Hayden Briscoe

China’s decision earlier this month to change the way in which the central parity or “fix” rate of the renminbi (RMB) is determined has been widely characterised as a devaluation designed to shore up the country’s export trade. We question this assessment, for a number of reasons.

In our view, the move is much better understood in the context of China’s continuing efforts to deleverage and reform its economy, while avoiding a hard economic landing. As a competitive devaluation, it seems to make little sense from either a structural or cyclical perspective.

By a structural perspective, we mean the changes in the policy environment related to the reform process. A key reform, of course, is the internationalisation of the RMB, as a prerequisite to the opening-up of China’s capital markets.

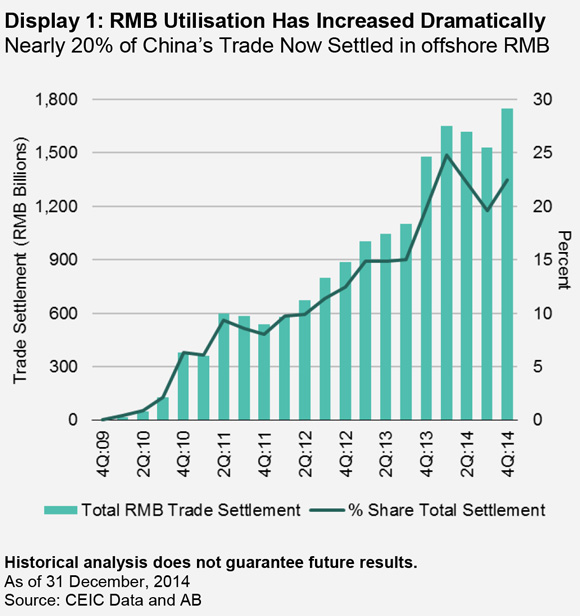

China has made great strides in this respect in the commercial arena: in the last five years or so, the offshore RMB (known as CNH and traded in Hong Kong) has become the settlement currency for nearly 20% of the country’s trade (Display 1).

The currency has yet to make the same impact in the financial sector, but this is about to change. In a little-publicised move in July, China opened its capital markets to central banks, supranationals and sovereign wealth funds—a highly significant first step in the liberalisation of its capital account.

Given that these policies are aimed at increasing global usage of the RMB—and potentially elevating it to the status of a reserve currency— it seems strange that China would choose such a moment to “devalue” and risk losing the confidence of global investors.

Devaluation would hurt, not help…

From a cyclical perspective, devaluation seems to be unnecessary. For example, while China’s exports slumped 8.3% year-on-year in July compared with a 2.8% rise in June, the drop was less severe than the double-digit contraction experienced by the country’s regional peers.

The drop did little harm to China’s balance of payments because imports are falling even more quickly than exports, leaving the country’s trade in a net positive position.

The fall in imports is attributable both to lower Chinese demand for commodities (a result of another reform, the normalisation of the infrastructure programme) and to the associated fall in commodity prices. China, as a net importer of commodities, benefits from this.

That, from our point of view, is another reason not to devalue. For years during the commodity boom, the upward surge in prices was a headwind to China’s growth. Falling prices are a boost to the margins of Chinese commodity importers, and devaluation would reduce this advantage.

Falling imports also feed the country’s record trade surplus (Display 2) which has become something of an embarrassment to China in its political relationships with its trading partners. A deliberate devaluation of the currency would only exacerbate this problem.

… And would be politically embarrassing

It would do so at a bad time, too, as President Xi Jinping is due to meet President Barrack Obama in the US next month to discuss bilateral trade. For years, the US Senate has complained that China has kept the currency artificially undervalued. To devalue now, just a few weeks before the meeting, would look politically inept at the very least.

The Chinese president has another reason for keeping on the good side of his US counterpart: China wants the RMB to be included in the Special Drawing Rights (SDR) basket of the International Monetary Fund, and President Obama’s goodwill could be helpful in that respect.

In light of these considerations, we believe that the best explanation for the adjustment in the central parity rate was the one given by the People’s Bank of China: that it was intended to close the unusually wide gap that had opened between the fix and the spot price—in other words, to bring the RMB’s valuation more in line with that of the market.

A more market-oriented currency is, of course, essential to China achieving its broad policy objective of modernising the economy and opening it to foreign and domestic private investment.

Other aids to growth

While we don’t expect the currency adjustment to make any difference to exports, our analysis suggests that China’s policy measures will have a positive incremental effect on the currency and the economy in the next few months.

The opening of the capital account to central banks, supranationals and sovereign wealth funds will benefit China’s capital inflows, in our view. Between them, these institutions are estimated to control US$20 trillion to US$30 trillion. Even if the allocations they made to China were relatively small in percentage terms, they could have a profound effect.

Supranationals in particular are key users of the SDR currency basket, and so their involvement in RMB flows is likely to increase once the currency joins the basket.

Earlier this year the central government introduced a budgetary law which forced provincial and municipal governments to reduce their dependence on bank finance and raise capital in the domestic bond market. This gave rise to the municipal bond market where issuance, since inception three months ago, has reached about RMB1.70 trillion (US$270 billion).

We expect that, once the central government announces its 13th Five-Year Plan in October, this pool of liquidity will be channelled into infrastructure and other activities which will provide a boost to the economy late this year and into 2016.

The big picture matters

One conclusion we draw from the above is that it’s as important now as it’s ever been to look at the big picture when trying to understand what’s happening in China. As one stands back from the daily machinations of the markets, it seems strange that the world has been pressing China to accelerate its embrace of a more capitalist economic model, only to reel in anxiety and confusion as the country struggles with the reality of the challenge.

A likely consequence, in our view, is that investors and financial analysts will grasp the importance of incorporating into their China research a deeper understanding of the country’s internal politics, macroeconomic cycles, cultural differences with the West and—perhaps most importantly of all—its potential impact on global capital markets.

By Hayden Briscoe, Director—Asia Pacific Fixed Income

———–