Comparing Exchange Traded Bond units (XTBs) with other investments in the fixed income world. In this paper we look at how XTBs and Hybrids compare and contrast.

- The first Classes of XTBs commenced trading on ASX on 14 May 2015.

- Each Class of XTB offers exposure to the returns from a different senior corporate bond issued by some of the largest ASX listed companies, or their subsidiaries.

- XTBs are not a fund investment, they are individual securities trading on ASX, each based on a different bond. XTBs pay out 100% of the underlying bond’s coupons and principal.

- XTBs, exchange-traded bond funds (ETFs), bond managed funds, hybrids, term deposits and Cash all have their place in a properly diversified portfolio. However, the differences between them can matter as much as the similarities.

- XTBs relate to senior corporate bonds, which are fixed income investments. Hybrids have some fixed income features, but also have equity features that tend to become more evident when equity markets undergo significant downturns or high volatility.

- Fixed income investments such as bonds and XTBs are generally negatively correlated to equities. In strong market conditions hybrids can tend to be correlated with fixed income, but they tend to become more positively correlated with equities when conditions deteriorate.

- In a portfolio sense, hybrids sit between fixed income and equity. As a result some advisers do not consider them part of the fixed income asset class and others do.

- At the very least advisers and investors need to understand how hybrids work when making comparisons between them and bonds and XTBs for portfolio purposes.

Hybrids & XTBs compared

Like XTBs, hybrids are mostly, but not always, ASX traded securities. There is a wide variety of hybrids and making general comparisons is difficult. Some hybrids have more equity features than others, and some are more debt-like. COMMON FEATURES OF HYBRIDS All hybrids have some common features. They are neither true fixed income, nor pure equities, but a combination of both. All hybrids can be converted into equity in particular circumstances. Conversion is generally at the discretion of the Issuer, however for some, it can be at the direction of Australia’s prudential regulator APRA. If they do covert, it’s likely to be at a time of market stress for the Issuer, which means it’s highly unlikely to be at a time, or price that suits the hybrid investor. That’s a key rationale for the very existence of hybrids – in times of stress, companies have debt-like funding that acts as a buffer by turning into equity. Like bonds and XTBs, hybrids generally have a specified distribution, dividend or coupon that can be fixed or variable. Franking credits are often available. For some hybrids this payment is discretionary and the Issuer has a right not to pay the coupon, which then limits the issuer’s ability to pay other dividends. Most hybrids will not have a definite maturity date like a bond or XTB, but rather they have a ‘call date’, on which the issuer may end the hybrid and pay back the capital. Potentially some hybrids can be perpetual (similar to equities).

Common features of senior corporate bonds

Senior corporate bonds are far less complex. Their basic structure is that they are a tradable form of loan to the Issuer. They can never convert into equities. The maturity is fixed, and the bond’s coupon, whether fixed or variable, is set at the outset and the issuer is obliged to pay it. It follows that XTBs that relate to senior corporate bonds have the same general economic features as the bonds they relate to.

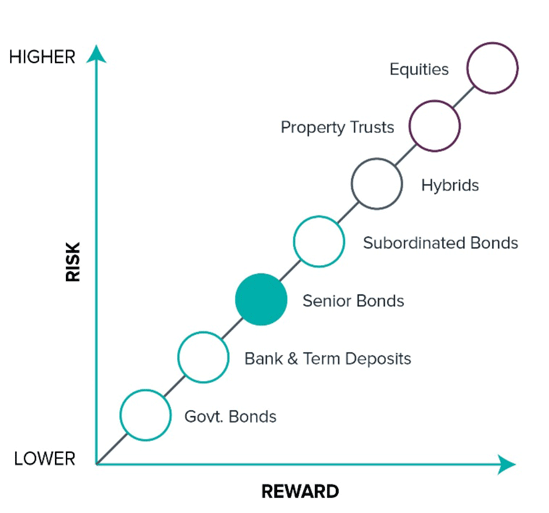

The Corporate Capital Waterfall

The chart below shows where senior bonds and hybrids sit relative to each other in a corporate capital waterfall diagram. The higher up on this curve – the greater the risk and the return of the security. In Yield terms, senior bonds sit somewhere between Term Deposits (for bank issuers) and hybrids from the same or similar issuers. XTBs are lower yielding securities than hybrids because the bonds they cover are more senior than hybrids, and they enjoy the benefits of bonds they cover ranking ahead of hybrids in a default or wind-up situation, which means the risk/return is lower.

Hybrids: Complex & Changing Nature

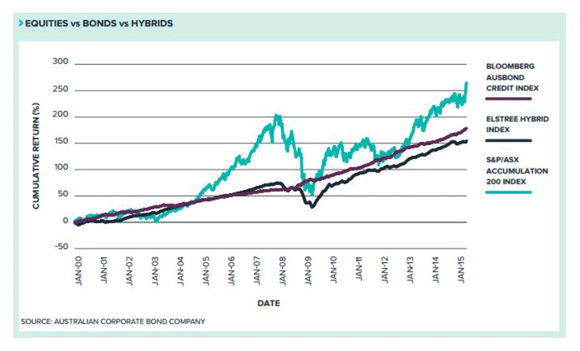

The market behaviour of hybrids can change over time. They can behave more like bonds, or more like equities depending on financial market conditions. When market conditions are stable or strong, the fixed income features of hybrids should be more apparent – they will pay defined income and will have lower market volatility and lower correlation to equities. But when market conditions deteriorate, the design of hybrids may result in the equity features becoming more evident and they are likely to have increased price volatility as concern increases they may convert into equity on terms that will be disadvantageous to the hybrid investor. Taken to an extreme, as happened during the GFC, hybrids traded much more like equities as the perceived risk that they would convert escalated. The relatively low correlation to equities during good times was replaced by direct positive correlation to equities. This feature means they are inherently more complex than corporate bonds and the XTBs that track corporate bonds. The chart on the next page shows how this played out in practice. It shows equity, hybrid and corporate bond indices from 2000 to February 2015 starting from a common base. From late 2007 to early 2009, through the most difficult part of the GFC, the Elstree Hybrid Index (price performance of hybrids on ASX), fell by over one quarter from peak to trough. The equity features of hybrids were thrown into relief and their performance became more closely correlated to equities than to bonds. Following the worst of the GFC the Index subsequently recovered quickly.

Hybrids: fixed income or growth?

Broker and adviser research and resulting advice and model portfolio construction seems to be split on this question. Based on the feedback provided to Australian Corporate Bond Company (Securities Manager of XTBs) by financial advisers, the trend in 2015 seems to be towards moving hybrids towards the growth part of the portfolio. While hybrids have been strongly supported in the market, the equity correlation feature of hybrids and resulting volatility creates a basic problem for investors looking to:

- Properly diversify their portfolio across different asset classes, and

- Select asset classes that are negatively correlated to equities and vice versa, particularly if their portfolio is already fully weighted or overweight equities as so many are in Australia.

Asset class correlation and volatility

Looked at in the light of asset class correlation: In tough times you really need an investment to behave as fixed income should, and be negatively correlated to equities. Unfortunately with hybrids this is the exact time their fixed income features fall away, and their equity features will roar into life, leaving investors with a security that is largely correlated with equities. If fixed income is your portfolio’s protection against the volatility of equity market downturns, then you shouldn’t view hybrids as part of that protection. This isn’t to say hybrids are a bad investment product. They’ve been a great investment for many investors and it would be like saying equity is a bad investment just because shares go down as well as up. It doesn’t mean the Issuers of hybrids are about to fall over and you’ll lose your capital. It doesn’t mean the Issuers of hybrids won’t pay the coupons or dividends.

Understand the characteristics of hybrids

What it does mean is that investors need to understand that this is exactly what hybrids are designed to do, and will do in difficult market circumstances. They play a role in the capital structure of corporates, particularly banks who issue the most by dollar value, by acting as a buffer to protect more senior debt and deposit holders from the shock of a significant market downturn (by the hybrid converting into equity). The volatility that impacts returns for hybrids is a natural consequence of their design features. Having observed the behaviours of hybrids in the GFC, more and more brokers and advisers are moving hybrids from the fixed income or defensive part of the portfolio, into the growth or equity part, and looking for other more traditional forms of fixed income investments for the defensive part of the portfolio.

Corporate bonds – Negatively correlated to equities

By contrast, the performance of senior corporate bonds versus equities during the GFC as shown in the chart is what’s expected from fixed income investments: corporate bonds were largely negatively correlated to equites in price terms when the market went through the worst of the GFC. This is what portfolio diversification theory is looking for – asset classes that are generally negatively correlated against each other in capital performance, so that overall portfolios are protected when one asset class becomes stressed.

Diversification is the key

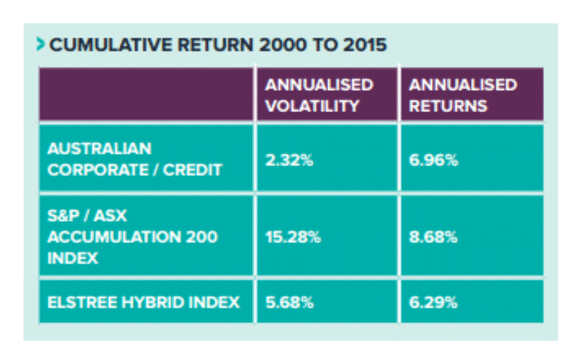

A key take away message from this chart is that a properly diversified portfolio across fixed income and equity asset classes would have probably withstood the worst of the GFC better than a portfolio with all its eggs just in the equities basket. Over the 15 years of this analysis: The equity index as expected outperformed both the bond index and the hybrid index with annualised returns of 8.68% The annualised return of the bond index was 6.96%, while the Hybrid index was 6.29%. Even though senior bonds generally have lower Yields than the equivalent term hybrid, the annualised returns from hybrids suffered during the period in question, because of the downturn during the GFC. The annualised volatility of the equity, hybrid, and bond indices over the period was 15.28%, 5.68% and 2.32% respectively. Volatility is a technical measure of how much prices and therefore returns move around over a period. As the name suggests, the higher the volatility, the riskier that asset is for your portfolio. Higher volatility, or risk is the price you need to pay to get the higher returns equities can often deliver. Corporate bonds, and XTBs over them have lower returns than equities, but they also come with much lower volatility plus a negative correlation to equities, which is why most advisers would recommend balanced portfolios mixing equities with fixed income assets like corporate bonds, XTBs or term deposits. Hybrids have fixed income features in strong market conditions, but by design will exhibit equity features when market conditions deteriorate. Their annualised volatility during the period in the chart was higher than corporate bonds, for what turned out to be lower returns.

To view the range of available XTBs visit xtbs.com.au/available-xtbs

———–