The Euro area in 2016: Solid growth, low inflation, easier policy

We expect the recovery to continue in 2016, but growth is unlikely to be strong enough to generate a sustained increase in core inflation. In which case, the ECB is likely to ease policy further. The major risks to this view are external, particularly in the form of weak emerging market growth. But political fragmentation is growing in Europe and merits close attention.

Although some hard data have been weak, December survey data suggest that the euro area ended 2015 on a firm footing. Shaking off weakness in France (partly related to the November terrorist attacks), the composite Purchasing Managers’ Index (PMI) matched its high for the year, while the broadly based economic-sentiment indicator (ESI) reached its highest level since April 2011. Moreover, the services component of the ESI was at its highest since October 2007, highlighting the domestic nature of the recovery.

Sustained recovery

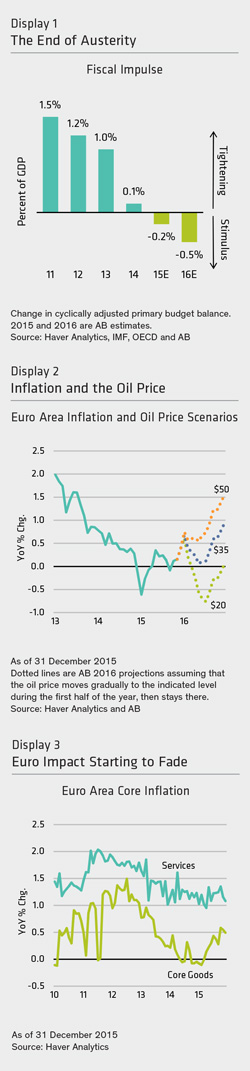

Helped by low oil prices and an increasingly supportive monetary/fiscal policy mix, we expect the recovery to continue in coming quarters. Our latest forecast (1.7%) is for growth to be a touch higher this year than it was in 2015 (1.5%). There are arguments for stronger growth, especially with fiscal policy turning overtly expansionary across the region (Display 1). But the recovery still faces important headwinds, not least in the form of weak emerging-market growth. Until the external backdrop improves, it’s difficult to see a material acceleration in the pace of euro-area growth.

Helped by low oil prices and an increasingly supportive monetary/fiscal policy mix, we expect the recovery to continue in coming quarters. Our latest forecast (1.7%) is for growth to be a touch higher this year than it was in 2015 (1.5%). There are arguments for stronger growth, especially with fiscal policy turning overtly expansionary across the region (Display 1). But the recovery still faces important headwinds, not least in the form of weak emerging-market growth. Until the external backdrop improves, it’s difficult to see a material acceleration in the pace of euro-area growth.

Subdued price

Pressures Inflation ended 2015 on a soft note, with the headline rate unchanged at 0.2%. There are two main reasons for this. First, renewed weakness in the oil price means energy prices continue to exert significant downward pressure on inflation (knocking 0.6 percentage points off the headline rate in December). Second, while the economy is recovering, growth is not yet strong enough to generate sustained upward pressure on core inflation.

Unless the oil price continues to fall, base effects should push headline inflation higher over the coming year (Display 2). But with the recovery eating only slowly into abundant spare capacity and global price pressures weak, lifting core inflation won’t be easy. All the more so, with the impact of a weaker euro on core goods price inflation starting to fade (Display 3, next page), and with service price inflation—a key gauge of domestic inflation pressure—anchored close to record lows.

More monetary easing

For the European Central Bank (ECB), weak headline and core inflation are equally problematic. The former has been below 0.5% for 18 months now. And the longer it stays there, the more worried the ECB is likely to become about a possible “unanchoring” of inflation expectations.

But even if the headline rate starts to rise, confidence that it will stay there—a key condition for ending the ECB’s asset purchase program—will only be possible if it’s accompanied by a decisive increase in core inflation. And barring an unexpectedly strong pickup in growth or further sharp drop in the euro, that doesn’t look likely. That’s why we expect more monetary easing in 2016, helping to anchor bund yields and providing further support for peripheral bond markets.

Challenges and risks

Our central case is therefore that the recovery continues in 2016, but that growth isn’t strong enough to generate a sustained increase in core inflation. In which case, the ECB will probably ease policy further.

As usual, there are a number of risks to this view. The most important of these would be a hard landing in China. The resultant economic and financial shockwaves would weigh heavily on euro-area growth, triggering a more forceful policy response from the ECB.

Domestically, the main risks are political. While no major elections are scheduled this year, political fragmentation is now a fact of life in most euro-area countries. This has led to an unstable, left-wing coalition in Portugal and is complicating the task of putting together a viable government in Spain. At the same time, Greek risks lurk in the background and the euro area would not be unaffected should the UK vote to leave the European Union. Add to this another influx of migrants/refugees from the Middle East, and it’s clear that, even if the euro area is on a firmer footing, challenging times still lie ahead.

By Darren Williams, Senior European Economist, Global Economic Research, AB

——–