The Dawson Partnership Financial Planning Remuneration Trends Survey canvasses a broad range of institutional and independently owned financial planning companies that are surveyed on an annual basis. Respondents are located Australia wide and comprise of business owners, CEO’S, GM’s and HR managers who are responsible for remuneration settings in their respective businesses.

Employee remuneration in the context of this survey is divided in to three components:

- Salary and superannuation and other benefits including the payment/subsidy of fees for relevant vocational courses, association/club memberships, parking, subsidised childcare and health care.

- Short term incentive schemes including cash bonuses.

- Long term incentive schemes that include participation in equity/shadow equity schemes.

The Dawson Partnership 2016 survey found that in terms of salary and superannuation and other benefits:

Increasing existing employee remuneration:

Of the 25% of businesses in the 2016 survey that stated that their intention was to increase remuneration:

- 56% stated that the increase was targeted primarily at employees who had met or exceeded their KPI’s

- 31% stated that the increase was targeted primarily at valued employees as a part of a retention strategy

- 13% stated that the increase was targeted primarily at those employees who weren’t being paid market remuneration.

Maintaining existing employee remuneration:

Of the 63% of respondents who stated that they would maintain employee remuneration levels:

- 69% stated that they will maintain the current remuneration settings in order to meet current and projected business targets and currently didn’t see there would be any change in their position in the 2016 year. However when asked if they would consider increasing remuneration levels if business conditions did improve beyond their current expectations 28% stated that they would consider it but only if they believed the improvement was sustainable.

- 31% stated that they were adopting a cautious approach to expenditure even though their businesses were experiencing increased business growth. 38% of these respondents expected this business growth to come from new and lower cost technology increasing productivity.

Decreasing employee remuneration

The 6% of respondents looking to decrease employee remuneration stated that this would be achieved by implementing cost reduction strategies including not replacing employees who leave their businesses and or replacing back office employees on lower level remuneration.

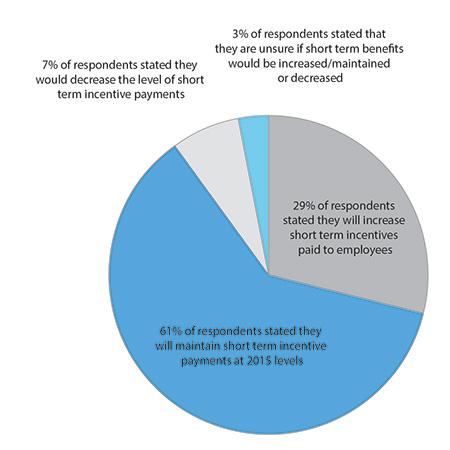

Short term incentives:

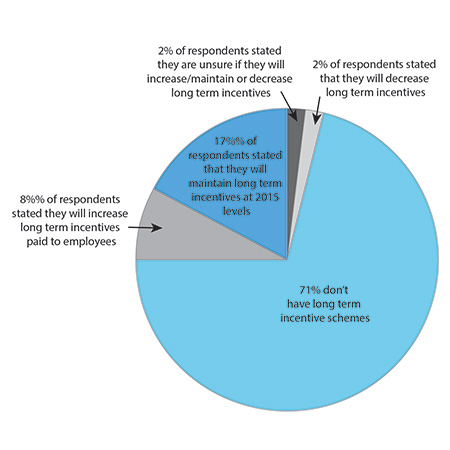

Long term incentives:

Other findings:

- 52% of employers who stated their intention is to increase employee remuneration in 2016 will do so by between 4-6%

- 44% stated they would increase remuneration in line with CPI

- 4% stated they would increase remuneration above 6%

- There was a focus on employee retention with 67% of those employers increasing remuneration seeking to offer market based remuneration to employees who had performed well and had demonstrated loyalty to them.

- 62% of those surveyed stated that they believed that that recruitment activity for high performance employees had continued to maintain the momentum from 2015 and that they were aware that their best employees were being approached by competitors either directly or by recruiters.

- 56% of employers stated that salaried financial planners with high level technical knowledge and strong communication skills were in particular demand with recruitment activity also picking up for paraplanners and support staff.

- 33% stated that they were interested in recruiting employees who are across digital technology.

While salaried financial planners employed by institutions received CPI increases or marginally below or above this level those employed by independent firms fared better, particularly those who contributed to the firm’s revenue growth with increases upward of 5%.

There was also an element of employers playing catch up. Employees who were identified as being paid below market or who had some stage during the year taken on additional responsibilities and there had been no adjustment to their remuneration were granted increases in the range of 7%-15%.

Sources of remuneration data/trends:

Respondents drew on the following sources to assist them in their remuneration decision making:

- 13% drew on market data available from web based resources including remuneration survey data released by remuneration and recruitment consultants

- 11% sourced the information from their practice manager or HR manager

- 6% had discussions with a remuneration consultant/recruiter

- 70% didn’t identify any sources of remuneration information

Positive factors cited by respondents:

- The improvement client sentiment

- The growth in business profitability

- Efficiency gains from technology

Negative factors cited by respondents:

- Continued volatility in investment markets and the flow on affect to client sentiment

- Further government changes to the legislative framework

- The impact of negative news related to personal insurance

‘We are seeing an upward trend in recruitment activity and an awareness by financial planning businesses that to retain their employees they need ensure they are remunerated in line with the market or they will face the possibility of losing them. It was clearly evident that there is more emphasis being placed on employees having high level technological skills and experience as financial planning practices refine their client communications strategies. Employees and candidates with requisite skills and experience will be the beneficiaries of higher level remuneration’.

Financial Planning businesses involved in this remuneration survey:

Ownership

- Institutionally owned – 42%

- Independently owned – 58%

Location

- Metropolitan – 74%

- Rural – 26%

Number of employees

- Between 1-10 – 26%

- 11-30 – 35%

- 31-50 – 15%

- 51-100 – 12%

- 101-200 – 7%

- 201-500 – 3%

- More than 501 – 2%