Asian equities can play a role in investor portfolios and this is becoming increasingly important in the current environment.

The investment playbook has long been anchored by the security of the Australian sharemarket, notably the ASX200. Investors have leaned on the ‘big four’ banks for yield and the mining giants for growth, supplemented by a tilt toward US mega-cap technology. However, with the ASX200 trading at record highs and forward P/E ratios stretched well above historical norms, the risks that a home bias can have on portfolios are acute.

Domestic inflation remains stickier than anticipated. This has forced the RBA into a hawkish stance that challenges some domestic equity valuations. However, our northern neighbours have entered a structural renaissance. While Asia has long been considered a ‘satellite’ allocation for somewhat speculative growth, in 2026 it has become an engine for growth, diversification and income.

These domestic issues take place while geopolitical events continue to reshape global capital markets. The extreme concentration in US assets, driven by fiscal policies that have now propelled US national debt close to a US$39 trillion[1] milestone, is showing clear signs of peaking. At the same time, the US dollar is navigating a period of structural softening; its long-standing safe haven premium is being eroded by the gravity of the country’s debt burden and a global trend toward currency diversification.

As well as these broad global thematics, there are other, more granular reasons to consider Asian equities for your clients. Each of these will be explored in further detail in this article.

- The ASX duopoly – the concentration of the Australian market means that many client portfolios are over-exposed to Financials and Materials. Asia offers diversity via direct exposure to a range of growth sectors, many of which are not accessible through the domestic market. This includes semiconductors, industrials and AI.

- The income evolution – traditionally, Australian investors looked to Asia for capital growth and stayed home for dividends. However, a growing number of Asian companies are delivering record share buybacks and yields that rival our domestic income staples (such as banks), but with far superior growth runways.

- A structural portfolio shift – large industry funds and other institutional investors are pivoting their private and public equity mandates toward Asia. AustralianSuper CEO Paul Schroder recently noted the fund is ‘just at the beginning’ of its Asian private equity expansion (Asia Asset Management, February 2026), while Aware Super’s $6bn digital infrastructure push has increasingly focused on Asian markets (i3 Insights, March 2026). This institutional appetite signals a shift from treating Asia as a volatile satellite to a core portfolio engine.

The case for Asia

For Australian investors, the case for Asia in 2026 has become stronger, driven by a fundamental shift in how global capital is allocated. As domestic valuations on the ASX face headwinds from a mature credit cycle and geopolitical factors, the Asian region offers a multi-speed growth profile that provides both a valuation cushion and exposure to sectors unavailable on the local exchange.

1. Diversifying beyond the banks and miners

For many Australian investors, diversification can be challenging to achieve in the domestic sharemarket. The S&P/ASX200 remains one of the most concentrated developed indices in the world, with 54.4 percent of the index weight tethered to just two sectors: Financials (29.5 percent) and Materials (24.9 percent)[2]. While this has historically provided a reliable stream of franked dividends, it can leave portfolios exposed to a ‘two-engine’ economy.

The Australian market is somewhat sparse when it comes to the sectors defining investment trends and economic power in the late 2020s. Asia, however, provides the structural bridge to these missing industries, such as:

Semiconductors – while the ASX has virtually no semiconductor footprint, Asia houses the entire global supply chain. Investing in the region provides direct exposure to several companies that are the gatekeepers of global computing power, from high-end logic chips to the high-bandwidth memory (HBM) required for generative AI.

The new industrial revolution – Australia’s industrial sector is largely comprised of transport and logistics firms. In contrast, Asia offers exposure to advanced robotics, precision manufacturing and automation. As China’s 15th Five-Year Plan prioritises new productive forces, the region is seeing a surge in industrial tech firms that are automating the world’s factories. This is a sector that does not exist at scale in the domestic market.

Artificial intelligence – Asia represents the Applied AI frontier, the practical integration of artificial intelligence into tangible hardware and industrial processes to solve real-world problems. Such businesses are focused on the commercialisation of the technology and converting AI capability into immediate, scalable revenue.

A strong rationale for the Australian investor is the shift from raw materials to refined technology. Many investors’ portfolios are dependent on the price of raw lithium or nickel; an allocation to Asia also provides exposure to those companies that turn those minerals into EV batteries, energy storage systems and so much more.

2. The income evolution

The traditional home bias of Australian investors has long been justified by a single, powerful incentive: franked dividends. This has been particularly important for retirees. Historically, Asia has been considered the investment destination for capital growth, while the domestic market remained the engine for yield.

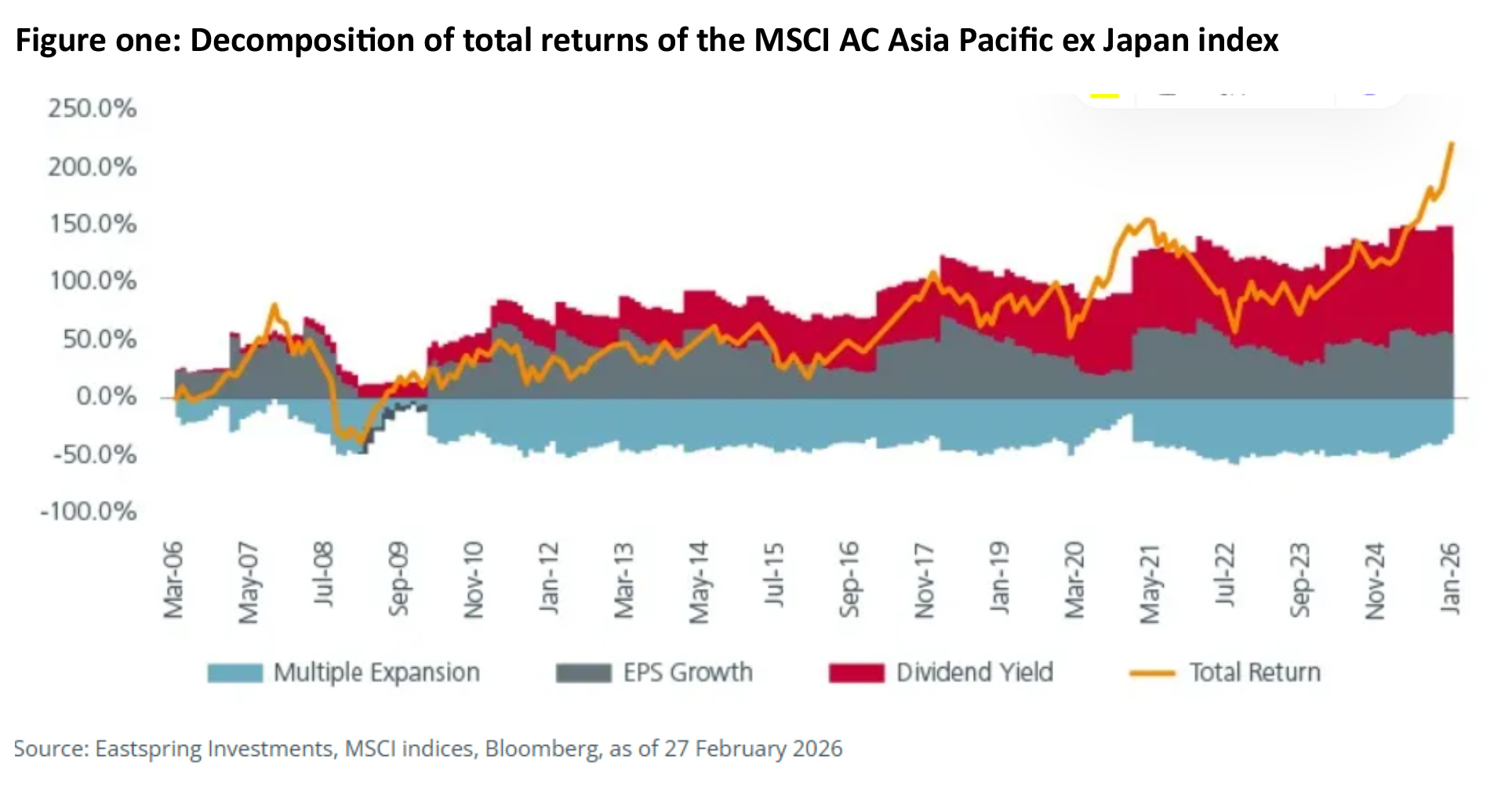

However, GSFM’s investment partner Eastspring Investments believes dividend yield has increasingly become a foundational pillar of long‑term wealth creation in Asia. A decomposition of returns for the MSCI Asia Pacific ex‑Japan Index from March 2006 to February 2026 reveals three distinct drivers: earnings growth, valuation changes through multiple expansion or contraction and dividends (figure one).

While valuation multiples can be highly volatile, swinging sharply between expansion and contraction and acting as both a tailwind and a headwind at different points in the cycle, earnings growth has been comparatively more consistent but remains subject to cyclical variation. Meanwhile the dividend component has delivered the most reliable and steadily compounding contribution to total returns over time.

Income from Asian equities is also being driven by a wave of corporate governance reforms that are forcing companies to prioritise shareholder returns over cash hoarding.

While the headline yields of Australian banks often hover between 5-6 percent, they frequently consume 75-90 percent of corporate earnings to maintain those payments. In contrast, several key Asian segments are now delivering similar total returns with payout ratios closer to 30-40 percent.

This shift is most visible in markets such as South Korea and Taiwan, where programs have incentivised boards to aggressively deploy capital back to investors. In 2025 and 2026, share buyback activity in these regions reached record highs, effectively creating a ‘synthetic yield’ that complements traditional dividends. Unlike the Australian banking sector, which is currently operating in a mature, low-growth credit environment, these high yield Asian companies are anchored in high-growth industries such as advanced semiconductors and regional logistics.

Case study: South Korea’s ‘Value-up’ Program[3]

South Korea’s corporate Value-up Program, which reached full maturity in early 2026, has seen major conglomerates move toward a 30/30/30 model: 30 percent payout, 30 percent buybacks and 30% reinvestment.

From a yield comparison perspective, top-tier Korean financials such as KB Financial Group are currently yielding approximately 5.2 percent. This is being achieved with a payout ratio of roughly 35 percent.

3. A structural portfolio shift

The shift toward Asia by Australia’s major industry super funds is significant. Historically, Australian industry funds treated Asian markets as high-beta satellites, allocations designed to provide a small growth kicker at the expense of significant volatility.

However, the sheer scale of the Australian retirement pool, now exceeding $4.5 trillion[4], has made the ASX a somewhat crowded trade. For Australia’s large institutional investors, Asia has become a necessary frontier for absorbing large-scale capital in sectors that offer structural longevity.

The announcement in late 2025 of a ‘strategic pivot’ into Southeast Asia was aimed at mobilising superannuation capital into the region’s high-growth sectors. The pivot was being formalised through a partnership between the Australian government and IFM Investors, specifically to target long-term opportunities in manufacturing, the energy transition and infrastructure[5].

When institutional investors move, they create the liquidity and corporate engagement that eventually lowers the risk profile for individual retail investors. This institutionalisation provides three key benefits for client portfolios:

- The presence of large institutional funds in these markets signals that the regulatory and governance frameworks have reached institutional grade.

- Through professional managers, clients can now tap into both private and public markets in Asia, some of which were previously inaccessible.

- As the benchmark for a ‘balanced’ super fund shifts toward a higher Asian weighting, it may become easier to present a positive investment case to your clients.

The China story remains intact

GSFM’s investment partner Man Group believes the Gulf conflict indicates that the world’s second-largest economy’s push for self-reliance appears to be paying off. China’s first quarter gross domestic product growth recently came in at 5 percent, beating expectations and accelerating from 4.5 percent in the final quarter of last year. This was mostly driven by better-than-expected exports and a rebound in infrastructure spending.

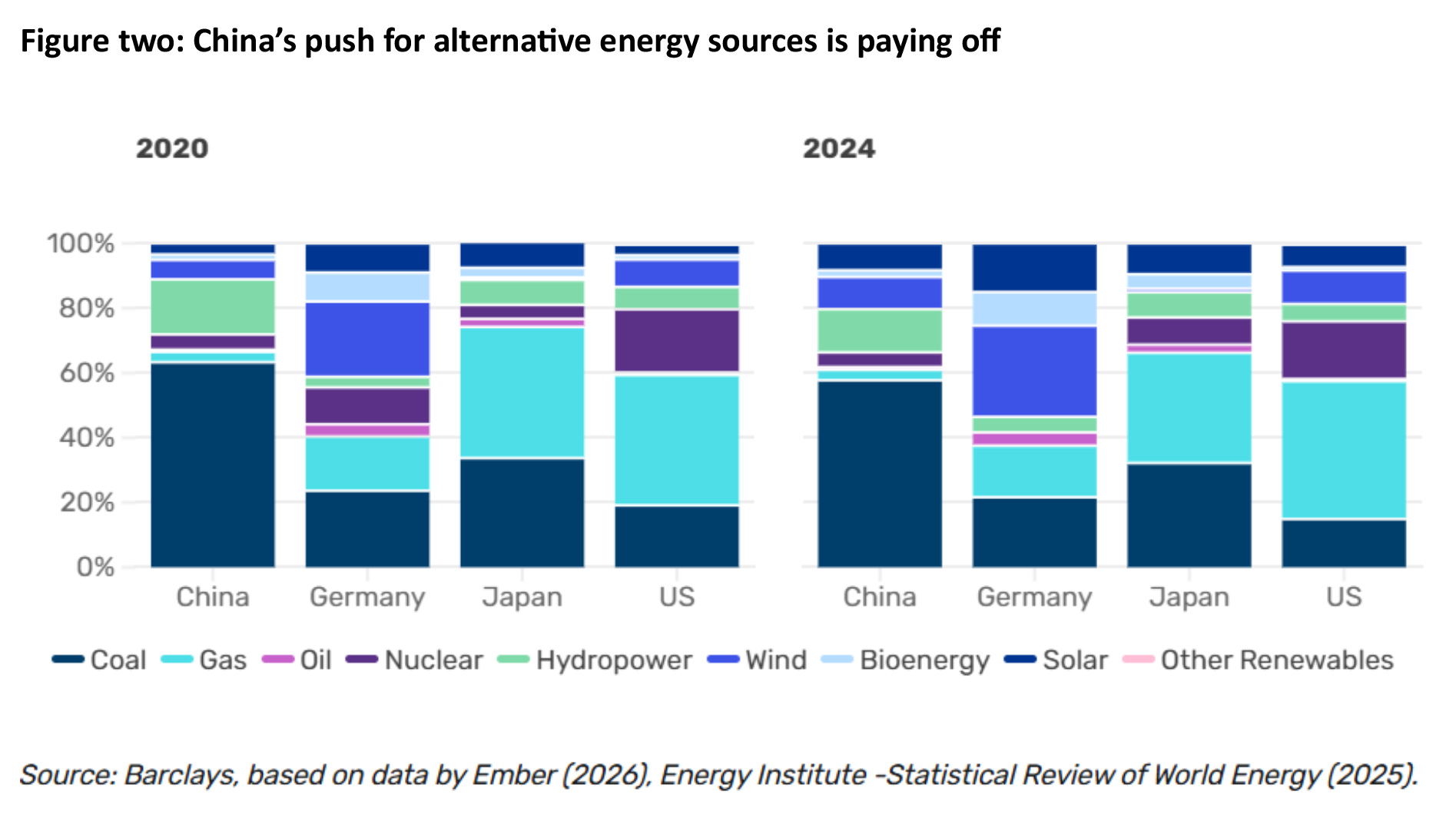

China is probably the least impacted economy in Asia from the Gulf conflict. Its reliance on oil as a share of the energy mix is considerably lower than most countries (figure two), largely because of years of investment in renewables, making its oil stockpiles go a lot further.

The structural build out continues

Meanwhile, the structural build-out continues to gather pace. China is no longer simply catching up with the US in AI. In areas like AI inference – the process of using a trained machine learning model to make predictions, decisions, or generate outputs from new, unseen data – it is beginning to overtake.

What makes this particularly significant is the phase that AI is now entering. As the technology moves from software into the physical world through robotics and humanoids, China’s manufacturing dominance becomes a decisive advantage. This is where decades of industrial capacity meet cutting-edge innovation, and it is difficult to see how competitors can close that gap quickly.

The innovation story is also broadening into biotech. The government recently signalled its willingness to reform China’s drug pricing system, recognising that ‘high level innovative drugs with a high degree of innovation and significant clinical value’ should command prices consistent with their higher investment and risk. In Man Group’s view, this likely drives further upside to an already much improved biotech sector in China.

Easing headwinds

Several persistent drags on sentiment with respect to China are also stabilising. In the property market there has been slowing deterioration, as well as some early signs of stabilisation and improvement in both sales volumes and pricing.

On deflation, higher oil prices have driven the Producer Price Index back into positive territory for the first time since September 2022, ending a 41-month streak of deflation. Consumer prices rose one percent year-on-year in March but remain well below the government’s two percent target, and core inflation (excluding food and energy) was 1.1 percent

The export question

The open question is whether China can maintain its export momentum as global growth likely slows under the weight of a more prolonged increase in energy costs. China may stand to benefit as competitors feel the drag from the energy shock and a global desire to reduce reliance on hydrocarbons sourced from the Middle East drives demand for renewables. China manufactures 92 percent of the world’s solar modules and 82 percent of wind turbines.

If global exports do eventually slow, that may become the catalyst for an internal consumption pivot. Man Group believes China has delayed consumer-related policy reform partly because the strength of its broader export volumes has offered a credible backstop to sustained GDP growth, and partly because the focus has shifted to ensuring self-sufficiency against a backdrop of increasing geopolitical fragmentation. A prolonged decline in external demand could be what finally forces China’s hand.

Asian shares are shifting from a high-risk growth satellite allocation to a core part of a well-balanced portfolio. For Australian investors, this is one of the biggest opportunities in years. By moving beyond the local focus on banks and mining stocks, and investing in areas such as AI, semiconductors and other advanced industries, you can reduce the home bias from clients’ portfolios and improve long-term outcomes. Asia is no longer just an option; it’s becoming a key foundation for building a strong, future-ready portfolio.

Take the FAAA accredited quiz to earn 0.25 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.25 hour.

Legislated CPD Area: Technical Competence (0.25 hrs)

ASIC Knowledge Requirements: Securities (0.25 hrs)

please log in to start this quiz

———–

Notes:

[1] https://www.us-debt-clock.com/, accessed 27 April 2026, debt figure $38.8 trillion

[2] Spglobal.com, S&P/ASX200 Fact Sheet, 31 March 2026

[3] Korea Exchange (KRX) Market Data, 2025 Annual Shareholder Return Report, January 2026

[4] ASFA Super Statistics, 30 September 2025

[5] Super funds to drive south-east Asia investment growth, Super Review, 28 October 2025

The information included in this article is provided for informational purposes only and is general advice only. It does not take into account an investor’s own objectives. The information contained in this article reflects, as of the date of publication, the current opinion of GSFM, Eastspring Investments and Man Group, and is subject to change without notice. Sources for the material contained in this article are deemed reliable but cannot be guaranteed. We do not represent that this information is accurate and complete, and it should not be relied upon as such. Any opinions expressed in this material reflect our judgment at this date, are subject to change and should not be relied upon as the basis of your investment decisions. All reasonable care has been taken in producing the information set out in this article however subsequent changes in circumstances may occur at any time and may impact on the accuracy of the information. None of Eastspring Investments, Man Group or GSFM Pty Ltd, their related bodies nor associates give any warranty nor makes any representation nor accepts responsibility for the accuracy or completeness of the information contained in this article.

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.25 hour.

Legislated CPD Area: Technical Competence (0.25 hrs)

ASIC Knowledge Requirements: Securities (0.25 hrs)

please log in to start this quiz———–

Notes:

[1] https://www.us-debt-clock.com/, accessed 27 April 2026, debt figure $38.8 trillion

[2] Spglobal.com, S&P/ASX200 Fact Sheet, 31 March 2026

[3] Korea Exchange (KRX) Market Data, 2025 Annual Shareholder Return Report, January 2026

[4] ASFA Super Statistics, 30 September 2025

[5] Super funds to drive south-east Asia investment growth, Super Review, 28 October 2025

The information included in this article is provided for informational purposes only and is general advice only. It does not take into account an investor’s own objectives. The information contained in this article reflects, as of the date of publication, the current opinion of GSFM, Eastspring Investments and Man Group, and is subject to change without notice. Sources for the material contained in this article are deemed reliable but cannot be guaranteed. We do not represent that this information is accurate and complete, and it should not be relied upon as such. Any opinions expressed in this material reflect our judgment at this date, are subject to change and should not be relied upon as the basis of your investment decisions. All reasonable care has been taken in producing the information set out in this article however subsequent changes in circumstances may occur at any time and may impact on the accuracy of the information. None of Eastspring Investments, Man Group or GSFM Pty Ltd, their related bodies nor associates give any warranty nor makes any representation nor accepts responsibility for the accuracy or completeness of the information contained in this article.

Have feedback on this article? Contact Us

Earn CPD Points

CPD: The spectrum of growth

CPD: The spectrum of growthCompanies that generate strong, sustainable growth are valuable sources of long term capital appreciation in a portfolio, but these businesses are rare, difficult to identify and exist on a broad [...]

CPD: Record-keeping in financial advice – the key to compliance and consumer protection

CPD: Record-keeping in financial advice – the key to compliance and consumer protectionIntroduction The financial services regulatory framework is a key pillar of financial consumer protection. Regulatory compliance is therefore not merely about avoiding penalties, but is a critical step in building [...]

CPD: Trust and ethics in financial advice

CPD: Trust and ethics in financial adviceIn 2024, trust in financial advisers reached an all-time high. This article, proudly sponsored by GSFM, explores the inseparable links between trust and ethical practice when providing financial advice. Defined [...]

CPD: Retirement Income Strategies

CPD: Retirement Income StrategiesIt has been almost 40 years since award superannuation was introduced in Australia, and 33 years since the introduction of mandatory occupational superannuation. This means the next decade will see [...]

CPD: Free cash flow works

CPD: Free cash flow worksThe difference between earnings and free cash flow is an important investment concept, one explained here by GSFM’s investment partner TD Epoch. Earnings have long played a dominant role in [...]