Introduction

For Investors seeking the most tax effective investment vehicles there are a number of choices. For many, superannuation may work very well, for some high net wealth investors, they may seek greater diversification and flexibility and often look to other structures to build wealth.

Many turn to company structures, setting up private companies to hold investments. Earnings on the funds held within such a private company are taxed at the company’s rate of 30%.

Ultimately investing in a company structure may only be a tax deferral mechanism. Eventually funds paid out of the company will be taxed at the investor’s marginal rate at the pay-out date. In the case of high net worth investors, it’s probable that the marginal rate at payout date will often be higher than the company tax rate.

So while a company structure may offer increased flexibility, it is not without its limitations. Aside from the tax payable, there may be other requirements that that need to be considered.

- Capital gains tax reporting or compliance is required.

- The company structure offers little protection from creditors following a bankruptcy event.

- Estate duties may be payable if the investor dies, at a loss to the surviving beneficiaries.

What if there was another alternative investment vehicle with less of these limitations? What if that investment structure provided the additional investment flexibility to effectively compliment a superannuation fund but did so with greater simplicity, and also potentially reducing the tax liability of the investor over the long-term (10 years or more)?

Introducing Investment Bonds.

For high-income earners, investment bonds are a tax effective alternative investment vehicle. If funds can remain invested for at least 10 years, then personal tax obligations are permanently removed after year 10. Bonds can thus provide a significant tax saving, especially if the investor is paying tax at the highest marginal rate.

How are investment bonds taxed?

The taxation of an investment bond falls under company tax rules. Tax on earnings is payable at the company tax rate, currently 30%. In contrast, the top marginal rate on personal taxes, inclusive of the Temporary Budget Repair Levy and Medicare Levy, is 49%. If an investment bond is held for at least 10 years, then earnings do not need to be included in the investor’s tax return. This means tax within the bond is capped at the company tax rate of 30%. While this may be one of the advantages of investing in a Bond, compared to a company structure, there are other tax advantages worth considering.

- If a withdrawal is made within the first 10 years, the earnings are included in the investor’s personal tax return (only a portion is included in the ninth and tenth year) and a 30% tax credit applies. However, unlike a company where the grossed-up dividends are included as taxable income, only the net after-tax income received from an investment bond is taxable.

- If the Bond proceeds are withdrawn due to the death of the life insured, neither the beneficiary nor the estate needs to pay any further tax.

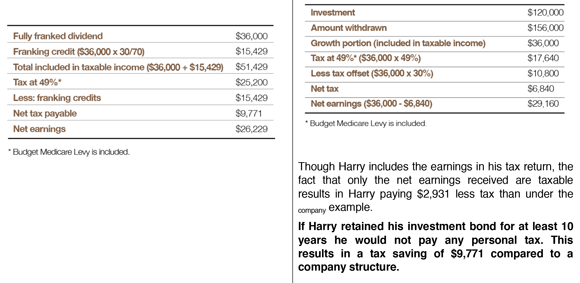

The differences between these two investment structures are outlined in the example below. Consider the following:

Features of investing in an investment bond structure

While the investment bond offers a tax advantage alternative to the company structure, it also offers many more key benefits that make it a viable complement to an investor’s portfolio. Here are our top 7.

Flexible investment options

Investment bonds allow clients to access many asset classes and provide a market-linked investment vehicle to help meet investment goals.

No limit on the investment amount

There is no limit on the amount that can be invested to establish an investment bond. Investors can also make subsequent investments up to maximum of 125% of the previous year’s contribution without restarting the 10-year period. Investors can choose to start new investment bonds if higher amounts are to be invested.

No excess contributions tax

Investment bonds can provide a tax effective means of investing and avoid excess contributions tax that may otherwise apply in superannuation.

Flexibility

Investment bonds give investors the flexibility to access funds at any time, which can act as a hedge against the restricted access for superannuation.

Capital gains tax simplicity

Investment bonds provide simplicity as earnings are automatically reinvested in the bond. This means reinvestment dates do not need to be tracked for capital gains tax purposes. Investors can also switch between investment options without triggering personal capital gains tax.

Transfer of ownership

The ownership of the investment bond can be easily assigned or transferred at any time. The original start date is retained for tax purposes. This may not be achieved within a company structure without creating tax liabilities.

Bankruptcy protection

Investment bonds may offer protection from creditors in the case of bankruptcy (subject to certain rules), which may not be provided through a company structure.

Conclusion

If your clients are looking for alternatives to invest in a tax effective manner, then investment bonds provide a range of advantages to investors seeking more flexibility and diversification to complement their superannuation.

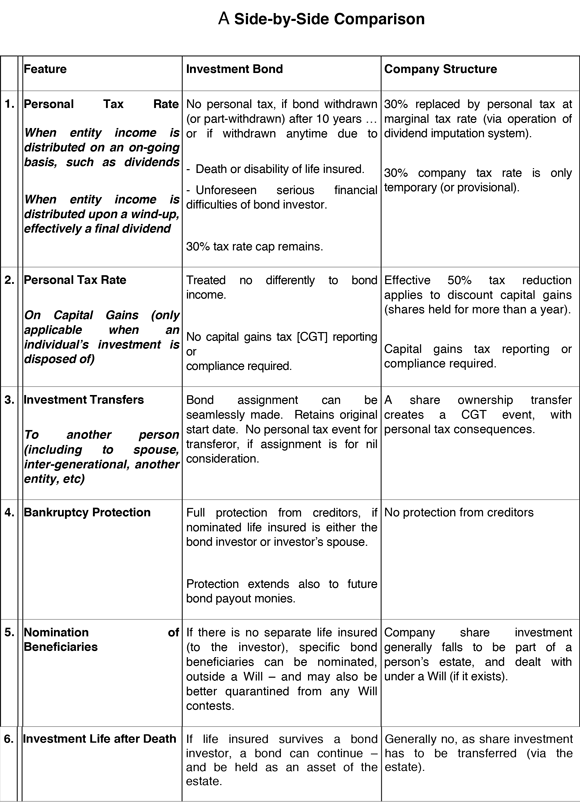

When compared to company structures, investment bonds can provide significant advantages, especially if funds are invested longer than 10 years. The table which below gives a good side-by-side comparison.

———-

This paper contains general information and is intended as an informational guide for financial advisers. In preparing this paper, no individual circumstances have been taken into consideration and therefore may not be applicable to an adviser or their client’s particular circumstances. Before making any investment decision, you and your clients should obtain and read a copy of the PDS of any financial product before making a decision to invest. Centuria Life Ltd (ABN 79 087 649 054 / AFS Licence 230867) (“Centuria”) is the issuer of this paper and the Centuria TaxAstute series.