Decarbonisation is reshaping the global economy, creating long-term investment opportunities across clean energy, energy efficiency, circular economy infrastructure and climate-driven innovation.

Few themes rival the scale, urgency and long-term significance of climate change. Consequently, regions, countries, companies and individuals are taking positive action to decarbonise the planet and work toward net zero 2050 goals. For growth equity investors, decarbonisation is not simply a regulatory obligation or a moral imperative. It is the single largest, earnings-driven wealth-creation opportunity of our generation.

Decarbonisation has crossed the threshold from future ambition to today’s dominant economic reality, propelled by an unprecedented alignment of policy, corporate capital and investor mandate. With over 90 percent of global GDP now bound to net-zero targets, the regulatory floor has permanently shifted.

Corporate giants like Microsoft, Walmart and Samsung are no longer just making promises, they are deploying hundreds of billions of dollars to re-engineer supply chains, lock down clean energy grids and build climate-resilient operations. For investors, this isn’t a passive ESG checkbox; it is a directive to deploy capital into the businesses driving this structural transformation.

Yet, transitioning the global economy is a monumental task. Hitting terminal climate targets requires an enormous, sustained capital expenditure cycle across every major sector. While early market attention focused heavily on renewable energy and electric vehicles, the next phase of growth is far more diverse. The most compelling, earnings-driven opportunities now span critical, high-barrier sectors including advanced nuclear energy, energy efficiency and circular economy infrastructure.

Climate and the S-curve

Climate is not a cyclical trend; it is a permanent structural rewrite of the global economy that will span decades. Achieving net-zero emissions by mid-century will require estimated capital in excess of US$50 trillion. For growth investors, the critical question is no longer whether this capital allocation will happen, but rather, which companies will capture the lion’s share.

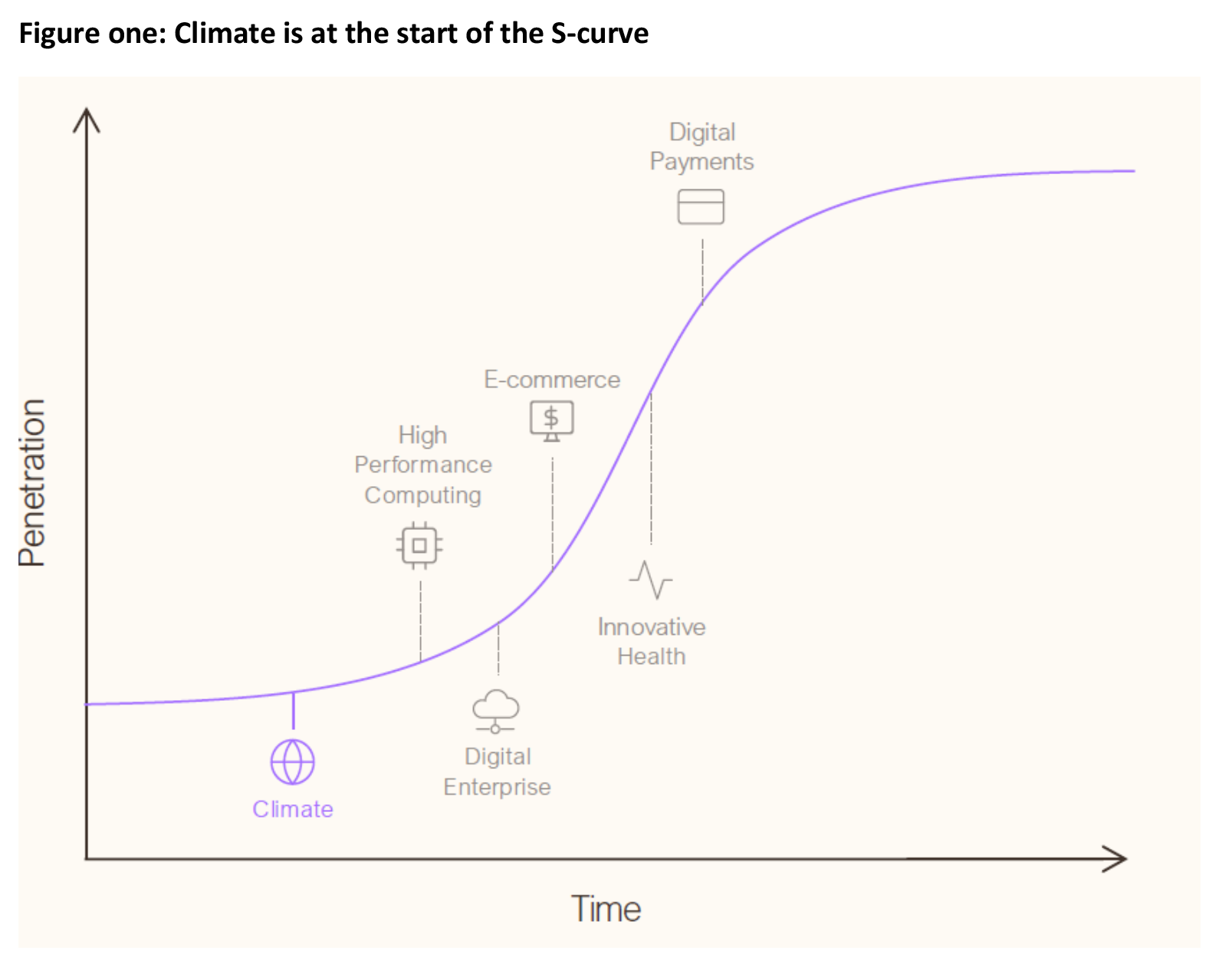

To reinforce the opportunity available to investors, one only needs to look at climate’s S-curve.

The S-curve models how an investment theme, such as climate, moves from niche concept to dominant market standard. Rather than a straight line, the S-curve breaks down into three distinct structural components, each representing a critical phase in that thematic’s lifecycle.

- Incubation phase – at the bottom of the curve, pioneering technologies often face high initial capital costs, regulatory bottlenecks and steep engineering hurdles.

- Inflection and acceleration – once a technology hits commercial viability it crosses a critical threshold. Costs drop, demand surges and growth enters a hyper-accelerated phase. The most resilient compounders in a global growth portfolio capitalise on this multi-year runway, scaling their total addressable market and generating durable earnings growth.

- Saturation – eventually, the curve flattens. The market matures, competition intensifies and incremental gains become harder to secure.

As illustrated in figure one, climate and related decarbonisation technologies are right at the start of the S-Curve. This means a long runway of growth, significant earnings growth potential and ultimately, positive contribution to investor portfolios.

Driving forces of the climate transition

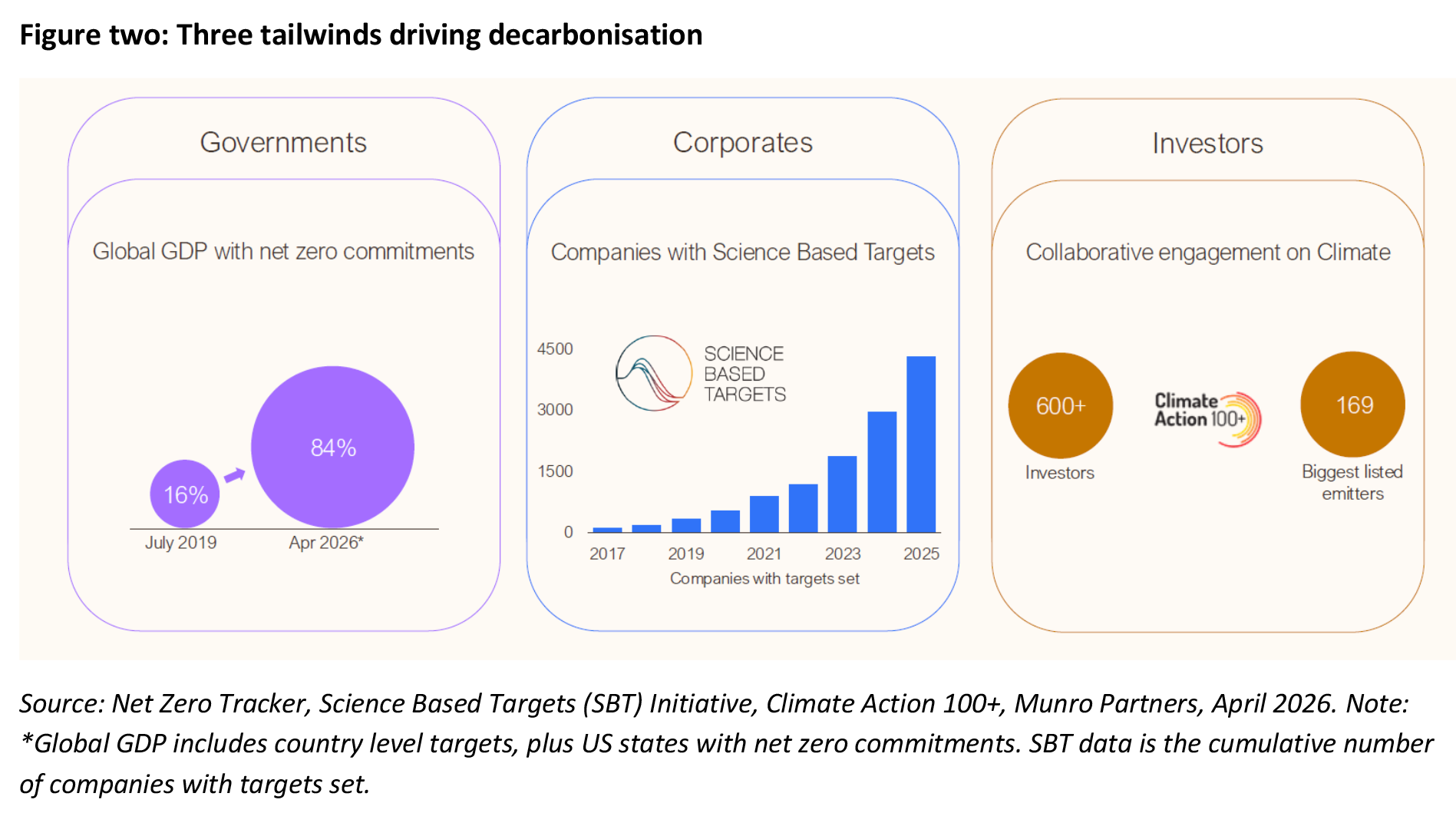

This massive macroeconomic shift is sustained by an interlocking trio of structural drivers (figure two):

- Geopolitical policy and mandates – subsidies, tax incentives and regulatory penalties are setting a permanent economic floor for green tech adoption.

- Corporate capex reallocation – market leaders are proactively deploying hundreds of billions to future-proof their supply chains and operational resilience.

- Investor capital mandates – institutional asset allocation is permanently shifting, starving carbon-heavy legacy businesses of capital while rewarding green compounders.

Crucially, these three forces do not operate in isolation. They form a self-reinforcing feedback loop that creates a multi-decade compounding tailwind for the high-growth companies anchoring the transition. Let’s examine each of these tailwinds in greater detail.

Geopolitical policy – the foundation for action

Over the past decade, climate policies have evolved from aspirational targets to enforceable regulations, reshaping entire industries. The Paris Agreement set the global benchmark for emissions reduction, while COP28 reinforced the ambition with commitments to triple renewable energy capacity by 2030 and nuclear energy by 2050.

National policies are now following suit. The Inflation Reduction Act in the United States – despite some rollbacks from President Trump in the ‘One Big Beautiful Bill’ in July 2025 – and the European Union’s Green Deal are directing hundreds of billions of dollars in public support and mobilising trillions in total investment toward clean energy, electrification and industrial decarbonisation.

While the political landscape varies by region, the trend is clear – governments are using regulation, financial incentives and carbon pricing to steer capital toward low-emissions technologies. Countries representing more than 90 percent of global GDP have now adopted net-zero targets, up from roughly 16 percent in 2019[1].

The scale of these policy-driven investment flows is accelerating the adoption of renewables, grid infrastructure, energy storage and efficiency technologies, thereby reinforcing the case for long-term structural growth.

Corporate leadership and capex reallocation

While government policy is providing the framework for the energy transition, corporate capital is increasingly driving its implementation. Some of the world’s largest companies are investing directly in renewable and low-carbon energy sources, including nuclear power, while securing long-term power purchase agreements (PPAs) to guarantee access to reliable, carbon-free electricity.

These investments are motivated by more than sustainability objectives. The rapid growth of AI, data centres and electrification are creating unprecedented demand for power, making energy security and affordability strategic priorities for businesses. At the same time, commercial property owners and industrial operators are investing in energy-efficient infrastructure. This ranges from HVAC systems, insulation and building upgrades, to lower operating costs and reduce emissions.

Together, these trends reflect a fundamental shift in corporate climate strategy. Rather than relying primarily on carbon offsets, businesses are embedding decarbonisation into their operations, supply chains and physical assets. This is creating growing demand for the technologies and infrastructure needed to support a lower-carbon economy, from energy storage and grid modernisation to advanced efficiency solutions.

Investor influence – capital allocation as a force for change

The financial sector is playing a critical role in accelerating the climate transition. Global investment in the energy transition reached a record US$2.3 trillion in 2025, up 8 percent from the previous year, with capital flowing into renewable energy, electrified transport, power grids, energy storage and other decarbonisation technologies[2]. This demonstrates a compelling investment opportunity.

ESG strategies have shifted from passive screening to active capital deployment. Instead of just picking companies that already boast low emissions, forward-thinking investors are targeting the enablers of true decarbonisation – those scaling clean power, advancing the circular economy and maximising energy efficiency.

Concurrently, shareholder pressure is intensifying. Businesses face mounting demands to lock in emissions targets, boost transparency and clean up their supply chains. In short: climate risk is now a core financial risk, and laggards are losing their competitive edge.

Climate investing does not always mean avoiding high-emissions companies altogether. Some of the most critical investment opportunities lie in companies with significant carbon footprints that are leading their industries in decarbonisation – whether by transitioning to clean energy, adopting breakthrough efficiency technologies or setting ambitious emissions reduction targets. These businesses may not be low carbon today but their role in transforming industrial processes, power generation, and heavy transport is essential to reaching net zero.

Opportunities within climate: four key sub-themes

Within its climate fund, Munro Partners focuses on four key sub-themes: clean energy, energy efficiency, the circular economy and clean transport.

Clean energy – the foundation of decarbonisation

Clean energy is essential to reaching net zero. However, not all clean energy investments are created equal. Renewables like solar and wind are now well established, but they face increasing commoditisation, intense competition and supply chain risks. For example, Chinese dominance in solar panel manufacturing has driven prices lower and squeezed profit margins, making these investments less attractive. Meanwhile, the dependence of renewables on weather conditions means they cannot meet rising energy demand alone. Regardless of this, solar and onshore wind are on the trajectory to be the more cost competitive energy technologies globally[3].

Nuclear energy, on the other hand, is seeing a resurgence as a reliable, carbon-free baseload power source. Hyper scalers, including Microsoft and Amazon, are actively securing long-term nuclear power contracts to meet their sustainability commitments and ensure a stable energy supply for their AI-driven data centres. While small modular reactors (SMRs) hold promise, their commercial deployment is still in the early stages and likely won’t scale until the 2030s.

While power generation is vital, a highly compelling investment opportunity exists in energy enablers. These companies provide the grid upgrades, energy storage and critical infrastructure required to seamlessly integrate renewable and nuclear power into the broader energy ecosystem.

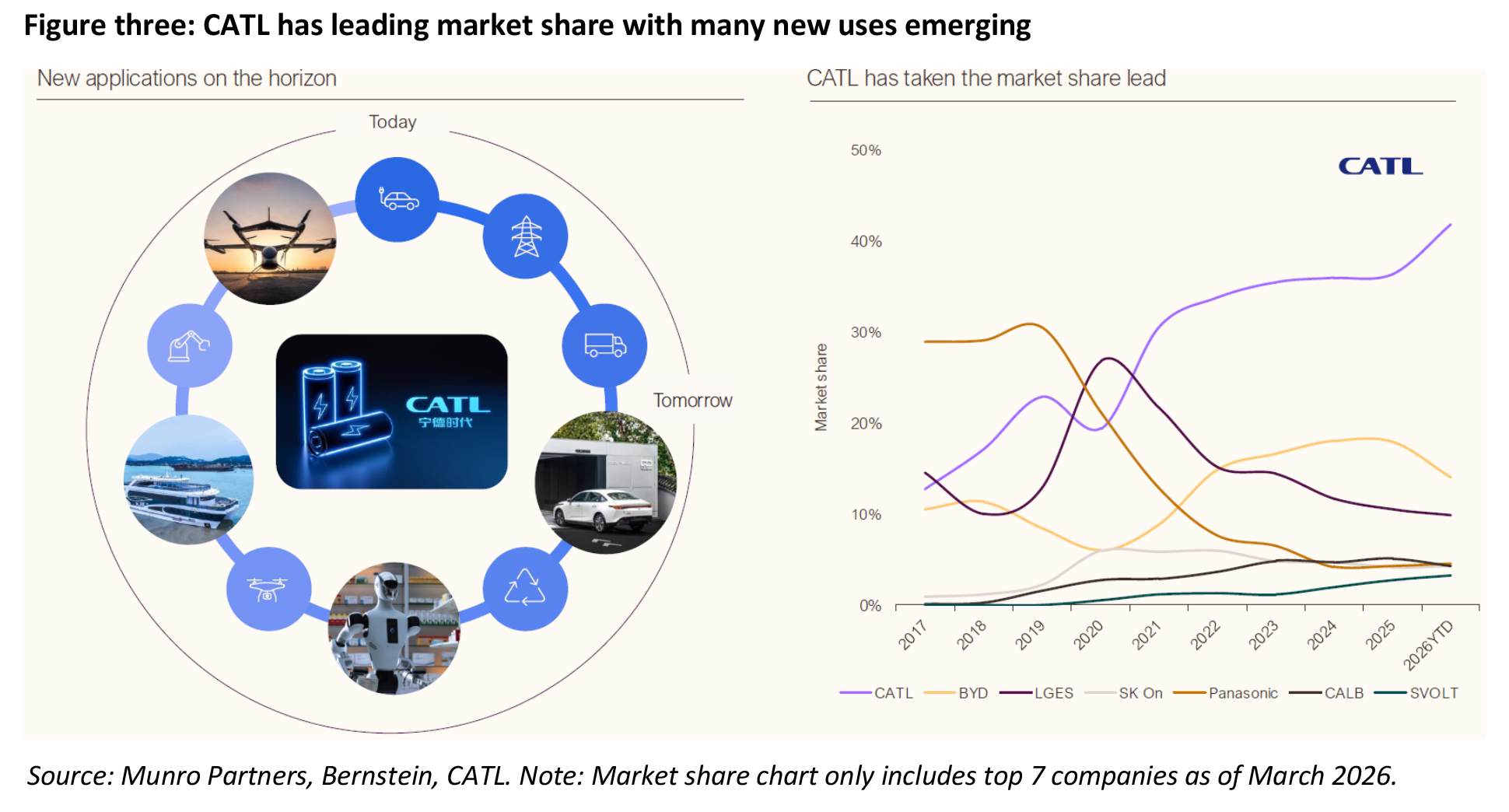

Stock story: CATL (China)

Contemporary Amperex Technology Co. Limited (CATL) is the world’s largest battery manufacturer. holding a 39.2 percent global market share in electric vehicle (EV) batteries and 30.4 percent in grid-scale Energy Storage Systems (ESS) according to 2025 data from SNE Research. To sustain growth, the company is diversifying away from pure automotive dependency into higher-margin utility-scale storage, driven by surging AI data centre energy demands, alongside electric shipping and aviation.

Energy efficiency – the unsung hero of decarbonisation

Despite being an overlooked climate asset, energy efficiency outperformed renewables in reducing US emissions over the past decade. By eliminating demand at the source rather than just decarbonising supply, efficiency solutions deliver a dual advantage: immediate cost savings and structural emissions reductions.

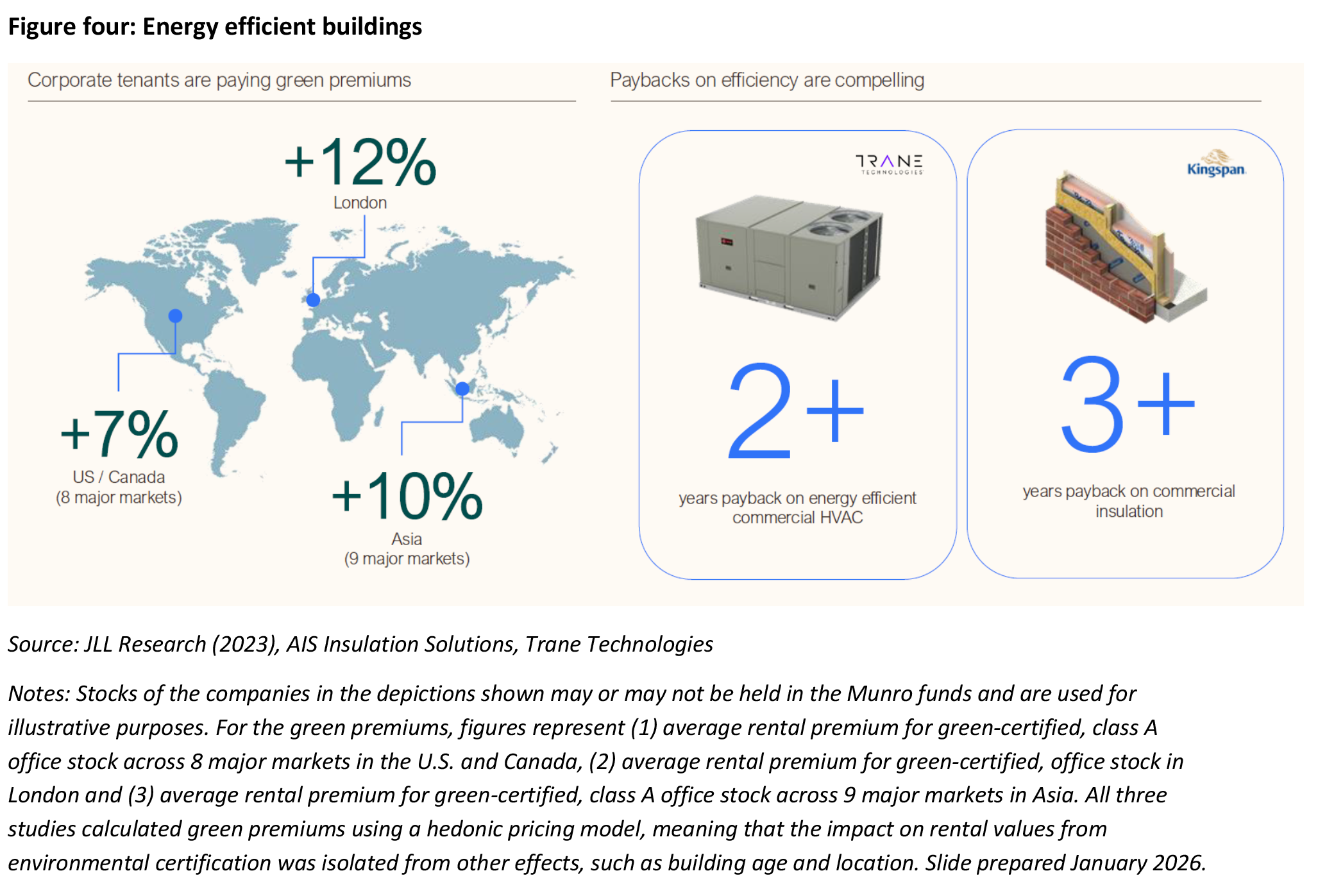

Buildings alone account for nearly 40 percent of global energy use, making HVAC systems, insulation and energy management software critical areas of investment. With short payback periods – often under two years – energy efficiency solutions represent one of the fastest-growing and most financially attractive areas of climate investment.

Industrial energy efficiency is becoming a major investment theme. Technologies such as industrial process optimisation, heat pumps and waste heat recovery are improving operational efficiency in manufacturing, logistics and data centres.

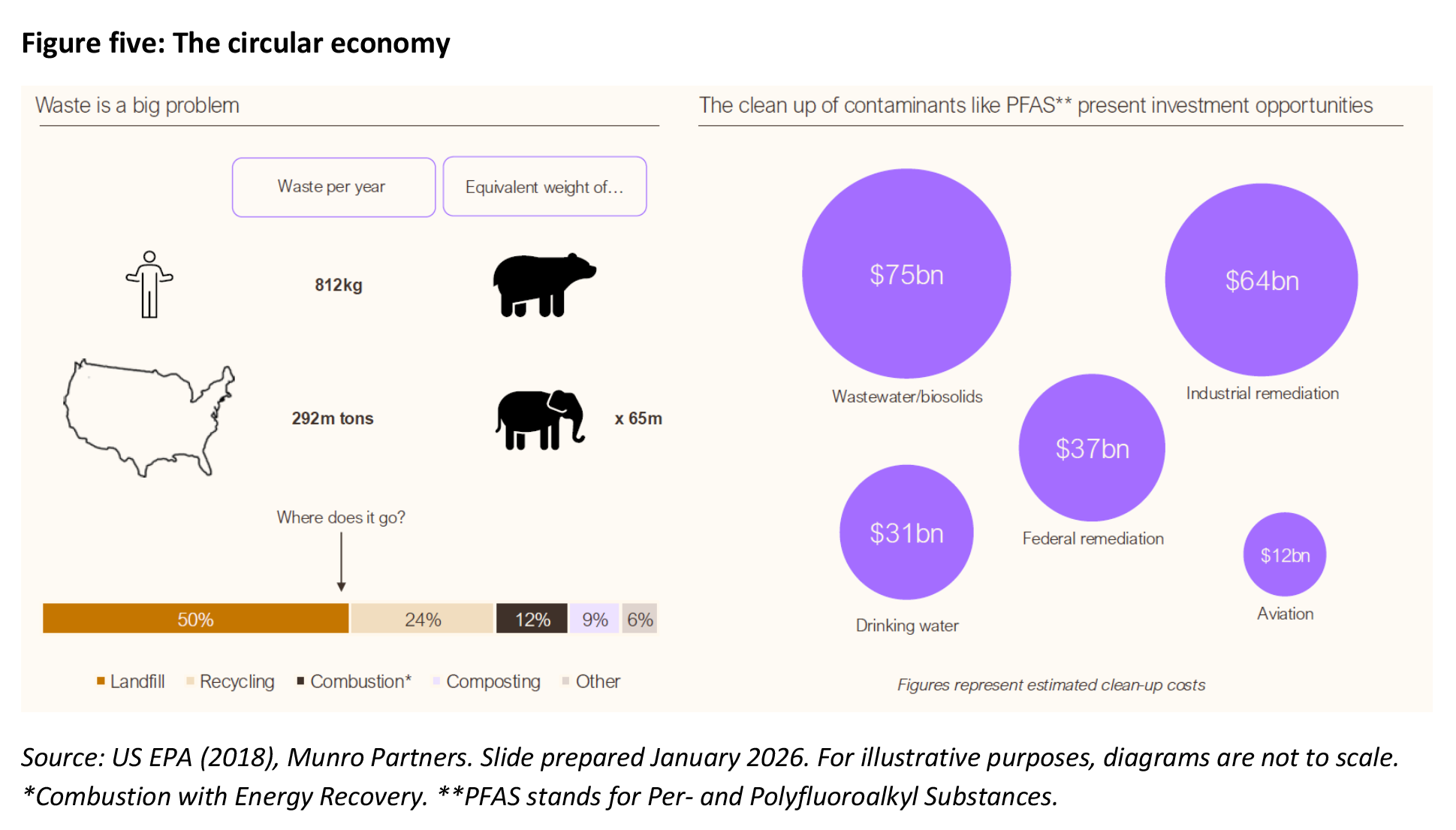

Circular economy – reducing waste, increasing sustainability

The transition to a sustainable economy is also about redefining how we use materials. The circular economy focuses on waste reduction, increased recycling and the creation of more sustainable production systems.

Plastics, industrial waste and water scarcity present some of the biggest environmental challenges today. Companies involved in waste management, advanced recycling and water treatment solutions are seeing rising demand, particularly as corporate and government policies push for higher sustainability standards in packaging and industrial processes.

Beyond traditional waste management, innovation in alternative materials – such as bio-based plastics, low carbon cement and synthetic fuels – is opening new investment opportunities. These industries are still in the early stages, but they are set to grow as global supply chains adapt to increasing regulatory and consumer pressure.

Stock story: Clean Harbours (United States)

Clean Harbors is North America’s largest environmental services provider and a primary executor of the industrial circular economy. Through its Safety-Kleen subsidiary, the company operates a closed-loop infrastructure network that processes hundreds of millions of gallons of hazardous waste and used motor oil annually. Clean Harbors collects roughly one out of every five gallons of waste oil in North America, re-refining it into high-quality base oils and lubricants that require up to 85% less energy to produce than crude oil alternatives. The company’s recycling volumes reached 1.9 million metric tons in 2024, clearing its 2030 target years ahead of schedule[4].

For investors, this asset-heavy infrastructure creates a significant competitive moat; the company leverages recurring service revenues from a diverse corporate customer base to drive compounding free cash flow, capitalising directly on rising corporate ESG mandates and supply chain reshoring trends.

Clean transport – beyond the EV

The rise of electric vehicles (EVs) is one of the most visible shifts in the climate transition, but the investment case for direct EV exposure is becoming more complex. A combination of oversupply, slowing demand and aggressive competition from China has put pressure on automakers, making investments less compelling in the short term.

However, the broader clean transport ecosystem remains an attractive investment theme. The supply chain behind EVs – including battery materials, charging infrastructure and grid integration technologies – continues to grow as electrification expands across passenger vehicles, trucks and public transport.

At the same time, low-carbon fuels, hydrogen, and sustainable aviation solutions are emerging as potential areas for future investment, particularly in industries where electrification is not yet viable.

Looking ahead: emerging drivers and innovations

Decarbonisation is accelerating, shifting climate investing beyond its first generation. Investors must look past standard renewables and efficiency to capture emerging opportunities driven by changing energy grid dynamics, new technology deployment, and shifting corporate sustainability mandates.

The rapid adoption of artificial intelligence is reshaping global energy consumption. AI workloads are significantly more power-intensive than traditional computing, and as businesses deploy AI at scale, data centre electricity demand is set to surge.

According to the International Energy Agency (IEA), total global electricity consumption from data centres is projected to roughly double by 2030, climbing from 485 terawatt-hours (TWh) to 950 TWh, accounting for approximately 3 percent of global electricity demand. Notably, power consumption from data centres specifically focused on AI is poised to triple, reaching 465 TWh by 2030 to nearly match the energy footprint of conventional data centres[5].

AI is also playing a role in energy efficiency and grid optimisation. Machine learning models are being used to improve electricity demand forecasting, enhance battery storage performance and increase the efficiency of industrial and building energy systems. While AI is accelerating the need for clean power, it is also emerging as a key enabler of smarter energy use.

At the same time, heavy industry is undergoing a structural shift. New industrial technologies are emerging – from green steel and cement to low-carbon chemical production – driven by both regulation and corporate commitments to reduce supply chain emissions. While these areas are still in the early stages, they may represent the next major investment wave in the climate transition.

The transition to net zero will fluctuate rather than progress in a straight line, dictated by changing political landscapes, technological breakthroughs and shifting consumer behaviour. Yet the macro trajectory remains undeniable. Capital allocation from both public and private sectors is steadily flowing into decarbonisation, targeted directly at upgrading energy infrastructure, scaling efficiency tech and modernising resource management.

For forward-looking investors, the climate transition has transcended ethical necessity to become a structural economic theme defining the 21st century. This systemic shift is already reshaping global industries and is unlocking substantial value across energy, transport agriculture and finance. Driven by tightening regulatory mandates, shifting consumer preferences and institutional capital favouring sustainable assets, the financial momentum behind decarbonisation will continue to compound.

Take the FAAA accredited quiz to earn 0.5 CPD hour:

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: General (0.5 hrs)

ASIC Knowledge Requirements: Economic Environment (0.5 hrs)

please log in to start this quiz

———–

References:

[1] https://zerotracker.net/

[2] BloombergNEF, Energy Transition Investment Trends 2025

[3] Wood Mackenzie, Global competitiveness of renewable LCOE continues to accelerate

[4] https://resource-recycling.com/plastics/2025/09/24/clean-harbors-hits-2030-recycling-goal-early/

[5] Key Questions on Energy and AI, International Energy Agency, April 2026

The information included in this article is provided for informational purposes only and is general advice only. It does not take into account an investor’s own objectives. The information contained in this article reflects, as of the date of publication, the current opinion of Munro Partners and is subject to change without notice. Sources for the material contained in this article are deemed reliable but cannot be guaranteed. We do not represent that this information is accurate and complete, and it should not be relied upon as such. Any opinions expressed in this material reflect our judgment at this date, are subject to change and should not be relied upon as the basis of your investment decisions. All reasonable care has been taken in producing the information set out in this article however subsequent changes in circumstances may occur at any time and may impact on the accuracy of the information. Neither Munro Partners, GSFM Pty Ltd, their related bodies nor associates gives any warranty nor makes any representation nor accepts responsibility for the accuracy or completeness of the information contained in this article.

CPD Quiz

The following CPD quiz is accredited by the FAAA at 0.5 hour.

Legislated CPD Area: General (0.5 hrs)

ASIC Knowledge Requirements: Economic Environment (0.5 hrs)

please log in to start this quiz

———–

References:

[1] https://zerotracker.net/

[2] BloombergNEF, Energy Transition Investment Trends 2025

[3] Wood Mackenzie, Global competitiveness of renewable LCOE continues to accelerate

[4] https://resource-recycling.com/plastics/2025/09/24/clean-harbors-hits-2030-recycling-goal-early/

[5] Key Questions on Energy and AI, International Energy Agency, April 2026

The information included in this article is provided for informational purposes only and is general advice only. It does not take into account an investor’s own objectives. The information contained in this article reflects, as of the date of publication, the current opinion of Munro Partners and is subject to change without notice. Sources for the material contained in this article are deemed reliable but cannot be guaranteed. We do not represent that this information is accurate and complete, and it should not be relied upon as such. Any opinions expressed in this material reflect our judgment at this date, are subject to change and should not be relied upon as the basis of your investment decisions. All reasonable care has been taken in producing the information set out in this article however subsequent changes in circumstances may occur at any time and may impact on the accuracy of the information. Neither Munro Partners, GSFM Pty Ltd, their related bodies nor associates gives any warranty nor makes any representation nor accepts responsibility for the accuracy or completeness of the information contained in this article.

Have feedback on this article? Contact Us

Earn CPD Points

CPD: The spectrum of growth

CPD: The spectrum of growthCompanies that generate strong, sustainable growth are valuable sources of long term capital appreciation in a portfolio, but these businesses are rare, difficult to identify and exist on a broad [...]

CPD: Record-keeping in financial advice – the key to compliance and consumer protection

CPD: Record-keeping in financial advice – the key to compliance and consumer protectionIntroduction The financial services regulatory framework is a key pillar of financial consumer protection. Regulatory compliance is therefore not merely about avoiding penalties, but is a critical step in building [...]

CPD: Trust and ethics in financial advice

CPD: Trust and ethics in financial adviceIn 2024, trust in financial advisers reached an all-time high. This article, proudly sponsored by GSFM, explores the inseparable links between trust and ethical practice when providing financial advice. Defined [...]