Whilst our (in my opinion) overly politically-correct industry leaders eschew the benefits of fees over “ugly” commissions let’s put an investment manager’s hat on and look at the business of financial planning. It may come as a shock to some in the mainstream press, but planners, apart from helping their clients achieve their life goals are also running a business and most do not have the luxury of regular salaries. They may also have to talk to a number of potential clients before a new client agrees to their services and fees.

The question I want to explore is what does the business of financial planning look like in 5 to 10 year’s time ? Well from a fund manager’s point of view it’s really about return on equity that the FAN (Financial Advisory Network) can generate, as it is with any business.

The big question

Ok, let’s “compare the pair” – Assume an hitherto unknown crazy relative (lets call him Uncle Alfie) has left you $50m in his Will with the requirement that you can only spend it in one of two ways :

Option 1. Develop a holistic financial planning planning FAN business

Option 2. Develop a new, low cost predominantly Superannuation based platform business sold direct to customers but employing a limited advice model.

Alfie says your decision should be entirely rational, based on the long term return on equity of each alternative, rather than on you personal beliefs or motivations. Furthermore dear departed Alfie has specified you must answer this in a few words to the executor in order get the $50m – you must also give an answer today to get the dough.

An answer

To the Executor of Uncle Alfie’s Estate – thanks a million for the $50m. I’ve done a lot of reading and have waited until the election to give you my initial response. Without going into great detail this advice industry is amidst some seismic changes and after listening to everyone I could I see there are two forces that will govern this decision.

Firstly the Government is going to place advisers with a stricter fiduciary responsibility. Now while they sort of have that now and some tell me this is no big deal I think it is. The greater the fiduciary responsibility the more the power and revenue source shifts from the FAN to the individual adviser (who essentially has the relationship with the client). In the extreme sense the the FAN model (Option 1) could still make money but my model says that I make the most with asset based fees and in an extreme fiduciary World I’m concerned that I may only receive a portion of the fees in return for a lot of FAN responsibility. If all FANs have to offer all the best options for every client I’m also concerned about my value-add to get an army of advisers working with me. But as most things in life it is a question of degree – how far will this new Shorten fellow go ?

The next decision point comes in my ability in Option 1 to package products to be “sold” by my holistic advisers.

Basically I have found out that the FAN’s revenue model is based on a cut of the adviser fee (or commission) and a lot seems to come from products, including platforms (although some FANs call them services). Regardless of what these products and services are called they’re a big part of the revenue model for Option 1. Now some advisers seem happy to play the current game and continue to support the products that the FAN packages but there is also talk of banning rebates and product and service packaging may be much harder to do in the future.

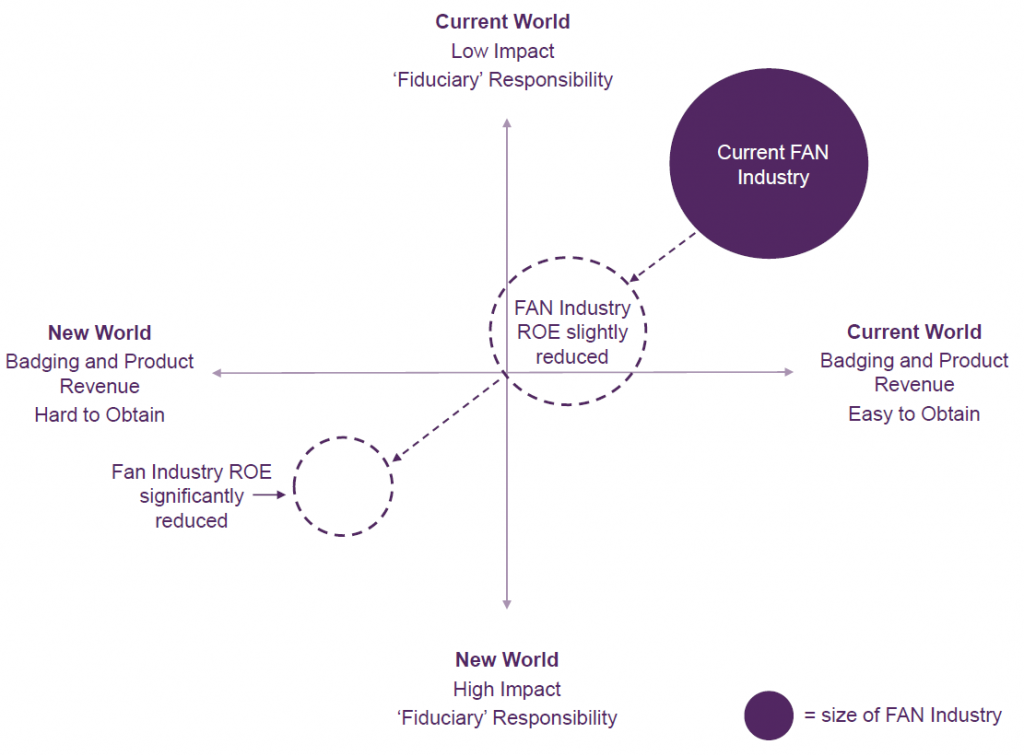

I’ve even put my decision dilemma in a chart. If the advice industry stays more like it is today (shown as the Option 1 bubble on the chart) – perhaps a bit smaller and with more restrictions then Option 1 looks good as most people need good holistic, un-biased advice. On the other hand the industry bubble could move further to the left bottom quadrant (shown as Option 2) with very heavy fiduciary and product packaging requirements restricting the ROE potential for the FAN and shrinking the industry with less FANs willing to invest.

If I didn’t have to make a decision today I’d probably back both horses (ie build and promote a low cost super fund and have a dabble in holistic advice)