CPD: SMSF advice under the microscope – what REP 824 means for advisers

ASIC’s findings across REP 575 and REP 824 highlight that the consumer protection risks associated with SMSFs are not theoretical.

Introduction

When considering the various sector reviews conducted by ASIC during 2025, one could be forgiven for recalling Taylor Swift’s sentiment from 2017 “This is why we can’t have nice things”.

Because true to their brief of revealing the (small number of) bad apples in advice, and hot on the heels of exposing red flags in both the private credit and managed account sectors, November 2025 saw ASIC turn its gaze to Self-Managed Super Funds (SMSFs), with the release of REP 824, a damning examination of the advice behind SMSF establishments.

The headline finding of this review was that more than 60% of the advice files reviewed failed the Best Interests Duty and were therefore non-compliant[1]. The review also identified a consistent pattern of other advice failures, explored in more detail below.

ASIC’s scrutiny of SMSF establishments, and the advice behind them, comes at a time of record growth for the sector, which now comprises over 1.2 million members, holding over $1 trillion in assets in more than 650,000 funds[2]. It also comes at a time when AFCA complaints about SMSF advice almost doubled over 12 months, to now represent a third of all advice complaints[3].

For advisers, the sheer size and significance of the SMFS sector (it accounts for around one quarter of total superannuation savings[4]), as well as ASIC’s heightened scrutiny, makes it imperative to understand the full compliance context for SMSF advice, including the consumer motivations behind SMSF establishment and the challenges in managing SMSFs.

As well as examining this context, this article will explore the reasons ASIC regard SMSF advice as high risk, explain the detailed findings and recommendations of REP 824[5], and provide a practical framework for advisers to ensure their advice in this sector remains compliant and in the best interests of clients.

Consumer context: the myth of control and love of property drives SMSF growth

In order to appreciate the reasons for ASIC’s concerns, and their likely areas of focus, it is helpful to first understand the context for the popularity of SMSFs.

In their 2018 report into SMSF advice – REP 575 – ASIC found that the strongest single consumer motivation to establish an SMSF was a desire to have more ‘control’ – cited by 48% of trustees establishing SMSFs between 2015 and 2018[6].

This control included financial control (for example, anticipated control over investment performance); and emotional control (for example, investing in an asset class that gives a greater feeling of security). Other motivations included the desire to purchase a property (22%), the desire to have more say in equity selection (29%), and the desire to pay lower fees (25%).

In the years since 2018, this context has evolved significantly. Downward pressure on fund manager and administration fees has been significant, undermining the ‘I can do it myself cheaper’ argument. And when it comes to control, consumers have far more avenues to be ‘hands -on’ with their investments, either through innovative retail offerings, or managed accounts. In other words, the strength of these particular motivations has diminished somewhat.

What has endured however is the desire to use SMSFs as a vehicle to purchase property.

While for older investors, this was often due to an inherent conservatism – manifesting as an overriding preference for bricks and mortar – in more recent times, investors in their mid-forties (the median age for new SMSFs is 46[7]) are seeing SMSFs as a way to secure an investment property in an increasingly expensive market.

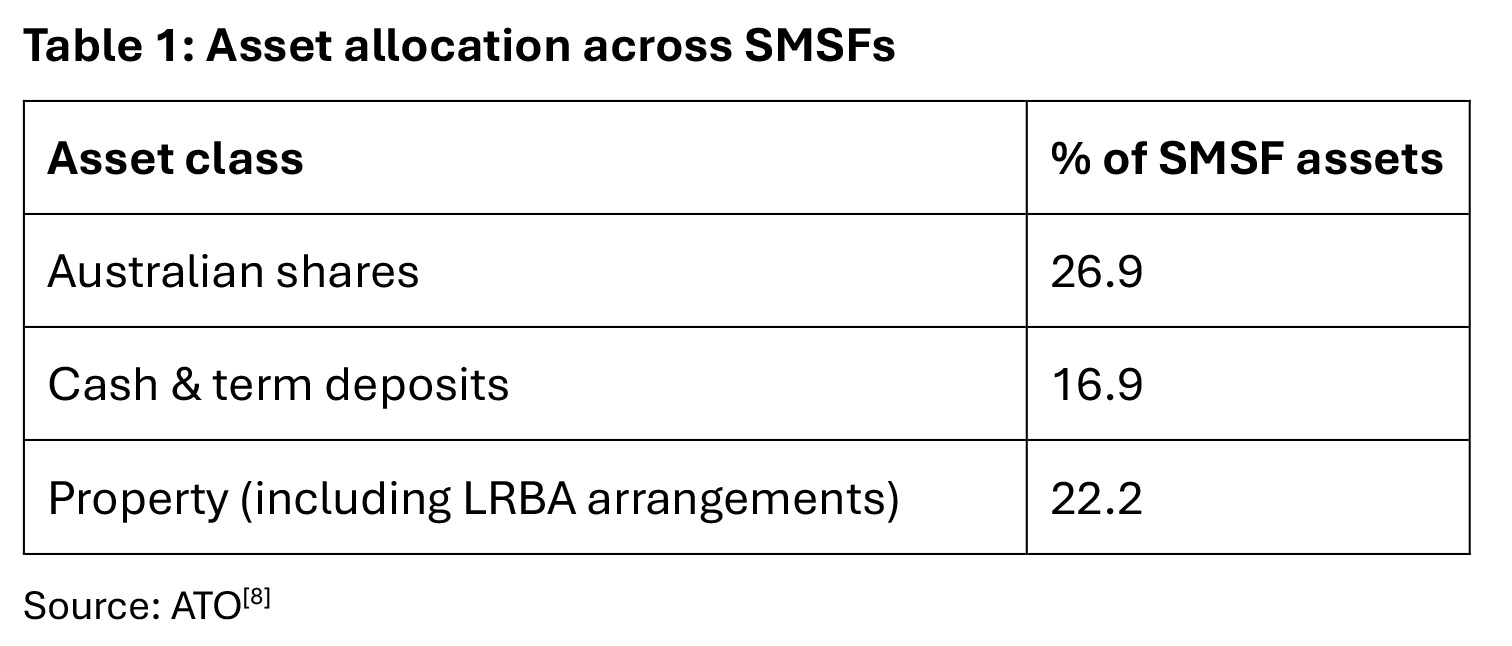

This nexus between property and SMSFs is plain for all to see when one examines ATO data on asset allocation. As seen in Table 1, property (residential and commercial) accounts for 22.2% of all SMSF assets.

SMSF ownership does not signal any degree of financial savvy, nor particularly high levels of wealth.

The stereotype of the SMSF as a ‘mum and dad fund’ is reasonably accurate, with around 68% of SMSFs comprising two members. While the median asset holding for all funds is $933,000, new funds are being established with median assets of just $345,000. Just over half of all SMSFs are in the accumulation phase[9].

Despite their superior long term growth potential compared to domestic equities, overseas shares are not widely held, with ATO data showing they account for just 2.1% of assets for funds in accumulation phase (when growth should be prioritised) – another signal of an overall lack of sophistication.

Asset concentration, borrowing and retirement risk

Asset concentration within SMSFs has been a persistent concern for ASIC, evident across both REP 575 and REP 824, particularly where property and borrowing are involved.

While concentration risk can exist in any investment structure, ASIC has repeatedly observed that it is most acute in newly established SMSFs, and often insufficiently addressed in advice files.

ATO data shows that a material proportion of SMSFs hold extremely concentrated portfolios. Almost 30 per cent of SMSFs have 90 per cent or more of their assets invested in a single asset class, with around one-third of those funds concentrated in property[10]. This level of concentration significantly increases exposure to liquidity risk, valuation risk and sequencing risk, particularly as members approach retirement.

Borrowing amplifies these risks at the point of establishment. REP 824 found that 50 per cent of the SMSF establishment advice files reviewed involved a limited recourse borrowing arrangement (LRBA), most commonly to facilitate direct property investment[11]. ASIC observed that advisers frequently failed to adequately assess whether the SMSF could sustain loan repayments under adverse conditions, such as interest rate increases, rental vacancies or reduced contributions. Stress testing and downside analysis were often absent from client files.

Separate from servicing risk, ASIC also identified systemic liquidity weaknesses. Property-heavy SMSFs with LRBAs often had limited capacity to fund ongoing expenses or pension payments without relying on continued contributions or asset sales. ASIC noted that advisers frequently underestimated how illiquid assets constrain cash-flow flexibility over time, particularly once members transition into retirement, when contribution inflows cease and benefit payments commence.

ASIC also linked concentration and borrowing risk to poor insurance outcomes. In several high-risk files, advisers recommended establishing an SMSF and acquiring property without adequately considering the erosion of insurance cover previously held within APRA-regulated funds. Where insurance was retained, it was often reduced or poorly aligned to the fund’s increased financial risk profile.

High-risk SMSF business models and conflicts of interest

ASIC’s review also highlights that non-compliant SMSF advice is frequently associated with particular business models, rather than isolated adviser error. A recurring feature of higher-risk files reviewed for REP 824 was the presence of property-led SMSF establishment models. In these arrangements, the decision to establish an SMSF was often closely linked to a pre-determined property acquisition, sometimes supported by an LRBA. ASIC observed that where property outcomes effectively drove the advice, assessment of alternatives, diversification, liquidity and retirement outcomes was frequently subordinated or incomplete.

ASIC also identified risks arising from lead-generation and referral arrangements, particularly where advisers received clients from property promoters, accountants or marketing businesses with a commercial interest in SMSF establishment. Even where such arrangements were disclosed, ASIC questioned whether advisers had taken sufficient steps to ensure that the advice was free from undue influence and demonstrably prioritised client interests over third-party outcomes.

Vertical integration and related-party arrangements were another area of focus. ASIC found that in some cases, advisers recommended SMSF strategies that directed revenue toward related entities through property development fees, borrowing arrangements, administration services or ongoing advice fees. REP 824 reinforces that disclosure alone is not sufficient where conflicts are material. Advisers and licensees must be able to demonstrate that conflicts have been actively identified, managed and, where necessary, avoided.

Importantly, ASIC’s findings make clear that these risks are not mitigated by client consent or enthusiasm. Where advice outcomes align too neatly with commercial incentives, ASIC will look closely at whether the advice was shaped by professional judgement or by the underlying business model. In REP 824, files associated with conflicted or property-centric models were disproportionately represented among those assessed as posing a high risk of consumer detriment.

Where commercial structures increase the likelihood of bias, ASIC expects stronger governance, clearer separation of functions and more rigorous documentation to demonstrate that client interests have genuinely been prioritised.

Other risks faced by SMSFs

In addition to those risks driven by market context, trustees and members face a variety of other significant risks, including, but not limited to:

- Risks associated with the complexity of managing the administration and compliance obligations of SMSFs

- Underestimating the time and cost of managing an SMSF

- The costs of small balance funds

- Insurance cover risks (through inappropriate cancellation of existing cover or reduced access to group rates)

- Poor investment decisions made by unsophisticated investors

- Reduced access to dispute resolution bodies

- Lack of statutory compensation for theft or fraud

- Complexities and costs associated with fund structure, including

- Winding up the fund in the event of death or relationship breakdown

- Loss of capacity of a trustee

- Fund value falling below a financially viable level

- The treatment of death benefit nominations

These risks add an additional layer of complexity that advisers must be conscious of when providing SMSF advice.

REP 824 in detail: where SMSF advice fails

REP 824 concludes that the compliance issues identified in SMSF establishment advice are not isolated technical errors, but recurring failures in how advisers apply professional judgement. In conducting their review, ASIC reviewed 100 SMSF establishment advice files and found that 62 failed to demonstrate compliance with the Best Interests Duty (BID), with 27 raising significant concerns about potential client detriment. These failures occurred across a range of adviser and licensee business models, suggesting systemic rather than individual weaknesses.

A central failing was the treatment of SMSF advice as an execution exercise rather than a suitability assessment. ASIC found that in 58 of the reviewed files, advisers did not base their advice on the client’s relevant personal circumstances. In many cases, advisers acted on a client’s stated interest in establishing an SMSF without undertaking a reasonable investigation into whether that structure was appropriate. ASIC was explicit that reliance on client preference, autonomy or a desire for ‘control’ does not satisfy the BID.

Another recurring issue was the failure to properly assess and document alternatives. ASIC found that 53 of the advice files did not demonstrate that advisers had conducted a reasonable investigation into alternatives to an SMSF, including APRA-regulated superannuation funds. Where alternatives were mentioned, documentation often failed to explain why those options were unsuitable in the client’s circumstances, contributing to ASIC’s conclusion that advice lacked a reasonable basis.

Property-driven strategies featured prominently in non-compliant advice. Of the files reviewed, 57 involved direct property investment, and as mentioned previously, 50 involved limited recourse borrowing arrangements. ASIC observed that in many of these cases advisers failed to adequately consider concentration risk, liquidity constraints, cash-flow sustainability or downside scenarios, particularly in retirement. These omissions were a significant factor in files assessed as posing a high risk of client detriment.

ASIC also identified widespread shortcomings in the treatment of insurance and trustee capability. In 16 of the 27 high-detriment files, advisers failed to properly consider insurance needs following SMSF establishment. In addition, ASIC frequently found insufficient assessment of whether clients had the skills, time and capacity to meet their ongoing trustee obligations.

In summary, REP 824 signals that SMSF advice most commonly fails where advisers prioritise client intent, structural preference or commercial convenience over evidence-based suitability analysis.

The legal test ASIC applies to SMSF advice

While REP 824 documents how SMSF advice fails in practice, it also shows how ASIC assesses those failures against the legal framework governing personal advice. ASIC’s analysis is anchored in the BID, the appropriateness obligation, and the requirement that advisers base their advice on a reasonable investigation of relevant alternatives, as set out in the Corporations Act and reinforced through ASIC guidance.

Through INFO 274[12] (‘Tips for giving self-managed superannuation fund advice’) ASIC sets out an expectation that SMSF advice requires advisers to apply heightened professional judgement. Advisers must assess not only the client’s objectives and preferences, but also their financial position, risk tolerance, experience, capability and capacity to meet the ongoing governance obligations of running an SMSF. INFO 274 explicitly warns that an SMSF will not be appropriate for all clients, and that perceived benefits such as control or flexibility must be weighed against costs, risks and complexity.

REP 824 demonstrates how ASIC applies this guidance in practice. Under BID, ASIC rejected advice rationales that relied on client intent, autonomy or a desire for control without evidence that an SMSF delivered a net benefit relative to alternatives. ASIC emphasised that professional judgement cannot be displaced by client request or informed consent.

ASIC also assessed whether advisers could demonstrate that an SMSF recommendation was appropriate in light of the client’s circumstances, including cost-effectiveness, trustee capability and long-term retirement outcomes. Where advisers failed to meaningfully compare SMSFs with APRA regulated superannuation funds, ASIC concluded that the advice lacked a reasonable basis.

Taken together – REPs 575 and 824 and INFO 274 – clarify that SMSF advice is subject to a higher evidentiary threshold than many other superannuation recommendations. Advisers must be able to demonstrate, on file, not only why a client wanted an SMSF, but why establishing one was legally appropriate and in the client’s best interests.

SMSF governance essentials: investment, insurance, and trustee capability

The appropriateness of an SMSF does not turn solely on the decision to establish the fund, but on the quality of its ongoing governance. INFO 274 places particular emphasis on investment governance, insurance considerations and trustee capability, and REP 824 demonstrates how failures in these areas continue to underpin non-compliant advice.

Investment governance and diversification

INFO 274 requires advisers to consider whether clients are capable of implementing and maintaining an appropriate investment strategy within an SMSF, including managing diversification, liquidity and risk over time. ASIC expects advisers to assess not only the proposed asset mix at establishment, but whether the strategy remains sustainable as circumstances change. REP 824 found that advisers frequently failed to articulate an investment rationale beyond facilitating a specific asset purchase, most commonly property, with limited consideration of diversification or downside risk. Where investment strategies were highly concentrated, ASIC expected stronger justification and clearer evidence that risks had been understood and accepted in an informed way.

Cash flow, liquidity and retirement outcomes

ASIC guidance also requires advisers to consider how an SMSF will meet ongoing cash-flow needs, including expenses, loan repayments and pension payments. INFO 274 warns that illiquid or leveraged strategies may be unsuitable where they compromise flexibility or increase the risk of adverse retirement outcomes. REP 824 found that many advice files lacked evidence of stress testing or scenario analysis, particularly where borrowing was involved, undermining the appropriateness of the recommended strategy.

Insurance considerations

Insurance is a recurring governance weakness in SMSF advice. INFO 274 explicitly requires advisers to consider whether clients will have appropriate insurance cover after establishing an SMSF, and whether cover previously held in an APRA-regulated fund will be lost, reduced or become more expensive. REP 824 identified multiple files where insurance was either not considered at all or was addressed superficially, despite the increased financial risk associated with concentrated or leveraged strategies.

Trustee capability and ongoing oversight

INFO 274 emphasises that advisers must assess whether clients have the time, skills and capacity to meet their ongoing trustee obligations. REP 824 shows that advisers often underestimated the operational and compliance burden of SMSFs, particularly for clients with limited experience managing complex investment arrangements. ASIC expects advisers to consider not only initial capability, but how trustee competence will be supported over time.

Practical compliance checklist: what ASIC expects to see in SMSF advice

For advisers and licensees, ASIC’s expectations are easily distilled into a practical checklist:

Before recommending an SMSF

- Clear articulation of why an SMSF is being considered

- Documented comparison with APRA-regulated alternatives

- Assessment of trustee capability, time and experience

- Explicit consideration of costs and scale

Where property or borrowing is involved

- Analysis of concentration risk and diversification

- Cash-flow modelling and stress testing

- Consideration of downside and exit scenarios

- Documentation of why borrowing is appropriate

Investment and insurance governance

- An articulated investment rationale, not just an asset outcome

- Consideration of liquidity and retirement phase needs

- Documented insurance assessment and replacement strategy

Conflicts and oversight

- Identification of any referral, related-party or commercial conflicts

- Evidence of how conflicts were managed, not just disclosed

- Licensee oversight where higher-risk models are used

ASIC’s consistent position is that SMSF advice will be judged on evidence rather than adviser intent.

Conclusion

ASIC’s findings across REP 575 and REP 824 highlight that the consumer protection risks associated with SMSFs are not theoretical. They arise where proactive client demand, asset preference or perceived control displaces disciplined suitability analysis, and where advisers fail to adequately test whether an SMSF structure can support sustainable retirement outcomes over time. The persistence of these issues, despite years of regulatory guidance, suggests that structural risks in SMSF advice remain poorly understood or insufficiently challenged in practice.

Importantly, ASIC’s scrutiny is not confined to whether an SMSF was legally established, but to whether the advice process properly addressed alternatives, risks, governance and trustee capability in a way that was specific to the client’s circumstances. Where advice relies on assumptions of favourable markets, continued contributions or client confidence alone, it is unlikely to meet regulatory expectations. This is particularly so where advice involves borrowing, concentrated investments or the loss of default insurance protections.

SMSF advice demands a higher standard of investigation, documentation and ongoing oversight than many other forms of personal advice. Those who approach SMSFs as a product outcome rather than a governance framework expose clients, and themselves, to unnecessary risk. By contrast, advisers who apply rigorous suitability analysis, clearly evidence their reasoning and maintain disciplined review processes are far better placed to deliver compliant advice and protect long-term client outcomes.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Regulatory Compliance & Consumer Protection (0.5 hrs)

ASIC Knowledge Requirements: SMSF (0.5 hrs)

please log in to start this quiz

———

References:

[1] https://www.afr.com/companies/financial-services/most-smsf-advice-not-complying-with-best-interest-test-asic-says-20251106-p5n86t

[2] https://www.ato.gov.au/individuals-and-families/super-for-individuals-and-families/self-managed-super-funds-smsf/smsf-newsroom/latest-annual-statistics-for-smsfs

[3] https://www.professionalplanner.com.au/2025/07/afca-complaints-show-tale-of-two-sectors/

[4] https://data.gov.au/data/dataset/2fd970ec-984e-4593-bbad-2e69a5fa7a89/resource/7a50c5c8-5c0e-4a4b-a11e-feaad39f2bd0/download/smsf-annual-overview-2023-24.xlsx

[5] https://download.asic.gov.au/media/g2jloagp/rep824-published-6-november-2025.pdf

[6] https://download.asic.gov.au/media/4779820/rep-575-published-28-june-2018.pdf

[7] https://www.ato.gov.au/individuals-and-families/super-for-individuals-and-families/self-managed-super-funds-smsf/smsf-newsroom/latest-annual-statistics-for-smsfs

[8] https://data.gov.au/data/dataset/2fd970ec-984e-4593-bbad-2e69a5fa7a89/resource/7a50c5c8-5c0e-4a4b-a11e-feaad39f2bd0/download/smsf-annual-overview-2023-24.xlsx

[9] https://data.gov.au/data/dataset/2fd970ec-984e-4593-bbad-2e69a5fa7a89/resource/7a50c5c8-5c0e-4a4b-a11e-feaad39f2bd0/download/smsf-annual-overview-2023-24.xlsx

[10] https://data.gov.au/data/dataset/2fd970ec-984e-4593-bbad-2e69a5fa7a89/resource/7a50c5c8-5c0e-4a4b-a11e-feaad39f2bd0/download/smsf-annual-overview-2023-24.xlsx

[11] https://download.asic.gov.au/media/g2jloagp/rep824-published-6-november-2025.pdf

[12] https://www.asic.gov.au/regulatory-resources/financial-services/giving-financial-product-advice/tips-for-giving-self-managed-superannuation-fund-advice/

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: Regulatory Compliance & Consumer Protection (0.5 hrs)

ASIC Knowledge Requirements: SMSF (0.5 hrs)

please log in to start this quiz

———

References:

[1] https://www.afr.com/companies/financial-services/most-smsf-advice-not-complying-with-best-interest-test-asic-says-20251106-p5n86t

[2] https://www.ato.gov.au/individuals-and-families/super-for-individuals-and-families/self-managed-super-funds-smsf/smsf-newsroom/latest-annual-statistics-for-smsfs

[3] https://www.professionalplanner.com.au/2025/07/afca-complaints-show-tale-of-two-sectors/

[4] https://data.gov.au/data/dataset/2fd970ec-984e-4593-bbad-2e69a5fa7a89/resource/7a50c5c8-5c0e-4a4b-a11e-feaad39f2bd0/download/smsf-annual-overview-2023-24.xlsx

[5] https://download.asic.gov.au/media/g2jloagp/rep824-published-6-november-2025.pdf

[6] https://download.asic.gov.au/media/4779820/rep-575-published-28-june-2018.pdf

[7] https://www.ato.gov.au/individuals-and-families/super-for-individuals-and-families/self-managed-super-funds-smsf/smsf-newsroom/latest-annual-statistics-for-smsfs

[8] https://data.gov.au/data/dataset/2fd970ec-984e-4593-bbad-2e69a5fa7a89/resource/7a50c5c8-5c0e-4a4b-a11e-feaad39f2bd0/download/smsf-annual-overview-2023-24.xlsx

[9] https://data.gov.au/data/dataset/2fd970ec-984e-4593-bbad-2e69a5fa7a89/resource/7a50c5c8-5c0e-4a4b-a11e-feaad39f2bd0/download/smsf-annual-overview-2023-24.xlsx

[10] https://data.gov.au/data/dataset/2fd970ec-984e-4593-bbad-2e69a5fa7a89/resource/7a50c5c8-5c0e-4a4b-a11e-feaad39f2bd0/download/smsf-annual-overview-2023-24.xlsx

[11] https://download.asic.gov.au/media/g2jloagp/rep824-published-6-november-2025.pdf

[12] https://www.asic.gov.au/regulatory-resources/financial-services/giving-financial-product-advice/tips-for-giving-self-managed-superannuation-fund-advice/

Have feedback on this article? Contact Us

Earn CPD Points

CPD: Consumer protection essentials – AFCA and advice complaints

CPD: Consumer protection essentials – AFCA and advice complaintsAs essential component of a robust framework for protecting financial consumers is the presence of mechanisms that hold individuals and organisations to account for causing consumer harm and allow consumers [...]

CPD: A new approach to assessing risks in retirement

CPD: A new approach to assessing risks in retirementIn our last article, we examined the common risks that can impact retirement. The financial risks we’re all acutely aware of: longevity risk, inflation risk, market risk and sequencing risk. [...]

CPD: Ethics and financial abuse

CPD: Ethics and financial abuseFinancial abuse is becoming more prevalent in Australian society. This article, proudly sponsored by GSFM, examines financial abuse in the context of an ethical financial advice practice. A lot of [...]

CPD: Seeking stability

CPD: Seeking stabilityAt a time of sweeping geopolitical change and clear challenges for riskier assets, bond markets offer a source of stability. Key takeaways The world has entered a period of geopolitical [...]

CPD: The year ahead for fixed income markets

CPD: The year ahead for fixed income marketsThe forces shaping fixed-income markets found themselves at a confluence of economic, fiscal, and political factors heading into 2025. Inflation dynamics remained in flux, a new Treasury Department was in [...]