Allocation to private credit markets can provide an investment opportunity.

Private markets offer the potential to outperform public markets over the mid to long-term with the potential for lower volatility. Within this, private credit offers investors an attractive opportunity to benefit from regular income and strong investor protections, irrespective of the prevailing economic conditions. This article from GSFM examines this growing asset class, provides an outlook for the year ahead and explores the investment opportunity private credit presents for your clients.

Private market investments are investments in assets not traded on public exchanges. This sector spans real estate, infrastructure, private equity and private credit (sometimes called private debt – the terms are used interchangeably). Once the purview of institutional investors because of the large investments required, product innovation means private market assets are now widely available to most investors.

Industry projections suggest private markets could grow from US$13 trillion in 2024 to more than US$20 trillion by 2030 and it is anticipated that private credit and infrastructure will grow the fastest[1]. In fact, private credit is expected to climb to US$2.6 trillion by 2029, from US$1.5 trillion at the start of 2024[2].

The Australian private credit market is small relative to the global private credit market and other business lending but is growing rapidly. It accounts for around 2.5 percent of total business debt, including both intermediated lending and corporate bond issuance outstanding. Private credit grew faster than business debt over the past few years and is around two percentage points higher than the growth of traditional business debt[3].

What is private credit?

As an asset class comprised of privately negotiated loans and debt financing from non-bank lenders, private credit operates independently from the traditional banking system and serves as an alternative source of financing for privately held companies. This can take the form of loans, bonds, notes, private securitisation issues or asset backed financing.

All this means increased opportunities for investors as traditional lenders shift their focus toward servicing larger corporates. This move has left a large number of smaller borrowers looking elsewhere to meet their funding needs. Consequently, there’s been a large number of private credit providers enter the market to fill this gap, and an increase in the number of private credit funds available to investors.

Borrowers seek private credit for various reasons, including:

- an inability to access public credit markets or traditional bank financing

- bank financing is too restrictive for the borrower’s needs

- does not wish to be diluted by issuing new equity

- requires funds quickly.

Private credit covers a wide range of risk profiles, from small startup venture capital types of businesses through to large investment grade companies.

Why invest in private credit?

Australia’s largest superannuation funds are leading the way by allocating billions of dollars into private credit, a trend private credit specialist Tanarra Credit Partners expects to continue. Several larger industry superannuation funds such as Cbus and Aware Super are directly investing in private credit, while other funds are choosing to invest through specialist private credit fund managers to gain exposure to the asset class.

AustralianSuper is one of the largest investors and has allocated over US$4.5 billion (A$7 billion) in private credit globally, with the stated ambition to triple its exposure in the coming years. Cbus is reportedly planning to triple its global allocation to private credit over the next 18 months, while fellow industry fund Hostplus is also looking to add to its already record holdings of the asset class[4].

Investing in a private credit fund can offer several potential benefits to investors, be they large institutions or individuals, including:

- Potential for attractive returns: private credit funds generally offer higher returns than traditional fixed-income investments because they invest in non-publicly traded debt instruments, such as private loans or structured credit, which typically offer higher yields.

- Steady income: private credit investments generally involve loans with regular interest payments, providing a stable and predictable income stream; this makes private credit attractive to income-focused investors, such as retirees.

- Diversification: private credit funds provide diversification benefits to an investor’s portfolio because investors gain exposure to a range of different debt instruments and borrowers, which can help to spread their risk and potentially improve the overall performance of your clients’ portfolios.

Further, private credit provides exposure to asset classes that may not correlate strongly with equities or traditional fixed income investments, which can help reduce overall portfolio volatility and improve risk-adjusted returns.

- Lower volatility: private credit funds can offer lower volatility amid geopolitical uncertainties, inflationary pressure and historically high asset valuations when compared to more traditional investment products.

- Access to institutional-quality investments: private credit funds have historically been only accessible to institutional investors or high net worth individuals. By investing in a private credit fund, individual investors can gain access to institutional-quality investments.

- Potential for downside protection: private credit funds generally have tight covenants in place that provide downside protection. These covenants reduce the risk of capital loss and help to ensure that appropriate returns are maintained relative to any changes in the credit risk of an underlying investment.

- Increased market opportunity: as banks continue to reduce their lending to certain borrowers due to stricter regulations, there are growing opportunities for private credit investors.

Private credit outlook – it’s 2024 2.0!

As tight bank lending conditions endured through 2024, borrowers continued to appreciate the speed and adaptability of private credit solutions. At the same time, investors valued the role private credit can play to diversify portfolios, as well as the high cash income and low volatility of a senior secured credit product. Consequently, the private credit sector finished 2024 with strong performance.

Competing asset classes also finished the year positively, but with more volatility. Australian equities shook off economic concerns and the impact of higher rates to notch up a strong end to 2024; the S&P-ASX 200 Index was up 7.5 percent and close to $2 billion was added to the value of the benchmark index. Domestic residential property valuations remain elevated, although they did experience some softening in Sydney and Melbourne.

Heading into 2025, several concerns have not been resolved: inflation remains sticky, expectations as to the timing and quantum of central bank rate cuts have been lowered, and geopolitical risk continues to be elevated. At the same time, equity and residential property valuations appear stretched.

While inflation has been reduced and rate cuts have started in some jurisdictions, market risk lingers on a number of fronts. This contributes to the attractiveness of private credit.

Inflation has moderated: Despite lower inflation, in Australia it remains above the RBA’s targeted 2-3 percent rate. Consequently, the RBA is unlikely to drop rates as far or as fast as other central banks. In the US there is a risk of inflation ticking up this year based on new policies, such as tariffs, announced by President Trump.

Rate cuts: Australia is expected to cut rates twice in 2025; however, with above target inflation resulting from higher energy and food prices, coupled with a constructive labour market, the RBA will likely remain cautious. This positions the Australian private credit market to offer attractive returns versus overseas markets such as the US, where the Federal Reserve has already cut rates by 100 basis points, with an additional 50 basis points priced in for 2025.

Global uncertainty: The only certainty to result from President Trump’s policy statements with respect to trade, inflation and investor flows is the likelihood of global uncertainty. The largest trade impact could be felt by China, with tariff threats of up to 50 percent, and its flow-on effect on Australia. Threats of higher tariffs have also been made to Canada and Mexico. US tax cuts, a continued focus to onshore US manufacturing and deregulation could also have an impact.

Higher default rates: As corporations service debt with higher interest rates, the risk of default increases. In the more transparent markets, US leveraged loan market defaults are now around 4.5 percent[5]. A similar increase is evident in Australia where Australian companies entering default are at record numbers[6]. Weakness is especially felt in consumer focused corporations and property developers.

Historically expensive valuations: Equity valuations remain at all-time highs with the US S&P500 within 0.1% of its peak[7] and the ASX200 reaching an all-time high of $8,514.50 in December 2024. At the same time, despite some pull back in house prices, affordability for Australian residential property remains low, with a median dwelling value-to-income ratio of 8.0 times[8]. In other sectors, commercial real estate is grappling with ~US$4.7 trillion[9] of debt.

Momentum to continue: The Australian private credit market is poised to see continued deal activity in 2025, building on the momentum from late 2024, thanks to a robust pipeline of deals in the sponsor-backed market.

Ongoing uncertainty creates a challenging environment for investor allocations. While the Australian private credit market is not entirely immune to global economic forces, it exhibits a degree of insulation from the volatility experienced in larger markets such as the US. This stability, coupled with the attractive yields offered by private credit, makes it a compelling investment proposition irrespective of the prevailing economic conditions in 2025.

In this environment, private credit offers investors diversification into an attractive, defensive asset class with features and characteristics that mitigate several investor concerns:

- Attractive return profile – private credit provides regular income and attractive risk-adjusted returns.

- Hedge against inflation/interest rate risk – private credit continues to benefit from higher-for-longer interest rates with its floating-rate yield profile.

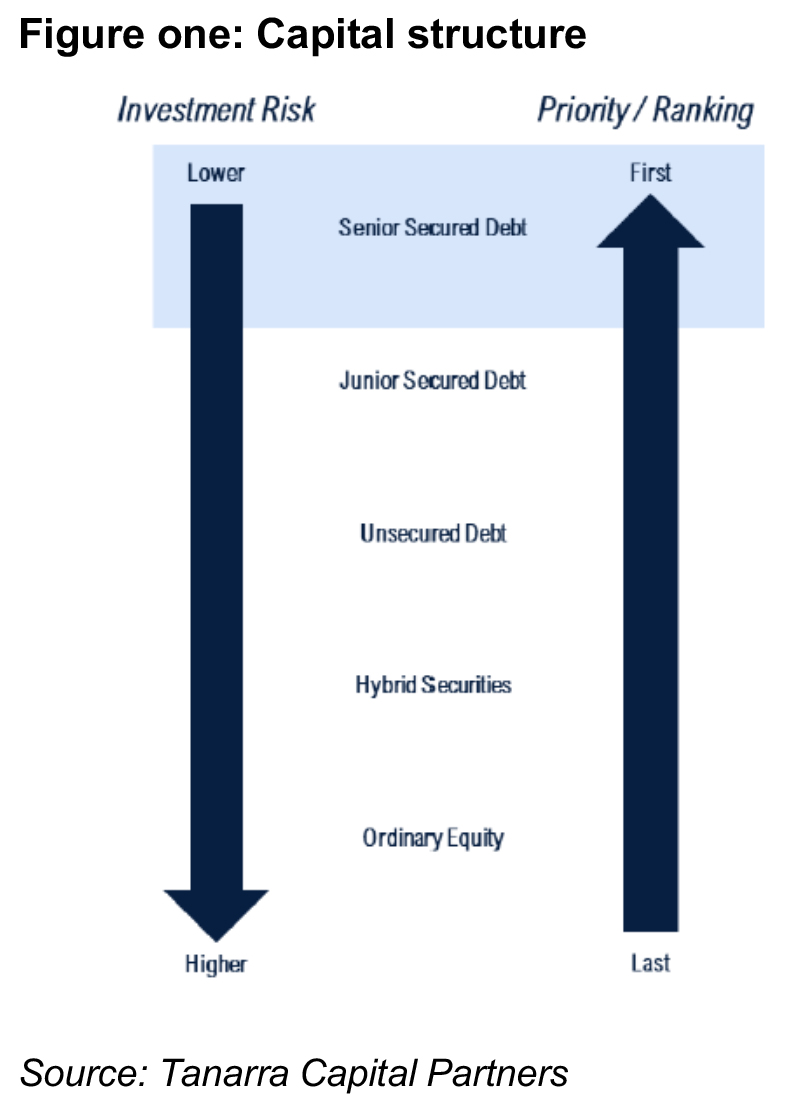

- Alternative to asset classes with stretched valuations – private credit investments are senior in the capital structure (figure one) and that provides a meaningful equity buffer against deterioration in valuation and has low correlation with other asset classes

- Managing risks during economic downturns – private credit has strong downside protection features that helps to manage the risk of underperforming borrowers during economic downturns. These might include:

- Senior ranking security that provides first right to cashflows and assets of borrowers hence providing a buffer against deterioration in earnings.

- Regular testing of financial covenants that can provide an early warning signal against deterioration in credit quality of the borrower. This enables the private credit manager to take action if required to protect the investment.

What to look for in a private credit manager

Private credit continues its strong growth trajectory. It remains an asset class well-suited to navigate the complex economic environment ahead in 2025, one likely to deliver positive real returns for investors.

However, there is a perception that the higher returns offered by private credit (compared to traditional bank lending) means that it is a high risk investment that should be avoided as either the borrowers are low-quality, or the deals carry too much risk.

This perception is exacerbated by the cashflow lending nature of corporate private credit and limited hard asset security compared to some traditional bank loans. However, there are a number of tools and structures deployed by private credit managers to mitigate and manage the risks associated with private credit financing, which when combined with the returns available, can deliver an appealing risk/return proposition for investors. It’s important that advisers ensure any private credit manager they consider have robust risk management processes that include rigorous due diligence and lender protections.

Rigorous due diligence

Detailed due diligence on prospective borrowers should include a review of third party financial, legal and commercial due diligence reports, as well as detailed financial modelling to assess a range of downside scenarios. This enables the manager to better understand the credit profile of the businesses they are looking to finance. It also allows the manager to ascertain the ability of the cashflows of the business to service the debt.

Lender protections

There are several downside protection features available for private credit investors. These include:

- Senior ranking security: a manager that primarily invests into senior secured loans will have first rights to the cashflows and assets of borrowers. Further, investments that have meaningful equity capital that sits underneath the debt in the capital structure is ideal; the equity bears the volatility and risk of earnings or deterioration in valuation. In such cases, significant value would need to be eroded before the capital is at risk.

- Maintenance financial covenants: these are typically tested quarterly and provide an early warning signal if there is deterioration in the credit quality of the borrower. This enables the private credit manager to take action as required to protect their capital.

- Documentation protections: loan documentation will typically impose a range of restrictions on the borrower that protect the private credit manager’s position as a lender, including cashflow sweeps to repay debt should the business underperform, restrictions on ability to make acquisitions and disposals (without debt repayment), and not allowing distributions to shareholders until leverage has reduced.

It is also important that the investment team has the experience to navigate through an uncertain economic environment, which is critical for rigorous due diligence, successful deal selection and ongoing portfolio management. The ideal private credit team will have extensive corporate lending experience and will have successfully navigated a number of economic and credit cycles.

Investing in private credit can be a compelling strategy for investors and provide an attractive opportunity to benefit from regular income, strong investor protections and low volatility, irrespective of the prevailing economic conditions in 2025. By partnering with an experienced private credit investment manager, your clients can tap into the growing potential of private credit while mitigating risks. As regulatory changes and evolving market dynamics continue to create opportunities, private credit remains an attractive addition to a well-rounded investment portfolio, particularly for those with a long-term perspective and a willingness to explore alternatives beyond traditional markets.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Alternative Assets (0.5 hrs)

please log in to start this quiz

———-

Notes:

[1] Preqin, Quarterly Update September 2024

[2] Preqin, Future of Alternatives 2029 Report, December 2024

[3] RBA Bulletin, Growth in Global Private Credit, October 2024

[4] Firstlinks, Should investors follow super funds into private credit?, July 2024

[5] JP Morgan, Credit Strategy Weekly Update, 17 January 2025

[6] ASIC, Weekly Insolvency Statistics, accessed 21 January 2025

[7] Market Index, Morning Wrap: ASX 200 to fall, S&P 500 near record highs, Market breadth flips negative, 23 January 2025

[8] ANZ, Housing Affordability Report, November 2024

[9] Houlihan Lokey, Commercial Real Estate – Debt Market Update, October 2024

The information included in this article is provided for informational purposes only and is general advice only. It does not take into account an investor’s own objectives. The information contained in this article reflects, as of the date of publication, the current opinion of Tanarra Credit Partners and is subject to change without notice. Sources for the material contained in this article are deemed reliable but cannot be guaranteed. We do not represent that this information is accurate and complete, and it should not be relied upon as such. Any opinions expressed in this material reflect our judgment at this date, are subject to change and should not be relied upon as the basis of your investment decisions. All reasonable care has been taken in producing the information set out in this article however subsequent changes in circumstances may occur at any time and may impact on the accuracy of the information. Neither Tanarra Credit Partners, GSFM Pty Ltd, their related bodies nor associates gives any warranty nor makes any representation nor accepts responsibility for the accuracy or completeness of the information contained in this article.

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Alternative Assets (0.5 hrs)

please log in to start this quiz———-

Notes:

[1] Preqin, Quarterly Update September 2024

[2] Preqin, Future of Alternatives 2029 Report, December 2024

[3] RBA Bulletin, Growth in Global Private Credit, October 2024

[4] Firstlinks, Should investors follow super funds into private credit?, July 2024

[5] JP Morgan, Credit Strategy Weekly Update, 17 January 2025

[6] ASIC, Weekly Insolvency Statistics, accessed 21 January 2025

[7] Market Index, Morning Wrap: ASX 200 to fall, S&P 500 near record highs, Market breadth flips negative, 23 January 2025

[8] ANZ, Housing Affordability Report, November 2024

[9] Houlihan Lokey, Commercial Real Estate – Debt Market Update, October 2024

The information included in this article is provided for informational purposes only and is general advice only. It does not take into account an investor’s own objectives. The information contained in this article reflects, as of the date of publication, the current opinion of Tanarra Credit Partners and is subject to change without notice. Sources for the material contained in this article are deemed reliable but cannot be guaranteed. We do not represent that this information is accurate and complete, and it should not be relied upon as such. Any opinions expressed in this material reflect our judgment at this date, are subject to change and should not be relied upon as the basis of your investment decisions. All reasonable care has been taken in producing the information set out in this article however subsequent changes in circumstances may occur at any time and may impact on the accuracy of the information. Neither Tanarra Credit Partners, GSFM Pty Ltd, their related bodies nor associates gives any warranty nor makes any representation nor accepts responsibility for the accuracy or completeness of the information contained in this article.

Have feedback on this article? Contact Us

Earn CPD Points

CPD: Private markets and alternatives – consumer protection challenges

CPD: Private markets and alternatives – consumer protection challengesIntroduction Interest in alternative assets – including private markets and infrastructure – has surged in recent years, a strong growth trajectory that is expected to continue well into the future. [...]

CPD: The adviser’s fiduciary duty in an ethical practice

CPD: The adviser’s fiduciary duty in an ethical practiceIt is both a legal and ethical requirement for financial advisers to fulfil their fiduciary duty to their clients. This article, proudly sponsored by GSFM, explores the importance of the [...]

CPD: The spectrum of growth

CPD: The spectrum of growthCompanies that generate strong, sustainable growth are valuable sources of long term capital appreciation in a portfolio, but these businesses are rare, difficult to identify and exist on a broad [...]

CPD: Record-keeping in financial advice – the key to compliance and consumer protection

CPD: Record-keeping in financial advice – the key to compliance and consumer protectionIntroduction The financial services regulatory framework is a key pillar of financial consumer protection. Regulatory compliance is therefore not merely about avoiding penalties, but is a critical step in building [...]

CPD: Trust and ethics in financial advice

CPD: Trust and ethics in financial adviceIn 2024, trust in financial advisers reached an all-time high. This article, proudly sponsored by GSFM, explores the inseparable links between trust and ethical practice when providing financial advice. Defined [...]