Bifurcation in the economy matters deeply for investors, particularly in fixed income.

When Charles Dickens opened A Tale of Two Cities with his now-famous line, he was describing a world defined not by a single prevailing condition, but by sharp contrasts existing at the same moment in time. Prosperity and hardship, confidence and fear, progress and stagnation were not sequential chapters, they were simultaneous realities, depending on where one stood.

In the view of fixed income specialists Payden & Rygel, today’s global economy bears a striking resemblance. Headline data suggest resilience: growth has proven more durable than expected, labour markets remain firm in many regions, and asset prices continue to reflect optimism around technological innovation and future productivity.

Yet beneath the surface lies a far more uneven picture. Large parts of the economy remain under pressure from inflation, higher borrowing costs and constrained affordability. Wealth and income outcomes have diverged meaningfully, as have regional growth paths across the globe.

This bifurcation matters deeply for investors, particularly in fixed income. A world defined by dispersion rather than uniformity rewards selectivity and flexibility, and it places a premium on sourcing risk away from traditional benchmarks.

It challenges the usefulness of averages and elevates the importance of understanding who is benefiting, who is struggling, and where capital is truly being compensated.

This article frames the investment environment as a modern Tale of Two Cities and explores three areas where the ‘best of times’ and the ‘worst of times’ coexist:

- the concentration of growth driven by AI and capital investment

- the widening divide between asset owners and non-asset owners

- the divergence between China and the rest of the emerging market universe.

Together, these contrasts help explain not only where opportunities exist today, but why a global, unconstrained approach to fixed income remains essential as we navigate the year ahead.

The First Divide

Concentrated Growth in an AI-Driven Economy

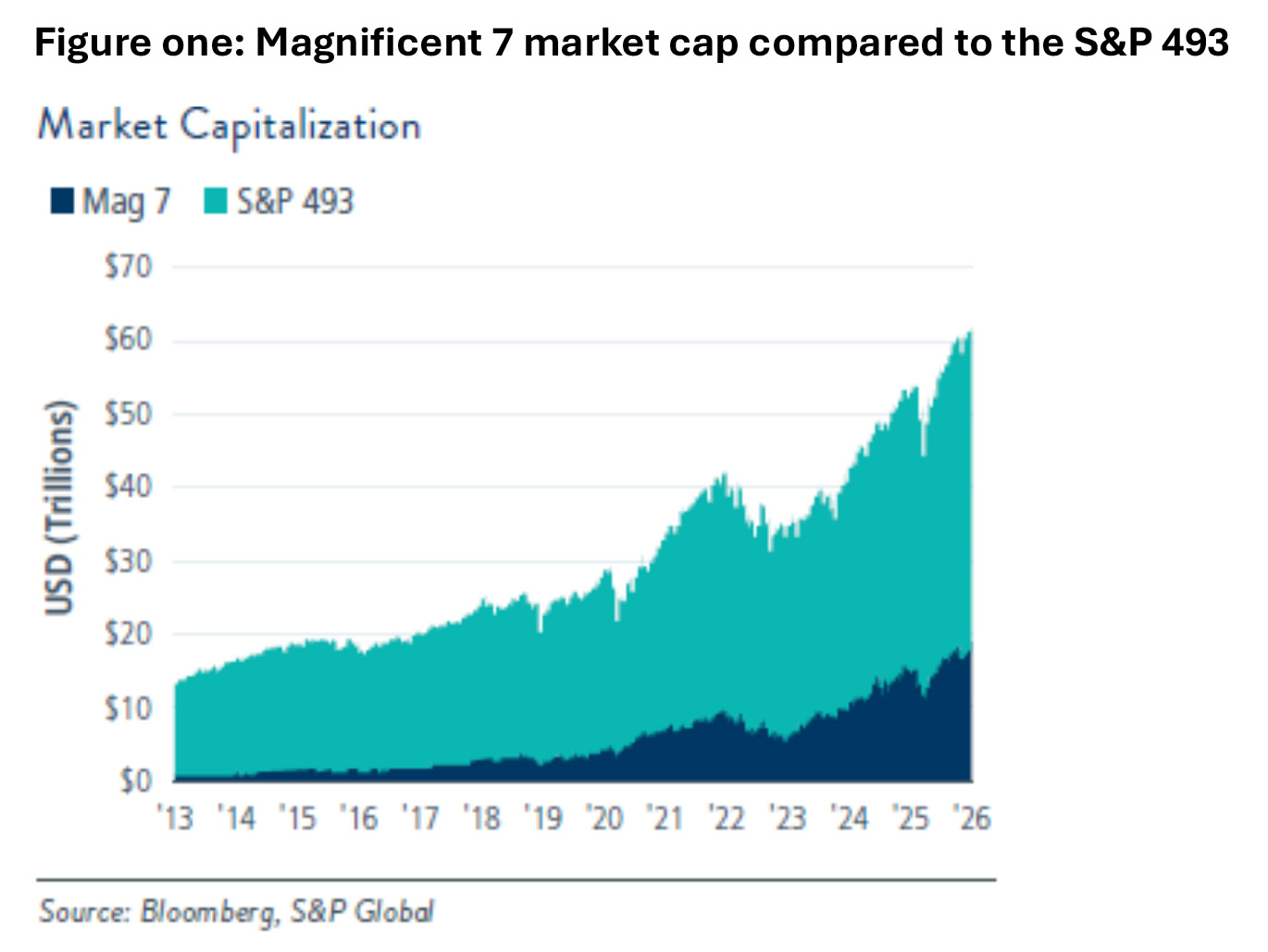

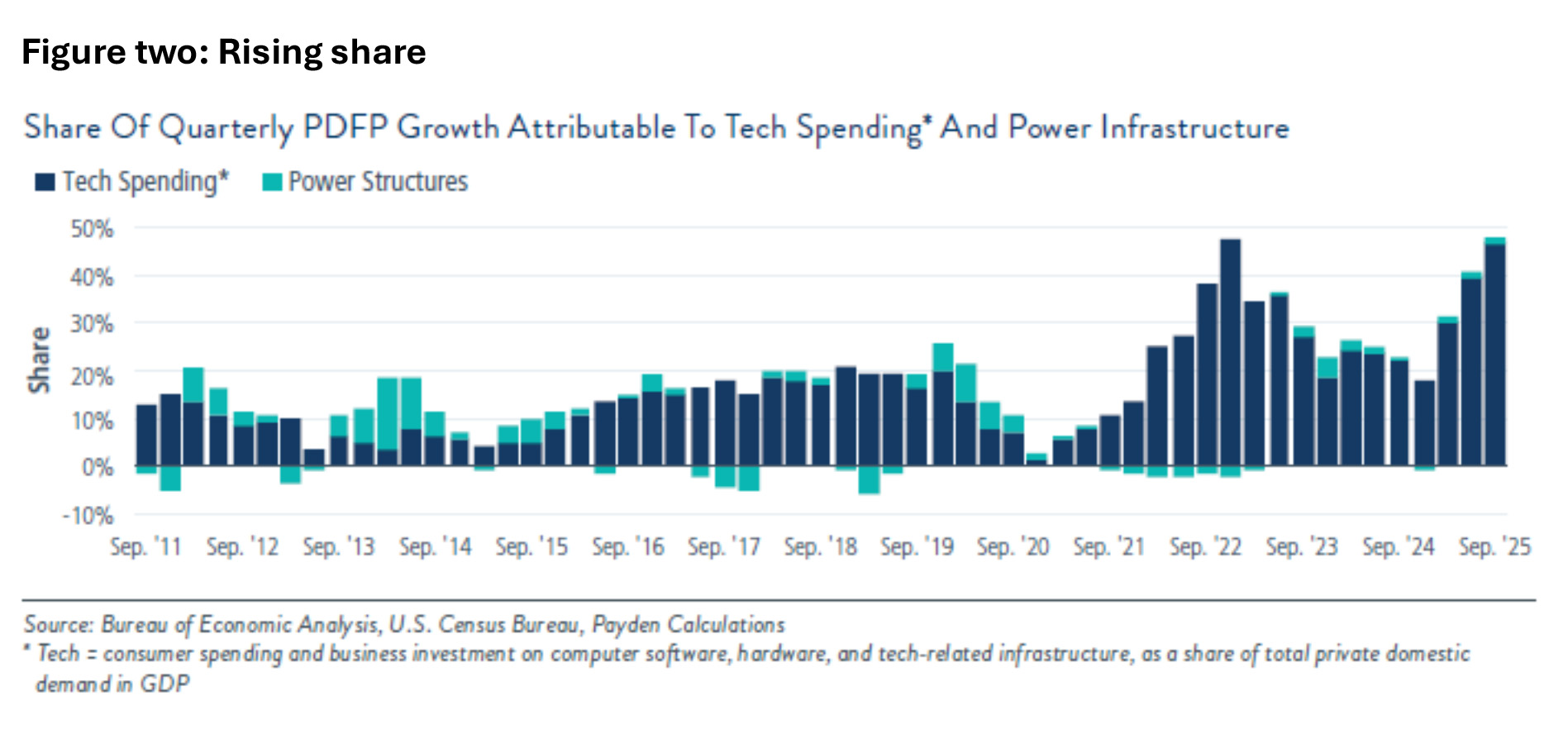

The first, and perhaps most discussed, dynamic in today’s economy is the growing divide between areas experiencing strong, durable growth and those that are languishing. At the centre of the ‘best of times’ sits a powerful – but highly concentrated – investment cycle driven by artificial intelligence and the capital expenditures required to support it. Spending on semiconductors, data centres, power infrastructure and automation has surged, supporting earnings expectations and asset valuations for a relatively narrow set of beneficiaries (figures one and two).

Outside of these areas, however, the picture is far less robust. Many parts of the economy continue to face sluggish productivity growth, tighter financial conditions and limited pricing power. For these sectors, higher interest rates have proven more challenging, while the spillover effects from technological investment have so far been modest. The result is an economy where growth exists but is unevenly distributed, and where headline GDP masks a wide dispersion of underlying outcomes.

For investors, this distinction is critical. A concentrated growth environment can remain resilient for longer than expected, even in the face of restrictive monetary policy. That dynamic supports an ongoing willingness to own credit, as default risk remains contained among growth beneficiaries and higher-quality borrowers.

At the same time, it argues strongly against indiscriminate exposure. When growth leadership is narrow and well understood, simply buying the market often offers limited compensation for risk.

Instead, this is an environment that in fixed income, rewards idiosyncratic credit selection. Within portfolios, this has meant sourcing credit exposure through areas where structure, collateral, and dispersion create opportunities, such as select segments of Commercial Mortgage-Backed Securities (CMBS) rather than relying on broader corporate beta in areas such as Collateralised Loan Obligations (CLOs). In CMBS, careful underwriting and security selection allow the astute investment manager to participate in economic resilience while avoiding some of the most crowded expressions of risk.

This theme of dispersion, of some thriving while others struggle, extends beyond corporate investment and into the household sector, where the contrast between economic ‘cities’ becomes even more pronounced.

The Second Divide

Asset owners and inflation’s uneven burden

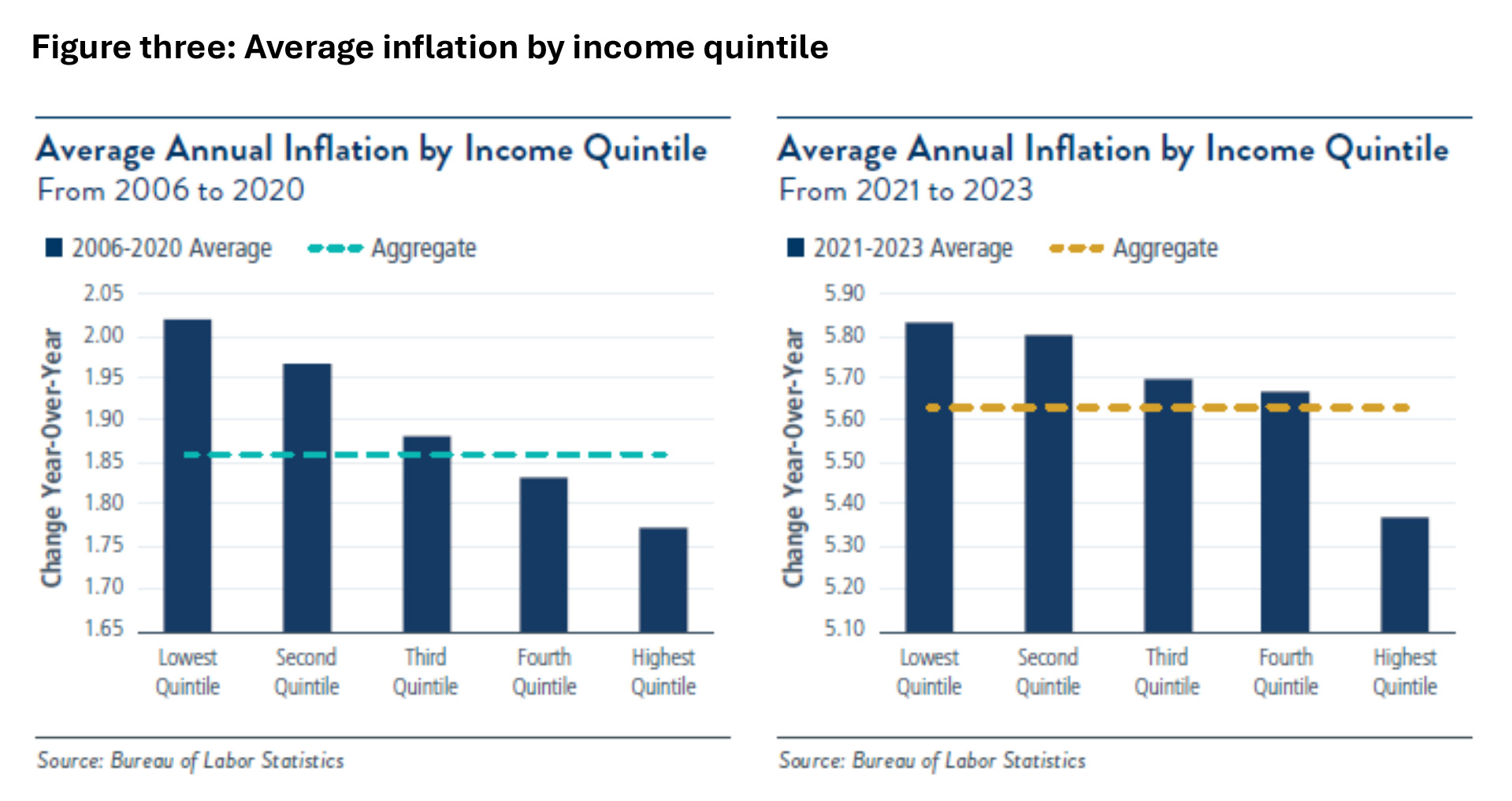

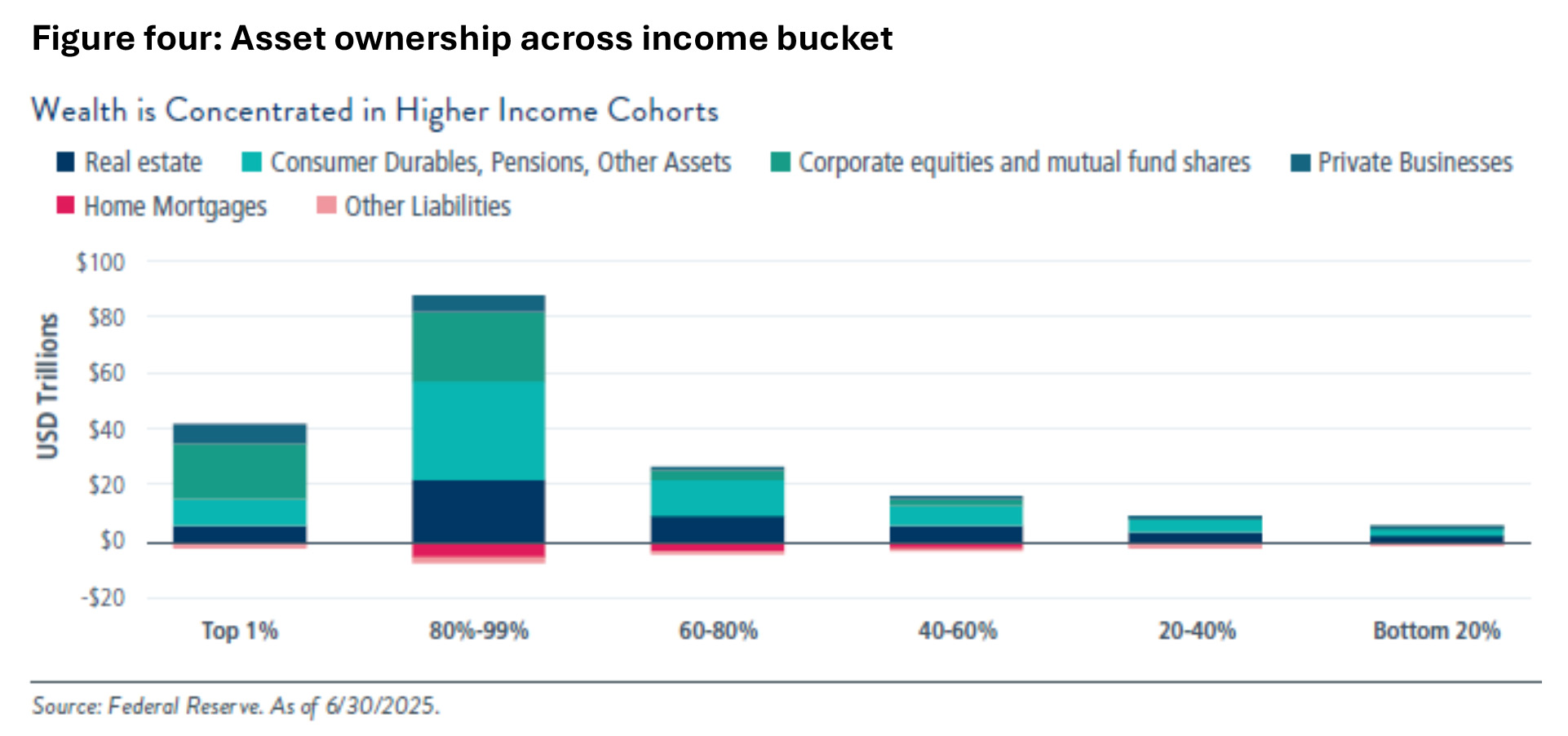

The second divide is defined by a widening gap between those who own assets and those who don’t. For households with equity holdings, real estate ownership or fixed-rate debt locked in prior to the rate hiking cycle, the past several years have been relatively forgiving. Rising asset prices and stable employment have helped offset higher living costs, leaving many higher-income households financially resilient.

For lower-income cohorts and non-asset owners, the experience has been markedly different. Inflation has been most acute in essentials such as housing, food and insurance; categories that represent a disproportionate share of spending for these households. At the same time, higher interest rates have pushed homeownership further out of reach, limiting wealth accumulation and reinforcing financial insecurity. While aggregate consumption data remain buoyant, they increasingly conceal pockets of stress beneath the surface.

This uneven transmission of inflation and monetary policy has important implications for credit markets. Aggregate indicators may suggest stability, but credit performance is diverging meaningfully by income, asset ownership and borrower quality. In Payden’s view, this calls for a more selective approach to consumer exposure.

Within portfolios, Payden has expressed this view through a preference for the prime and super-prime consumer, particularly in residential mortgage credit, where borrower balance sheets remain relatively strong and structural housing undersupply continues to provide support. Conversely, the firm has remained cautious toward below-prime segments of the consumer, including portions of auto ABS and unsecured consumer credit, where affordability pressures are intensifying and credit stress is more likely to emerge.

This same bifurcation informs sector exposure. Payden continues to favour defensive areas of the economy, such as grocery retail, where demand remains resilient across income levels, while avoiding segments more reliant on discretionary spending from financially stretched consumers.

Just as household outcomes are diverging domestically, so too are economic trajectories across the global landscape. The contrast between resilience and strain is increasingly visible across regions, most notably between China and the rest of the emerging market (EM) world.

The Third Divide

China and the myth of a monolithic EM

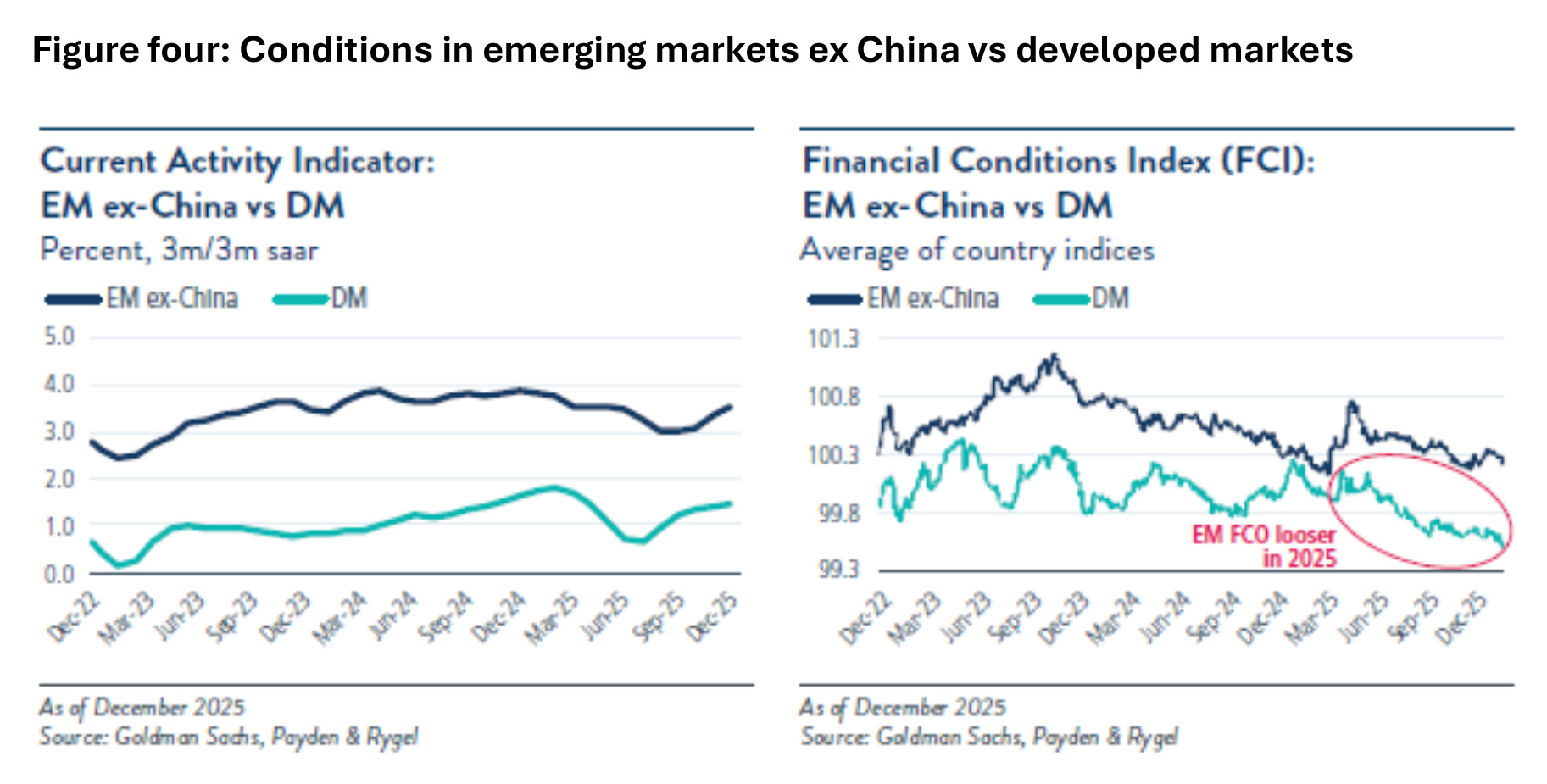

Nowhere is the ‘two cities’ metaphor more evident than within emerging markets. China, long viewed as the anchor of EM growth, continues to face a challenging adjustment. A prolonged real estate downturn, weak consumer confidence, unfavourable demographics – particularly among younger cohorts – and diminishing returns to policy stimulus have weighed on economic output. It is Payden’s view that these challenges are not merely cyclical, but structural in nature.

In contrast, many other EM economies are experiencing a more favourable environment. Growth remains relatively robust, inflation has moderated and policy credibility has improved across several regions. A weaker US dollar has also provided relief for local currencies and balance sheets, supporting domestic demand and external financing conditions.

This divergence underscores a critical point: China does not equal emerging markets. EM dispersion today is structural, not cyclical, and broad generalisations obscure meaningful differences in fundamentals and return potential. For investors, this elevates the importance of fundamental analysis, country selection and currency exposure.

Within portfolios, emerging markets have been Payden’s preferred expression of beta in recent quarters, across both hard-currency sovereign debt and local market exposures. Valuations remain reasonable relative to developed markets and in many cases, EM fundamentals compare favourably to those of countries where debt burdens are higher and growth prospects less compelling.

Positioning further strengthens the case. Emerging markets remain a structurally under-owned asset class, particularly relative to developed markets such as the United States, where global investors are overweight equities and both public and private credit. In a world defined by dispersion and crowding, this imbalance creates opportunity as foreign investors look to diversify a portion of their overallocation to the US going forward.

Where to invest in a bifurcated economy

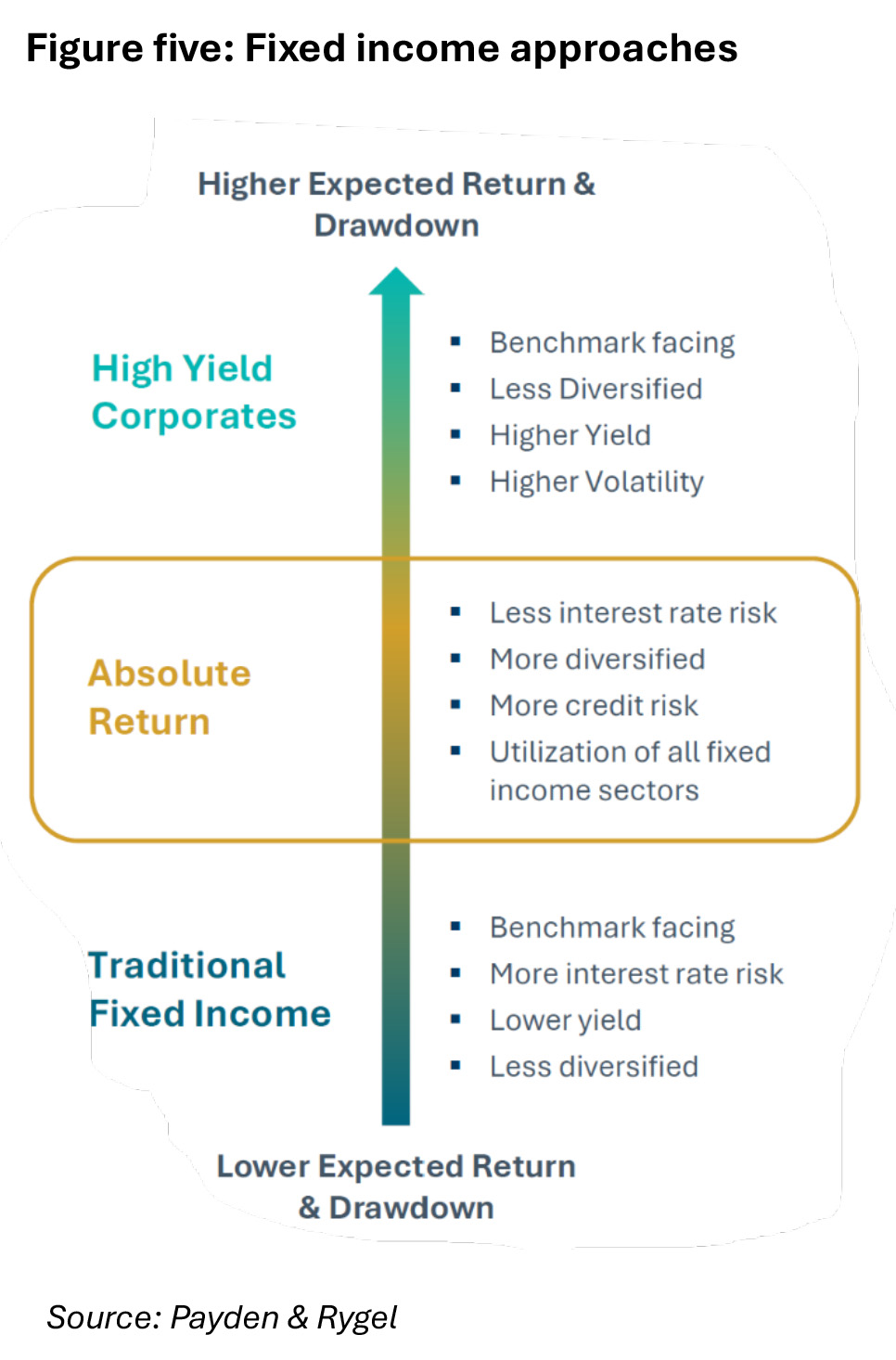

Given these three divides, how do you best manage your clients’ exposure to fixed income? With an economic environment characterised by uncertainty, many investors turn to unconstrained or absolute return fixed income strategies rather than the more traditional bond funds.

Traditional fixed income funds (as well as passive bond funds and ETFs) typically focus on relative return, striving to outperform benchmarks such as the Bloomberg Global Aggregate Bond Index. However, this approach often forces managers to mirror the index’s structure, leading to specific risks that investors should consider.

While a market-cap-weighted index provides a snapshot of the bond market, replicating it may not be the most prudent investment strategy for several reasons:

- By design, these indices give the highest weightings to the most indebted entities, providing a ‘reward for debt’. A benchmark-hugging strategy essentially increases your exposure to those with the most leverage.

- Passive and relative-return funds are often tethered to long-duration assets, increasing duration risk; this may not be the optimal position particularly when the economic environment is unstable.

- Any strategy that mimics an index inevitably inherits that index’s specific vulnerabilities.

In today’s climate of geopolitical tension and economic uncertainty, the ‘set it and forget it’ nature of benchmark-based investing is being challenged. When the market is unpredictable, a rigid adherence to traditional indices may no longer be the most effective way to preserve or grow capital.

Unlike traditional bond funds where most of the return is driven by the performance of the benchmark (figure five), returns from unconstrained strategies are driven by the investment approach adopted by the manager.

Unlike traditional funds, an absolute return strategy operates independently of rigid bond benchmarks. This flexibility allows managers to navigate a shifting economic landscape with greater precision, focusing on positive gains rather than simply trying to beat a fluctuating index.

By benchmarking against cash equivalents rather than a broad bond index, these strategies unlock several strategic benefits:

- Unconstrained flexibility, with managers not tied to specific sectors or durations. They can pivot across the entire fixed income spectrum to find the best risk-adjusted opportunities for your clients.

- These funds typically maintain lower duration (and lower duration risk), meaning they are less sensitive to interest rate hikes. This is a crucial advantage in a volatile rate environment.

- While traditional managers may be slowed down by benchmark constraints, absolute return managers can adjust their positioning rapidly as market conditions evolve.

Absolute return fixed income in the current environment

US policy is the wild card in 2026, and the long end of the yield curve has been responding more to policy than it has to fundamentals. Payden does not believe that investors are being compensated to incur the level of volatility in the long end of the yield curve; and probably won’t be compensated until there is clarity around US economic policy. This includes a new chair of the US Federal Reserve in May, ongoing issues around tariffs and other geopolitical and domestic events.

A key benefit of an absolute return portfolio is being able to identify risk and swiftly take appropriate action to protect the portfolio. Being able to do this early is paramount; when things go poorly and investors are trying to exit positions at the same time, it can have negative consequences for the portfolio.

Because an absolute return fixed income portfolio isn’t managed to a benchmark, there are fewer risks that need to be managed to (such as duration or liquidity risk). It provides the investment manager with greater flexibility and greater latitude with respect to asset class participation; securitised assets, corporate bonds, emerging market debt, developed government debt. In short, a lot of opportunity for diversification.

An absolute return approach to fixed income is better placed in the current environment because it:

- Removes the benchmark from the equation

- Can focus on companies/countries with the least amount of debt

- Can focus on lower duration securities

- Actively selects issuers that will add value to the portfolio

- Can embed additional yield for investors

- Actively manages risk exposure irrespective of benchmark positions

- Focuses on positive returns.

Regardless of the strategy chosen, fixed income remains a cornerstone of a balanced portfolio. The asset class continues to provide stable income through the reliable interest payments and the return of principal. Importantly, fixed income provides portfolio diversification and can be a defensive buffer during equity market turbulence.

Dickens’ A Tale of Two Cities was ultimately not just a story of contrast, but one of navigation, of individuals and institutions forced to operate between extremes rather than choosing a single reality. That lesson resonates strongly in today’s investment environment.

The defining feature of the current cycle is not whether growth persists or falters, inflation rises or falls, or policy tightens or eases. It is that very different outcomes are unfolding at the same time, across sectors, households and regions. Concentrated growth driven by capital investment coexists with broader economic fatigue. Asset owners experience resilience while affordability challenges intensify for others. China’s struggles stand in contrast to healthier dynamics across much of the emerging market world.

For fixed income investors, this is not a backdrop that rewards blunt positioning or reliance on historical correlations. Instead, it favours a global, unconstrained approach, one that embraces dispersion, emphasises selectivity and seeks to source risk where it is genuinely compensated.

In Dickens’ world, the future was shaped by those who understood the forces at work on both sides of the divide. In today’s markets, Payden believes the same holds true. By recognising where it is the best of times, where it is the worst of times, and, most importantly, how those realities intersect, the firm aims to navigate a complex and bifurcated global economy with discipline, flexibility and consistency.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Fixed Interest (0.5 hrs)

please log in to start this quiz

——–

The information included in this article is provided for informational purposes only and is general advice only. It does not take into account an investor’s own objectives. The information contained in this article reflects, as of the date of publication, the current opinion of GSFM and is subject to change without notice. Sources for the material contained in this article are deemed reliable but cannot be guaranteed. We do not represent that this information is accurate and complete, and it should not be relied upon as such. Any opinions expressed in this material reflect our judgment at this date, are subject to change and should not be relied upon as the basis of your investment decisions. All reasonable care has been taken in producing the information set out in this article however subsequent changes in circumstances may occur at any time and may impact on the accuracy of the information. Neither Payden & Rygel, GSFM Pty Ltd, their related bodies nor associates gives any warranty nor makes any representation nor accepts responsibility for the accuracy or completeness of the information contained in this article.

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Technical Competence (0.5 hrs)

ASIC Knowledge Requirements: Fixed Interest (0.5 hrs)

please log in to start this quiz——–

The information included in this article is provided for informational purposes only and is general advice only. It does not take into account an investor’s own objectives. The information contained in this article reflects, as of the date of publication, the current opinion of GSFM and is subject to change without notice. Sources for the material contained in this article are deemed reliable but cannot be guaranteed. We do not represent that this information is accurate and complete, and it should not be relied upon as such. Any opinions expressed in this material reflect our judgment at this date, are subject to change and should not be relied upon as the basis of your investment decisions. All reasonable care has been taken in producing the information set out in this article however subsequent changes in circumstances may occur at any time and may impact on the accuracy of the information. Neither Payden & Rygel, GSFM Pty Ltd, their related bodies nor associates gives any warranty nor makes any representation nor accepts responsibility for the accuracy or completeness of the information contained in this article.

Have feedback on this article? Contact Us

Earn CPD Points

CPD: The spectrum of growth

CPD: The spectrum of growthCompanies that generate strong, sustainable growth are valuable sources of long term capital appreciation in a portfolio, but these businesses are rare, difficult to identify and exist on a broad [...]

CPD: Record-keeping in financial advice – the key to compliance and consumer protection

CPD: Record-keeping in financial advice – the key to compliance and consumer protectionIntroduction The financial services regulatory framework is a key pillar of financial consumer protection. Regulatory compliance is therefore not merely about avoiding penalties, but is a critical step in building [...]

CPD: Trust and ethics in financial advice

CPD: Trust and ethics in financial adviceIn 2024, trust in financial advisers reached an all-time high. This article, proudly sponsored by GSFM, explores the inseparable links between trust and ethical practice when providing financial advice. Defined [...]

CPD: Retirement Income Strategies

CPD: Retirement Income StrategiesIt has been almost 40 years since award superannuation was introduced in Australia, and 33 years since the introduction of mandatory occupational superannuation. This means the next decade will see [...]

CPD: Free cash flow works

CPD: Free cash flow worksThe difference between earnings and free cash flow is an important investment concept, one explained here by GSFM’s investment partner TD Epoch. Earnings have long played a dominant role in [...]