Welcome to the third in the series of papers addressing an alternate method of building property into portfolios. (Read part one here and part two here). This paper takes an in depth look at fractional investing into property – how it works, who the participants are and their roles and before closing we’ll look at the types of portfolios where fractional investing can be applied.

So exactly what is fractional property investing?

It is a technology solution that can ‘fractionalise’ ownership of any property for sale in Australia via a segregated sub-fund in which the property is individually held. In essence, an investor can buy in ‘fractions’ of a property negating the need to buy an entire property the capital or finance for which might not be available or indeed, prudent. Fractionalised investing into property sees one or more investors all contributing money in order for the Fund to acquire a property. Investors therefore own fractions of that property(s) when units in the sub-fund are issued to them, upon the purchase by the sub- fund of that property. These units represent an investor’s proportionate interest in the underlying property and their respective rights and interests are attended to by the fund manager, responsible entity and the custodian. Fractionalised property investing can be applied to all forms of property – residential, commercial, retail, industrial, rural and new developments.

In Australia, at present, the only fractionalised property investment option is the DomaCom Fund. It is an intermediated product that requires investors to go through an adviser authorised by an Australian Financial Services Licence (AFSL) holder. It’s a registered Managed Investment Scheme (MIS) and as such, it must be listed on the AFSL’s Approved Product List before it can be recommended to clients.

How does it work?

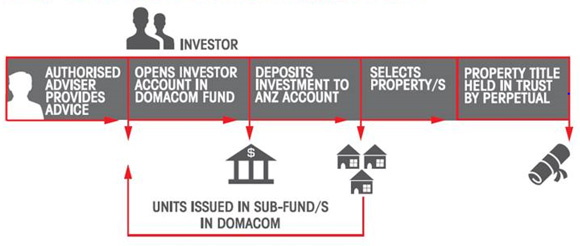

Advisers need to be ‘accredited’ in order to open client accounts on the platform and transfer cash to the cash pool. While held in the cash account the investor’s money earns interest at a bank cash rate + 60 basis points (currently 2.6%).

The next step is for the accredited adviser to liaise with a qualified property adviser to identify a suitable property(s) for their clients. When a property(s) is found, the fund manager then lists the property(s) for the accredited adviser to initiate the online book build process. That is, the property is then open for other investors to join as co-owners of the property(s).

The book build process is simply a pledge for a specific amount or contribution towards the purchase of the property. As the pledges grows the fund manager undertakes the due diligence on each property which includes a formal valuation, various property inspections and finally, the acquisition of the property(s).

When the book build is fully subscribed, the fund manager appoints a buyer’s agent to purchase the property on behalf of the Fund. If the property is successfully purchased, units are allocated to investors in proportion to their monetary contribution. The fund manager then appoints a property manager to source a tenant for the property and to carry out all future management work for the property.

Who are the participants?

The parties involved at various points in fractional property investing are:

- Investors

- Advisers

- Qualified Property Adviser (optional)

- Fund Manager

- Responsible Entity

- Custodian

- Auditor and other due diligence parties

Property Adviser

Property advisers do not sell property – they are not real estate agents. Rather, they are advocates for property buyers sourcing suitable properties measured against the parameters set by the investor and/or adviser. As such, property advisers are buyers and there is an important distinction to make between them and real estate agents who are property sellers and who are paid by the vendor. At law, real estate agents represent the vendor – not the buyer – whereas a qualified property adviser is acting for the buyer.

Investors and advisers looking to engage a qualified property adviser should look to professionals who are members of PIAA (Property Investment Advisers Association) or PIPA (Property Investment Professionals Association).

Types of investors

Fractional property investing can be applied to a wide range of portfolio situations however some of the more prominent include SMSFs seeking growth and/or income from an asset allocation to property. Arguably, there is also a place for it in the investment plans for Gen Y investors looking to gain an initial exposure to property investment without the need to buy a property outright with what, for many if not most, would otherwise involve large indebtedness.

And in an era of low interest rates, which might yet go lower, investors looking to maintain their overall portfolio income returns could look to own part of a property(s) based on yield returns rather than being over-allocated to the sector with outright purchase of property(s).

And what about liquidity?

One of the downfalls of some forms of property investment is, of course, the lack of liquidity. The liquidity crisis surrounding the unlisted property trust sector in the early 1990s underscores this point. Liquidity problems can still be found in both direct and indirect property investment such as syndicated funds which have ‘maturity’ dates with no (or restricted) facility for redemption prior to maturity. However, in the case of the fractional property investment we have developed a secondary market to provide a liquidity facility for investors wishing to exit prior to the usual expiry of the fund, which is 5 years.

The secondary market is an online buy/sell trading platform similar to an ETrade or Commsec account and enables investors to sell some or all of their units at a price of their choosing or at the prevailing valuation, subject to the availability of a buyer prepared to buy at that price.

So why use fractional property investing in client portfolios?

- The fractional model can solve the property asset allocation problem by allowing investors to purchase portions of property rather than a whole property thus avoiding single asset risk exposure;

- SMSF trustees in accumulation phase wanting/needing an asset allocation to real property for growth – property can be a strong anchor for any growth portfolio – residential is a higher growth category;

- SMSF trustees in pension phase wanting/needing an allocation to real property for income – property can be a sound anchor for income oriented portfolios – notably commercial and student accommodation pay higher yields;

- Generation Y seeking a start in property investing –fractional property investing outperforms cash rates;

- Non-SMSF investors seeking diversification in the property asset classes for similar reasons;

- Investors wanting Defence Housing, NRAS but in proportion to their asset allocation.

Like all forms of investment, there are advantages for investing in property on a fractional basis but there are also disadvantages. In the next instalment in our series, we will explore both the advantages and the disadvantages of this method of property investment.

Read part one here: Property – aspiration to fulfilment

Read part two here: Taking point on property