When we look back over the last 12 months probably the most surprising aspect of the 2014 financial year is the fact that the status quo in markets has been maintained in terms of price action and money flows.

Historically low government bonds and property yields, equity prices that continue to edge higher impervious to any geopolitical news, such as the war in Crimea, and a local currency that sustains itself at high levels despite the fact that export prices have now contracted by 30 to 40%.

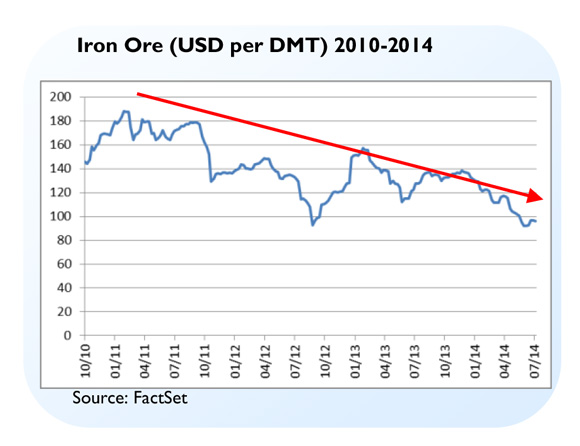

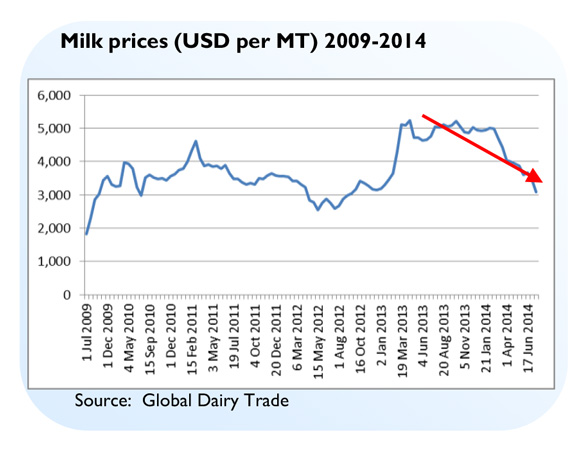

The charts below highlight iron ore in Australia and dairy prices in New Zealand.

Further, there is very low volatility and other risk metrics seem benign as we approach a phase of increasing long-term interest rates as QE programmes start to wind down and China enters a period of lower growth. It appears that the monetary authorities have becalmed markets.

CBOE Volatility Index (VIX) 2007-2014

Despite this, there is no doubt that the tide is in fact at a turning point. The price action of different asset classes and industry sectors we have witnessed over the last few years is unlikely to be repeated going forward and will likely be very different over the next five years

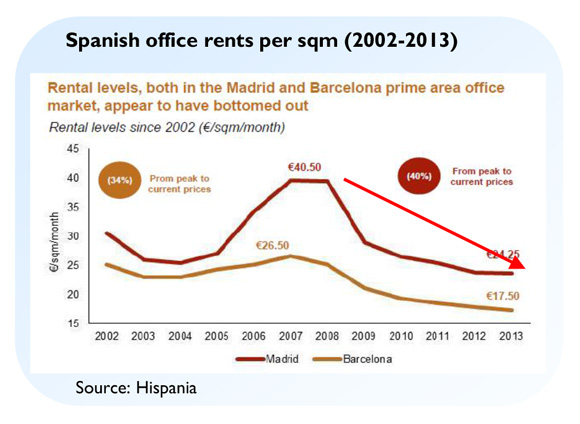

This thought process is reflected in the composition of PM CAPITAL’s equity portfolios where we have sold down a number of positions over the last twelve months, with a view that opportunities to redeploy capital would be provided at some future point in time. The basic framework we employ at PM CAPTIAL has not changed, as we firmly believe that the risk reward from owning a business is far superior to that of owning government bonds, property or cash. How superior is difficult to determine because we have an abnormally low level of global interest rates, while the valuation discrepancies in Australia are limited, which combined with the elevated currency and the minimal offshore diversification by domestic investors, would favour the perusal of international equity opportunities. The investment opportunities we are finding most interesting in global markets at present is the evolving recovery in property prices that were disseminated by the Global Financial Crisis, originally in Las Vegas, but recently we have also made investments in Ireland and Spain. There is no doubt that valuations have in fact recovered, however they are still operating under industry conditions that are well below normalised levels and there is a strong prospect of solid earnings growth looking forward, which will drive further valuation expansion. The US housing market has recovered, yet yearly sales are still at least a third below normalised trends. Spain and Ireland are additional examples of the further recovery in property prices. Ireland bore their medicine early and is further advanced in the process, but what we have seen over the last 12 months is a decent recovery in rental levels– office rentals and housing prices in Ireland. A considerable amount of foreign money is streaming into the market and prices are beginning to bid up. Spain is lagging in the process, yet we expect since bottoming late last year, combined with considerable foreign capital starting to flow in, arbitrage opportunities are emerging.

We are also attracted to a number of consumer branded companies, Google, Heineken and Anheuser however price action has not afforded us the opportunity to add to this mix, yet we believe if we are patient some of the businesses we are finding will experience headwinds in terms of near term earnings, and that will create some short term disappointment, which investors will be able to take advantage of.

By Paul Moore, Chief Investment Officer, PM CAPITAL