CPD: Ethics and moral dilemmas

Upholding professionalism requires a strong ethical foundation, and advisers must often make subjective judgments in complex, ‘grey’ situations

When it comes to financial advice, the numbers may be black and white, but the ethical decisions often aren’t. This article, proudly sponsored by GSFM, examines moral dilemmas and the ‘grey’ areas inherent in providing financial advice.

Financial advisers may face moral dilemmas that test their judgement, integrity and responsibility to clients. Some of these situations involve clear-cut misconduct, such as falsifying information or failing to disclose conflicts of interest. But many fall into shades of grey, where the right course of action depends on balancing competing priorities, such as respecting a client’s autonomy while safeguarding their financial wellbeing.

Moral dilemmas and ethical challenges in financial advice can range from clear misconduct to complex, situational judgments. A deeper appreciation for this spectrum illuminates the importance of sound ethical reasoning, the professional standards and Code of Ethics that underpin trusted advice.

What is a moral dilemma?

The Cambridge dictionary defines a moral dilemma as ‘a situation in which there is a difficult choice to make about what is the right thing to do’. In such situations, professionals must rely on their personal moral compass: the ability to judge a situation and act accordingly. However, this internal guide is subjective and varies significantly from person to person.

An interesting framework is the States of Moral Development[1], developed by psychologist Lawrence Kohlberg. It posits that moral reasoning develops through a series of six distinct stages, grouped into three levels. As an individual progresses through the stages, their reasoning for moral decisions becomes less self-centred and more complex and abstract.

Level 1: Pre-Conventional Morality

This is typically seen in children aged 3-7. At this level, the moral code is shaped by the standards of adults and the consequences of following or breaking their rules.

Stage 1: Obedience and punishment orientation

An individual’s primary motivation is to avoid punishment. An action is considered morally wrong if the person who commits it gets punished. The more severe the punishment, the “worse” the act is perceived to be.

Stage 2: Self-interest orientation

Individuals are motivated by self-interest and rewards. Behaviour is judged as “right” if it serves one’s own needs or results in a favourable outcome. There is a sense of reciprocity, but it is manipulative and self-serving.

Level 2: Conventional Morality

This is generally seen in adolescents aged 8-13. At this level, individuals begin to internalise the moral standards of valued adult role models, their peer group and societal norms. Kohlberg believed most people do not progress beyond level two, adopting their moral views from their environment rather than through independent ethical reasoning.

Stage 3: Living up to expectations

Moral reasoning is based on living up to the social expectations and roles of the family and community. There is a strong emphasis on conformity, being “nice,” and considering how choices will influence relationships. Approval from others is a key motivator.

Stage 4: Law and order morality

The focus shifts to maintaining social order. The individual now considers society when making judgements. The reasoning involves obeying laws, respecting authority and performing one’s duty to uphold the established system. Most adults remain at this stage in level two.

Level 3: Post-Conventional Morality

This level is typically reached in adulthood – if at all. Individuals develop their own personal set of ethics and morals that may or may not fit the law. They understand that rules are not absolute but can be changed for the greater good.

Stage 5: Social contract and individual rights

Individuals understand that laws are essentially social contracts that people enter for the benefit of all. While laws should be respected, they are viewed as flexible tools to improve society. An individual at this stage might argue for a law to be changed if it no longer serves the public good.

Stage 6: Universal ethical principles

Moral reasoning is based on abstract reasoning using universal ethical principles. The individual develops their own moral guidelines which may or may not fit the law. These principles (such as honesty, integrity and fairness) are applied to everyone. A person at this stage is prepared to act in defence of these principles.

For a financial adviser, conventional morality (level two) is not sufficient. The profession demands a more developed moral framework capable of navigating ‘grey’ areas to serve the client’s best interests. An adviser’s moral compass must not only distinguish right from wrong but also compel them to take the course of action that achieves the best possible outcome for every client.

Morals and a Code of Ethics

When it comes to ethics, answers aren’t always straightforward. Comprehensive guides, such as the Financial Planners and Advisers Code of Ethics 2019 (Code of Ethics), aim to define acceptable conduct in specific situations and workplaces. This brings clarity to decision-making and provides a framework to evaluate past actions and real-world scenarios that often present complexities.

Investopedia defines a code of ethics as “a guide or principles designed to help professionals conduct business honestly and with integrity.” These codes typically outline the foundational principles of an industry or organisation, along with the expected approach professionals should take when faced with a problem. This approach often requires drawing upon an individual’s personal morals.

The Code of Ethics was established to boost public trust in financial advisers by elevating professional standards. It introduces ethical obligations that go beyond current legal requirements, aiming to foster and embed a higher level of conduct and professionalism within the financial advice sector.

Crucially, the Code of Ethics places the responsibility squarely on individual advisers to understand and apply their professional judgment to their ethical duties during client interactions. This ensures their professional conduct is always focused on providing advice that truly serves the client’s best interests.

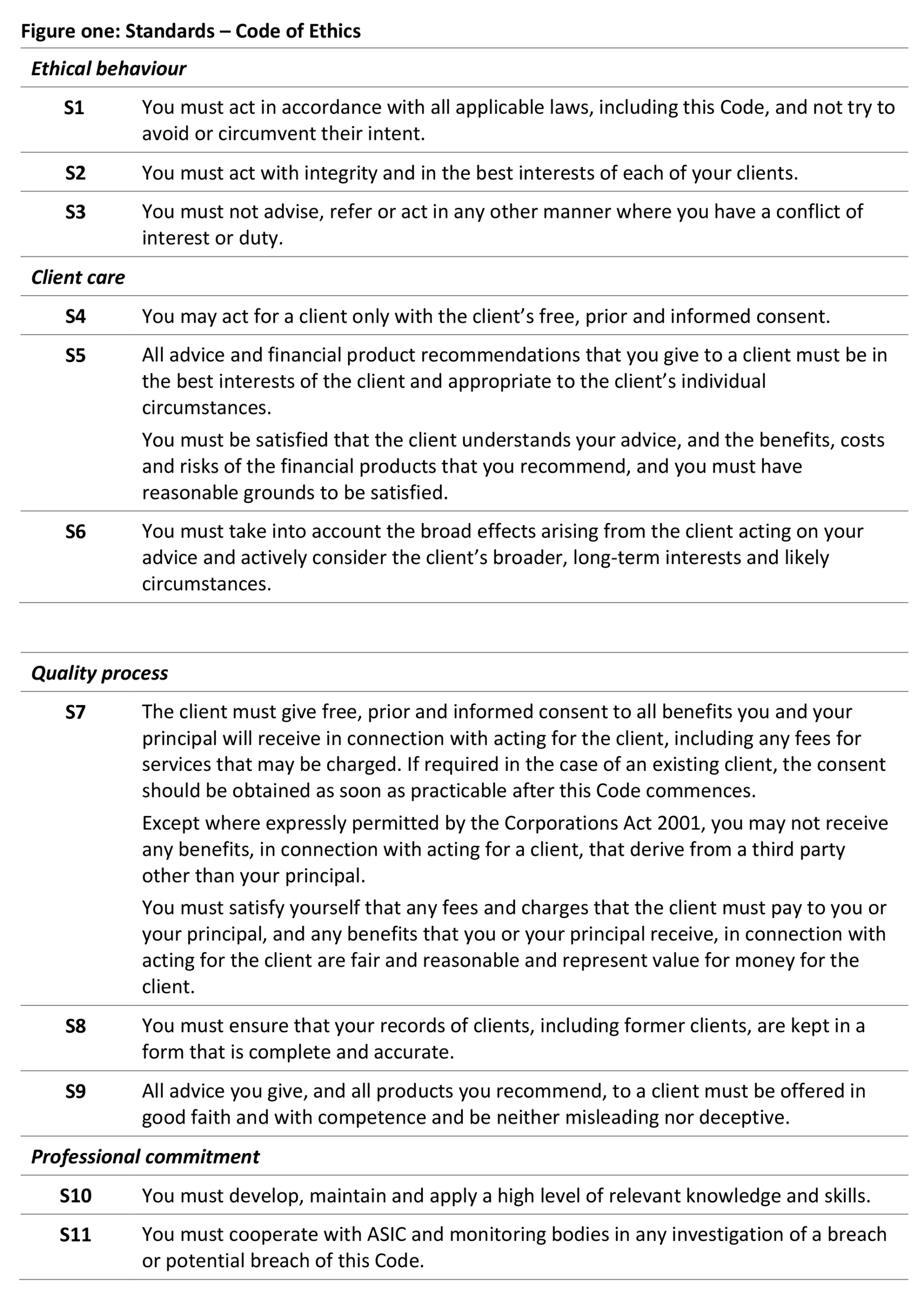

Additionally, financial advisers are required to act in a manner that clearly aligns with the twelve ethical standards outlined in figure one.

A study[2] that investigated the effects of codes of ethics on perceptions of ethical behaviour found the presence of a code in businesses improved the organisational climate. It provided:

- support for ethical behaviour

- freedom to act ethically

- greater satisfaction with the outcome of ethical problems

- a positive impact on perceptions of ethical behaviour in organisations.

Further, it’s been determined[3] that a code of ethics – whether industry or organisation wide – can provide benefits, including:

- A well-crafted code of ethics is instrumental in cultivating a workplace culture grounded in trust, ethical behaviour, integrity and excellence. Building trust is crucial for forging strong relationships, a principle that applies equally to the financial advice profession as a whole and to individual advisers within their practices.

- The financial advice profession has faced considerable challenges in recent years, with each incident potentially damaging its reputation at both the industry and individual level. Therefore, cultivating and upholding a reputation for professionalism, trustworthiness and ethical practice is vital for the industry’s future.

- Because the Code of Ethics requires compliance with all laws, it will further advance trust with clients and trust in the industry.

- There’s been a well-publicised exodus of advisers over the past few years. This, coupled with Australia’s ageing population, highlights a clear need for more financial advisers. To build a robust and successful industry, and equally strong individual practices, it’s crucial to attract the right people—those who will not only meet the requirements but also embody the spirit of the profession.

- A stronger, more professional financial advice industry will naturally draw in more clients, leading to the “normalisation” of seeking financial advice. This is a crucial shift. As Australia’s population ages and people live longer, professional financial advice becomes even more vital for ensuring the financial wellbeing of all Australians.

Even with the industry Code of Ethics in place, you’ll likely encounter ethical dilemmas that aren’t clear-cut. These ‘shades of grey’ situations demand professional and moral judgment to resolve effectively.

Black, white and grey in practice

Ethics isn’t just about how you operate; it’s also about the conduct of your colleagues and referral partners. That’s why it’s crucial to consistently educate and reinforce the importance of ethical practices within your business and with those you collaborate with.

While ‘grey’ ethical issues often demand time and effort to resolve, tackling them can offer valuable insights for your practice. It can help you proactively avoid or smoothly resolve similar challenges down the line.

In fact, ethical challenges can be a powerful tool for growth. Recognising these ‘shades of grey’ and using real-world examples or case studies that aren’t clear-cut provides an excellent opportunity for training and discussion within your team.

A smart approach is to document potential ethical situations your team might encounter daily. These scenarios can then be used in staff training sessions, allowing your team to collaboratively work through possible resolutions that lead to the best outcomes for clients. Being proactive today can prevent the development or escalation of an ethical challenge tomorrow.

Crucially, the existence of moral dilemmas that are ‘shades of grey’ underscores the importance of every employee in a financial advice business being aligned with its core values and practices. You can’t assume everyone shares the same highly developed sense of ethics or that it perfectly matches your expectations. This highlights why it’s so important to regularly educate, reiterate and reinforce the significance of integrity, trust, your corporate values and ethical behaviour as a consistent part of your training.

Being transparent about how to handle ethical issues significantly reduces the chance of breaching the Code of Ethics. This, in turn, lessens the likelihood of you, your peers, or your practice facing enforcement action.

Moral dilemmas are sometimes black and white…

Those dilemmas that are black and white generally involve clear ethical breaches or situations with obvious right and wrong. Examples include:

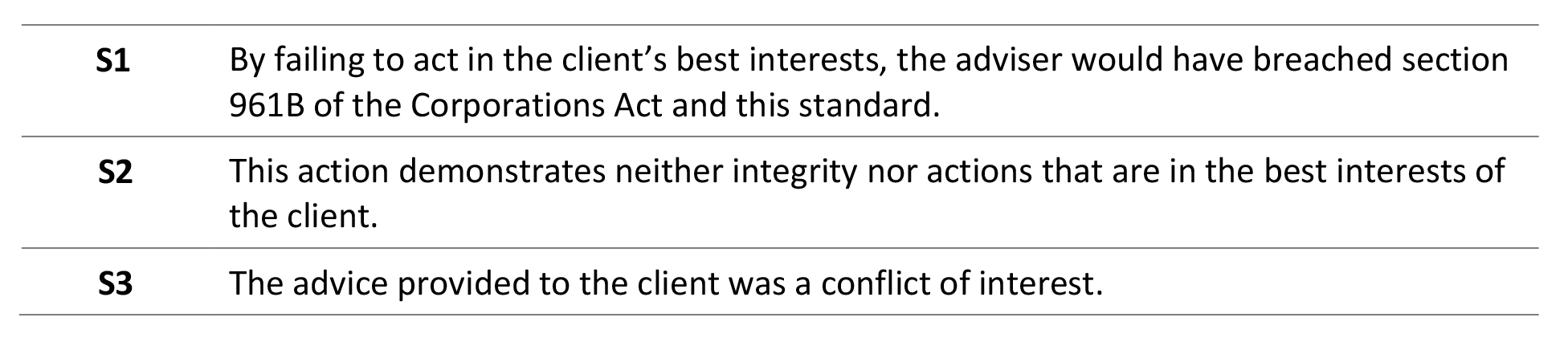

An adviser recommends a related party high-risk investment to a conservative client

This clearly violates ethical standards and violates fiduciary duty and best interest obligations. Some examples of standards potentially breached in such a scenario could include:

In addition, the adviser could be seen to breach standard four (in the event informed consent was not obtained), standard six (failure to consider long-term implications of advice) and standard 12 (failing to maintain standards of the profession).

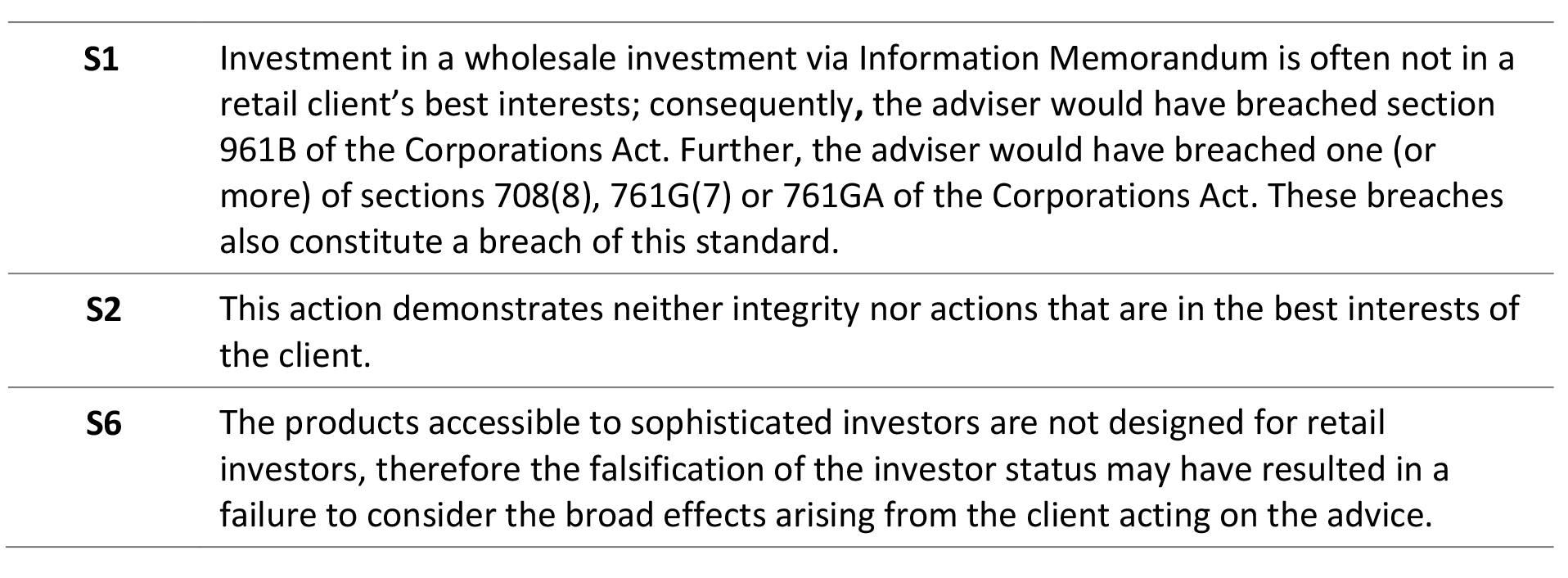

Adviser falsifies documents or information to indicate client is ‘sophisticated’ to access an investment opportunity

AFCA noted an increase in complaints where the wholesale investor test was manipulated by advisers to provide access to wholesale investments for individuals and SMSFs. This is both illegal and unethical, and breaches compliance, trust and professional standards. Examples of standards potentially breached include:

The adviser could also be considered to have breached standard five (financial product advice not in the client’s best interests), standard nine (advice provided in good faith and with competence) and standard 12 (failing to maintain standards of the profession).

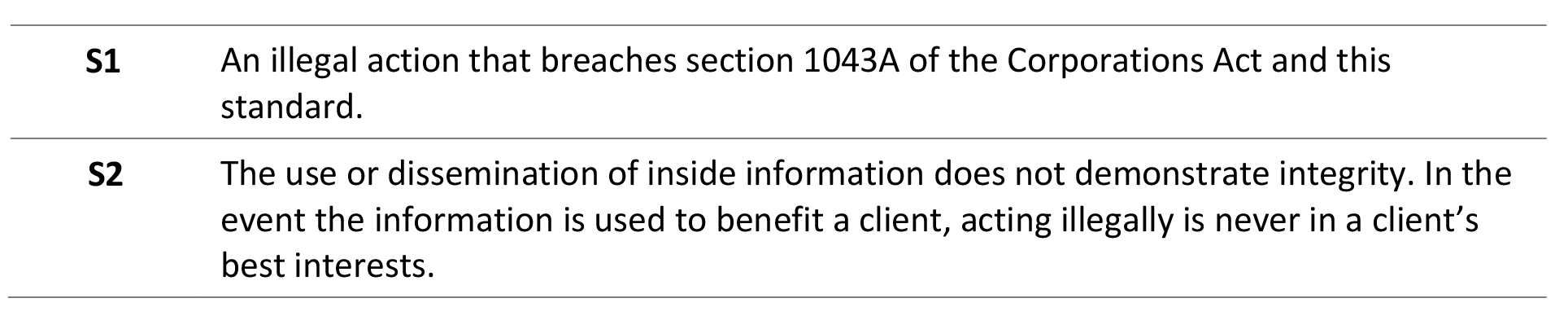

Insider trading or misuse of confidential information

Using or passing on confidential knowledge about market-sensitive events to benefit themselves or clients is unambiguously wrong – it’s both against the law and the Code of Ethics.

Examples of standards potentially breached include:

In addition, the adviser could be seen to breach standard four (in the event informed consent was not obtained), standard six (failure to consider long-term implications of advice that could include hefty fines and jail sentences) and standard 12 (failing to maintain standards of the profession).

…other times, moral dilemmas may be more ‘grey’

Moral dilemmas which could be classified as ‘grey’ tend to be more nuanced ethical questions where context, judgement and values play a more significant role. Examples include:

Balancing client autonomy versus adviser concern

A client insists on a strategy the adviser believes is not appropriate for the client; too risky, too conservative, even financially dangerous. The dilemma is, should the adviser comply with the client’s wishes, or push back to protect them?

In an ideal world, your knowledge and communication skills should be able to convince the client to adopt an appropriate strategy. However, the client may go against your recommendations. To avoid potential ramifications in the event of a client complaint, it is important to have all conversations, communications and your recommendations well documented and, as outlined in standard 8, ensure that your records of clients are kept in a form that is complete and accurate. This should include evidence that you have acted in the client’s best interests (and upheld standards 2 and 5) and that you have considered the client’s long-term interests (standard 6). Doing this also demonstrates your technical competence (standard 9).

Fee-for-service versus value delivered

Charging an ongoing fee for ongoing advice services that were not delivered was a key issue raised at the 2018 Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. Despite numerous advice firms being penalised for this, AFCA continues to receive numerous complaints about ongoing fees and a lack of service to earn them.

Advisers and licensees need to consider what value they deliver for their fees. In some cases, clients may not recognise what is being done on an ongoing basis and the value of that work. That means good communication and record keeping demonstrating just what you do for your clients and its contribution to their financial wellbeing and them meeting their objectives.

If there is no ongoing service, there should not be ongoing fees. To charge fees would demonstrate a lack of integrity (standard 2), actions not in client best interests (standards 2 and 5) and standard 12 (failing to maintain standards of the profession).

Case studies

The following case studies are mostly based on real events; however, the names of people and organisations have been changed, and some details altered. The case studies have been drawn from ASIC and the Australian Financial Complaints Authority (AFCA). For each, potential breaches of the Code of Ethics are identified.

Case study one: Inappropriate advice

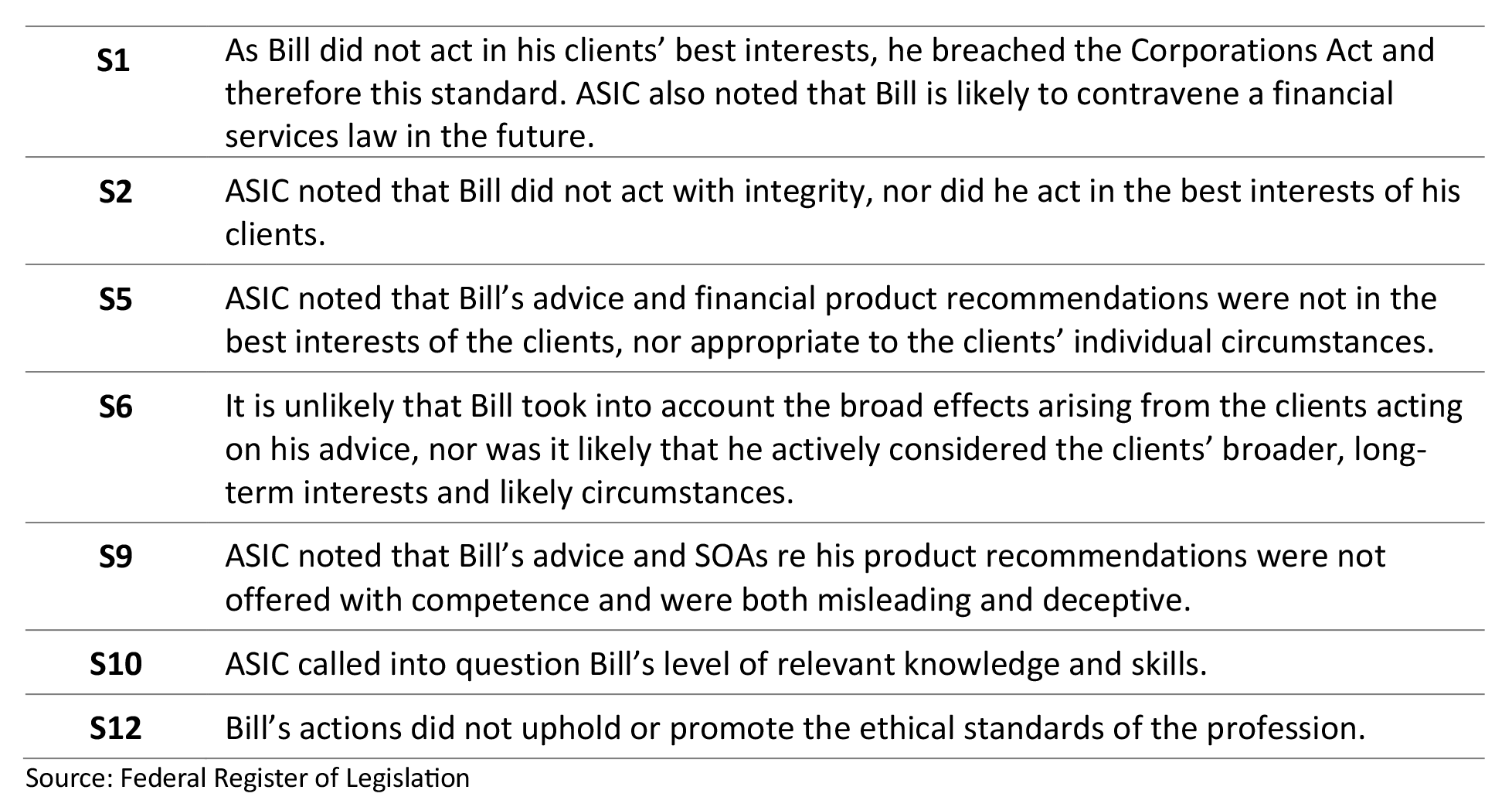

In a case that could be described as black or white, ASIC recently banned Sydney-based financial adviser Bill from providing financial services, controlling an entity that carries on a financial services business or performing any function involved in the carrying on of a financial services business for eight years.

ASIC found that Bill provided inappropriate advice to some of his clients; advice that was not in their best interests. This advice recommended that these clients invest most of their superannuation into the High Growth or Growth class of the ACME Master Fund. These classes of the Master Fund invested in high-risk investments, and the recommendations were made to clients irrespective of their risk profile.

ASIC also found that Bill’s statements of advice to certain clients included false and misleading statements that implied clients would enjoy better returns if their superannuation were invested into ACME Master Trust. This included:

- Projection tables and statements for client’s superannuation that did not have reasonable grounds

- Representations that ACME Master Fund had a higher performing track record against other super funds when it had only been in existence for a short period.

Consequently, ASIC claimed reason to believe that Bill is not a fit and proper person to provide advice, is not adequately trained or competent and is likely to contravene a financial services law.

Given ASIC’s findings, Bill is likely to have breached the following ethical standards:

Case study two: SMSF Advice

Self-managed superannuation funds (SMSFs) continue to boom. On 31 March 2025, there were 646,168 funds with 1,197,293 members; in total, these SMSFs held estimated assets under management over one trillion dollars[4] and represented more than one quarter of total superannuation assets.

The decision to establish a Self-Managed Superannuation Fund (SMSF) can originate from various sources – be it advice from an accountant, another third party or the client’s own initiative. It’s crucial to understand the reasoning behind this decision, especially if you have any reservations about whether an SMSF structure is appropriate for the client and if they can meet their obligations in managing it. Inappropriately recommended SMSFs comprise many of the complaints made to AFCA.

If a third party has established the SMSF and the client approaches you for investment advice, it’s vital to ensure they fully grasp their responsibilities as trustees. You need to emphasise that they are personally liable for all decisions made by the fund, including acting on any advice you or other service providers provide.

Lisa and Anthony sought financial advice after their accountant recommended the couple establish an SMSF. Lisa has run a successful business as a virtual assistant for many years, which she plans to sell in the coming 3-4 years. Anthony works in wholesale distribution. The couple intends to retire when Lisa sells her business.

Anthony has regularly contributed to super and has around $300,000 in retirement savings. Lisa has not made regular contributions, so her retirement savings will result from the sale of her business. Their accountant believes they should establish an SMSF now and transfer both super balances, followed by the proceeds of the business sale once complete. Anthony is keen to do that as he wants to buy a commercial premises, an idea suggested by one of his friends.

The couple meets with financial adviser George to get an investment strategy for the SMSF, as well as assistance with the strategy’s implementation. This is George’s first meeting with Lisa and Anthony. When he probes them about the SMSF and their roles and responsibilities, he realises they do not understand what’s involved with the ongoing management of an SMSF.

George explained their responsibilities as trustees of the SMSF and that they could be penalised for non-compliance in several ways:

- Their fund losing its concessional tax treatment

- Being disqualified from their role as trustee – this means they can no longer be members of the SMSF, and they are unable to start a new one

- Fines or imprisonment, depending on the seriousness of the breach.

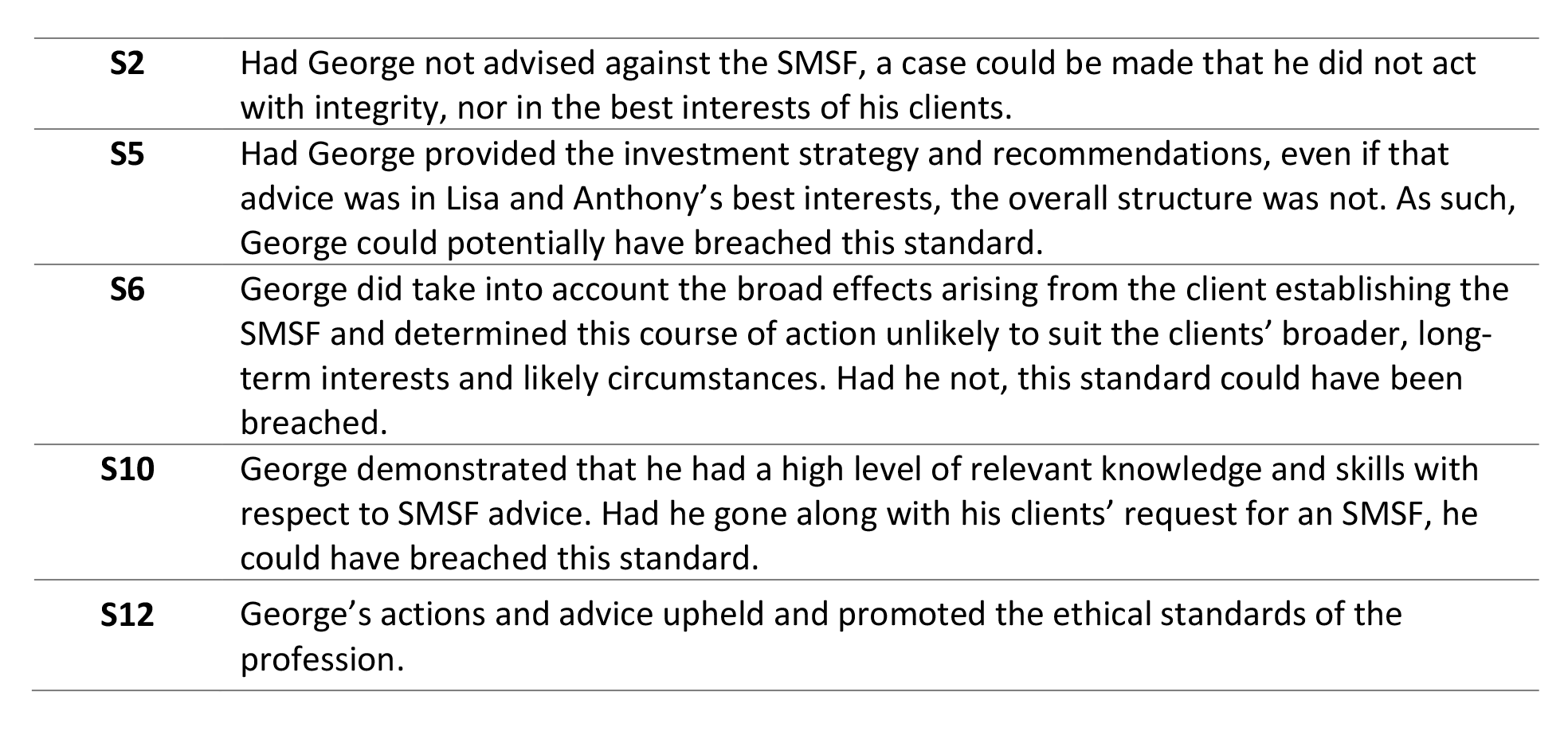

After lengthy discussions, George concluded that Lisa and Anthony were unlikely to have the requisite knowledge or time required to make an SMSF viable. As a result, he advised against this course of action.

Had George simply accepted the accountant’s advice to establish the SMSF and created an investment strategy and implementation plan as requested, he could make the case he was acting on his clients’ wishes and their accountant’s recommendation. The situation is not black and white. However, by engaging with Lisa and Anthony and understanding their capacity, George has acted in their best interests by recommending against the course of action.

George acted in his client’s best interests. Had he not taken that course of action and the clients were adversely impacted, the case could be made that he had breached the following standards in the Code of Ethics.

Case study three: Not fit and proper

A black and white case with little moral dilemma apparent on behalf of the adviser.

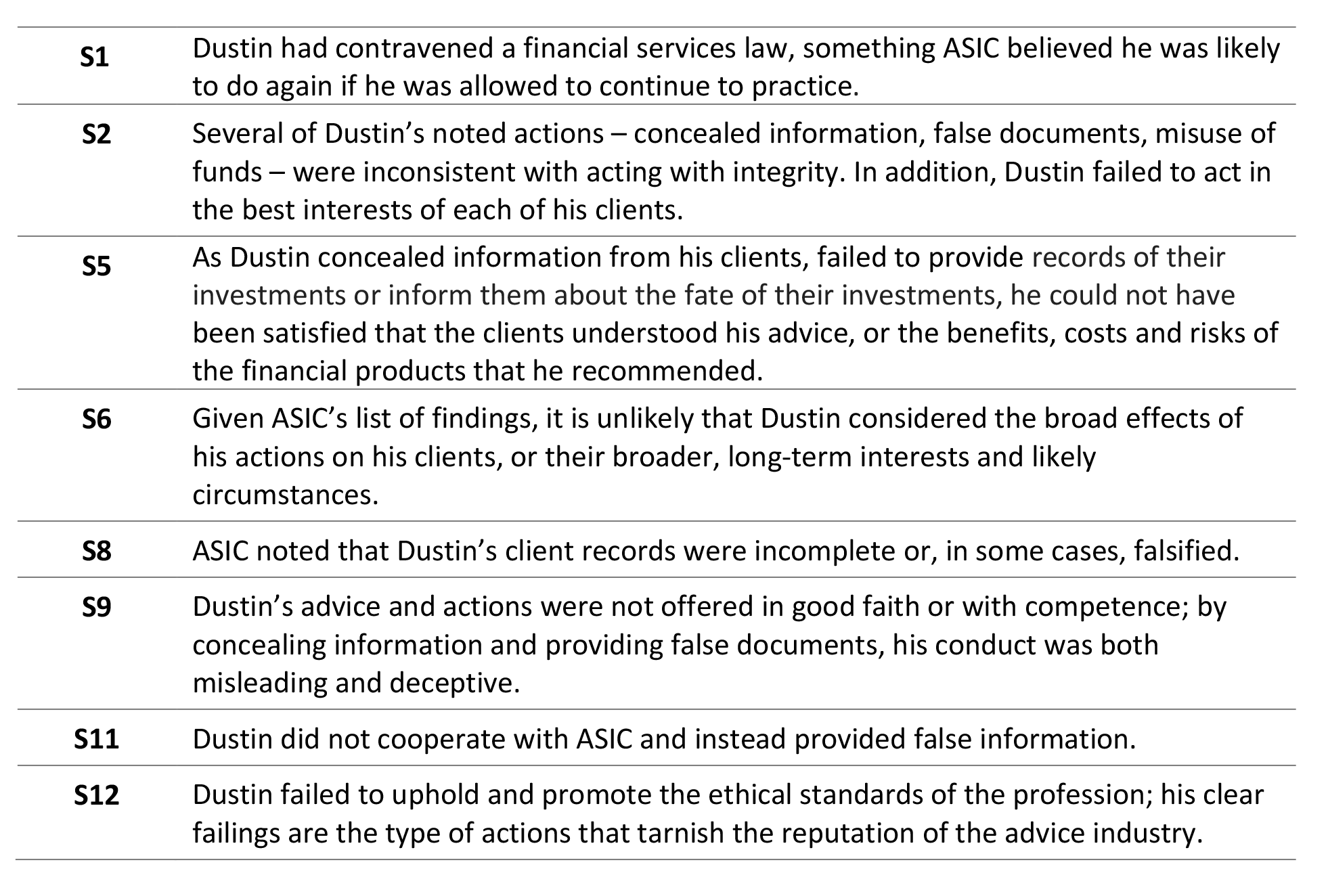

ASIC recently permanently banned adviser Dustin, an Adelaide based authorised representative of ACME Advice. ASIC found that Dustin’s conduct was dishonest, involved the misuse of client funds and the provision of false documents.

Further, ASIC determined that Dustin was not a fit and proper person to provide financial services and that he is likely to contravene a financial services law due to the regulator’s findings that he:

- Concealed information from his clients

- Made false representations to ASIC

- Caused false documents to be provided to his clients

- Managed client funds without obtaining written authorisation

- Misused client funds by directing payment of those funds to his personal liabilities

- Did not provide clients with records of their investments or inform them about the fate of their investments.

Dustin’s actions were likely to have breached the following standards:

Case study four: When good intentions lead astray

Even though falsifying documents is usually a clear-cut ethical breach, imagine a scenario where an adviser does so to secure a client’s access to an investment opportunity that genuinely serves their best interests. It’s still wrong, of course, but some might argue it was done with good intentions.

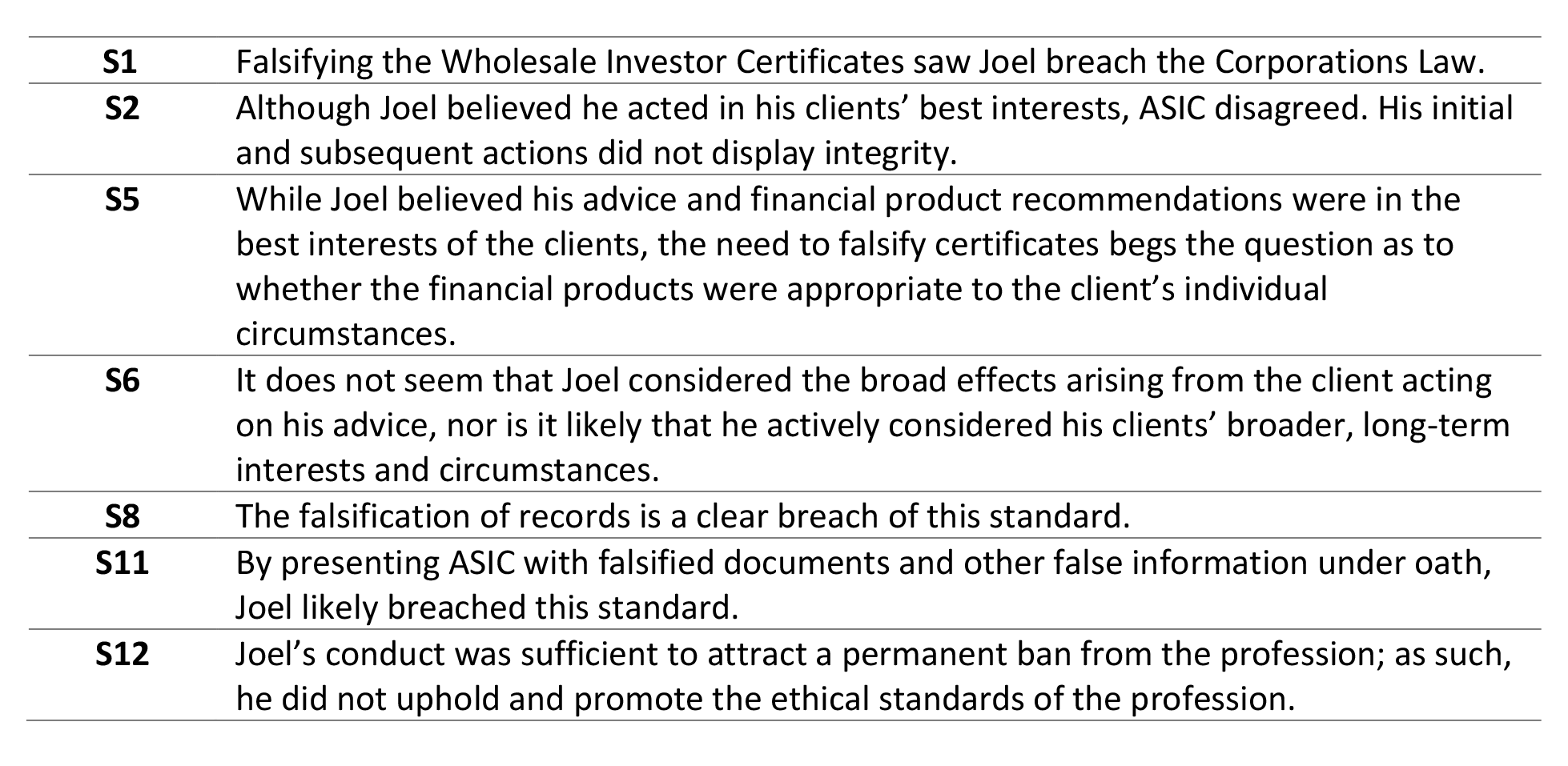

Joel, a financial adviser in Brisbane, found himself in serious trouble after providing several of his clients with falsified wholesale client certificates. His aim was to give them access to financial products typically reserved for “sophisticated investors,” as defined by Chapter 6D of the Corporations Act 2001. These certificates should have been issued by a qualified accountant, verifying the client met specific net asset or gross income criteria.

Joel genuinely believed these financial products were in his clients’ best interests, offering exposure to asset classes difficult for retail investors to access and with lower fees.

However, during an ASIC audit of Joel’s practice, he presented these falsified documents. He was subsequently accused of repeatedly attempting to deceive the corporate regulator. As a result, ASIC issued Joel a permanent ban for misleading or deceptive conduct related to the fabricated evidence. He had also knowingly provided false answers and information concerning the fake documents when questioned, both under oath and via statutory notice.

Joel’s actions went further, including fabricating other evidence like emails and witness statements, which were used during an ASIC hearing. These deliberate acts of deception moved Joel’s initial intent, which might have started in a “grey zone,” firmly into the realm of clear misconduct.

Joel’s actions see him potentially breaching the following standards in the Code of Ethics.

The Code of Ethics makes ethical practice a binding requirement for financial advisers, no matter if a situation is clearly defined or presents a moral dilemma with many ‘shades of grey’. Advisers have a fundamental obligation to consistently prioritise their clients’ best interests and uphold ethical standards. While this might seem like an obvious expectation, frequent media reports of misconduct and its repercussions unfortunately highlight that some practitioners and advice practices neglect these vital responsibilities.

A genuinely ethical and professional partnership between adviser and client forms when the client fully understands the adviser’s recommendations and trusts that the advice truly serves their best interest. If there’s any uncertainty about the advice, especially when the right course of action isn’t entirely clear-cut, it’s crucial to consider the ultimate benefit to the client.

Ask yourself: Will your client be in a better position if this advice is implemented? Does the advice go against any standards in the Code of Ethics? Does it align with your personal moral code? If any ambiguity remains, it’s always wise to discuss it with your colleagues and licensee.

At its heart, ethics is about discerning the right course of action for your clients and steadfastly following through—always with the best interests of every client at the forefront.

Take the FAAA accredited quiz to earn 0.75 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Professionalism and Ethics (0.75 hrs)

ASIC Knowledge Requirements: Ethics (0.75 hrs)

please log in to start this quiz

———

Notes:

[1] https://www.simplypsychology.org/kohlberg.html

[2] Codes of Ethics as Signals for Ethical Behavior; Adams, Tashchian & Shore, February 2001

[3] https://brainhub.eu/library/benefits-of-code-of-ethics

[4] SMSF Quarterly Statistical Report March 2025, ATO

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: Professionalism and Ethics (0.75 hrs)

ASIC Knowledge Requirements: Ethics (0.75 hrs)

please log in to start this quiz

———

Notes:

[1] https://www.simplypsychology.org/kohlberg.html

[2] Codes of Ethics as Signals for Ethical Behavior; Adams, Tashchian & Shore, February 2001

[3] https://brainhub.eu/library/benefits-of-code-of-ethics

[4] SMSF Quarterly Statistical Report March 2025, ATO

Have feedback on this article? Contact Us

Earn CPD Points

CPD: Consumer protection essentials – AFCA and advice complaints

CPD: Consumer protection essentials – AFCA and advice complaintsAs essential component of a robust framework for protecting financial consumers is the presence of mechanisms that hold individuals and organisations to account for causing consumer harm and allow consumers [...]

CPD: A new approach to assessing risks in retirement

CPD: A new approach to assessing risks in retirementIn our last article, we examined the common risks that can impact retirement. The financial risks we’re all acutely aware of: longevity risk, inflation risk, market risk and sequencing risk. [...]

CPD: Ethics and financial abuse

CPD: Ethics and financial abuseFinancial abuse is becoming more prevalent in Australian society. This article, proudly sponsored by GSFM, examines financial abuse in the context of an ethical financial advice practice. A lot of [...]

CPD: Seeking stability

CPD: Seeking stabilityAt a time of sweeping geopolitical change and clear challenges for riskier assets, bond markets offer a source of stability. Key takeaways The world has entered a period of geopolitical [...]

CPD: The year ahead for fixed income markets

CPD: The year ahead for fixed income marketsThe forces shaping fixed-income markets found themselves at a confluence of economic, fiscal, and political factors heading into 2025. Inflation dynamics remained in flux, a new Treasury Department was in [...]