Even before the correction in China’s A-Shares market, a number of investors expressed to us scepticism about our positive outlook for the renminbi (RMB). Some even saw devaluation as a possibility. For a variety of reasons, we continue to see the currency appreciating.

In the aftermath of China’s A-Shares correction, many investors may be more concerned about the potential for further instability in the country’s financial markets than mindful of areas of relative calm. One such oasis is the bond market, which behaved as bond markets are supposed to do in an equities sell-off, providing a safe haven for investors who suddenly became risk-averse.

Another is the currency market. Both the offshore (CNH) and onshore (CNY) renminbi remained essentially flat relative to the US dollar, with the Daily Fix being kept stable, indicating that policy makers wanted to keep the currency steady.

A number of investors we spoke to before the correction were sceptical as to how long the RMB could stay the course, given China’s slowing growth and multiple policy challenges. That scepticism has only intensified since the market pullback, amid broader doubts about how effectively China is pursuing its goal of becoming a more open, market-oriented economy.

We think such concerns are understandable, but that they need to be kept in perspective.

SDR is a sideshow

One example of what we regard as a distorted perspective is the extent to which the market correction and the government’s attempts to bring it under control are, somehow, seen as evidence that China’s economic and financial reform programme is in danger of being derailed.

According to at least one commentator, the government’s efforts to stabilise the market raised questions as to whether it would allow the RMB, once the currency reached full convertibility, to trade freely during times of market volatility.

Another currency-related example of distorted perspective, in our view, is the tendency to see the eventual inclusion of the RMB in the Special Drawing Rights (SDR) basket of the International Monetary Fund (IMF) as a measure of the currency’s progress towards full internationalisation.

For some time now, the IMF has been saying that the currency’s inclusion in the basket is a matter of when, not if. The basket is reviewed every five years with the next review due later this year and a decision expected in November.

Expectations until recently were strong that the RMB would be admitted to the SDR at that point.

Since the market correction, however, those expectations have evaporated, largely on the assumption that the IMF will want to wait until clarity has returned to the outlook for China’s markets and reform programme before taking further action.

As it happens, we agree that the RMB is unlikely to be included in the SDR this November; in our view, however, the reasons have nothing to do with impressions created by the share market correction and everything to do with high-level international politics.

During September, China’s President Xi Jinping will visit the US for talks with President Barack Obama on a range of topics, including bilateral trade agreements. This is a particularly important issue for China, which has not been included in the Trans-Pacific Partnership trade agreement being negotiated between the US and several Pacific Rim countries[1] .

Given the degree of influence that the US and its allies have within the IMF, we believe it’s likely that the RMB’s inclusion in the SDR basket will be held over until next year, or at least until after the US-China talks reach an outcome that both sides can support.

The symbolism of this would be useful both to the US, allowing it to be seen as having a degree of leverage over China (the implication being that SDR inclusion lies within its gift), and to China (by giving the RMB implicit US endorsement in the eyes of the rest of the world).

Incidentally, the value of RMB inclusion in the SDR is largely symbolic anyway, in our view, and attempts to present it otherwise (by suggesting that a delayed inclusion reflects negatively on the IMF’s view of China, for example) are another instance of what we regard as a distorted perspective.

China eyes the endgame

Our own perspective on the RMB is shaped by its fundamentals and our conviction that China’s reform programme—which we always expected would be buffeted in the short-to-medium term by setbacks such as market corrections and corporate defaults—remains on track for the long term.

The progress that the government has made in internationalising the currency, for example, illustrates the consistency in China’s policy thinking and implementation. The SDR issue has some relevance here: in 2010, the IMF considered but rejected the RMB for inclusion on the grounds that the currency wasn’t traded widely enough.

Today, partly as a result of the government’s vigorous promotional efforts, the RMB has become the second most used currency for documentary credit transactions (such as letters of credit), ranks fifth as a world payment currency and is the world’s sixth foreign exchange currency. We expect it soon to overtake the Japanese yen, one of the four components of the SDR, as a world payment currency (Display 1).

This alone could be enough to warrant the currency’s inclusion in the SDR, in our view (and it’s worth noting that, in May, the IMF said that the RMB was no longer undervalued—a clear signal that the organisation was favourably disposed towards the currency’s inclusion in the SDR).

Another criterion for inclusion, however, is “full convertibility”, which the currency has yet to achieve. Progress here depends on the liberalisation of China’s capital account—a process the government has escalated. In February, for example, capital account restrictions were removed for companies and banks in the Shanghai free-trade zone, freeing them to raise funds offshore, and the People’s Bank of China has indicated that full liberalisation could occur this year.

The impetus for liberalisation is building rapidly, as indicated by the growth in two-way cross-border investment encouraged by the Qualified Foreign Institutional Investor and Renminbi Qualified Foreign Institutional Investor programmes, the Qualified Domestic Institutional Investor schemes and Shanghai-Hong Kong Stock Connect—a system for trading between the onshore and offshore exchanges (soon to be followed by a system linking the Shenzhen and Hong Kong exchanges).

While these programmes are still subject to investment quotas, the quotas are constantly being increased and in time will be removed entirely. Indeed, in a dramatic development this month China announced that central banks, sovereign wealth funds and supranational organisations could now access the Chinese bond markets directly and without quotas—effectively fully opening up the capital account.

Not only is access to markets being improved, new investment opportunities are being created. As part of its push towards a more open economy, China is restructuring its state-owned enterprise (SOE) sector with a view to privatising parts of it. It’s also pushing local governments into refinancing their bank loans in the domestic bond market.

One effect of this is to reduce banks’ exposure to local governments, and so reduce systemic risk; another is to create a new municipal bond market. This sprang to life in June this year with RMB734 billion of issuance and is expected to be capitalised at around RMB6 trillion by the end of next year.

For China, the end game of capital account liberalisation is the country’s full inclusion in global investment indices. As with full currency convertibility, the country is not quite there yet, but is on its way: in May this year, for example, index provider FTSE Russell began transitioning China A-Shares into its global benchmarks.

Monitoring unemployment

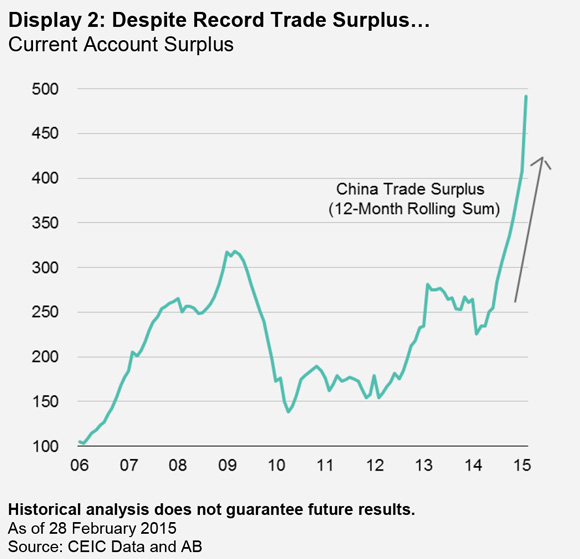

To achieve these policy goals, China self-evidently needs to maintain some stability in the currency, and this alone is a strong argument against near-term volatility or depreciation, in our view. The currency’s fundamentals make a similar point: despite a record trade surplus (Display 2), the RMB’s appreciation to date has captured only a fraction of the growth in China’s massive near US$4 trillion of foreign exchange reserves (Display 3).

Our frequent conversations with policymakers in Beijing provide further grounds for regarding the RMB as riding at anchor in a sea of stability. The impression we have formed during recent discussions is that currency depreciation is unnecessary, given that China’s exports continue to perform well on a relative basis; it would also be self-defeating, as the effect would be to export deflation across the world which, in turn, would ultimately undermine China’s exports trade.

Also, as a net importer of commodities, China clearly benefits from the near-term stability and longer-term appreciation of the currency.

The one risk we see to our RMB outlook is that the currency could come under pressure if unemployment in China were to rise. This is something we would monitor carefully, particularly as restructuring of the SOE sector gets underway. To date, however, it’s worth nothing just how resilient China’s labour market appears to be: despite the steady slowdown in growth in recent years, unemployment has remained stable at around 4%.

On balance, while risks remain and more setbacks can be expected in China’s long and arduous road to becoming a modern economy, the prospects for stability and long-term appreciation in the RMB remain sound, in our view.

By Hayden Briscoe, Director, Asia Pacific Fixed Income, AB

[1] Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Singapore and Vietnam

———