AI’s promise is powerful, but real productivity and profit gains will take longer to emerge than markets currently expect.

Ever since ChatGPT’s public release in late-2022, the world has been overwhelmed by headlines about AI’s astonishing progress, with improved models and breathtaking capabilities. Top executives have described AI as the most significant breakthrough in human history, even surpassing the impact of electricity or fire, and as a technology capable of transforming or saving the world. This article from GSFM’s investment partner TD Epoch explores the economics of technology and the implications for AI.

However, consider the economics of previous tech breakthroughs, from railways and electricity through to PCs and the internet. Such innovations always take decades to mature and typically evolve along unpredictable paths. While TD Epoch is bullish on the long-term potential of AI, it believes the latest tech wave will take longer than expected to turbocharge productivity and profits. It always does.

We are richer than our grandparents because of the history of innovations. Much of this reflects automation, which involves shifting production tasks away from slowly improving human labour to rapidly improving machines. This doesn’t occur overnight; it takes decades, with most of the value added coming from entirely new products, services and even sectors. No one is ever smart enough to foresee how a tech wave will unfold.

Roughly 20% of companies were using AI in 2025, but few saw a measurable return

Before diving into the history of productivity and tech waves, this section discusses five surveys that help us understand where we are today, beginning with one by McKinsey[1]. It found that a majority of companies are beginning to use the technology, including agentic AI. However, most are still in the preliminary stages, experimenting and running pilots, with few capturing a significant return on investment. The study emphasises that successfully introducing AI requires redesigning workflows, a process both challenging and time intensive.

A second survey from Massachusetts Institute of Technology (MIT), found that 95% of organisations see no measurable return on their investment in AI pilots[2]. The article stressed that most fail due to misalignment with day-to-day workflows, with the lack of customisation constituting a core barrier to success. The sectors that reaped the greatest benefit were tech, media and finance.

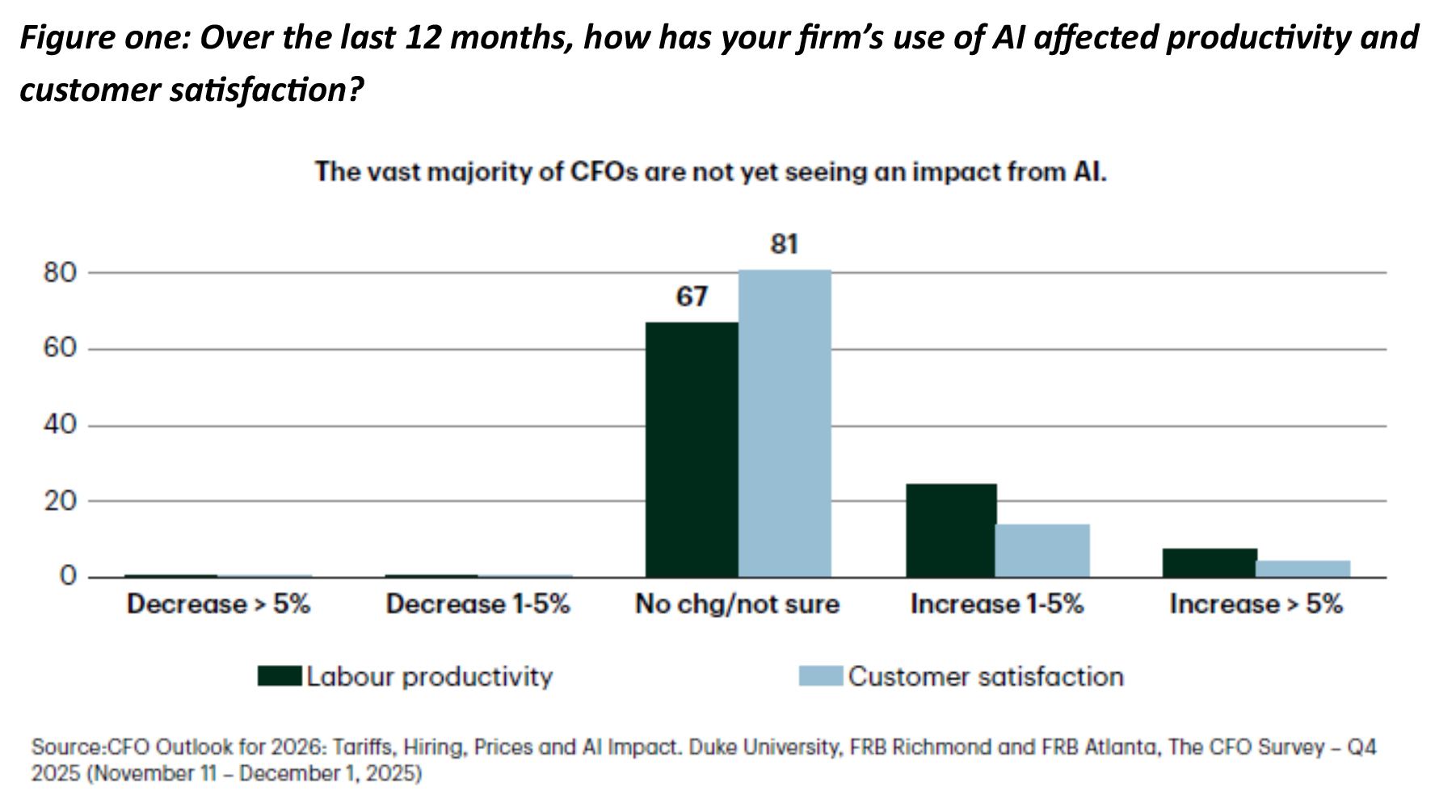

The next survey, of roughly 500 CFOs, is from Duke University, in conjunction with the Fed (figure one)[3]. Similar to the results from McKinsey and MIT, it found AI is having negligible impact at the enterprise level[4].

Fourth, a University of Chicago survey asked a large panel of economists to evaluate the statement, “Adoption of AI will lead to a substantial increase in the growth rate of real per capita income over the next ten years[5].” The most common response was “uncertain,” with participants emphasising:

- there’s considerable uncertainty about both the timeframe and the net impulse to growth, and

- AI is likely to prove more positive for corporate profits than for personal income, exacerbating the K-shaped economy.

Finally, the US Census Bureau surveys 1.2 million firms every two weeks (figure two). Note that the share of enterprises adopting AI is rising, but the pace of increase is much lower than many overly enthusiastic headlines would have you believe.

What does history tell us about the likely impact of AI on productivity?

While much is going on below the surface, AI progress at the enterprise level has so far been modest. Regardless, techno-optimists remain adherents of the ‘explosive growth’ theory, which predicts a golden age is imminent with productivity growth at least doubling from the historical trend.

Epoch pushes back hard on this view and believes the impulse from AI is likely to be in the range of 0.2 to 0.6 percentage points (ppts), with a median forecast of 0.4 ppts[6]. Epoch also emphasises that, while 0.4 ppts of extra growth might sound small, if it is maintained for a decade or more, it represents enormous value creation – probably the biggest global wealth impetus in history.

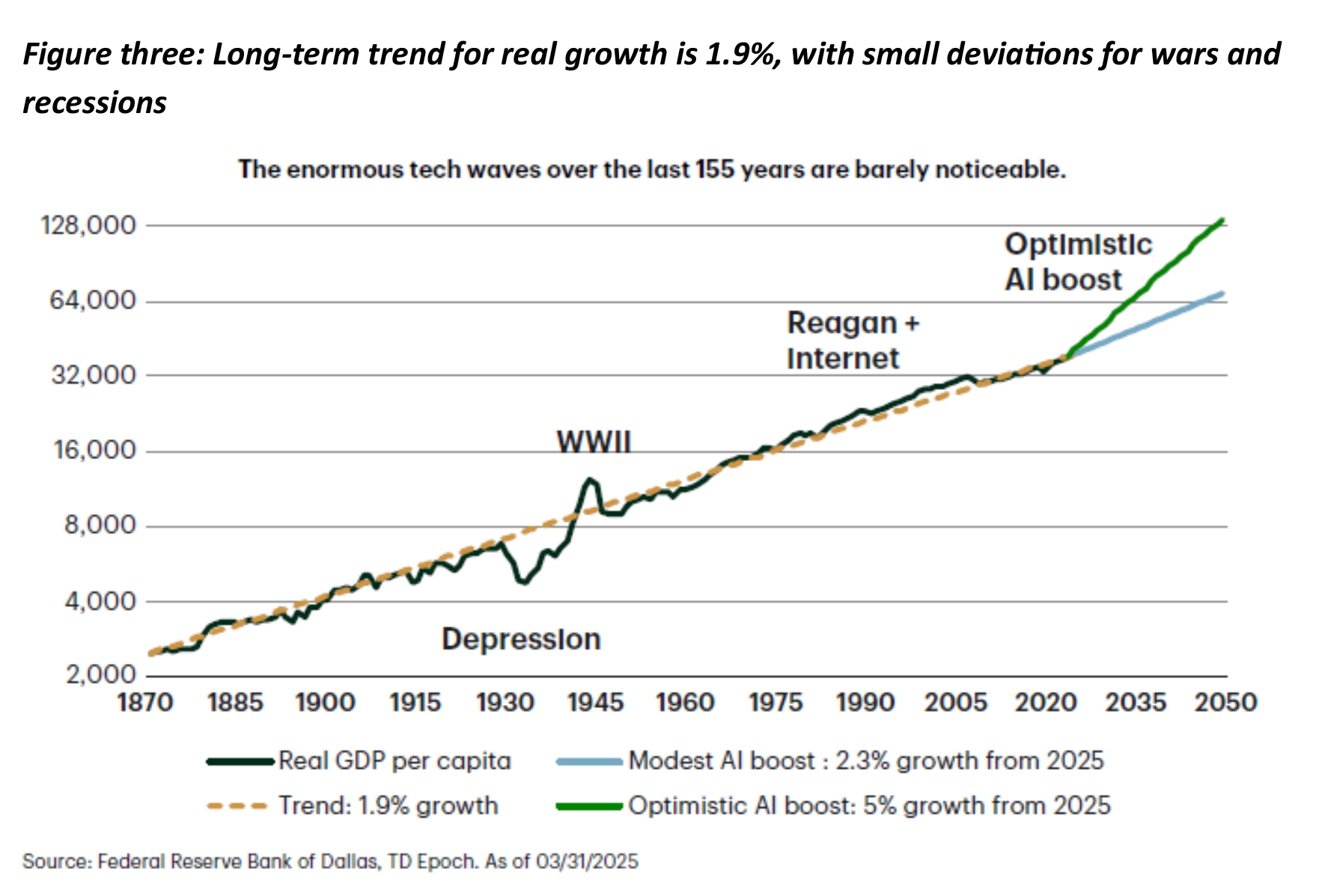

A key reason for this prediction of a 0.4 ppt impulse is the history of productivity growth (figure three). Since 1870 it has averaged 1.9% with the odd episode below (the Great Depression) and the occasional period above (WWII, 1986-2007). Today it is bang on 1.9% and there has never in history been anything similar to what techno-optimists are calling for. To illustrate, an “Optimistic AI boost” scenario added to figure three – a 3.1 ppt impulse, bringing productivity growth up to 5%, beginning from 2025.

The period since 1870 has witnessed more tech waves than ever before in history, yet there is nothing remotely like what AI optimists believe is in the cards. As Sir John Templeton cautioned, the four most dangerous words in investing are “This time is different.” It is conceivable that explosive growth could happen, but it hasn’t before in our species’ 300,000-year history.

Technology investing from railroads to the internet: implications for the AI cycle

We now turn to the history of tech waves, which serves as a vital, though not exact, guide for understanding the AI revolution. Based on an analysis of innovations since 1870, Epoch emphasises five insights[7].

The first concerns commercial uncertainty. Achieving sustainable business and financial success is far more difficult than the initial invention, however brilliant that might have been. History is full of brainiacs, from James Watt to Guglielmo Marconi to Bill Gates. Each of these individuals famously misunderstood the eventual scale and evolution of breakthroughs such as the steam engine, radio, the PC and the internet.

The second is the long struggle for viability and sustainable free cash flow (FCF). Most pioneers, including Thomas Edison, Alexander Graham Bell and Henry Ford, faced decades of financial hardship and scepticism before reaching profitability. The constant need for risk capital incentivises extravagant claims, which historically fuelled exuberance in railways, radio and the 1990s internet. Elon Musk and Sam Altman are just the most recent in a long line of showmen.

Next, the path from impressive demo to widespread adoption is inherently unpredictable and torturously long. For example, it took nearly 50 years from the invention of the light bulb until a majority of US homes were electrified. Most recently, it took the internet well over a decade for real businesses to emerge. This offers a valuable lesson if we make the analogy that ChatGPT (released Nov 2022) is to AI as Netscape Navigator (launched December 1994) was to the Internet[8].

At this point in the internet boom (early 1998), the world’s largest search engine had not yet been incorporated, Mark Zuckerberg and Daniel Elk (founder of world’s leading music streaming platform) were in middle school, and the creators of the top vacation rental platform were in high school. So, 2026 is just exceedingly early in the AI wave.

Fourth, market dominance and “winner-takes-most” dynamics are not new. However, first-mover advantage appears more fragile in the age of digital tech, as seen with displaced firms within browsers, search, music, social media and smartphones. Today’s tech behemoths are likely more vulnerable than consensus recognises.

The final takeaway concerns complementary innovations. The long lag between an impressive tech demo and commercial success is largely due to the necessity of complementary innovations. A single breakthrough is never enough to create a viable, sustainable industry; it requires an ecosystem of secondary inventions. Examples include Bessemer steel for railroads, alternating current for electricity, and pneumatic tyres for automobiles. For modern robotics, it will require advances in multimodal world models, spatial intelligence, high-torque actuators, tactile sensing, solid-state batteries and semantic connectivity. Regardless of Elon Musk’s promises, this will take at least a decade and probably more.

AI is just the latest form of automation: a process that has been ongoing for centuries

Having surveyed the last two centuries of tech innovation, let’s examine the economics of progress, which largely consists of substituting capital for labour. Such automation has occurred relatively steadily since at least 1780, with AI representing the latest fashion.

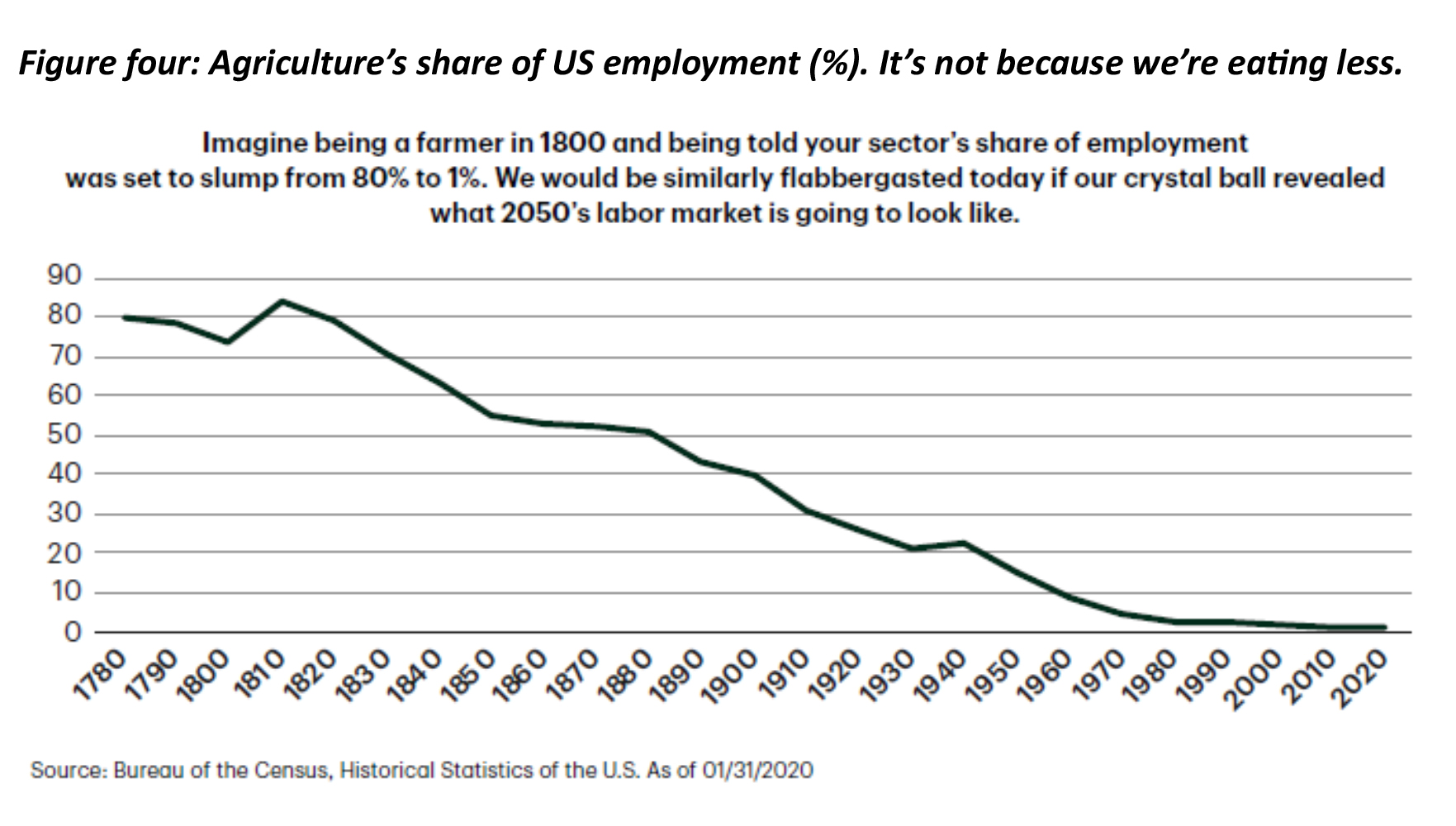

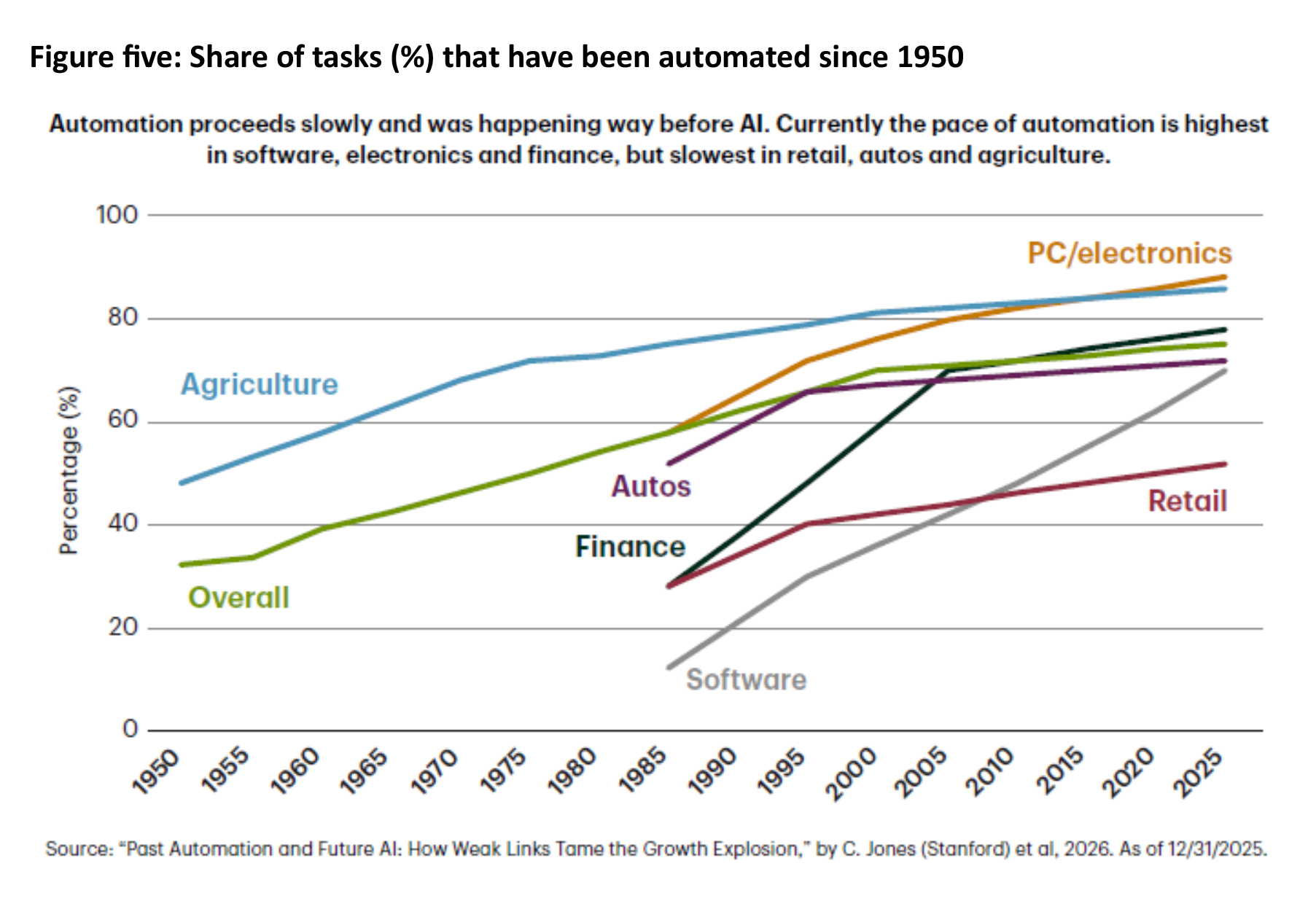

Farmers once threshed grain by hand; now a single combine harvester replaces dozens of workers and agriculture productivity has soared (figure four). Similarly, telephone operators, typists and travel agents were once ubiquitous; today, software handles most of these tasks. In auto plants, welding and painting have moved from human workers to industrial robots. More topically, large language models (LLMs) are increasingly able to write code to replace some of the tasks of software engineers. Further, AI agents are progressively replacing customer service representatives (CSRs) and maybe, one day, even radiologists.

We are richer than our grandparents because of automation: but it’s a slow process

Agriculture illustrates that most wealth creation over the centuries has come from shifting the production of tasks away from slowly improving human labour to rapidly improving machines. Alternatively put, productivity growth has been driven by improvements in the efficiency with which capital performs tasks across a variety of sectors. Since 1950, capital productivity growth has averaged 5% per year, which is roughly ten times the productivity growth rate for labour.

A recent study examined the automation process for six sectors and the aggregate US economy (figure five)[9]. It found that the pace of substitution is slow, which can be attributed to various bottlenecks or weak links. To economists, the pace is measured by the elasticity of substitution, with a value of one implying it is rapid (capital and labour are close substitutes, so a 10% decrease in the cost of capital results in companies reducing the labour input by 10%). Empirically though, the elasticity is around 0.5, meaning substitution is relatively slow. That is, capital and labour are complements, with the labour input reduced by only 5% as substantial labour input is required to realise the productivity gains from the new and improved capital.

Bottlenecks or weak links explain why the diffusion of new technologies takes so much time. This is true even when the study’s model, calibrated on the historical elasticity of substitution, is primed for big AI-induced benefits.

By 2040, output is only 4% higher than the base-case (0.3 ppts per year), and by 2060 the gain is still only 19% (0.6 ppts per year). That is, even when advances in AI mean capital is improving rapidly, and many tasks can be increasingly automated, output gains are still constrained by the gradual pace of substitution away from slowly improving labour.

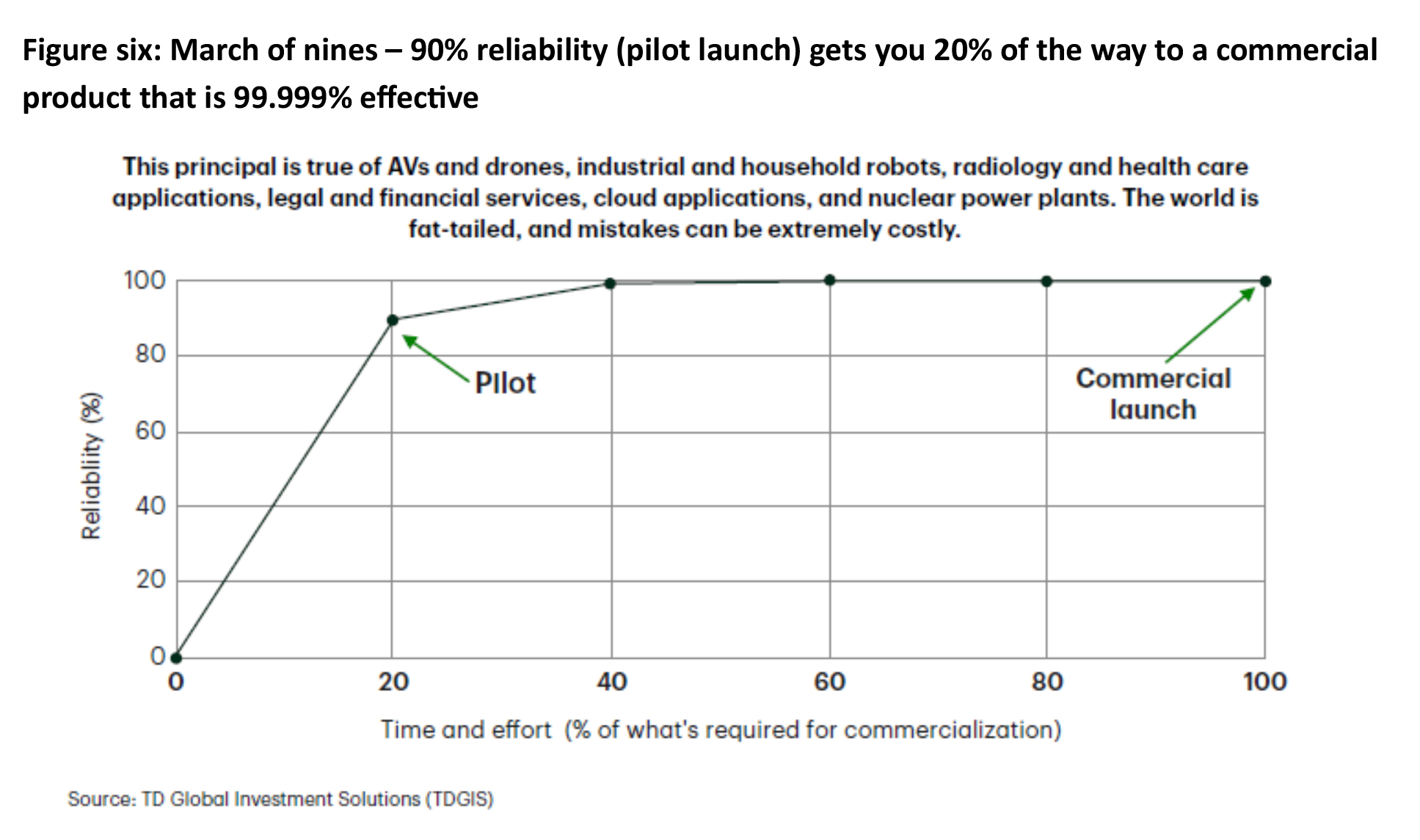

The march of nines: The long road from a cool demo to five-nines reliability[10]

It’s not enough if an AI agent books the right flight or makes the correct hotel reservation 90% of the time. With a 10% error rate, it’s more work to verify and fix. Even though today’s agentic models possess ever more sophisticated tool-calling capabilities, we’re still years away from autonomous systems that can reliably book your next holiday.

Ninety percent reliability might be acceptable where the cost of failure is comparatively low. However, for many purposes, the standard that society sets is much higher, 99.999% (figure six). Autonomous vehicles (AVs) may already be safer than humans, but the long tail of errors represents complex “edge cases” that challenge the best engineers. For AVs, each successive “nine” of reliability requires a constant amount of work, meaning the slog to near perfection takes five times longer than the initial breakthrough.

LLMs are a “dead end”: world modelling

The previous two sections explained why economists and engineers expect relatively slow diffusion of AI. We now turn to three leading AI researchers who, while extremely bullish on the medium- to long-term, agree that current AI architecture is a “dead end” for achieving true AGI.[11]

Fei-Fei Li emphasises that the next frontier of AI requires systems that can see, reason, and act within the 3D physical world. In her view, world modelling is about spatial intelligence. Language is one component, but a world model must also include visual awareness, physical actions, and the natural laws of the world.

One challenge in creating a world model is obtaining data. Training LLMs is relatively easy because language data is all over the internet. Video data is plentiful, and helpful, but the real world is multimodal. It’s spatial, has fundamental 3D information, including geometry, physics, and dynamics. This type of data is not easily obtainable, but is critical to the success of robots, drones and AVs. This suggests a long journey to commercialise physical AI.

Demis Hassabis stresses that LLMs can generate brilliant text, images, and even code, but AI lacks a world model. It just predicts patterns, it doesn’t understand. Real insights require an internal model of how the world works, continuous learning, selective memory, stronger reasoning capabilities and long-term planning.

Yann LeCun is especially outspoken, arguing “the AI industry is completely LLM-pilled,” with everyone in Silicon Valley working on the same thing[12]. A world model must be a representation of how reality actually works. Just as a baby learns by watching a ball fall, AI should learn from sensory inputs like video to understand gravity, causality and object permanence. This is an extremely high bar and raises an almost philosophical issue on the nature of intelligence.

Moravec’s paradox: hard problems are easy, and the easy problems are hard

Hans Moravec wrote in 1988 “It is comparatively easy to make computers exhibit adult level performance on intelligence tests or playing checkers, and difficult or impossible to give them the skills of a one-year-old when it comes to perception and mobility[13].”

What’s easy for humans is hard for computers and vice versa. That is, tasks that humans find difficult – such as playing chess, solving calculus problems, writing code or analysing vast amounts of financial data – are comparatively easy for computers to master. However, robots find it exceedingly difficult to perform easy tasks, such as walking across a cluttered room or picking up a glass of water[14].

Moravec believed the reason lies in evolutionary history. Survival skills like vision, movement and physical coordination have been “optimised” by natural selection over millions of years. The underlying neural machinery is vast, complex and highly efficient, even if we aren’t consciously aware of the effort involved. On the other hand, tasks like chess, calculus, abstract reasoning, coding and protein folding are relatively recent. Being “new” to our brains, they feel difficult, but they actually require much simpler logical structures that are easy to encode into software.

Why does this matter? It seems natural to assume that physical AI such as AVs, drones and robotics will happen quickly, because they only have to master tasks that appear simple to us, things we learn quickly as children. However, Moravec suggests this will take considerably longer than consensus believes. Tech optimists expect artificial general intelligence (AGI) to be achieved by 2030 or so, while most serious AI researchers believe 2040 is more likely. Regardless, there is a wide band around these estimates, illustrating the diversity of opinions, even regarding what AGI means.

Why AI is so slow: radiology, AVs and robotics as examples

In 2016, Geoffrey Hinton warned that all radiologists would be replaced by AI in 5 to 10 years[15]. Not only didn’t that happen, but the number of radiologists in the US has increased by 11% and there is a growing shortage. Why? First, AI isn’t perfect at reading scans (still far from the “Five Nines” of reliability).

Second, that is only one of a radiologist’s tasks. The job’s broader purpose is to diagnose disease and help patients. And on these dimensions, AI is unlikely to replace radiologists for decades[16].

The second example concerns AVs, which represent an overnight success that was 40 years in the making[17]. Tremendous strides have been made since 1985, and it is likely that AVs will represent a majority of miles driven in America by 2040-2050. However, it has been a long road involving numerous breakthroughs and still requires complementary innovations such as spatial intelligence (cameras and light detection and ranging (LiDAR)), solid-state batteries and semantic connectivity (to talk to other cars and traffic signals). Further, road safety nirvana requires better training on edge cases (such as heavy snow, construction sites and power outages), improved reasoning capabilities, and a more transparent and consistent regulatory environment[18].

Robotics may well become the biggest industry ever but is unlikely to develop nearly as rapidly as boosters suggest. The robotics industry has been developing for decades from 1961 when a major American multinational automotive corporation installed the first industrial robot (for die-casting) and 1977 when NASA designed, manufactured and deployed the Sojourner rover on Mars. However, the rollout of industrial robots has been disappointingly slow, with few employed outside of auto plants and warehouses. Further, general-purpose humanoid robots remain in the research stage and are years away from mass adoption. Morgan Stanley forecasts little growth over the next decade but expects 134 million units to be sold in 2040 (valued at $1.2 trillion), soaring to 1,019 million units in 2050 ($4.7 trillion)[19].

The “march of nines” is especially daunting for robotics, which requires a host of complementary innovations including: multimodal world models, high-torque actuators (the “muscles” of the robot, which represent 60% of a humanoid’s material cost), tactile sensing (digital skin), spatial intelligence (cameras, LiDAR), solid-state batteries (higher energy density, better thermal stability) and semantic connectivity (to talk to smart elevators, security systems, and other robots in real-time).

Implications for investors

1. AI capex growth to moderate to a more sustainable trajectory

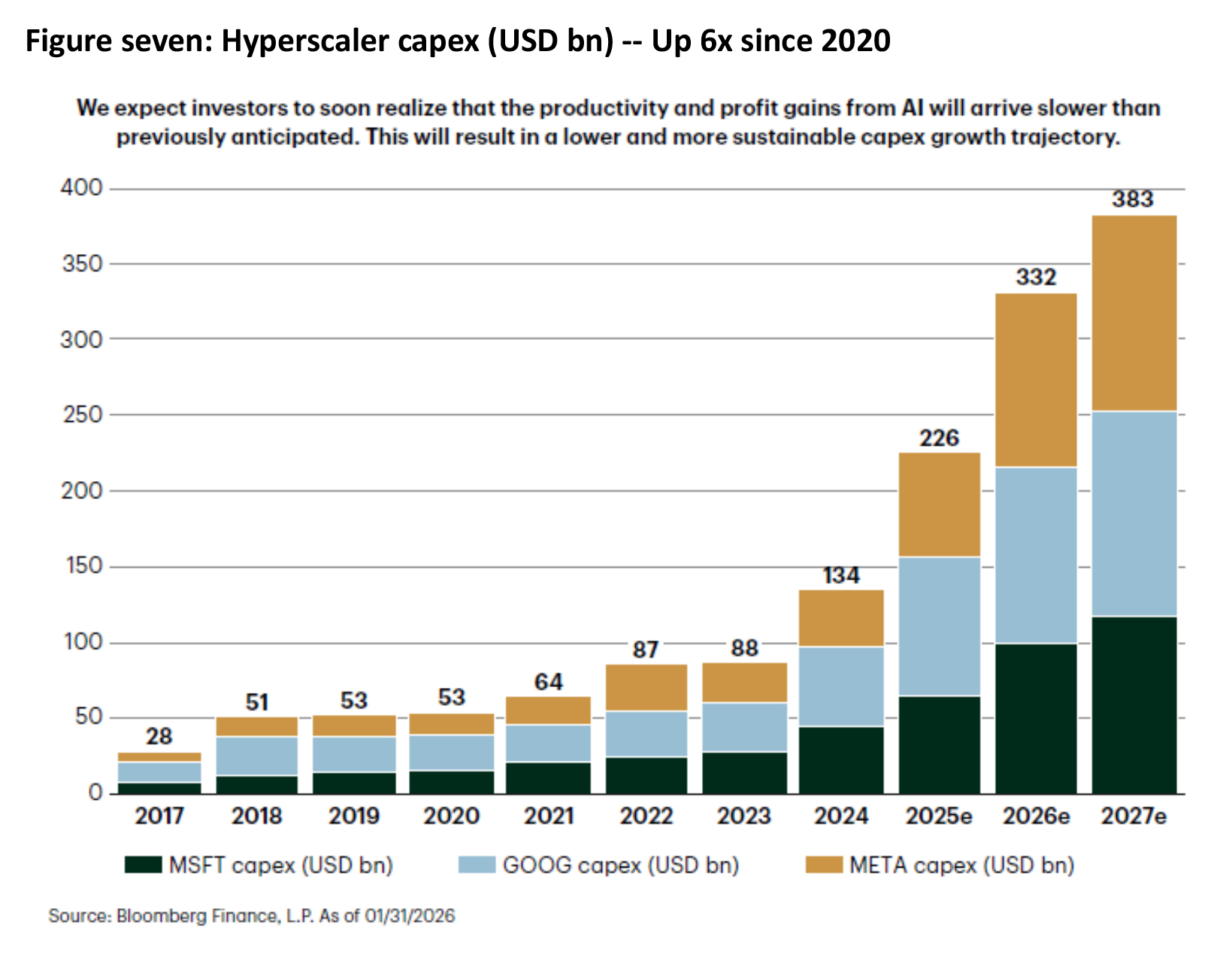

Numerous investors have argued there is a bubble in LLMs, emphasising that some (mostly private) companies are spending tens of billions of dollars, are unlikely to turn FCF positive this decade, but are still able to fundraise at astronomical valuations. This is especially concerning given the limitations of LLMs and the prevalence of open-source labs. It seems reasonable to expect that many of the new startups will lose money and are accidents waiting to happen. That was the pattern with railways, electricity, autos, the internet, and all other episodes of tech disruption.

Regardless, the tech cycle will endure. “AI bubble” is too binary a term, as public equity valuations are only moderately stretched and, at the epicentre of AI capex, are the world’s most profitable companies. This is the critical difference from previous tech cycles, including the 1990s. Still, what happens if – as occurred with railways in the 19th century – investors recognise their returns won’t be realised quite as rapidly as they had forecast? We expect this to happen during the next few quarters and believe capex growth will then moderate from its current torrid pace to a more sustainable path (figure seven)[19].

2. Emphasise quality tech

Quality means companies generating sustainable FCF, with solid margins and a return on invested capital (ROIC) that is greater than its weighted average cost of capital (WACC). This includes the hyperscalers which have real businesses, with large existing user bases. Aside from defensive characteristics, having lots of customers unlocks the flywheel at the centre of every great tech company.

The users make the algorithm better, which improves the product, attracts more customers, and the machine just spins. It’s not quite spinning yet in AI, but you can squint and see it[21]. Additionally, the infrastructure layer is usually a safer place to be at this stage of a tech revolution. There will be tons of opportunities in applications, but it is still too speculative with enormous unknowns.

3. Diversify beyond the US

Epoch remains constructive on US equities, but many investors hold overly concentrated portfolios in US tech. Further, the US valuation premium often doesn’t appear justified by fundamentals, and Epoch believes the USD is over-valued[22]. Epoch’s team especially likes global champions outside the US, including China, which meet their definition of quality.

4. Creative destruction and the innovator’s dilemma: Turbo-charged by AI

Tech revolutions are always associated with massive churn in corporate leadership. To illustrate, of the top twenty-five global tech companies in 2000, only four of them are still members of that list. What will this list look like in 2040? This is difficult to imagine as today’s champions always appear bulletproof and insurmountable. Regardless, history strongly suggests that a majority of firms on today’s leaderboard will fall off within the next decade or two.

While the current AI surge often draws comparisons to the 1990s, this era represents a structural “slow burn” toward hyper-profitability rather than a speculative bubble destined to burst. Unlike the dot-com crash, today’s landscape is defined by the immense profitability and low debt of tech hyperscalers, a supportive liquidity environment, and a genuine supply-demand deficit in physical infrastructure such as data centres. Furthermore, AI has become a non-negotiable element of the global superpower race, cementing its role as a critical pillar of economic, technological and defensive sovereignty. Together, these factors suggest that while the transition will be gradual, the eventual boost to corporate margins will be grounded in tangible utility and geopolitical necessity rather than mere market euphoria.

The information included in this article is provided for informational purposes only and is general advice only. It does not take into account an investor’s own objectives. The information contained in this article reflects, as of the date of publication, the current opinion of TD Epoch and is subject to change without notice. Sources for the material contained in this article are deemed reliable but cannot be guaranteed. We do not represent that this information is accurate and complete, and it should not be relied upon as such. Any opinions expressed in this material reflect our judgment at this date, are subject to change and should not be relied upon as the basis of your investment decisions. All reasonable care has been taken in producing the information set out in this article however subsequent changes in circumstances may occur at any time and may impact on the accuracy of the information. Neither TD Epoch, GSFM Pty Ltd, their related bodies nor associates gives any warranty nor makes any representation nor accepts responsibility for the accuracy or completeness of the information contained in this article.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: General (0.75 hrs)

ASIC Knowledge Requirements: Economic Environment (0.5 hrs) and Generic Knowledge (0.25 hrs)

please log in to start this quiz

———–

References:

[1] The state of AI in 2025: Agents, innovation, and transformation,” by McKinsey & Company, 2025

[2] “The GenAI Divide: State of AI in Business, 2025,” A. Challapally et al, MIT, 2025

[3] “CFO Outlook for 2026: Tariffs, Hiring, Prices, and AI Impact,” Duke University, 2025

[4] “Artificial Intelligence in the Firm,” by F. Chen (Harvard) et al, 2026, obtains a similar result. Analysing a dataset that covers 100,000 engineers at 500 firms they conclude “AI adoption leads to moderate increases in productivity … However, these productivity gains do not pass through to effects on output, task composition, or employment.” That is employee-level improvements do not yet translate into firm-wide gains.

[5] “AI and growth,” University of Chicago, 2025

[6] Among the dozens of projections that have been published, the most credible are from the OECD, ECB, McKinsey & Company, McKinsey Global Institute, Penn Wharton Budget Model and the Peterson Institute, as well as academics such as Daron Acemoglu (MIT), Ricardo Reis (LSE) and Tyler Cowen (GMU)

[7] Sources include: “Engines that move markets: Technology investing from railroads to the internet and beyond,” by A. Nairn, 2018 and “How the internet happened: From Netscape to the iPhone,” by B. McCullough, 2018, as well as “The rise and fall of American growth: The US standard of living since the Civil War,” by R. Gordon, Northwestern, 2016 and “Power and Progress: Our Thousand-Year Struggle Over Technology and Prosperity,” by D. Acemoğlu (MIT) et al, 2023.

[8] See Gavin Baker’s “Nvidia v. Google, Scaling Laws, and the Economics of AI,” from the “Invest like the best” podcast, 2025

[9] “Past Automation and Future AI: How Weak Links Tame the Growth Explosion,” by C. Jones (Stanford) et al, 2026

[10] See the podcast, “Andrej Karpathy — AGI is still a decade away,” 2025. “March of nines” is similar to the systems perspective, applicable to many domains, that “linear progress requires exponential resources.”

[11] “From Words to Worlds: Spatial Intelligence is AI’s Next Frontier” by Fei-Fei Li, Stanford, 2025, as well as “The Future of intelligence” by Demis Hassabis, CEO of Google DeepMind, 2025 and “The information bottleneck” by Yann LeCun, NYU, 2025

[12] “An A.I. Pioneer Warns the Tech ‘Herd’ Is Marching Into a Dead End,’ by C. Metz, NYT, 2026

[13] “Mind Children,” by Hans Moravec, CMU, 1988

[14] “A Gap In AI Adoption? Moravec And The AI Productivity Paradox,” by A. Susarla (Michigan State), 2026, argues that Moravec’s paradox explains why the C-suite, which deals more with analytical issues that AI excels at, is constantly disappointed with AI launches that fail to produce firm-wide results.

[15] Hinton is often hailed as the “Godfather of AI,” won the Nobel prize in Physics (2024) and teaches at U Toronto. See “Radiology resident thumbs nose at Nobel Prize winner who predicted specialty would become obsolete,” Radiology Business, 2024 and “The Growing Nationwide Radiologist Shortage,” by S. Mirak et al, Radiological Society of North America, 2025

[16] For Jensen Huang’s discussion of the “task” vs “purpose” perspective see “NVIDIA’s Jensen Huang on Reasoning Models, Robotics, and Refuting the “AI Bubble” Narrative,” No Priors podcast, 2026

[17] Five milestones on the AV journey: 1985: CMU’s AV, funded by DARPA, achieved the first road-following demonstration using Lidar and computer vision, reaching a speed of 31 km/h. 1995: The “No Hands Across America” tour. CMU’s AV completed the first autonomous US coast-to-coast journey from Pittsburgh to San Diego. The vehicle was driven autonomously for 98.2% of the trip at an average speed of 102.7 km/h. 2005: Sebastian Thrun (widely known as the father of the AV) led the Stanford Racing Team to victory in the DARPA Grand Challenge. It was the first robot car to complete the 132-mile desert course, doing so in under seven hours and winning a $2 million prize. 2018: Waymo launches its robotaxi service in Phoenix, AZ. 2025: Waymo’s robotaxis completed 14 mn trips, driving 150+ mn miles, up 3x from 2024.

[18] “We Don’t Know If AVs Are Safer Than Human Drivers,” by David Zipper (MIT), Bloomberg, 2026

[19] Humanoids: Investment implications of embodied AI,” by Adam Jones et al, Morgan Stanley Research, 2025

[20] Even if AI capex growth in the US moderates it won’t turn negative. This is because AI is the key domain in which the US-China contest for global supremacy is being waged. More specifically, AI is core to all three domains of power – economic strength, tech prowess and defence capabilities.

[21] These themes are explored in “Gavin Baker and David George on Positional Strategy in AI,” a16z, 2025

[22] See “The Dollar is Our Currency, but It’s Your Problem: Rebalancing Requires a Much Weaker USD,” 2025

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.75 hour.

Legislated CPD Area: General (0.75 hrs)

ASIC Knowledge Requirements: Economic Environment (0.5 hrs) and Generic Knowledge (0.25 hrs)

please log in to start this quiz———–

References:

[1] The state of AI in 2025: Agents, innovation, and transformation,” by McKinsey & Company, 2025

[2] “The GenAI Divide: State of AI in Business, 2025,” A. Challapally et al, MIT, 2025

[3] “CFO Outlook for 2026: Tariffs, Hiring, Prices, and AI Impact,” Duke University, 2025

[4] “Artificial Intelligence in the Firm,” by F. Chen (Harvard) et al, 2026, obtains a similar result. Analysing a dataset that covers 100,000 engineers at 500 firms they conclude “AI adoption leads to moderate increases in productivity … However, these productivity gains do not pass through to effects on output, task composition, or employment.” That is employee-level improvements do not yet translate into firm-wide gains.

[5] “AI and growth,” University of Chicago, 2025

[6] Among the dozens of projections that have been published, the most credible are from the OECD, ECB, McKinsey & Company, McKinsey Global Institute, Penn Wharton Budget Model and the Peterson Institute, as well as academics such as Daron Acemoglu (MIT), Ricardo Reis (LSE) and Tyler Cowen (GMU)

[7] Sources include: “Engines that move markets: Technology investing from railroads to the internet and beyond,” by A. Nairn, 2018 and “How the internet happened: From Netscape to the iPhone,” by B. McCullough, 2018, as well as “The rise and fall of American growth: The US standard of living since the Civil War,” by R. Gordon, Northwestern, 2016 and “Power and Progress: Our Thousand-Year Struggle Over Technology and Prosperity,” by D. Acemoğlu (MIT) et al, 2023.

[8] See Gavin Baker’s “Nvidia v. Google, Scaling Laws, and the Economics of AI,” from the “Invest like the best” podcast, 2025

[9] “Past Automation and Future AI: How Weak Links Tame the Growth Explosion,” by C. Jones (Stanford) et al, 2026

[10] See the podcast, “Andrej Karpathy — AGI is still a decade away,” 2025. “March of nines” is similar to the systems perspective, applicable to many domains, that “linear progress requires exponential resources.”

[11] “From Words to Worlds: Spatial Intelligence is AI’s Next Frontier” by Fei-Fei Li, Stanford, 2025, as well as “The Future of intelligence” by Demis Hassabis, CEO of Google DeepMind, 2025 and “The information bottleneck” by Yann LeCun, NYU, 2025

[12] “An A.I. Pioneer Warns the Tech ‘Herd’ Is Marching Into a Dead End,’ by C. Metz, NYT, 2026

[13] “Mind Children,” by Hans Moravec, CMU, 1988

[14] “A Gap In AI Adoption? Moravec And The AI Productivity Paradox,” by A. Susarla (Michigan State), 2026, argues that Moravec’s paradox explains why the C-suite, which deals more with analytical issues that AI excels at, is constantly disappointed with AI launches that fail to produce firm-wide results.

[15] Hinton is often hailed as the “Godfather of AI,” won the Nobel prize in Physics (2024) and teaches at U Toronto. See “Radiology resident thumbs nose at Nobel Prize winner who predicted specialty would become obsolete,” Radiology Business, 2024 and “The Growing Nationwide Radiologist Shortage,” by S. Mirak et al, Radiological Society of North America, 2025

[16] For Jensen Huang’s discussion of the “task” vs “purpose” perspective see “NVIDIA’s Jensen Huang on Reasoning Models, Robotics, and Refuting the “AI Bubble” Narrative,” No Priors podcast, 2026

[17] Five milestones on the AV journey: 1985: CMU’s AV, funded by DARPA, achieved the first road-following demonstration using Lidar and computer vision, reaching a speed of 31 km/h. 1995: The “No Hands Across America” tour. CMU’s AV completed the first autonomous US coast-to-coast journey from Pittsburgh to San Diego. The vehicle was driven autonomously for 98.2% of the trip at an average speed of 102.7 km/h. 2005: Sebastian Thrun (widely known as the father of the AV) led the Stanford Racing Team to victory in the DARPA Grand Challenge. It was the first robot car to complete the 132-mile desert course, doing so in under seven hours and winning a $2 million prize. 2018: Waymo launches its robotaxi service in Phoenix, AZ. 2025: Waymo’s robotaxis completed 14 mn trips, driving 150+ mn miles, up 3x from 2024.

[18] “We Don’t Know If AVs Are Safer Than Human Drivers,” by David Zipper (MIT), Bloomberg, 2026

[19] Humanoids: Investment implications of embodied AI,” by Adam Jones et al, Morgan Stanley Research, 2025

[20] Even if AI capex growth in the US moderates it won’t turn negative. This is because AI is the key domain in which the US-China contest for global supremacy is being waged. More specifically, AI is core to all three domains of power – economic strength, tech prowess and defence capabilities.

[21] These themes are explored in “Gavin Baker and David George on Positional Strategy in AI,” a16z, 2025

[22] See “The Dollar is Our Currency, but It’s Your Problem: Rebalancing Requires a Much Weaker USD,” 2025

Have feedback on this article? Contact Us

Earn CPD Points

CPD: The spectrum of growth

CPD: The spectrum of growthCompanies that generate strong, sustainable growth are valuable sources of long term capital appreciation in a portfolio, but these businesses are rare, difficult to identify and exist on a broad [...]

CPD: Record-keeping in financial advice – the key to compliance and consumer protection

CPD: Record-keeping in financial advice – the key to compliance and consumer protectionIntroduction The financial services regulatory framework is a key pillar of financial consumer protection. Regulatory compliance is therefore not merely about avoiding penalties, but is a critical step in building [...]

CPD: Trust and ethics in financial advice

CPD: Trust and ethics in financial adviceIn 2024, trust in financial advisers reached an all-time high. This article, proudly sponsored by GSFM, explores the inseparable links between trust and ethical practice when providing financial advice. Defined [...]

CPD: Retirement Income Strategies

CPD: Retirement Income StrategiesIt has been almost 40 years since award superannuation was introduced in Australia, and 33 years since the introduction of mandatory occupational superannuation. This means the next decade will see [...]

CPD: Free cash flow works

CPD: Free cash flow worksThe difference between earnings and free cash flow is an important investment concept, one explained here by GSFM’s investment partner TD Epoch. Earnings have long played a dominant role in [...]