Passive investing in EM equity – The most active investment decision that you will make

Emerging markets have complicated governance structures, evolving macroeconomics and immature institutions, which leads them to be dynamic, complex and their stocks volatile.

Passive investment funds have grown in popularity and offer one key benefit, immediate market beta. However, investors beware! A passive approach to investing in emerging markets equity has several explicit and implicit ramifications.

Emerging Markets specialist Ashmore Investment Management, a PAN-Tribal Asset Management investment partner, considers seven in this article.

1. EM equity has significantly evolved

Let’s begin with some context. Emerging Markets (EM) equity market exchanges comprise US$39.9 trillion, which constitutes 32% of the US$124.5 trillion global equity universe[1]. EM have seen significant market expansion, having grown from US$16.3 trillion a decade ago.

As investor confidence in EM has grown and their prominence has increased, the EM equity investable universe has also evolved. EM capital markets have liberalised, broadened and deepened.

Stock markets better reflect underlying economic growth drivers and the diverse opportunity set. This trend has further to go as EM’s market cap to GDP at the end of 2021 is 103%, which compares to 151% for developed markets.

There has been a corresponding expansion in the range and sophistication of approaches to investing in EM. The diagram below represents some of the principal investment options currently available to investors.

2. The elephant in the room

Passive investment funds have grown in popularity, primarily because they offer a means to generate immediate market beta. However, in close second, is likely the perception by fund selectors that the odds of selecting a decent active manager are not in their favour. After all, is there not plenty of published analysis that shows the ‘average’ active manager struggles to outperform the index, especially on a consistent basis?

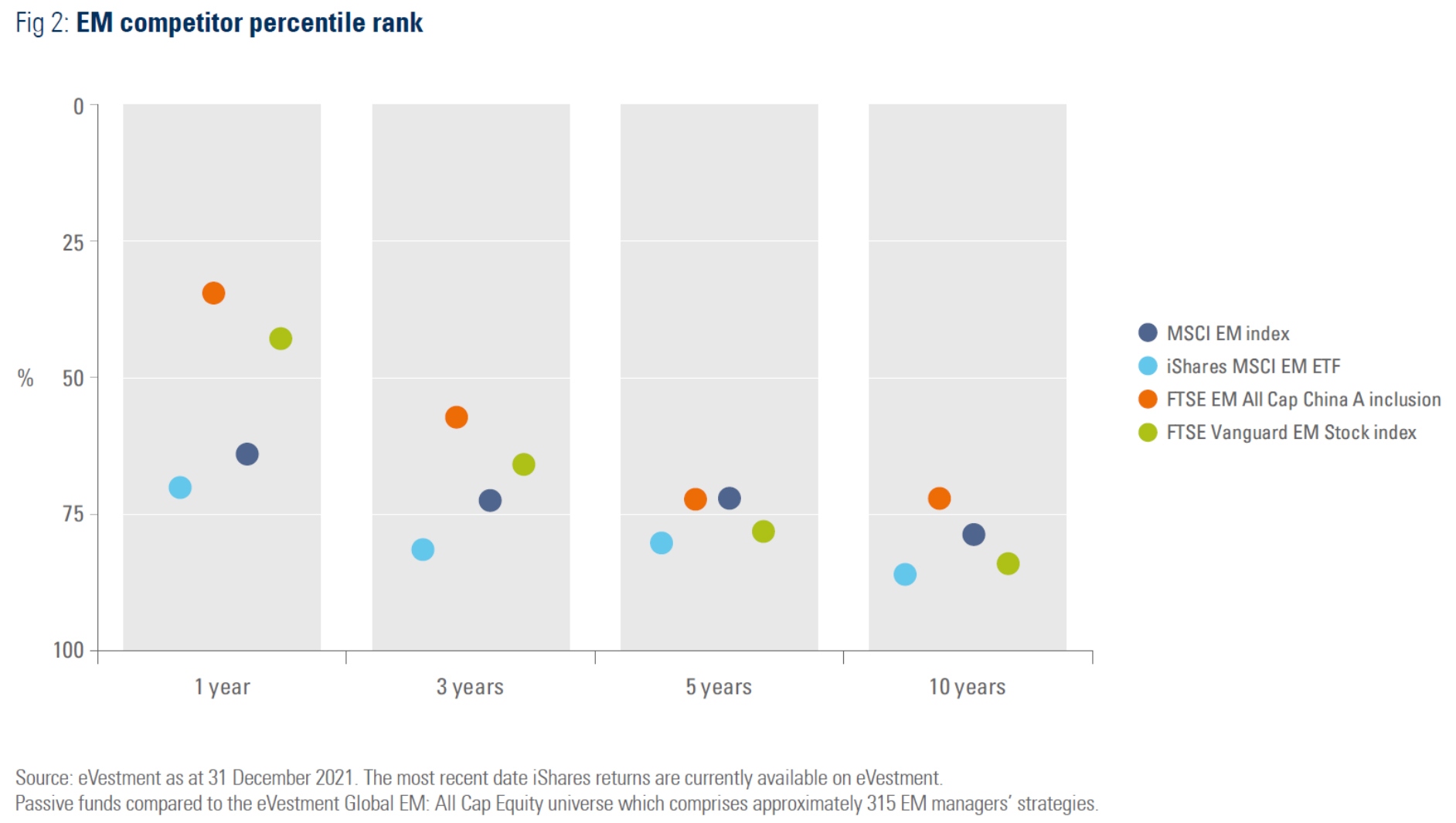

There may be some validity to this statement for active managers focused on the more stable and efficient developed markets. However, manager selection risk looks overstated in EM. Based on the eVestment analysis below, popular index trackers are in or close to the bottom quartile versus the peer group, over any period of length at least.

On this basis, around three quarters of active managers are ahead of trackers from three years and on. Moreover, a degree of manager due diligence should meaningfully increase the odds of picking an above ‘average’ manager.

3. Underperformance

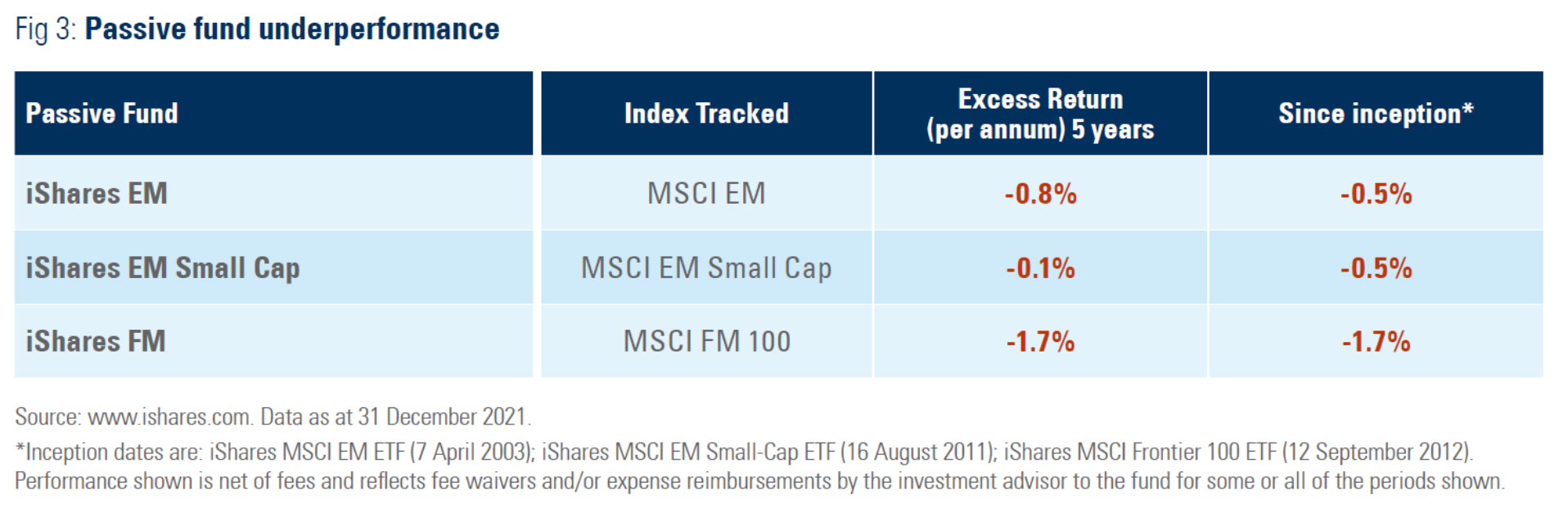

Let us turn now to the most self-explanatory ramification of investing in a passive fund. By virtue of the fact that passive funds are designed to track an index and there is a cost to investment, they will guarantee investor underperformance compared to the index, assuming the tracker can successfully replicate the performance of the index.

While passive fund costs have reduced for an EM index tracker, fees remain high for Frontier Markets and Small Cap trackers. Passive funds also generate high transaction costs given frequent rebalancing and high implied intraday trading premiums/discounts, since passive funds buy what is performing well and sell what is not.

These attributes mean it should not come as a surprise to see passive funds consistently underperform the index they are designed to track. This was clear in Figure 2 where it was clearly illustrated that the tracker underperformed the index across every period. It is also shown in Figure 3.

4. Active allocation decision

Index providers have improved their coverage of the free float adjusted market cap of EM stock markets. However, they continue to omit EM stocks listed overseas, stocks that trade OTC for technical reasons and stocks that do not meet their predefined criteria.

Frontier Markets indices still only provide only a small portion of the available universe.

The increased size and breadth of the EM opportunity has led index providers to carve the EM universe, somewhat arbitrarily, into segments that passive vehicles then seek to replicate. The decision as to which segment the fund seeks to track is the first of several active investment decisions the investor will make when they invest ‘passively’.

In contrast, an active manager has typically much more freedom to select opportunities across geographies and the market cap spectrum.

5. Active selection decision

A passive investment approach favours certain geographies, sectors and stocks. For example, China is approximately 32% of the MSCI EM index and is expected to increase in size over time. Add in South Korea and Taiwan and your MSCI EM passive tracker has 60% focused in three countries at all times. The five largest index stocks in the MSCI EM index are all technology-orientated companies and represent 19% of the total.

The methodology of index construction will also have a direct impact on passive fund exposure. The most common approach is market cap weighted, which disproportionately favours larger cap stocks on a systematic basis and skews investor’s exposure to previously strong performing areas of the market. In the case of EM, it currently leads to disproportionate exposure to state owned enterprises, potentially at the expense of faster growing and more dynamic corporates.

Investing in a passive fund also means an investor is relinquishing their ability to engage with company management, to try to improve a business’ sustainability and to hold company management to account, both on an ESG consideration basis as well as financial performance. The positive feedback loop between underlying investor, active manager and company management is broken.

6. Enhanced indexing/smart beta

As the EM universe has evolved and become more sophisticated, so too have the range of passive approaches available for investors. Enhanced indexing / smart beta are ‘rule based’ approaches that focus on factors deemed attractive, often based on back tested models. However, as highlighted further below, EM’s structural dynamism means it does not necessarily behave according to historical based rules nor back tested models.

7. Significant market inefficiency

The most important failing of a passive approach is not to recognise the significant market inefficiencies that exist in EM, and hence the ample opportunities for alpha generation.

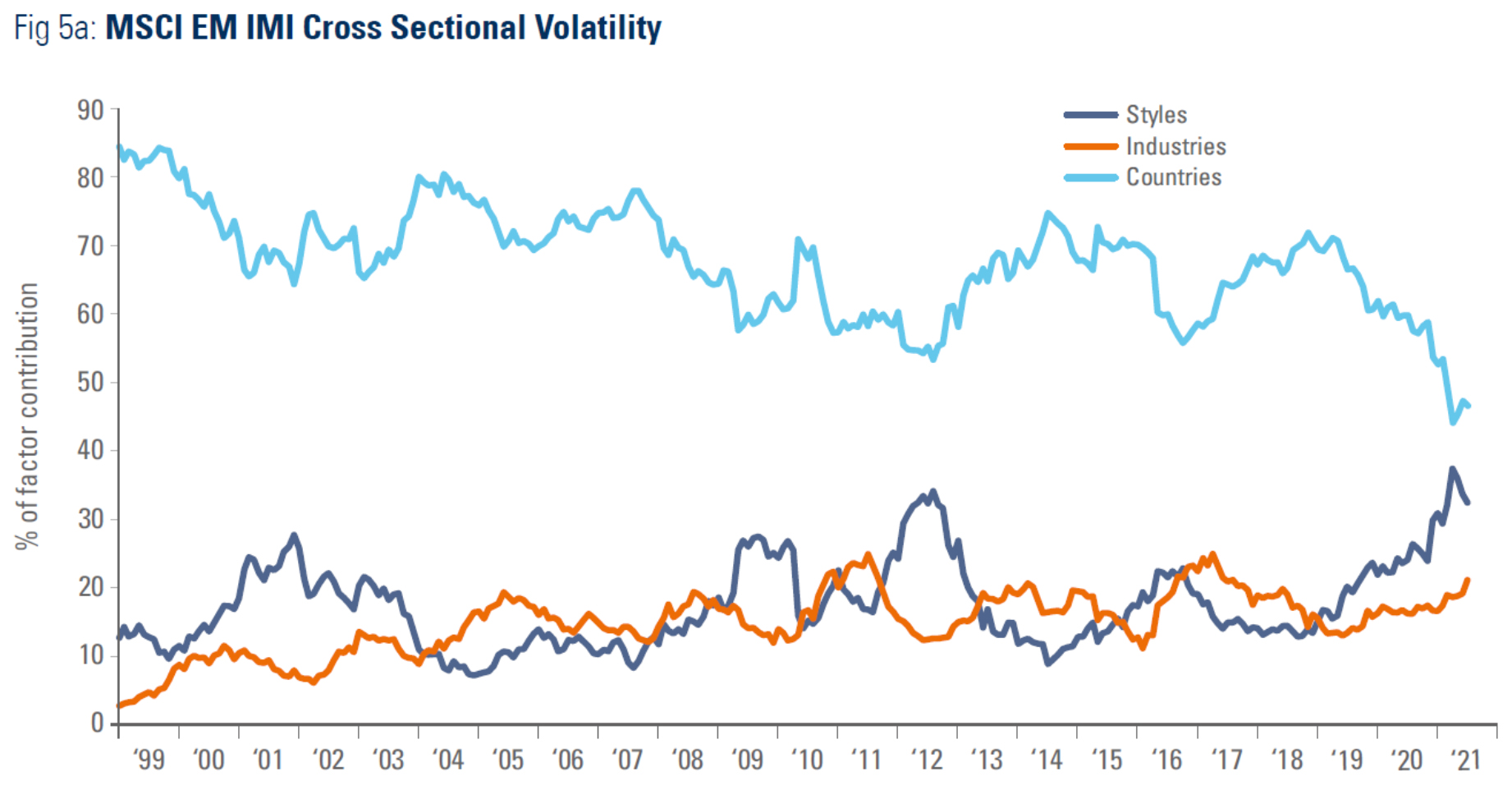

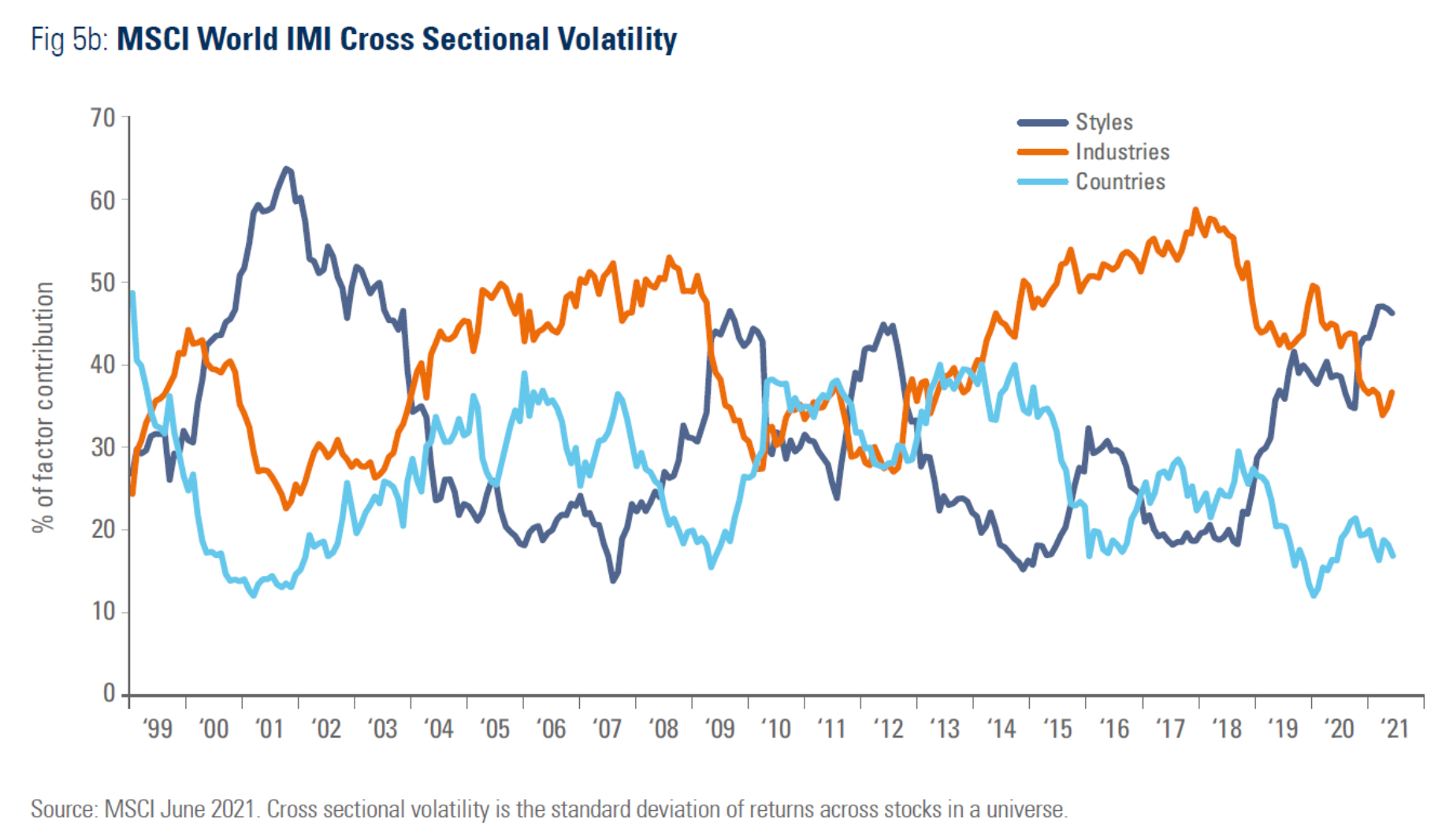

EM, excluding frontier markets, comprise over 20 markets, each at a different stage of development and maturity and each with a different currency and capital market structure. Consequently, EM are more volatile and dynamic compared to developed markets.

It also means EM have multiple drivers and top down factors, at both a country and industry level, play a disproportionately important role driving market returns compared to developed markets. Meanwhile, the dynamic nature of EM means style is not a key driver of returns on a sustained basis and is much less important than more stable developed markets.

EM are now a strategic allocation in global portfolios and are widely held. However, the drivers of EM are still often misunderstood. For example, market factors can disproportionately impact EM stocks and events in developed markets can have an asymmetric, and often irrational, impact on EM price trends and investor behaviour. Note, for example, the selloff in EM due to problems in Greece in 2015, despite no deterioration in fundamentals. The result is excessive EM price volatility relative to risk. This leads to significant pricing inefficiency.

In fact, passive funds themselves are a growing source of market inefficiency and, should they continue to grow in size, could present a systemic risk to markets. Indexing can distort valuations by leading index stocks to trade at higher multiples than off-index stocks. In turn, this can distort market beta and the pricing of risk.

Passive funds are also ‘self-fulfilling’ when they see inflows as they buy stocks they already own. However, this phenomenon reverses if the opposite becomes true on a sustained basis. Moreover, index reclassifications, for example a ‘promotion’ from MSCI FM to MSCI EM, can also lead to meaningful temporary market distortion. Investors target markets and stocks that they perceive will be the recipients of ‘forced’ passive fund buying and then sell post reclassification.

Emerging markets (EM) have complicated governance structures, evolving macroeconomics and immature institutions, which leads them to be dynamic, complex and their stocks volatile. This is good news because it creates significant market inefficiency and the potential for meaningful alpha generation from active management. The important skill is being able to discern between the good companies – those that can sustain strongly positive returns – and the rest.

As EM countries, their economies, policies and market structures, continue to develop and reform, this garners increased confidence among investors and buoys returns. In turn, this drives market liberalisation and improves market depth, or liquidity, which drives more investment. Active rather than passive managers are best placed to deliver positive returns to investors.

———