CPD: Aged care advice and ethics

As Australia’s population ages, the demand for aged care advice will inevitably surge.

Data from the Australian Institute of Health and Welfare (AIHW) shows that Australia’s population aged 65 and over is projected to reach 22% – or 8.8 million people – by 2057, reinforcing the need for specialist aged care advice. This article, proudly sponsored by GSFM, explores some of the issues around ethics and providing financial advice to ageing Australians.

Australia is an ageing nation. One in five Australians are aged 65 and over[1]. That does not include the tail end of the ‘baby boomers’, nor Gen X snapping on their heels. The percentage of the population aged 65 and over has increased from 12% at 30 June 1994 to 17% 30 June 2024[2].

Driven by improved nutrition, medical advancements and healthier lifestyles, Australian life expectancy now extends well into the 80s, underscoring a critical need for structured aged care advice. However, while post-retirement financial planning traditionally prioritises wealth decumulation and immediate lifestyle funding, long-term aged care strategies remain significantly underemphasised.

The aged care system is a complex web of providers, agencies and changing regulations that often overwhelms families during a period of high vulnerability. This makes access to accurate, conflict-free professional advice vital to safeguarding the best interests of older Australians.

The inherent complexity of the Australian aged care system has been amplified by the introduction of the Aged Care Act 2024 and its funding reforms that came into effect on 1 November 2025. In the wake of these reforms, Australians will increasingly rely on personalised guidance to make informed decisions tailored to their unique family circumstances. Professional support will be essential in helping Australians navigate their aged care funding options effectively.[3]

Aged care in Australia

While the aged care system is designed to support older Australians, it remains riddled with complexities and is challenging for families to navigate. These complexities make it difficult to both access the required support and understand the financial intricacies of that support.

There are two main pathways in the system, at-home support and residential aged care, funded by a mix of government support and personal contributions. However, it’s not as simple as making an application – the federal government’s own report, released the same day as the federal budget, revealed that it takes, on average, 12 months to get a spot in an aged care home or secure at-home support[4].

Further, senate estimates figures show that in December 2025, there were more than 230,000 Australians currently on the wait list for aged care, either for an assessment or a package at their approved level.

Care in the home – designed to help older Australians stay independent for longer, the Support at Home program (formerly In-Home Care program) provides a coordinated care plan tailored to meet the recipient’s specific needs. While it sounds great in theory, the application process is onerous and there’s a substantial waiting list for both assessment and allocation of a package.

Care in a residential aged care facility – this provides accommodation, daily care and lifestyle services within an aged care home. This can be a permanent move or a short-term stay (respite care). Permanent care is intended for those who can no longer live at home due to increased care needs.

As most aged care advice focuses on access to and funding residential aged care, in-home support services are not discussed further in this article.

A major reason people access aged care advice is the complexity of the fee structures associated with residential aged care. The following provides a brief overview of the fee structure, which – like many government programs – is subject to regular review and change. Major changes were implemented as part of the Aged Care Act 2024. The same fee structure is applicable whether the aged care facility is run by local or state government, a charitable organisation or corporate.

Aged care fees and the Aged Care Act 2024

The overhaul of residential aged care fees in the Aged Care Act 2024 represented a significant structural shift. The rationale for these changes stems directly from the recommendations of the Royal Commission into Aged Care Quality and Safety and the findings of the Aged Care Taskforce. The core objective was to create a dual-benefit solution: protecting the financial dignity of older Australians while ensuring the entire aged care sector does not collapse under escalating costs[5].

The major change to aged care fees introduced by the 2024 Act is drawing a line between what the government should pay for and what the individual should pay for.

The Act established that health and clinical care is a universal right. Therefore, the government funds 100 percent of clinical care, which includes nursing, medical management and allied health.

However, everyday living and accommodation costs are co-contributed; the rationale is that whether you live in your own home or a residential facility, you still have to pay for food, laundry, utilities and rent.

So, under the new act, the former ‘Means Tested Care Fee’ has been split into two distinct, means-tested categories:

- The hotelling contribution – a co-contribution to daily lifestyle and facility operational costs, capped at $22.15 per day

- The non-clinical care contribution – this covers personal care, such as showering, dressing and leisure activities, capped at $107.32 per day.

A significant change is the introduction of measures to inject capital directly into the infrastructure of aged care homes:

- RAD retention – aged care providers are now permitted to retain a small portion of a resident’s Refundable Accommodation Deposit (RAD). Providers can retain two percent per year for up to five years, a total maximum of 10 percent of the RAD. Given many RADs are over one million dollars, this can represent a sizable amount. This only applies to people entering aged care from 1 November 2025.

- Increased price caps – the maximum room price cap was raised from $550,000 to approximately $750,000 and indexed to inflation. This is the maximum price a provider can charge without seeking approval from the Pricing Authority.

The Act also introduced the ‘no worse off’ principle; anyone who was already in residential care prior to 12 September 2024 is strictly grandfathered. Their contribution arrangements stay exactly the same. As with any change, there are a lot of caveats around the new payments, and which payment applies to what person – this only adds to the already complex structures.

What are the costs?

The following is a summary of the primary aged care fees – specifically, the cost of the room. The reality involves far more complexity and will vary from client to client. This illustrates the importance of personal finance advice when it comes to accessing aged care services.

Prior to moving into a residential aged care home, the resident must agree on a room price with the provider. It’s important to note that prices will vary from one provider to the next. Whether an individual qualifies for government assistance to cover these accommodation costs, in full or in part, is determined by a formal means assessment.

There are three options for payment.

A refundable lump sum (RAD or RAC)

There are 2 types of lump sum, depending on the outcome of your client’s means assessment:

- Refundable accommodation deposit (RAD): This is when your client pays the full amount and is the accommodation price agreed with the provider.

- Refundable accommodation contribution (RAC): This is when the government helps with the costs and is worked out by the provider based on the daily accommodation contribution (DAC).

It is important to know that a refundable lump sum is counted as an asset in the aged care means assessment, even in the event it is paid by a family member. This means that paying a lump sum can affect overall fees charged by the provider.

A daily payment (DAP or DAC)

There are two types of daily payments, depending on the outcome of the client’s means assessment:

- Daily accommodation payment (DAP): this is when your client pays the full amount themselves and is the accommodation price agreed with your provider. Daily accommodation payments are indexed on 20 March and 20 September each year.

- Daily accommodation contribution (DAC): this is when the government helps with the costs; the amount is determined by Services Australia based on the client’s means assessment.

Daily payments are akin to rent payments and are not refunded when your client leaves care.

A combination of refundable lump sum and daily payments

This is when your client combines the two types of payments to meet their costs. The split of the combination can be made in the way that works best for the client’s financial situation.

The financial commitment of residential aged care extends beyond the initial room price. Once a resident moves in, they face ongoing daily fees for accommodation, care and hospitality services. Under the reforms that rolled out from 1 November 2025, the government restructured these fees to increase transparency. At the same time, a stronger user-pays model was introduced, one that scales based on an individual’s personal wealth.

The government’s website My Aged Care provides more information about aged care costs and how they are calculated.

Aged care advice

Access to quality aged care financial advice is incredibly important when it comes to making well-informed aged care decisions. Clients – and often, their families – need to understand the complexities of fees and costs and how to best structure finances to afford the required care.

However, there’s an ongoing problem with aged care advice, one beyond the inherent complexities in accessing and paying for care.

It’s an issue for the broader advice industry as well as extremely challenging for the clients and their families. The issue is this: a substantial amount of ‘aged care advice’ is provided by individuals who are unlicensed, not authorised, not on ASIC’s Financial Adviser Register. It’s provided by a range of people, professionals such as lawyers or accountants, individuals working in the aged care sector or with ancillary services. In some cases, aged care advice is provided by former (i.e. deregistered) financial advisers.

It can be difficult for families to source the right help and to understand the differences in the advice on offer. Are they receiving information only, general advice or comprehensive personal advice?

Information versus advice

In many cases, the ‘client’ is the family of the person entering aged care and the move is often event driven. As the event is often negative – an illness, a fall, the death of a partner – emotions and stress levels can run high.

It is not unusual that the seekers of advice often don’t have the luxury of time or the emotional clarity to check the credentials of someone offering aged care advice, let alone ensure the guidance provided is in their loved one’s best interests.

Of course, there’s a lot of information that can be imparted without crossing the line into advice. This includes:

- explaining aged care fees (including calculations for an individual’s fee scenario)

- explaining Centrelink entitlements

- sourcing appropriate temporary or permanent accommodation.

If the professional in question is simply providing information without affecting any decision making, it’s not advice.

However, once the provider of aged care information influences an action, this likely crosses the line into personal advice. This might include:

- discussing options about how the client could pay for the aged care fees, or

- making recommendations about payment options.

However, even where a recommendation isn’t made, simply influencing the client to decide about a specific option, product or product class falls into the realm of personal product advice. The Corporations Act 2001 outlines two steps to determine whether a person is providing personal product advice:

- The person providing the information or advice knows personal information about the client

- There is a suggestion or inference to make a change in respect to assets or products, or a class of products, and influencing the client’s decision about those assets.

Finding and funding accommodation is usually only the first step in holistic personal financial advice; there is often financial, tax, social security and estate planning considerations. These should be the purview of a registered financial adviser providing aged care advice.

For many consumers, the difference between information and advice is not clear. Decisions can be made in haste when those making them are emotional or vulnerable. Given the expenses associated with aged care, decisions about the advice may be driven by cost without understanding the implications of following a recommended course of action.

Unregistered advisers may be cheaper because:

- they don’t have applicable professional indemnity insurance

- they aren’t members of AFCA, thereby denying their clients an opportunity for redress

- they aren’t required to have memberships of professional associations

- they avoid ongoing educational requirements.

Importantly, an unregistered adviser is not bound by the Financial Planners and Advisers Code of Ethics (Code of Ethics).

Ethics and aged care advice

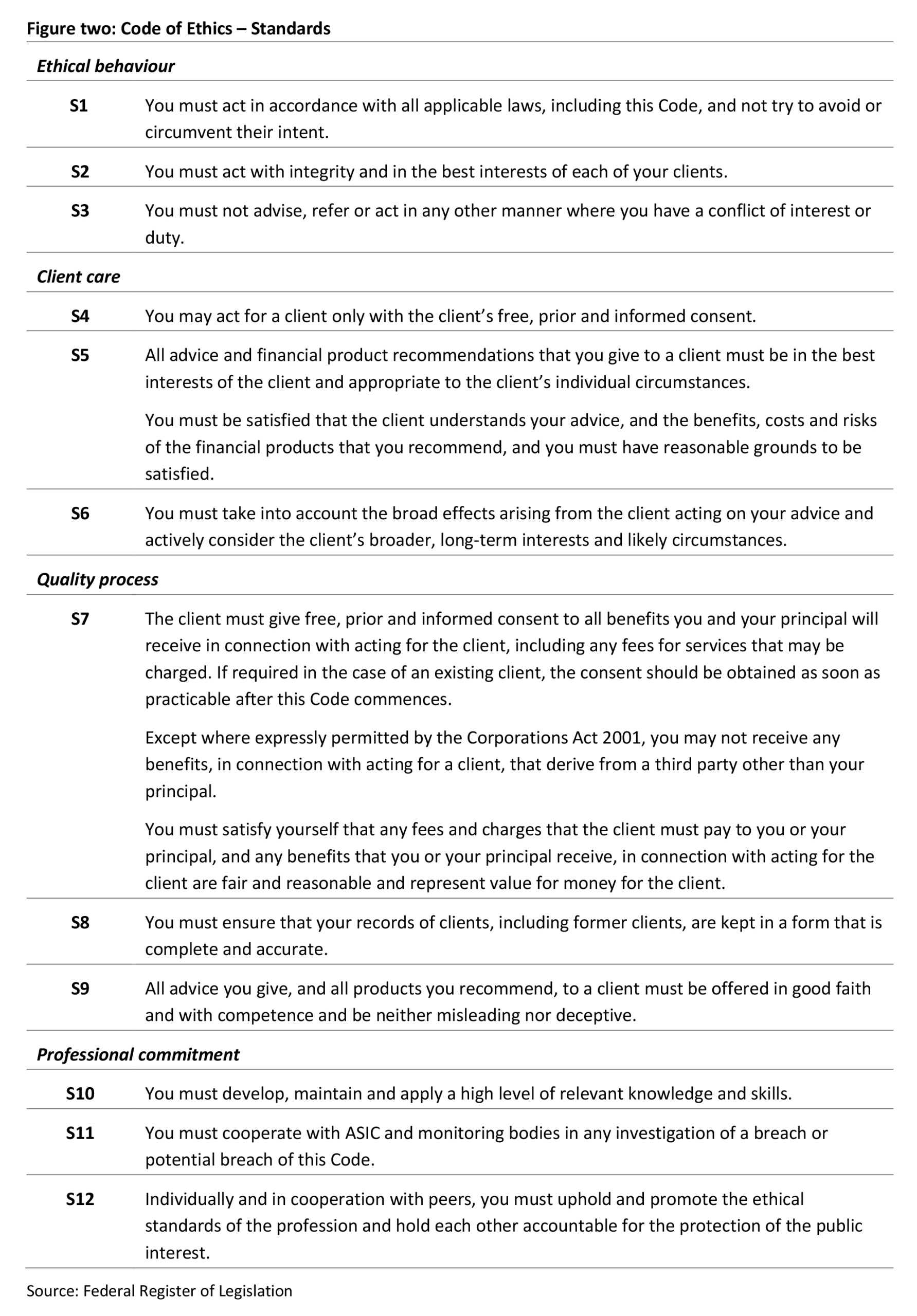

A registered financial adviser offering aged care advice is obliged to adhere to the Financial Planners and Advisers Code of Ethics (figure two).

The Code of Ethics was introduced to provide a layer of consumer protection and engender trust in the financial advice profession. The Code of Ethics requires financial advisers to meet their obligations in the law in respect of the advice provided to each client, including:

- The best interests duty

- The appropriateness of advice

- Prioritisation of client’s interests

- Additional requirements for product replacement recommendations

- Australian Taxation laws.

Further, licensed financial advisers are required to:

- Know your client

- Work out their situation, objectives, needs and their financial literacy level

- Have a reasonable basis for advice

- Know your product and the consequences of your advice, and ensure the advice is appropriate for the client

- Comply with statement of advice (SOA) requirements.

Those individuals who provide aged care advice (not just information) and are not registered advisers operate outside of this Code and the requirements outlined above. This has negative implications for consumers.

At best, unlicensed aged care advice can have mediocre client outcomes. At its worst, it can lead to elder abuse, in particular financial elder abuse. This is defined by the World Health Organisation as “The illegal or improper exploitation or use of funds or other resources of the older person” and is the subject of an earlier article in this year’s Ethics Series, Ethical financial advice for vulnerable clients – part two.

Registered financial advisers who provide aged care advice are licensed and regulated under the Corporations Act. Among other protections, their clients can take complaints to the Australian Financial Complaints Authority (AFCA).

Unregistered aged care advice is both a consumer protection and ethical issue for the industry. Although some clients receive personal product advice, they are not eligible for the protections available to clients of registered financial advisers, including access to AFCA.

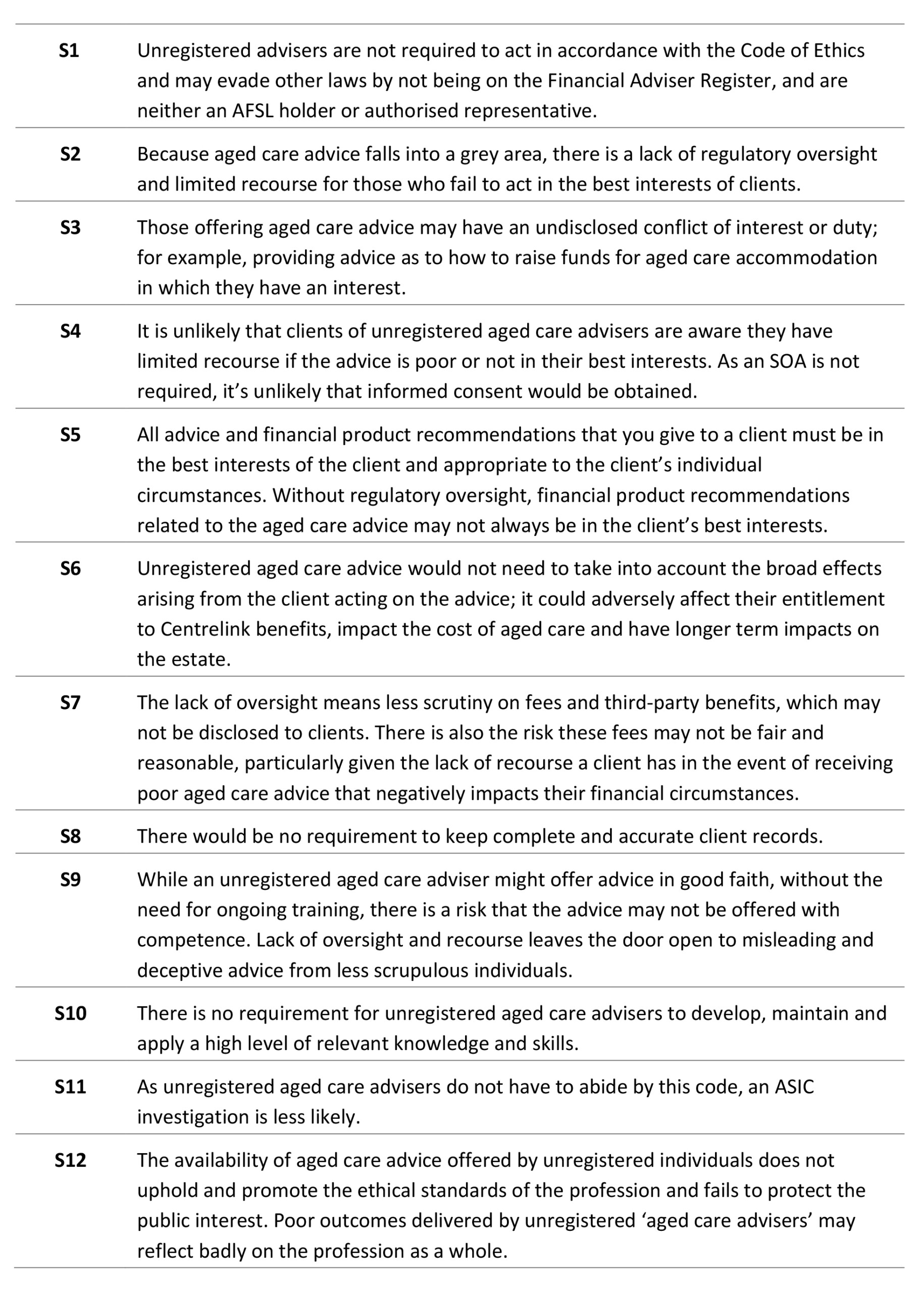

Although not beholden to the Code of Ethics, unregistered advisers providing aged care advice fail to deliver important outcomes for clients that can be unpacked in reference to the Code and its standards, as follows:

The lack of mandatory registration for aged care advisers raises significant consumer protection concerns, as it leaves the sector without a formal mechanism to verify qualifications and expertise. This regulatory void exposes vulnerable families to advisers who may lack the necessary training to navigate complex aged care needs. Consequently, consumers face an increased risk of receiving inadequate financial planning and securing unsuitable care arrangements.

Furthermore, exempting these advisers from the Code of Ethics removes critical safeguards that mandate transparency, conflict management and acting in the client’s best interests. Without these binding ethical standards, accountability is severely diminished, creating an environment where advisers might prioritise personal or institutional gains over client welfare. This absence of oversight significantly heightens the risk of biased, misleading or self-serving financial advice.

Finally, the intricate and constantly changing nature of the aged care system demands highly specialised knowledge, particularly regarding its interplay with financial planning. Without robust regulatory and ethical frameworks, consumers are uniquely vulnerable to outdated or inaccurate advice that fails to address their specific needs. Ultimately, this lack of oversight undermines public confidence and can lead to severe, long-lasting financial and emotional repercussions for families.

Case studies

The following case studies highlight the benefits of obtaining aged care advice from registered financial advisers through the lens of the standards comprising the Code of Ethics.

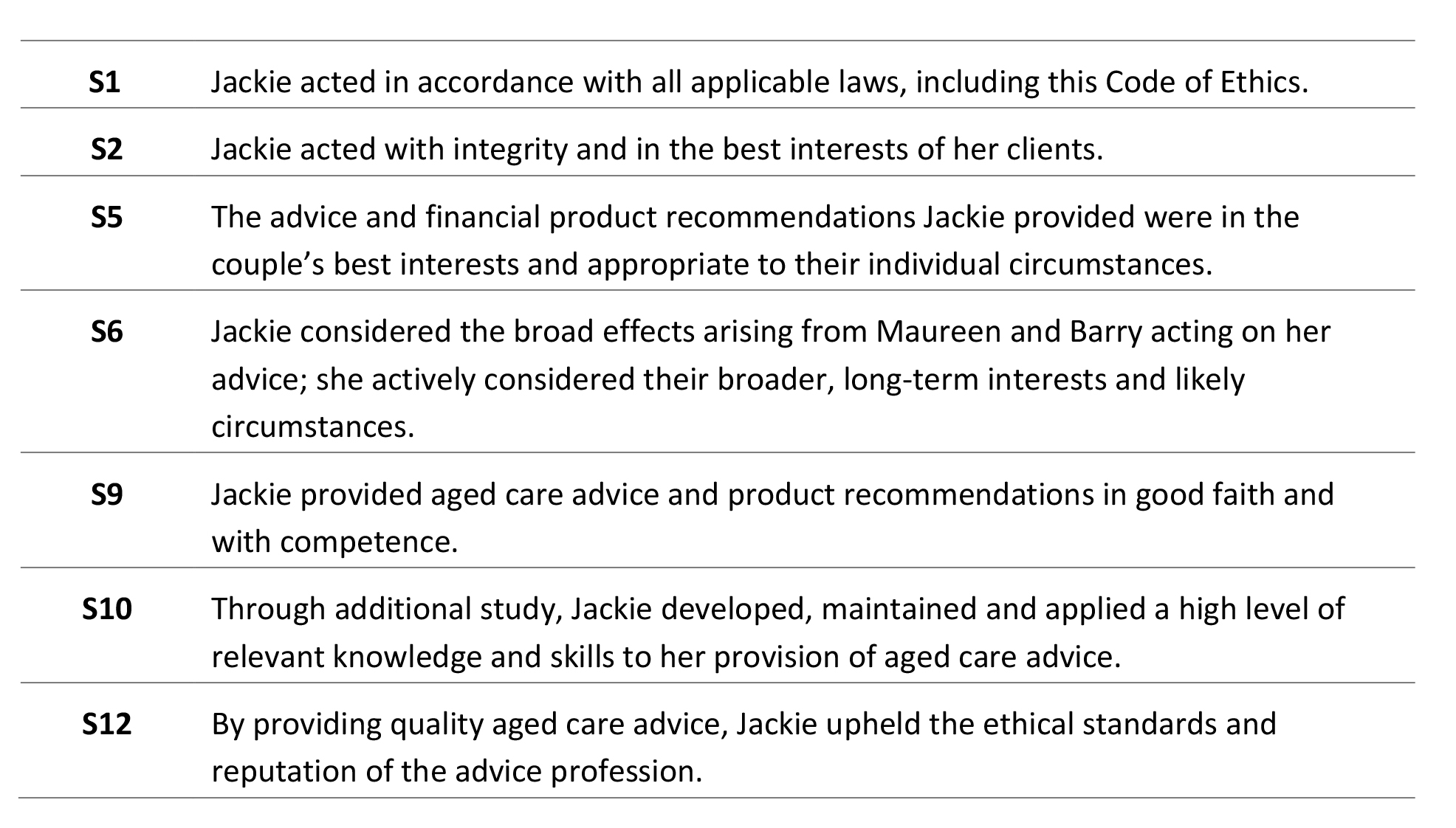

Case study one: Moving into aged care

Barry and Maureen, a couple in their early 80s, needed to arrange residential aged care for Barry due to his deteriorating cognition. Following a formal dementia diagnosis, Maureen and their children realised he needed professional care. Seeking guidance, they turned to an aged care adviser recommended by their neighbour. They were unaware that the recommended adviser was not a registered financial adviser.

The adviser, Nigel, provided Maureen with a detailed costing of the aged care options for Barry and suggested they sell the couple’s residence to pay for the Refundable Accommodation Deposit. They could then use the remainder of the sale proceeds plus their savings to buy a small unit for Maureen. While advice about buying or selling property, including the family home, is exempt from AFS provisions, the advice pertaining to the use of the couple’s savings is not.

However, Maureen was unhappy with the advice. She didn’t want to move; the couple had already downsized from their farm and moved into town – where else could she go? She was close to two of her three children, comfortable in her community and president of the local CWA. The downsized home was selected for its garden, and she didn’t want to have to give that up.

Encouraged by their children, Maureen and Barry sought a second opinion, this time from a registered financial adviser from ACME Aged Care Advice. Their new adviser, Jackie, explained that as clients of a registered financial adviser, they had a range of protections – and she had training and education related to the aged care sector. Further, she regularly undertook professional development to ensure she was familiar with current legislation and other changes to the sector.

Jackie helped the family understand the intricacies of the aged care fees they would incur and explain how they had changed post 1 November 2025. While the family had some understanding, what they understood to be the likely fees had changed. Jackie developed a strategy to ensure the family home would be retained, so Maureen could continue to enjoy her home, garden and community. Importantly, it ensured she had somewhere to live once Barry moved into aged care.

Jackie was able to recommend several strategies to rearrange the couple’s investments. She presented two funding options to determine which worked best for them. With tailored advice and support, the couple was able to fund Barry’s aged care needs and implement a financial plan that both prioritised their long-term wellbeing and considered all elements of their financial situation, including Centrelink entitlements and estate planning.

As a registered financial adviser, Jackie is bound by the Code of Ethics. Her conduct in this case study saw her meet her requirements under the Code, specifically in relation to the following standards:

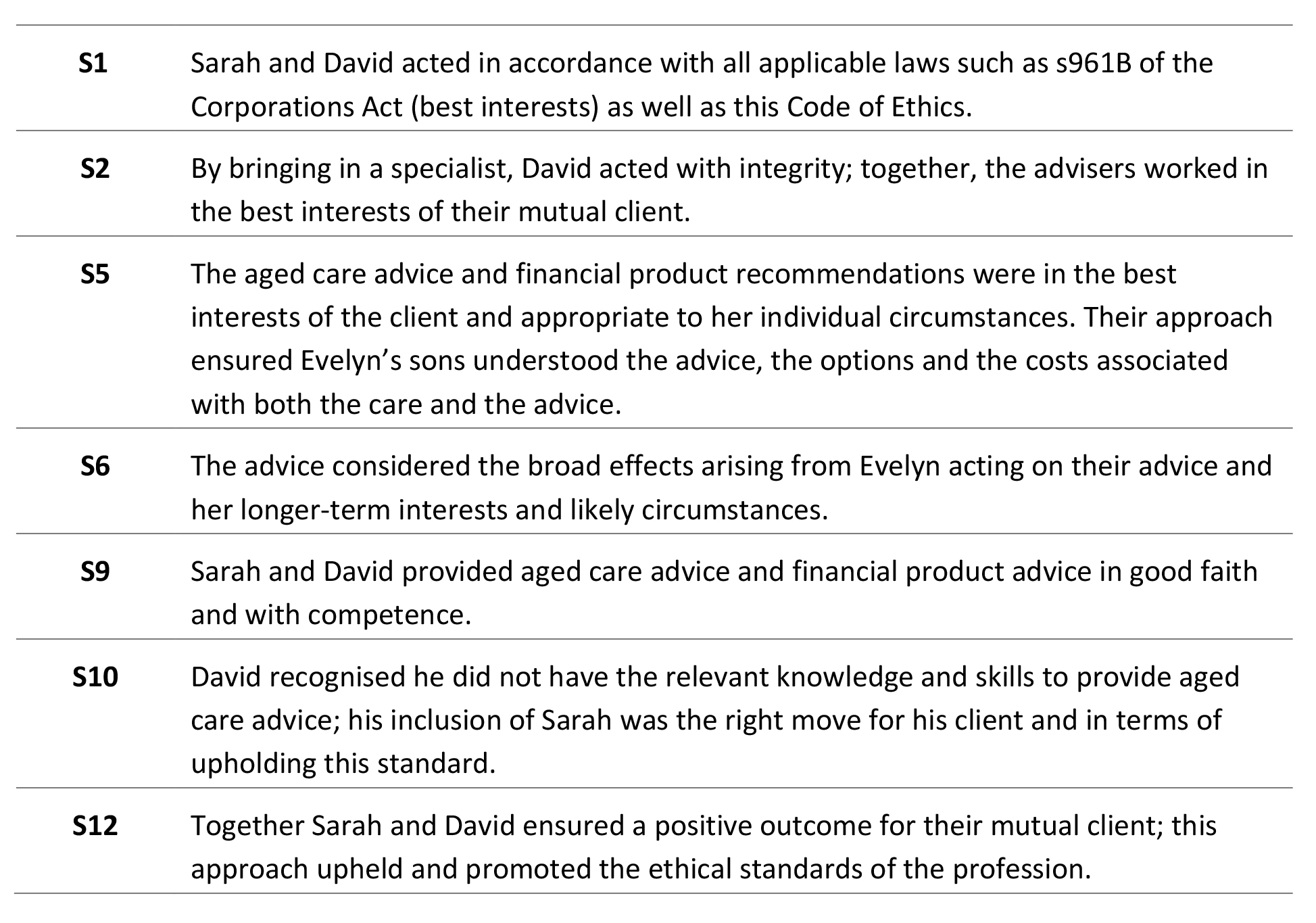

Case study two: Meeting aged care needs

Evelyn, a 79-year-old widow living alone, suffered a severe stroke that left her with permanent mobility challenges. Following an extended stay in an acute stroke unit, her multidisciplinary medical team advised her two sons that returning home independently was no longer safe, recommending a transition into permanent residential aged care instead.

Evelyn’s sons, who acted as her joint Powers of Attorney – one managing her medical decisions and the other overseeing her financial affairs – promptly scheduled a meeting with David, Evelyn’s long-standing financial adviser. Recognising that aged care involves highly complex, specialised regulatory frameworks, David immediately brought his colleague Sarah into the consultation. While both operated under the same financial services licensee, Sarah had completed advanced postgraduate certifications in aged care financial strategies to navigate the intricacies of means testing, payment options and the impact on Centrelink benefits.

Working collaboratively, Sarah and David modelled several funding scenarios for the brothers. A core constraint was Evelyn’s deep sentimental attachment to her family home; she refused to sell it, and her sons noted the property required significant deferred maintenance before it could fetch an acceptable market price anyway.

To solve this, Sarah proposed funding the transition via a Daily Accommodation Payment (DAP) instead of a lump-sum Refundable Accommodation Deposit (RAD). David then restructured Evelyn’s existing investment portfolio to generate a predictable, tax-effective monthly income stream dedicated entirely to covering the DAP and ongoing care fees. Ultimately, the coordinated approach ensured the brothers fully understood the financial commitments, fee structures and cash flow mechanics required to secure their mother’s quality of care without selling her home.

Working together, Sarah and David were able to provide Evelyn and her sons with positive outcomes, which ensured Evelyn’s care needs were met and her financial security assured. Their conduct in this case study saw the advisers meet Evelyn’s requirements under the Code of Ethics, specifically in relation to the following standards:

As Australia’s population ages, the demand for aged care advice will inevitably surge. Navigating this system often requires rapid decision-making during a highly stressful family crisis, making access to reliable, expert guidance more critical than ever.

However, the current regulatory ‘grey area’ allows unregistered, unregulated individuals to provide aged care advice while remaining exempt from the Code of Ethics. This lack of oversight poses severe risks to consumers, leaving them vulnerable to unqualified operators and biased recommendations that can jeopardise both their financial security and peace of mind. To safeguard vulnerable families, policymakers and industry stakeholders must close these loopholes and mandate that aged care advice be delivered exclusively by registered financial advisers.

Partnering with a specialist aged care financial adviser, either through a trusted external referral network or as an embedded specialist within the practice, can protect and enhance an advice firm’s client base as the wealth transition accelerates.

By integrating this specialised expertise, practices can seamlessly guide multi-generational families through highly stressful care transitions, preventing costly financial mistakes and securing the broader family’s loyalty. Ultimately, a proactive approach transforms a looming operational challenge into a powerful retention tool, positioning the practice as a holistic, indispensable partner for ageing clients and their beneficiaries.

Take the FAAA accredited quiz to earn 0.75 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Professionalism and Ethics (0.75 hrs)

ASIC Knowledge Requirements: Aged Care (0.75 hrs)

please log in to start this quiz

———-

Notes:

[1] National Ageing Research Institute demographic briefing

[2] https://www.aihw.gov.au/reports/australias-welfare/profile-of-australias-population

[3] The Risk of Unregulated Aged Care Advice: Protecting Older Australians and Ensuring Quality Advice, Aged Care Steps, January 2026

[4] Aged Care Act 2024 Wait Times Report: Residential care and Support at Home 1 November 2025 – 31 March 2026, published 12 May 2026

[5] https://www.agedcarequality.gov.au/providers/reform-changes-providers/about-new-aged-care-act-and-key-changes-providers

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Professionalism and Ethics (0.75 hrs)

ASIC Knowledge Requirements: Aged Care (0.75 hrs)

please log in to start this quiz

———-

Notes:

[1] National Ageing Research Institute demographic briefing

[2] https://www.aihw.gov.au/reports/australias-welfare/profile-of-australias-population

[3] The Risk of Unregulated Aged Care Advice: Protecting Older Australians and Ensuring Quality Advice, Aged Care Steps, January 2026

[4] Aged Care Act 2024 Wait Times Report: Residential care and Support at Home 1 November 2025 – 31 March 2026, published 12 May 2026

[5] https://www.agedcarequality.gov.au/providers/reform-changes-providers/about-new-aged-care-act-and-key-changes-providers

Have feedback on this article? Contact Us

Earn CPD Points

CPD: Consumer protection essentials – AFCA and advice complaints

CPD: Consumer protection essentials – AFCA and advice complaintsAs essential component of a robust framework for protecting financial consumers is the presence of mechanisms that hold individuals and organisations to account for causing consumer harm and allow consumers [...]

CPD: A new approach to assessing risks in retirement

CPD: A new approach to assessing risks in retirementIn our last article, we examined the common risks that can impact retirement. The financial risks we’re all acutely aware of: longevity risk, inflation risk, market risk and sequencing risk. [...]

CPD: Ethics and financial abuse

CPD: Ethics and financial abuseFinancial abuse is becoming more prevalent in Australian society. This article, proudly sponsored by GSFM, examines financial abuse in the context of an ethical financial advice practice. A lot of [...]

CPD: Seeking stability

CPD: Seeking stabilityAt a time of sweeping geopolitical change and clear challenges for riskier assets, bond markets offer a source of stability. Key takeaways The world has entered a period of geopolitical [...]

CPD: The year ahead for fixed income markets

CPD: The year ahead for fixed income marketsThe forces shaping fixed-income markets found themselves at a confluence of economic, fiscal, and political factors heading into 2025. Inflation dynamics remained in flux, a new Treasury Department was in [...]