Special rules apply to specific income types like capital gains and franked distributions or dividends. If permitted by the trust deed, these amounts can be streamed to particular beneficiaries. This is often done to optimise tax management; for example, allocating franked dividends to those beneficiaries who have the highest marginal tax rates.

Capital Gains Tax (CGT) and trusts

Trusts have specific and complex rules governing Capital Gains Tax (CGT), which significantly impacts how gains and losses are managed and taxed.

When a trust sells an asset and generates a capital gain, that gain is typically included in the trust’s net income and then distributed to beneficiaries in proportion to their respective entitlements.

Trustee liability: If there is no beneficiary legally entitled to the income generated by the capital gain, the trustee is taxed on that gain. Notably, if the trustee is taxed at the highest marginal rate, the 50 percent CGT discount is generally forfeited.

Net capital losses: A net capital loss generated by the trust cannot be distributed to beneficiaries. Instead, it must be carried forward and used to offset the trust’s future capital gains.

Specific entitlement: For strategic tax management, a trust can utilise the concept of ‘specific entitlement.’ This allows the capital gain to be allocated directly to a particular beneficiary. In this scenario, the capital gain is calculated for that beneficiary with the benefit of any applicable CGT discounts or concessions they may be entitled to.

Case study – specific entitlement

This example demonstrates how the power of streaming capital gains can impact the tax positions of different beneficiaries.

A trustee derived the following amounts in the 2023–24 income year:

- interest income of $100

- a capital gain of $200 that is eligible for the CGT 50% discount

The trust deed defines income to include capital gains. The income of the trust estate is therefore $300, comprised of $100 interest income + $200 capital gain.

When the 50% CGT discount is applied, the net income of the trust is $200 – $100 interest income + $100 net capital gain.

Assuming the trust deed does not prevent the trustee streaming capital gains, the trustee can make:

Beneficiary B specifically entitled to the $200 capital gain

Beneficiary A presently entitled to the remaining $100.

Beneficiary B has a $100 capital gain to consider in working out their own net capital gain. Because the gain was a discount capital gain, Beneficiary B must gross it up (double it) and apply the CGT discount (assuming they qualify for the CGT discount in their own right).

Beneficiary A has a $100 share of net income.

If the trustee did not stream the capital gain, Beneficiary A is presently entitled to one third of the income of the trust estate and Beneficiary B is presently entitled to two-thirds (because of their specific entitlement to the capital gain).

Consequently:

- Beneficiary A is assessed on $33 net income and has a capital gain of $34

- Beneficiary B is assessed on $66 net income and has a capital gain of $67

Source: ATO

Absolute entitlement: The principle of ‘absolute entitlement’ is highly significant for CGT purposes. A beneficiary is deemed ‘absolutely entitled’ to a trust asset if they have a ‘vested and indefeasible’ interest in the entire asset[1]. This means they have the power to demand the trustee immediately transfer the asset to them or to a third party. Where this rule applies, the asset is treated as if it were owned directly by the beneficiary, not the trustee.

Any CGT event that occurs in relation to that asset is considered to have been undertaken directly by the beneficiary rather than the trust. As a result, any capital gain or loss is made directly by the beneficiary and does not form part of the trust’s net income, simplifying the trust’s taxation of that asset.

Tax returns and payments

The trustee is required to lodge a trust income tax return, irrespective of the amount of net income involved, unless advised otherwise by the ATO. If the trustee is liable for tax, they will receive an income tax assessment as trustee; this is separate to their own assessment as an individual or corporate tax entity.

The beneficiaries (or the trustee when assessed on their behalf) may have to pay regular tax instalments based on their share of the trust’s instalment income.

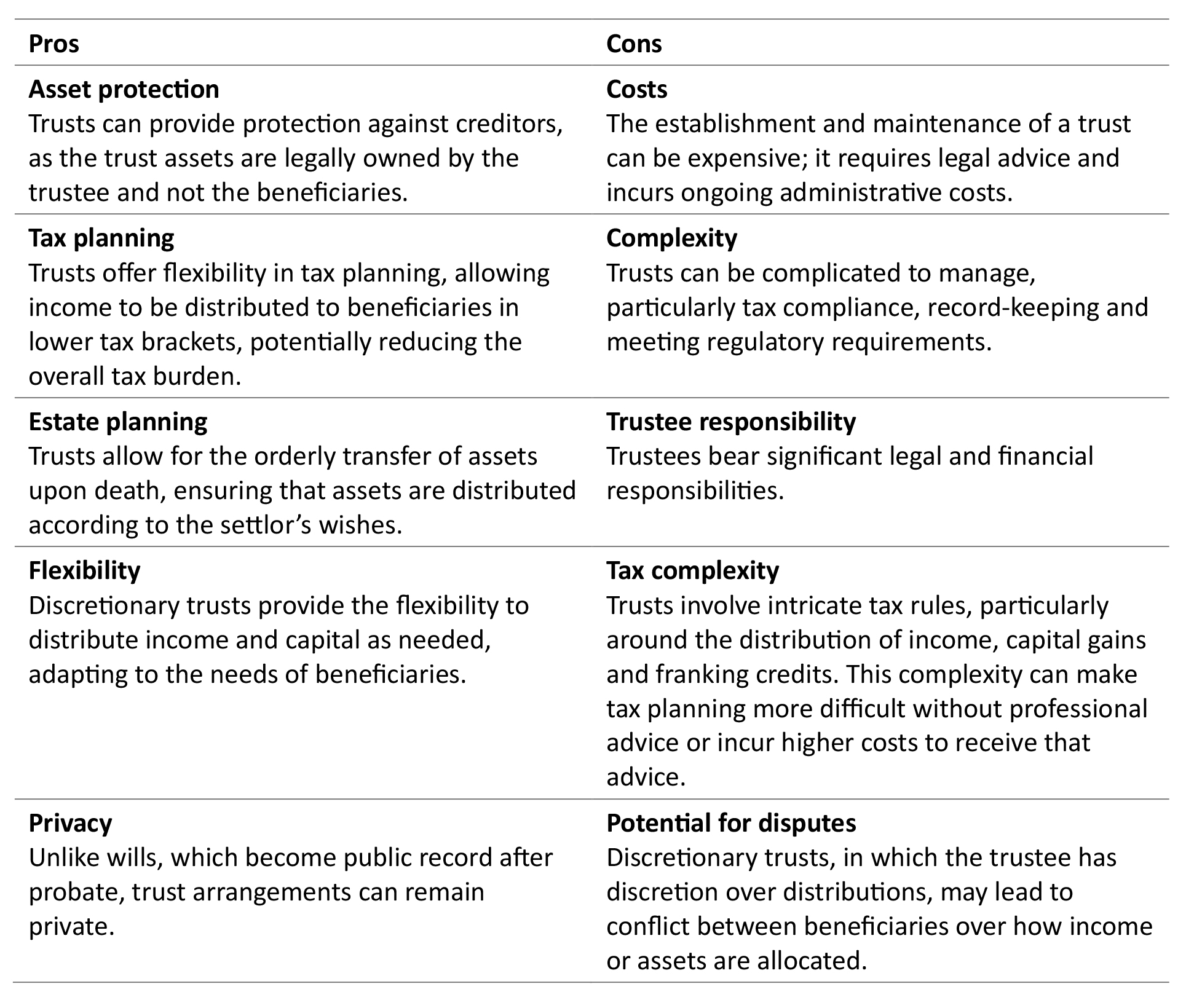

Pros and cons of trusts

The following table details some of the advantages and disadvantages of the trust structure but is not an exhaustive list. Specific client circumstances could impact whether certain trust features are advantageous or disadvantageous, particularly from a taxation perspective.

Discretionary Trusts

A discretionary trust is a legal arrangement where a trustee holds assets for beneficiaries, and that trustee has the sole discretion over who receives income or capital, and how much they receive.

A family trust is a type of discretionary trust but has a specific structure for the benefit of a family group. While the trustee has the power to decide how to distribute income and assets among beneficiaries of a discretionary trust, a family trust restricts this to immediate family members and is often used for asset protection and tax planning for family groups. When a trust makes a ‘family trust election’, it is recognised as a family trust; this confers certain tax advantages but also specific tax obligations. Given the wide use of family trusts in tax planning, this article will focus on that class of discretionary trust.

Family trusts explained

Because it’s typically a discretionary trust, a family trust gives the trustee the power to decide how and when to distribute both income and capital among the designated beneficiaries. The beneficiaries are generally members of the same family group, and their entitlement to distributions is entirely at the trustee’s discretion. This inherent flexibility is the core advantage, enabling strategic financial planning and optimal management of tax liabilities.

To establish the trust, a trustee is appointed. This may be either an individual or a corporate entity. Many families opt for a corporate trustee due to significant advantages, including enhanced asset protection, limited liability and smoother succession planning. The trust’s operation is governed by the trust deed, which serves as the foundational document outlining management procedures, beneficiary classes and the rules for making distributions.

A key step in maximising the tax utility of a family trust is making the Family Trust Election (FTE) to the Australian Taxation Office (ATO). The FTE qualifies the trust for certain tax concessions, particularly those related to the utilisation of trust loss provisions.

There is, however, a counterbalance to the FTE. This is the requirement to distribute only within the defined ‘family group.’ Any distribution made to an individual or entity outside this specific group may trigger Family Trust Distribution Tax (FTDT). This tax is levied at the highest marginal rate plus the Medicare levy, making compliance with the family group rule essential for effective tax planning.

Why use a family trust?

The most common reasons for setting up a family trust include:

- Asset protection: by holding assets in a trust, families can protect them from potential creditors or legal claims against individual family members. If a family member faces financial difficulties, the assets held by the trust are not considered part of their personal estate which provides a level of legal insulation.

- Tax planning: family trusts offer considerable flexibility when it comes to tax planning. By distributing income to beneficiaries with lower marginal tax rates, families can minimise the overall tax burden. For example, a trustee might allocate more income to a beneficiary who earns less or is not employed.

- Investment and business planning: many families use trusts to hold investments or business assets. For instance, if a family trust owns a commercial property, the rental income can be distributed in a tax-efficient way. Family businesses are often structured as trusts, offering both asset protection and tax benefits.

- Succession planning: a family trust can be an effective tool for estate and succession planning. Rather than transferring assets directly to heirs, which could trigger capital gains tax (CGT) or stamp duty, the assets remain in the trust, allowing beneficiaries to continue to enjoy the benefits, such as income from shares or property investments.

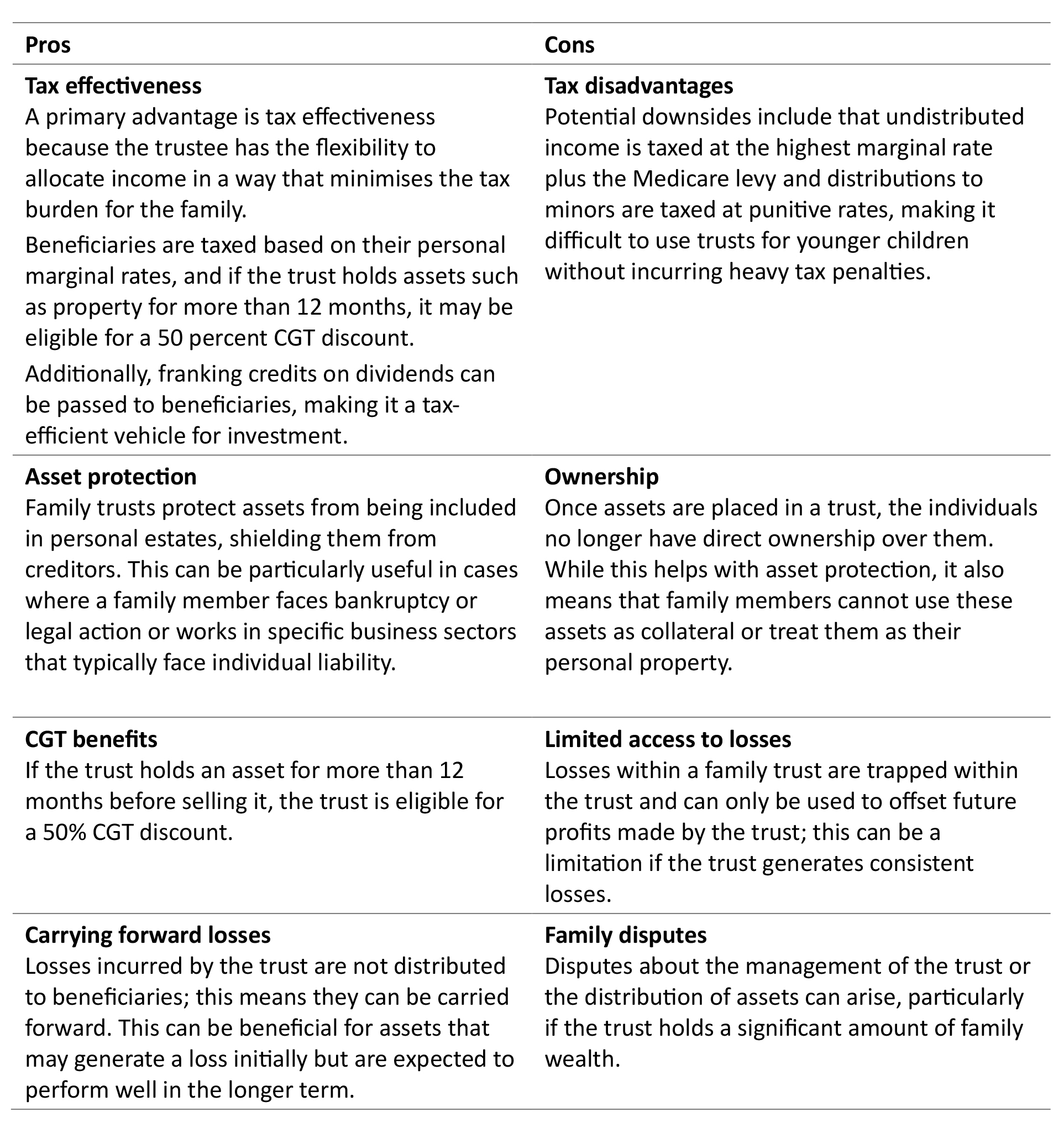

Pros and cons of family trusts

As with trusts more generally, specific client circumstances could impact how advantageous or disadvantageous certain family trust features can be.

Family trusts are effective tools used for tax planning, asset protection, and succession planning. Their primary advantage lies in giving trustees the flexibility to manage income distributions in a tax-efficient manner, offering advantages that other structures often lack.

Family trusts are effective tools used for tax planning, asset protection, and succession planning. Their primary advantage lies in giving trustees the flexibility to manage income distributions in a tax-efficient manner, offering advantages that other structures often lack.

Despite their benefits, family trusts can present certain challenges, particularly the need for careful ongoing compliance and the potential for disputes among beneficiaries. To ensure the trust meets its financial objectives while strictly adhering to legal regulations and tax obligations, careful planning and meticulous management are critically important.

Testamentary trusts

A testamentary trust is established through a will and only comes into effect after the will-maker – or testator – has passed away. Its main function is to control how assets from the deceased’s estate are distributed to beneficiaries.

Unlike a standard bequest, where assets are passed directly to the heirs, a testamentary trust holds these inherited assets under the control of a trustee. This trustee is legally bound to manage and distribute the assets strictly according to the terms outlined in the deceased’s will. This structured approach provides distinct legal, financial and tax advantages, making the testamentary trust a highly attractive option for effective estate planning.

Testamentary trusts explained

The creation of a testamentary trust formally occurs upon the death of the testator and only after the estate administration process has been completed. At this point, assets from the estate are legally transferred into the trust, where the trustee then manages them for the benefit of designated beneficiaries. These beneficiaries can include minor children, family members with specific needs, or individuals requiring financial protection.

Testamentary trusts may be structured as fixed trusts, where each beneficiary’s entitlement is predetermined, or, more commonly, as discretionary trusts. The discretionary form is preferred because it grants the trustee the flexibility to distribute income and capital among beneficiaries based on their current needs and prevailing tax circumstances. This high degree of discretion makes the testamentary trust, especially in its discretionary form, an invaluable tool for optimal long-term tax planning.

Why use a testamentary trust?

While testamentary trusts are primarily used to manage the distribution of assets to beneficiaries after death, they also serve several other key purposes:

- Tax efficiency: testamentary trusts can provide significant tax advantages, particularly when distributing income to minors. Normally, income distributed to children under the age of 18 is taxed at penalty rates to prevent parents from diverting income to lower-tax-rate children. However, testamentary trusts are an exception to this rule and minors who receive income from a testamentary trust are taxed at adult tax rates, which are typically much lower, and use can be made of the tax-free threshold. This provision allows families to reduce the overall tax burden on estate income and improve tax efficiency across family members.

- Asset protection: a testamentary trust can protect estate assets from creditors, legal disputes and family law claims. Because the beneficiaries do not have direct ownership of the trust’s assets – only an entitlement to income and distributions determined by the trustee – those assets are often shielded from legal action taken against the beneficiaries, such as bankruptcy or divorce settlements.

- Control over asset distribution: testamentary trusts allow the testator to retain control over how and when assets are distributed to beneficiaries. This is particularly useful to ensure that minors or financially irresponsible heirs do not receive large sums of money all at once. The trust can specify conditions for when beneficiaries can access their inheritance, such as reaching a certain age or meeting milestones, such as completing tertiary education.

- Long-term estate management: where an estate includes assets that require ongoing management, such as investments or property, a testamentary trust can ensure these assets are managed professionally and in the best interests of all beneficiaries. The trustee – who may be a family member, professional adviser or financial institution – oversees the investment and distribution of trust assets in accordance with the testator’s wishes.

A note on tax effectiveness

Tax efficiency is one of the most compelling reasons to establish a testamentary trust. Testamentary trusts allow for income splitting among beneficiaries, particularly those in lower tax brackets, thereby minimising the overall tax paid on estate income. By distributing income to beneficiaries based on their personal tax rates, the trustee can reduce the tax burden on the estate.

As indicated above, a notable tax advantage of a testamentary trust is the concessional treatment of income distributed to minors. Normally, income received by minors from trusts is taxed at penalty rates; however, income distributed to minors from a testamentary trust is taxed at the same rates as adults, which allows families to make use of lower marginal tax rates to their advantage. This can significantly reduce the tax on income derived from assets within the trust, such as rental income or investment returns.

However, it’s important to note that tax concessions are limited to income generated by assets directly transferred into the trust from the deceased’s estate. Income from assets introduced to the trust from external sources, such as gifts or loans, does not qualify for these tax benefits and will be taxed at the higher penalty rates for minors.

Pros and cons of testamentary trusts

As with trusts more generally, specific client circumstances can impact how advantageous a testamentary trust may be.

Testamentary trusts offer a powerful tool for estate planning, providing a robust mechanism for families seeking to protect assets, secure provisions for future generations, and optimise tax outcomes. However, they are not a one-size-fits-all solution; implementing a testamentary trust requires careful planning and consideration to ensure the structure perfectly aligns with the unique needs and circumstances of the family.

In summary, while family and testamentary trusts offer potent structural advantages for asset protection, succession planning and tax efficiency, these benefits are inseparable from the significant legal and tax obligations they impose. Trustees bear a crucial fiduciary duty to manage the trust’s assets and affairs strictly in the best interests of the beneficiaries, while the beneficiaries themselves are responsible for accurately reporting their share of the trust’s taxable net income. Given the complexity involved, particularly in areas such as income streaming and compliance with specific tax rules, any decision to establish or modify a trust structure must be carefully considered and always be guided by specialised professional advice. After all, a trust must operate in full compliance with all relevant legal and tax requirements and ultimately achieve the desired strategic and financial outcomes to be valuable part of a client’s financial and/or estate planning.

Take the FAAA accredited quiz to earn 0.75 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Tax (Financial) Advice (0.5 hrs) and Technical Competence (0.25 hrs)

ASIC Knowledge Requirements: Taxation (0.5 hrs) and Estate Planning (0.25 hrs)

please log in to start this quiz

———–

Notes:

[1] https://www.ato.gov.au/businesses-and-organisations/trusts/trust-income-losses-and-capital-gains/trust-capital-gains-and-losses

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Tax (Financial) Advice (0.5 hrs) and Technical Competence (0.25 hrs)

ASIC Knowledge Requirements: Taxation (0.5 hrs) and Estate Planning (0.25 hrs)

please log in to start this quiz

———–

Notes:

[1] https://www.ato.gov.au/businesses-and-organisations/trusts/trust-income-losses-and-capital-gains/trust-capital-gains-and-losses

Have feedback on this article? Contact Us

Earn CPD Points

CPD: The spectrum of growth

CPD: The spectrum of growthCompanies that generate strong, sustainable growth are valuable sources of long term capital appreciation in a portfolio, but these businesses are rare, difficult to identify and exist on a broad [...]

CPD: Record-keeping in financial advice – the key to compliance and consumer protection

CPD: Record-keeping in financial advice – the key to compliance and consumer protectionIntroduction The financial services regulatory framework is a key pillar of financial consumer protection. Regulatory compliance is therefore not merely about avoiding penalties, but is a critical step in building [...]

CPD: Trust and ethics in financial advice

CPD: Trust and ethics in financial adviceIn 2024, trust in financial advisers reached an all-time high. This article, proudly sponsored by GSFM, explores the inseparable links between trust and ethical practice when providing financial advice. Defined [...]

CPD: Retirement Income Strategies

CPD: Retirement Income StrategiesIt has been almost 40 years since award superannuation was introduced in Australia, and 33 years since the introduction of mandatory occupational superannuation. This means the next decade will see [...]

CPD: Free cash flow works

CPD: Free cash flow worksThe difference between earnings and free cash flow is an important investment concept, one explained here by GSFM’s investment partner TD Epoch. Earnings have long played a dominant role in [...]